The Great Macro Playbook

The Weekend Edition 180: The regime is shifting. The trigger is a war. The hedge is AI.

Markets are holding two contradictory truths at once. On one side, an oil shock is bleeding quietly into the real economy in ways the headlines have not fully captured. On the other hand, an AI boom is broadening, delivering real demand, and absorbing macro shocks that would have broken equity markets in any other cycle.

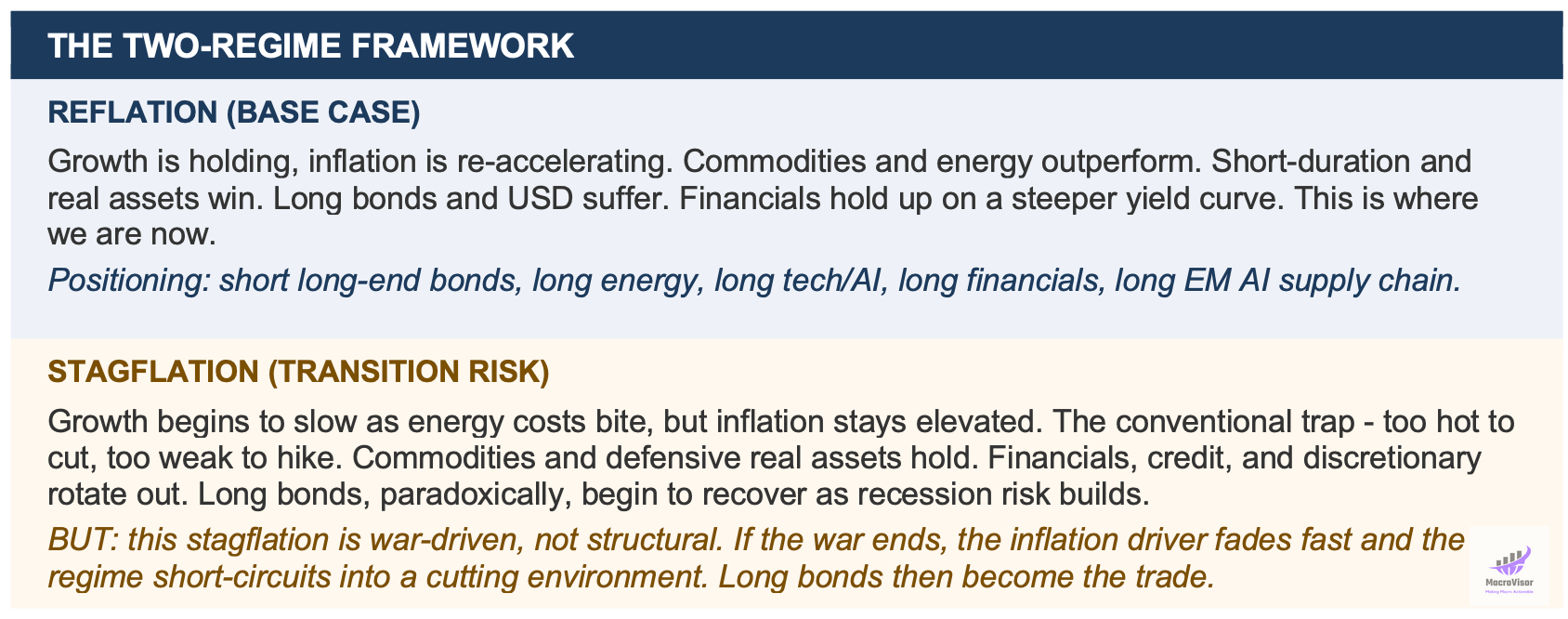

The standard framing treats these as opposing forces. We think that misses the more important question, which is about regime - where we are in the inflation and growth cycle, where we are going, and what triggers the turn. We are currently in a reflation environment, one where growth is holding, and inflation is re-accelerating. The risk is a transition to stagflation, where growth begins to fade, but inflation stays elevated. Those two regimes carry very different implications for almost every asset class.

