The Weekend Edition # 95

Market Recap - Rates and Yield Curves; Macro - Jobs Friday; Earnings Season - Second Quarter Incoming; The Week Ahead - Economic & Earnings Calendar; Closing Thoughts - The busy week ahead

Welcome to another issue of the Weekend Edition.

Thank you to all who’ve read and welcome to all the new subscribers this week!

Here’s what we cover:

Market Recap - Rates and Yield Curves

Macro - Jobs Friday

Earnings Season - Second Quarter Incoming

The Week Ahead - Economic & Earnings Calendar

Closing Thoughts - The busy week ahead

Let’s dive in ⬇️

Market Recap - 03 Jul - 07 Jul, 2023 📉📈

We had a shorter week with liquidity somewhat sketchy on Monday since it was a half-day for the US. We had the PMI data come out this week - Monday was the Manufacturing PMI, that slipped further into contractionary territory and Thursday was the Services PMI, coming in slightly higher than before.

Thursday also brought us the ADP Payroll data that surprised significantly to the upside coming in at 497k vs. 245k consensus estimates. This sparked off a spike in yields with the idea that the Fed now has reason to hike further.

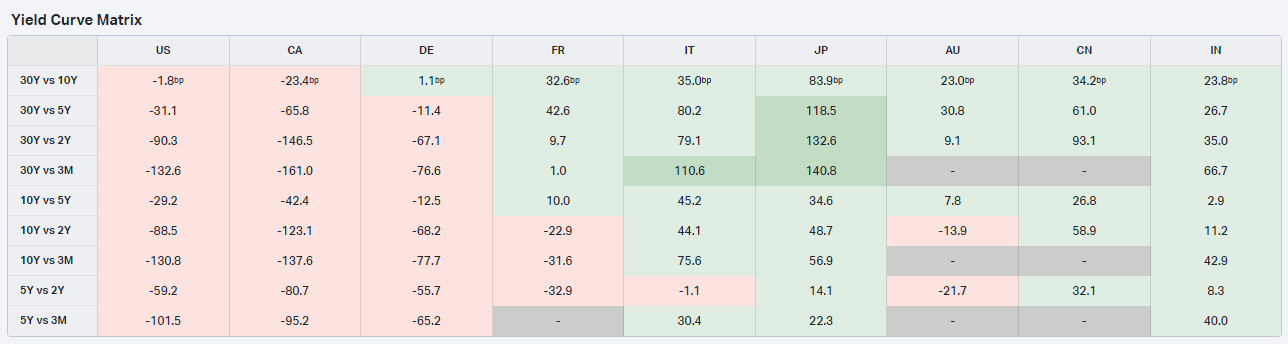

2-Year Yields crossed 5% and 10-Year Yields crossed 4%, causing a sell off in the market.

As you can see from the chart above, the 2-year still remains firmly above both the 10-year and the 30-year, with the Yield Curve remaining inverted across the curve. In fact, this is the case for both the US and Canada, and for Germany and France, at least as far as the 10s-2s are concerned. ⤵

We actually saw the markets close down for the week, on all the major indices. This certainly was a risk off week with Bitcoin down -0.55%, as well.

Commodities were a mixed bag during the week with most of the Agricultural Commodities closing lower. Oil has been looking chipper since the announcement from OPEC+ on further tightening of supply conditions.

We got an interesting surprise on Friday with the Jobs Report, which we cover next.

The charts in the recap section have been sponsored by Koyfin. We have a special discount of 15% for MacroVisor readers for any new sign-ups to Koyfin. To take advantage of this promo please sign up here - Koyfin MacroVisor Discount

