The Weekend Edition # 165 - Central Bank Bonanza

A Preview of next week's meetings of the Fed and the Bank of Japan

Welcome to another issue of the Weekend Edition!

Thank you for reading and subscribing to our newsletter.

Market Recap

10 -14 March, 2025

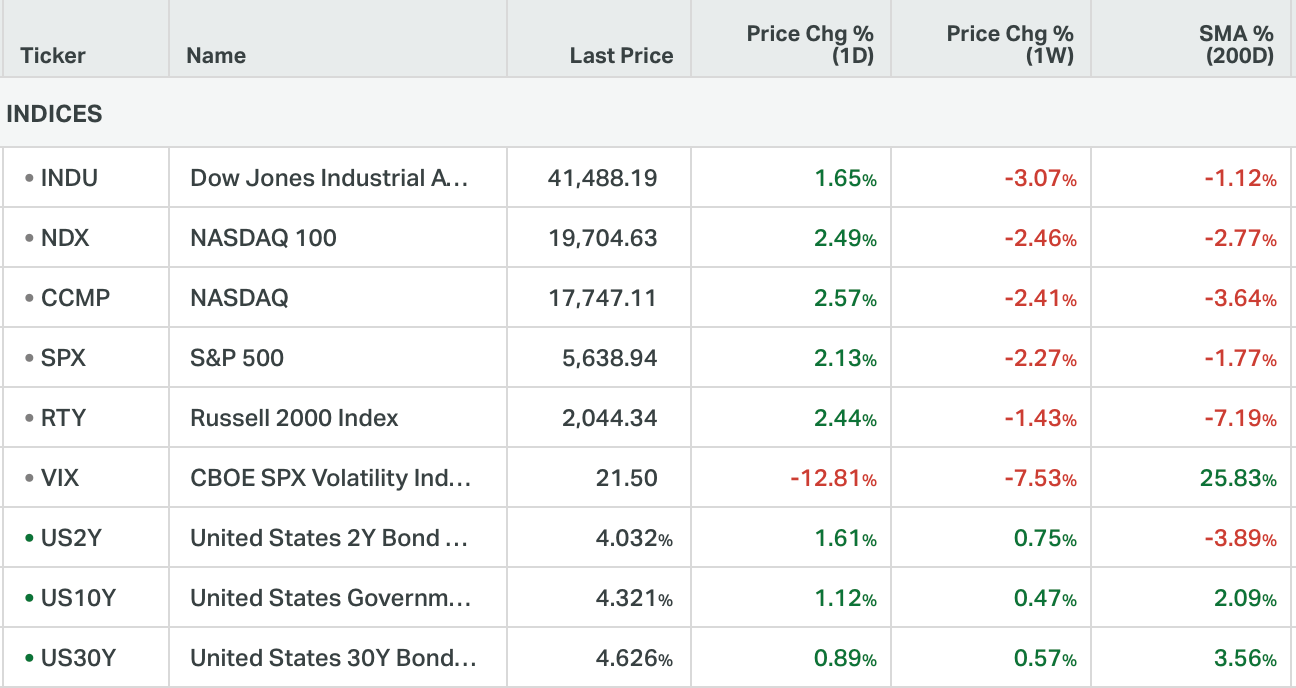

This has been a tough week that’s at least ended on a relatively good note.

We had a mix of macro data this week, with inflation numbers - both CPI and PPI - coming in softer than expected. While the CPI reversed some of the downward momentum, the PPI did nothing to help things, and Thursday saw the S&P 500 dip into correction territory, closing at -10.13% from its recent peak.

There’s been a lot of discussion on CTAs selling down and according to JPM, CTAs are back down to Oct 2023 levels but still above the lows in 2022. However, they don’t see signs of capitulation. Meanwhile, GS says they’re seeing “healthier Momentum” and Hedge Fund selling could be largely behind us.

I don’t think we have the all-clear as yet. The AI theme is still under some scrutiny. Uncertainty remains with policies and what’s next for the economy so we’re likely to see some turbulence. In fact, Morgan Stanley put out a note saying that buying the dip in what’s been working is probably not the best idea, and rotating to defensives such as Financials and domestic manufacturers could be a better play.

On the commodity front, Gold hit $3000/oz, our interim target, but pulled back afterward. We would be cautious here. Crude Oil saw a spike after sanctions were increased on Iran, and in a way Russia, as we discussed yesterday.

Now, let’s see what’s coming up next week.

Macro - Central Bank Bonanza - The Fed & The BoJ

It’s that time again - Central Bank Bonanza.

On Wednesday, March 19, we have Japan, the US, and Brazil.

On Thursday, March 20, we have the UK, Switzerland and Sweden.

These are the first Central Bank meetings from these countries after Tariffs went live. So, I’m guessing we’ll have some interesting conversations and statements.