What makes this moment unusual is that the path between them runs directly through one variable: the Strait of Hormuz. This is an energy-driven inflation cycle, not a structural one. That distinction matters enormously for how the Federal Reserve responds, and for where the biggest mispriced trade in markets sits right now.

War and Oil: The Pain Is Deeper Than the Price Tells You

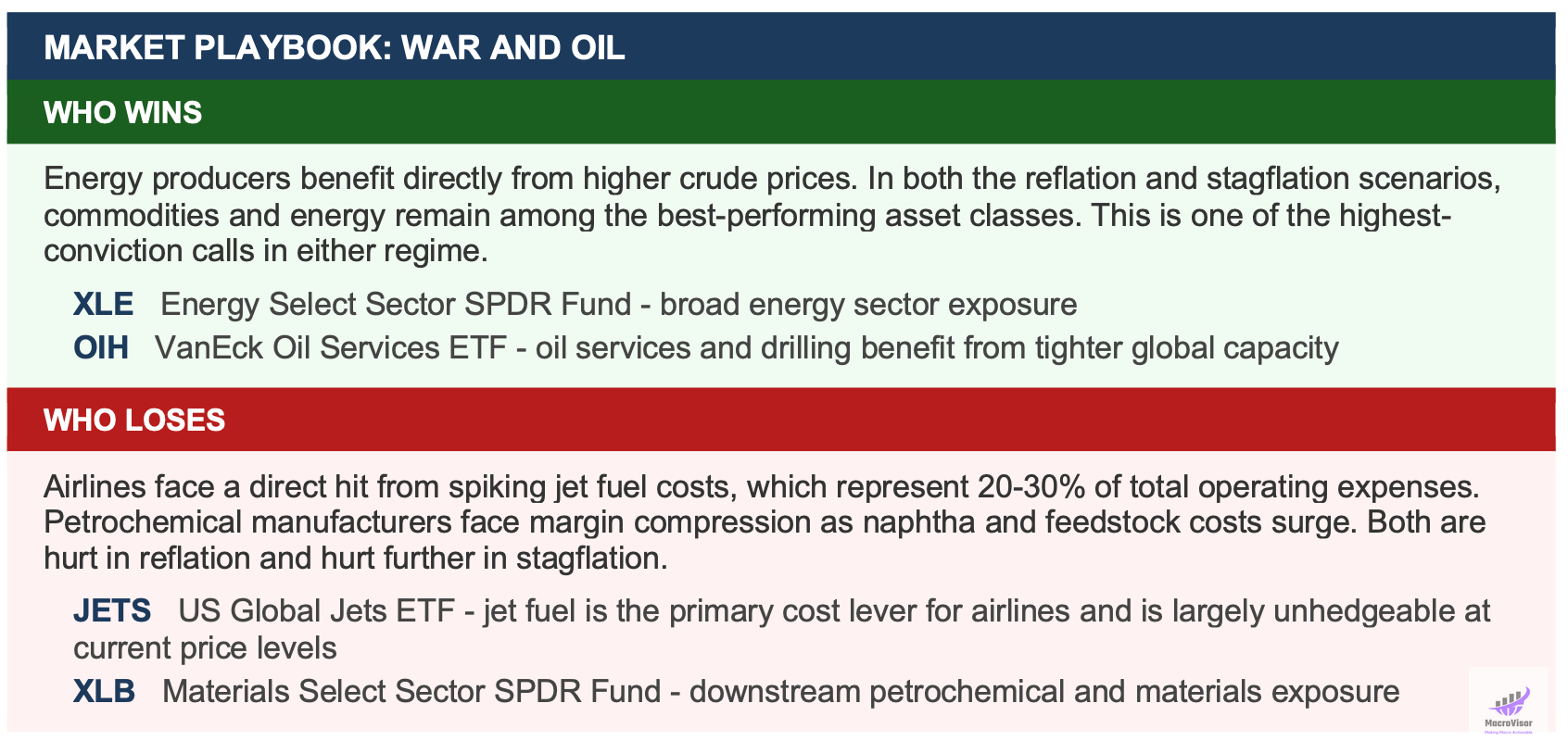

The Strait of Hormuz handles roughly 20% of the global oil supply. When passage is disrupted, the shock does not arrive instantly in the headline oil price. It arrives in the downstream markets that most investors never watch. Jet fuel, diesel, and petrochemical feedstocks are where the pressure builds first, because these products have fewer substitutes and tighter supply chains than crude itself.

That is exactly what is happening now. The downstream shortages are becoming concrete. Jet fuel and diesel prices are spiking. In Malaysia, factories cannot bottle milk because naphtha supply has dried up. That is not a financial market story yet. It is the oil shock arriving in the real economy.

The mechanism matters for investors. When energy costs rise through downstream channels, they do not show up immediately in consumer price data. They show up in producer prices first, then in corporate margins, and finally in consumer prices, with a lag of roughly two to four months. The full inflationary impact of the current disruption has not yet hit the data. That is precisely why markets are underpricing it.

Iran has floated the idea of charging a fee to reopen the Strait to selected vessels. This is not a resolution, and it is the kind of leverage that they will not be willing to give up. Control of the Strait is Iran’s single most powerful negotiating chip, more important in practical terms than the uranium enrichment discussions that have consumed most of the diplomatic airtime. A fee arrangement sets a dangerous precedent and guarantees nothing about safe passage.

The inventory buffer is nearly exhausted. An estimated 1.5 billion barrels will have been drawn down by June, just as summer demand arrives. Oil prices are heading higher, and the risk is asymmetric to the upside.