Macro - Jobs Friday

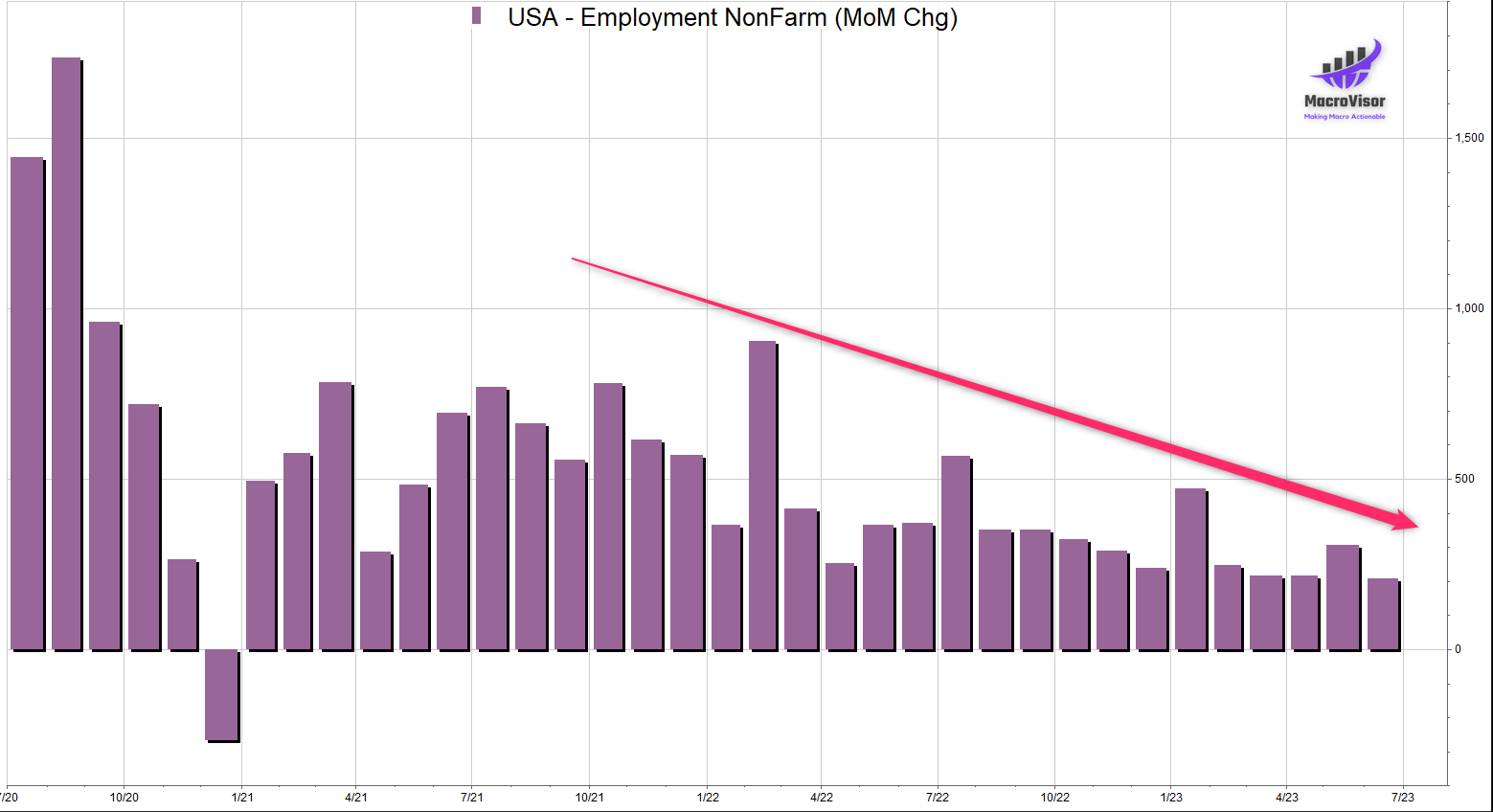

As we said above, the ADP numbers were much higher than expected, and the NFP was expected between 215k and 230k. We had expected above 250k. Morgan Stanley expected 270k.

To everyone’s surprise, the Non-Farm Payrolls on Friday came in at 209k, much lower than expected and there’s certainly a declining trend in values.

The Household Survey, i.e., the Unemployment Rate declined to 3.6% in line with expectations. Hourly Earnings remained unchanged, while the Average Workweek Increased slightly.

A few key takeaways from the report:

Job creation was led by government, health care, social assistance, and construction. Leisure & Hospitality is no longer in the lead position.

The labor force participation rate was 62.6 percent for the fourth consecutive month

The number of discouraged workers, a subset of the marginally attached who believed that no jobs were available for them, decreased by 112,000 to 310,000 in June.