The Fed

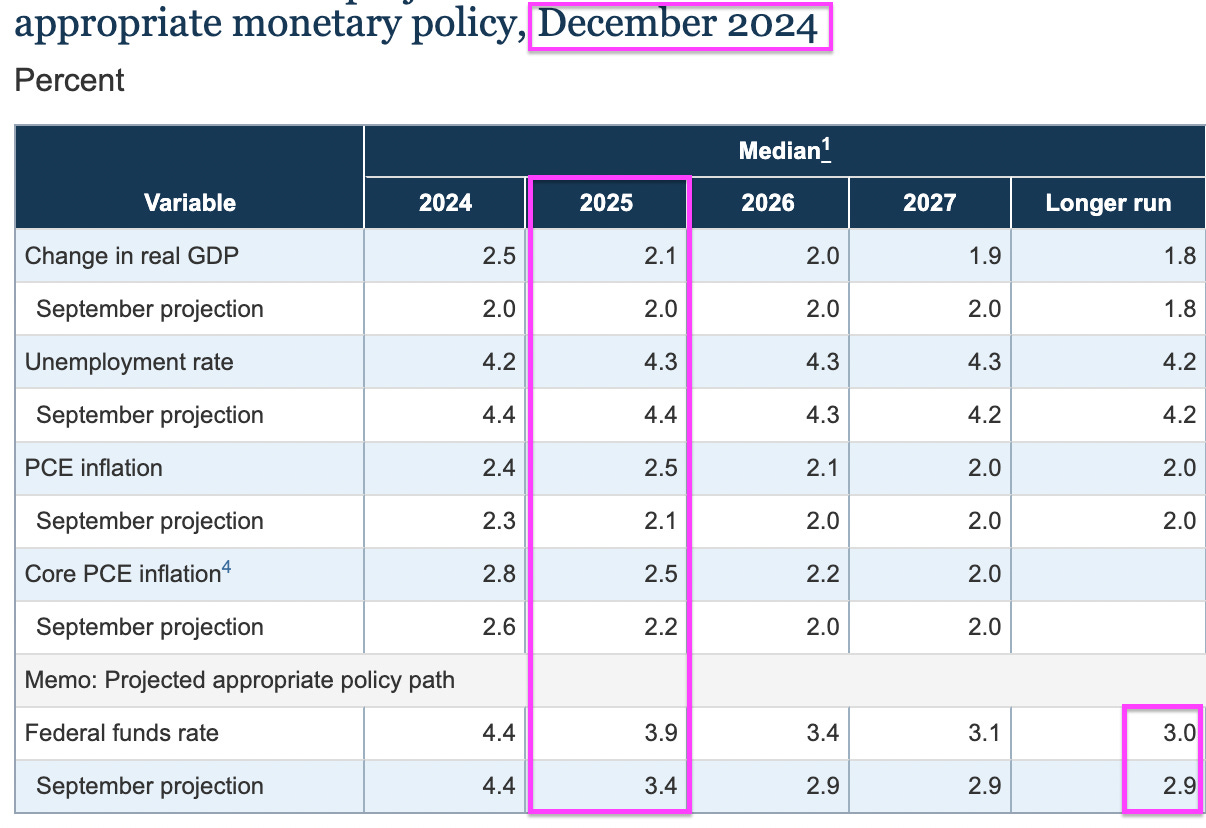

Let’s start with the US Federal Reserve. This meeting also comes with the Summary of Economic Projections that will tell us whether the Fed has changed its thinking on the state of the economy, and the number of rate cuts for the year.

For now, the Fed has signaled a soft pause, and the consensus is no change to the Federal Funds Rate during the March meeting. But what about the following meetings?

Let’s look at what the Fed told us last time:

The Fed surprised us, reducing the Federal Funds Rate (FFR) by only 0.5% (50bps) in 2025. That amounts to two 25-bp cuts for this year. This change came after quite a bit of turbulence in the projections that went from 4 cuts to 3 cuts to 4 cuts again. We can see that the rate cuts are very much a moving target at this point.

Now the market is pricing in 62.37bps, just over 2 cuts for the year. This comes after we’ve seen some respite in inflation numbers alongside a growth scare and weakening employment numbers, on the margin. But remember, the Fed is also concerned with what may happen and I think they realize now that they moved too slowly when inflation started picking up in 2021 and moved too fast when they saw the jobs data in Sep 2024.

With Tariffs now in place, and no longer just a threat, there is a higher chance that inflation stays sticky, at least for this year. And that is exactly what the Fed already thinks will happen, as we see their inflation forecast picked up between September and December.

So the Fed was convinced that what lies ahead would bring about higher prices. For what it’s worth, I don’t think tariffs were the only concern. We’ve made this case before as well - slower immigration policies will likely increase wages.

Another thing to remember is that the Fed is always concerned about inflation expectations.

As Volcker pointed out: When people begin anticipating inflation, it doesn't do you any good anymore, because any benefit of inflation comes from the fact that you do better than you thought you were going to do.

And we know that Chair Powell is an ardent follower of Volcker’s work. This is why in almost every meeting he talks about “inflation expectations remaining well-anchored”.