Rates: Short Bonds Now, But Watch for the Pivot

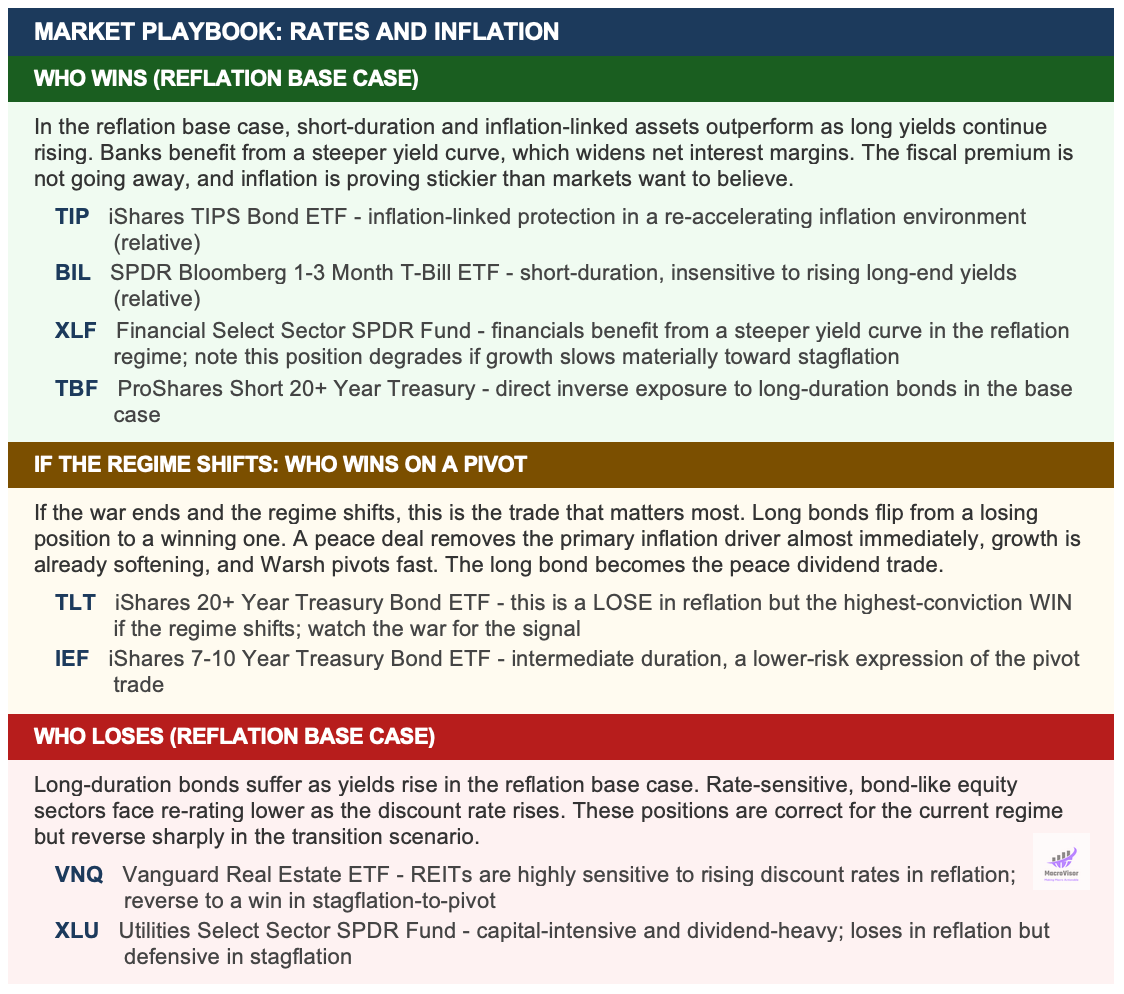

Central banks thought they were done with inflation. They are not. Near-term Fed rate cut expectations have evaporated, and traders are now pricing actual hikes starting in April 2027. This is the reflation regime expressing itself in the bond market, and our view is that it has further to run.

To understand why long-end yields are rising independently of what the Fed does, it helps to separate two concepts. The policy rate is what the Fed sets and controls directly. The term premium is the additional yield investors demand for holding a long-duration bond rather than rolling over short-term debt. When inflation is uncertain and fiscal deficits are large, term premiums rise, pushing long-end yields higher regardless of the policy stance. That is the environment we are in. We want to be short long-term bonds for as long as the reflation regime holds.

Three things make this inflation cycle more persistent than a standard one. First, inflation has been running above target for almost five years, which gradually erodes the credibility that allows central banks to look through shocks. Second, the tariff shock from earlier this year is still working its way through supply chains and has not fully shown up in prices. Third, AI is pushing electricity costs higher and generating sustained demand for hardware and infrastructure, none of which is deflationary in the near term.

But here is where the analysis becomes more nuanced, and where the biggest mispriced trade sits.

If the energy shock persists long enough, growth begins to slow. Consumer spending softens first, particularly among lower-income households who spend a disproportionate share of income on fuel and utilities. Corporate margins follow. We move from reflation into stagflation: inflation still elevated, but growth rolling over. In a normal stagflation, the Fed is trapped. Too much inflation to cut, too little growth to hike. They hold.

This is not a normal stagflation. This one is driven by a single, identifiable, war-related supply disruption. The inflation is not coming from excess demand or structural wage pressure. It is coming from a closed strait. If that strait reopens, the primary inflation driver fades within weeks, not quarters. You are left with slowing growth, falling energy prices, and a Fed that no longer has any reason to hold. That is an aggressive cutting environment, and it arrives fast.

Fed Chair Warsh has already signaled this logic implicitly. His public framing has consistently treated the energy shock as the binding constraint. If the constraint lifts, the pivot follows. There is also a direct political dimension: the closer Washington gets to the midterms, the stronger the incentive to pursue a resolution. A peace deal would likely trigger an immediate pivot toward easing. That is the trade hiding in plain sight.