The number of persons employed part time for economic reasons increased by 452,000 to 4.2 million in June, partially reflecting an increase in the number of persons whose hours were cut due to slack work or business conditions. These were people who had their hours cut or couldn’t find full time work. (Not a great sign)1

The total revisions for April and May have now come out to -110k (not a great sign either)

Excerpt from the BLS:

The change in total nonfarm payroll employment for April was revised down by 77,000, from +294,000 to +217,000, and the change for May was revised down by 33,000, from +339,000 to +306,000. With these revisions, employment in April and May combined is 110,000 lower than previously reported. (Monthly revisions result from additional reports received from businesses and government agencies since the last published estimates and from the recalculation of seasonal factors.)2

While the unemployment rate remains significantly low, indicating a tight job market, the decline in the NFP data including the downward revisions suggest that the market is beginning to soften.

Earnings Season - Second Quarter Incoming

Earnings season starts with JP Morgan reporting on Friday 14 July with some of the major banks and we have a handful of earnings the day before with Delta, Pepsi, Conagra, Fastenal and Progressive reporting on Thursday. (Calendar below)

Earnings came in better-than-expected last quarter due to a number of factors and this time there a few changes to that story:

Easier comps - Estimates were taken down quite a bit and this led to most companies coming in ahead of estimates. Given that companies have been guiding higher, and discussing improved performance, estimates have been revised upwards for this quarter.

Improved spending levels and residual fiscal stimulus - These go hand in hand. We still had the effects of SNAP payments, Cost of Living Adjustments, Pandemic Medical Benefits and student loan moratoriums during Q1. The first three fell away in March/April and we’re likely to see the effects of lower spending for much of Q2 results.

Tailwinds from easing supply chain conditions - We’ve been seeing the PPI numbers go down drastically. Input costs and freight costs have declined quite substantially, and this helped operating margins in Q1. We’re likely to see the lingering positive effect of these continue for the second quarter as well but, they may not be as pronounced.

Pricing Power - Companies were still wielding quite a bit of pricing power in the first quarter. However, we’ve seen the CPI and PCE numbers decline, particularly in non-service categories. So, we’re likely seeing pricing power fade gradually and that will be something to keep an eye on.

Labor Market - The labor market has still remained tight so it’s likely that consumption will not have dropped massively. Wages have started to decline and we are seeing many segments of the population pull back, and spend on credit. But the situation is not a uniform decline in consumption. The labor situation has improved for many sectors where hiring was a problem - healthcare, travel & leisure, and restaurants - and we’re likely to see these sectors fare better.

Nevertheless, we’re already in an earnings recession and this earnings season will have tougher comps with the Street estimates showing an earnings decline of over 7% on the S&P 500.

Final word of caution: I’m sure you’ve been seeing what’s happening with the Manufacturing PMI numbers. We’re seeing the PMI remain in contractionary territory and new orders have fallen significantly. Manufacturing is taking a hit.