But how long do they remain so? We’ve seen the Inflation Expectation readings spike over the past two months, with yesterday’s preliminary reading also coming in higher.

What’s interesting though is that the Fed projected a stronger economy - higher GDP growth and lower unemployment. Not by much, but still an improvement.

It makes me wonder whether the reason they decided to do that was to justify higher rates, because the market is seeing something totally different, and the bond market is certainly pricing in lower growth. Since the last Fed meeting on Jan 29, we’ve seen the 2-year Treasury Yield reprice lower.

Markets are worried about growth. And this was just exacerbated by the Atlanta Fed’s GDPNow Cast number of -2.3% going viral on social media. We talked about this last week, and the reason for the pullback is actually a drop in Net Exports (Exports - Imports), with the Import of gold being a big reason. Now, it’s debatable whether these gold imports get counted as a financial transaction, that will not be included in the GDP growth number.

Having said all that, we still think that growth is on a downward trajectory. Trade wars are never good for growth, and many believe that prices of goods are going to go up.

Fear begets fear - as we said last week as well, given that growth fears are permeating the economy, people and companies are going to defer spending decisions, and that decreases GDP growth.

What do we expect to see from the Fed?

I think it will be interesting to see what the Fed does with the growth numbers. We get the Retail Sales print for the US on Monday, and a miss could further some doubts about the economy. Fed Chair Powell’s recent speech, however, tells us that the Fed is not worried about growth, and therefore, we’re not likely going to see any drastic changes to the growth projection either.

On the Rates front, I don’t think the longer-run (neutral) rate will be changed here. 3% is high enough, and the aim will now be to make sure that the real neutral rate (i.e., Rate - Inflation) is 1%. That’s high or low, depending on who you ask. But, it’s certainly higher than what everyone expected a year ago. The way things are shaping up though, I wouldn’t be surprised if the longer-term rate starts to move higher, in time.

As for rate projections for this year, the safest outcome for the Fed is probably not to change projections at this stage. We have two opposing views in the market. One says inflation moves too high, and the Fed has to hike again - I think this is highly improbable. The other view says growth slows down enough that the Fed cuts more than expected - this could be possible.

My view is that the Fed takes a wait-and-see approach, and as long as PCE inflation remains within the Fed’s 2.5% for the year, we’re probably looking at 2 cuts.

The Bank of Japan

Now let's turn our attention briefly to the Bank of Japan.

There's been a lot of speculation that Governor Ueda will hike at this meeting and yields are pricing that in. Japanese Government Bond (JGB) yields have increased to the highest levels since the Great Financial Crisis. Now part of that is because of stronger macro data that we've been seeing over the last few weeks.

Inflation numbers have come in higher. GDP growth numbers have come in stable, and wage growth has been solid. Now, this is exactly what the Bank of Japan was looking for.

We have been talking a lot about the wage negotiations and the Shanto wage increases, which are the spring wage increases. As we know, Japan has always had a problem with deflation and the BoJ wanted to see wages move higher to drive structural inflation in the economy through consumer spending leading to GDP growth.

But Real Wages (wages adjusted for inflation) are slipping back into negative territory, and probably a reason that the BoJ doesn’t want to rush hikes.

We don't expect a hike during this meeting and Governor Ueda has signaled as much in the last few times that he's spoken. He's talked about the trend in inflation still being under 2% and we can see that when we look at pure core inflation, which excludes all food and energy, not just fresh food.

Coupled with the uptrend in wages, yields are spiking.

However, the Governor has also discussed long-term rates likely being driven by fear about overseas developments, and while they are committed to shrinking the balance sheet, they would be ready to step in with bond purchases if long-term yields behaved erratically. They still retain a hiking bias. And we do think we will see further hikes this year, just not during this meeting.

Now why is this important?

It's important because the spread between the yield on the 10Y JGBs and that of the 10Y US Treasury is now narrowing. People speculate that this could lead to another carry trade event, similar to what we saw in August 2024. However, we don't think there will be a big carry trade unwind. We do, however, want to note that quite often when we see a spike in JGB yields, we see the Russell 2000 start to go down.

Now this could be a spurious correlation or there could be something to it. Either way, it's something that we keep an eye on, and the moves from the BoJ will be on watch.

Closing Thoughts - Unstable

The relief rally on Friday was understandable, given the market moved into correction and the possibility of the US government shutdown being averted. Something tells me it was also a function of positioning since the market rallied even after an ugly UoM Sentiment print.

Market sentiment has declined significantly, and we’ve already seen some rotation into defensives. The markets got oversold and we’re seeing a bounce. We may see some continuation of this rally into next week but, we have the BoJ and the Fed next week so there could be volatility.

Most importantly, the underlying causes of the market sell-off still remain - policy uncertainty - and therefore, we continue to be cautious overall.

Have a safe trading week out there!

Sincerely yours,

Ayesha Tariq, CFA

There’s always a story behind the numbers.

Calendars

US Earnings Calendar

US Economic Calendar in Eastern Time (Source: Trading Economics)