This is not just a US story. The ECB may well be hiking in June. In Europe, energy prices transmit to core inflation faster and more directly than in the US. The UK deserves particular attention: gilt yields just hit their highest level since the Bank of England gained independence, with sterling falling simultaneously. Rising yields and a falling currency together are the hallmark of an emerging market crisis. In a G7 economy, that raises serious contagion risk into broader European sovereign markets, and that tail risk is significantly underpriced. We are short sterling.

The US Labor Market: The Bridge Between Regimes

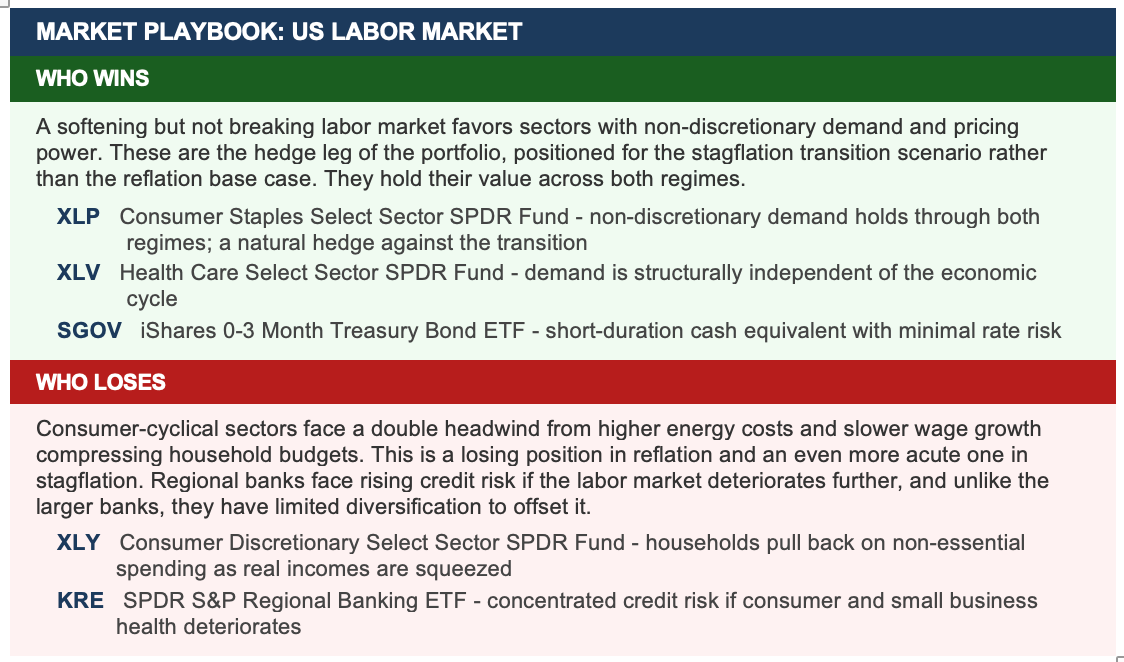

The US labor market is the variable that determines how fast the regime transition happens, if it happens at all. As long as employment stays resilient, consumption will remain resilient, and the Fed retains the credibility to hold. But if the labor market softens meaningfully, the stagflation argument strengthens, and the political pressure on the Fed to act intensifies.

Cracks are appearing at the edges. Initial jobless claims have been creeping higher in recent weeks, not dramatically, but consistently. Job openings have come off their peak. Wage growth, while still positive, is decelerating in services, the sector that matters most for core inflation. The labor market is not breaking. It is softening.

This is where the energy shock intersects with labor dynamics in a way that directly affects the timing of any pivot. When energy costs rise, lower-income consumers are squeezed first. If wage growth slows simultaneously, the combination of higher costs and smaller paychecks creates a genuine consumption headwind. It is the channel through which an energy shock becomes a broader economic slowdown, and it is the mechanism that would push the economy from reflation into stagflation faster than the base case anticipates.