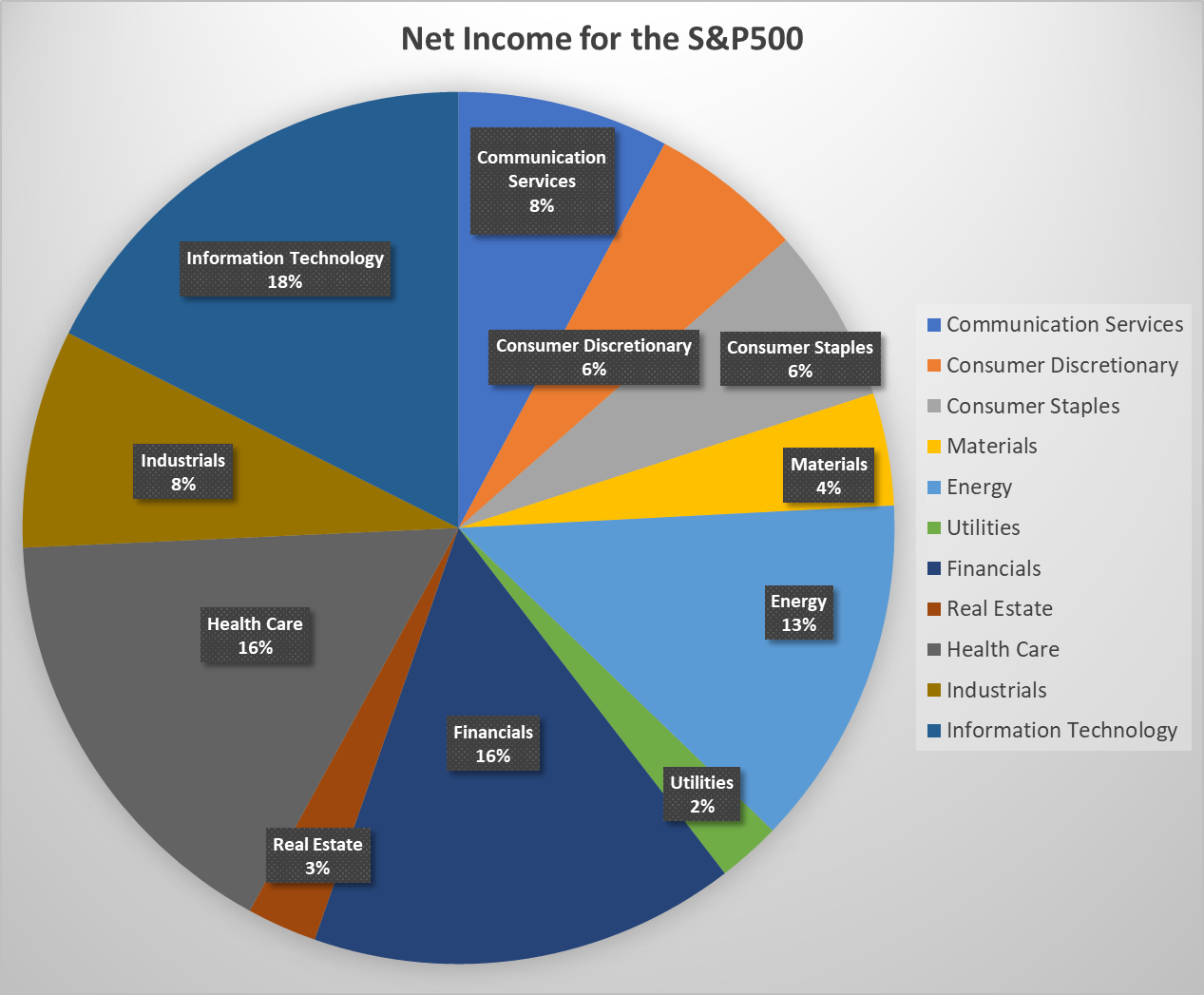

Here’s a chart of the Net Income for the S&P 500 based on forecasts for Q2, 2023 earnings. As you can see almost 66% comes from asset-heavy, non-services, i.e., companies that either manufacture themselves or have some links to manufacturing.

The Week Ahead 📅

US Earnings Calendar

US Economic Calendar in Eastern Time

Closing Thoughts - The busy week ahead

We have an action-packed week ahead with the CPI, PPI, Consumer Sentiment Data and Earnings. As if that wasn’t enough, we also have plenty of Fed Speakers in the mix.

A few of the banks report on Friday but, none of these are of much concern - at least not in terms of the issues that we saw with the regional banks. It will be interesting to see what JP Morgan has to say, as always. But this time, we’ll hear a little bit more on the First Republic acquisition.

In general, we’ll also be looking at provisions being taken by these bigger banks, net charge-offs and trading income. We’re likely to see trading income decline, at least that’s the consensus forecast.

There’s a lot to look forward to this week and here’s wishing you safe investing.

Sincerely yours,

Ayesha Tariq, CFA

There’s always a story behind the numbers.

None of the above is Investment Advice. I may or may not have positions in any of the stocks or asset classes mentioned. I have no affiliation with any of the companies other than explicitly mentioned.

Persons employed part time for economic reasons are individuals who would have preferred full-time employment but were working part time because their hours had been reduced or they were unable to find full-time jobs. - BLS

bls.gov

Thank you Ayesha! Great stuff as always. Excellent to see you again on Bloomberg as well.

Thank you Ayesha!