The Fed watches this closely, but so should equity investors. The labor market is one of the few variables that can move the policy timeline materially. A sharp deterioration in payrolls over the next two months would almost certainly pull forward the pivot discussion, particularly if it coincides with any diplomatic progress on the war. The two signals together, a weakening labor market and a peace deal, are the combination that triggers the most aggressive market move.

The key indicator is the labor force participation rate. If workers begin leaving the labor force rather than showing up in unemployment claims, the official rate understates the true weakness. A falling participation rate alongside rising claims is the warning sign to watch.

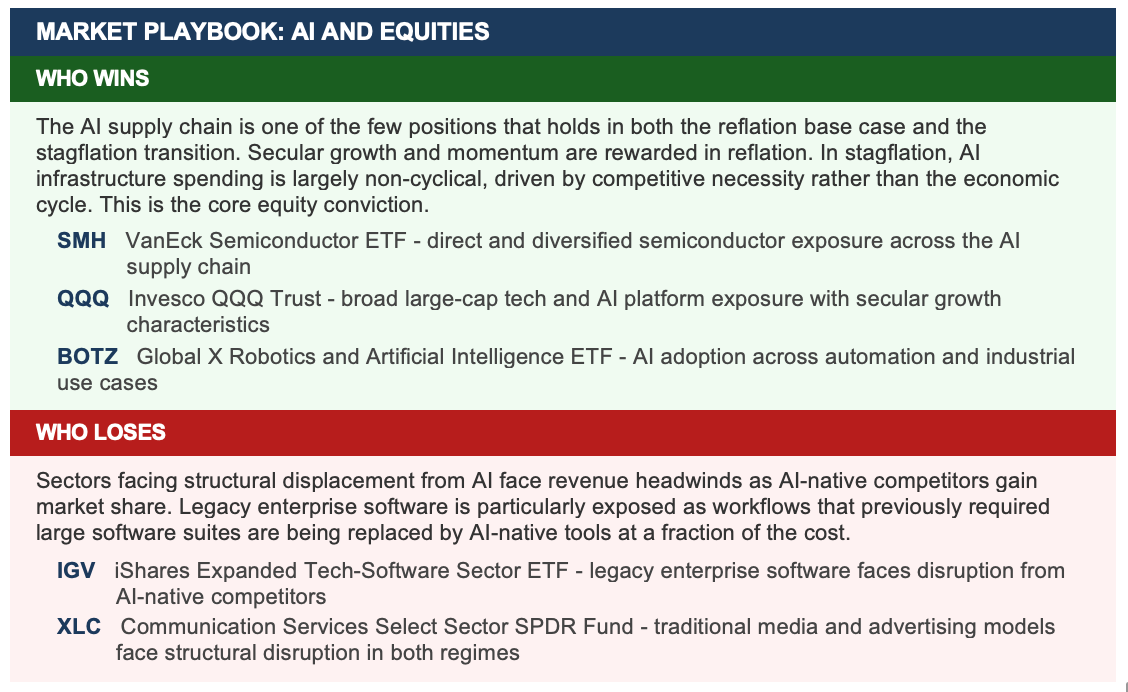

AI Is the Hedge Now: The Equity Story Holds

Despite everything outlined above, the dominant market signal remains bullish, and the reason is AI. The fundamental case is getting stronger, not weaker, and it is providing a degree of macro insulation that is genuinely unusual in a rising rate environment.

Adoption rates are accelerating. Demand for compute, measured in token consumption and data center capacity bookings, is growing faster than most forecasts projected eighteen months ago. The capex cycle that the market had been pricing speculatively for two years is now showing up in real demand figures. Corporate earnings are beginning to confirm what the valuations had long assumed. This is no longer primarily a re-rating story. It is a fundamental one.

To understand the macro significance, consider how AI spending flows through the economy. Hyperscalers invest heavily in hardware and infrastructure. That spending lands in semiconductor revenues, then in equipment manufacturers, then in the engineers who design and maintain the systems, and finally in the software companies whose platforms run on that compute. The multiplier effect of that capex cycle is now visible in earnings across a range of sectors, not just in a handful of mega-cap names.

The most important signal right now is earnings breadth. When AI-driven gains were confined to five or six names, the rally was fragile. Breadth is now improving across sectors, from industrials adopting AI in manufacturing to healthcare using it in diagnostics to financial firms deploying it in compliance and risk management. A broader rally absorbs macro shocks more effectively, and it reduces the single-stock concentration risk that made the earlier phase of the rally so vulnerable.

Critically, AI spending is largely insensitive to the energy shock and to the rate cycle in the near term. Hyperscaler capex commitments are multi-year. Enterprise adoption decisions are driven by competitive pressure and productivity gains, not by the monthly CPI print. In both the reflation and stagflation scenarios, the secular growth argument for AI infrastructure remains intact. This makes it one of the rare positions that holds across regime transitions.

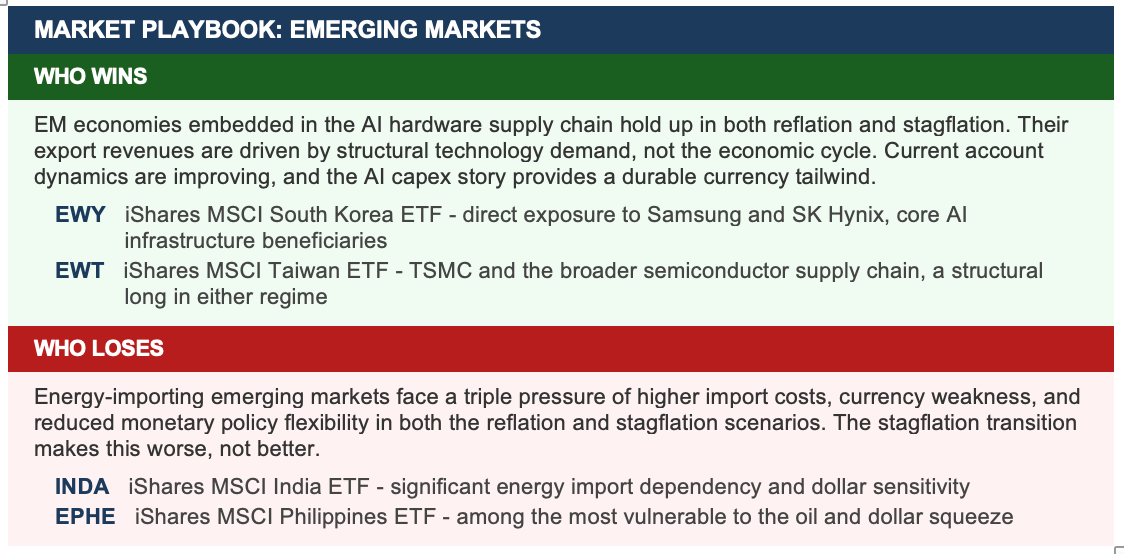

Emerging Markets: Know Which Side You Are On

Emerging markets are a tale of two stories - the AI haves and the Oil have-nots. And the gap

is widening in a way that maps almost perfectly onto the reflation versus stagflation framework.

On one side are the AI beneficiaries: South Korea and Taiwan, whose economies are directly embedded in the global AI capex boom through semiconductor and component manufacturing. Samsung, SK Hynix, and TSMC are not simply technology companies. They are physical infrastructure for the AI buildout. When hyperscalers increase AI spending, a meaningful portion of that capital lands in Seoul and Taipei. In the reflation regime, this is a straightforward export demand story. In stagflation, it holds, because AI spending is non-cyclical. These economies are positioned well in either scenario.

On the other side are the energy importers: economies like the Philippines and India that run significant current account deficits and import the majority of their energy. For these economies, a higher oil price means a weaker currency, a wider deficit, and higher domestic inflation, all simultaneously. Equity markets are pulling back and bond yields are spiking, with limited policy room to respond. In the reflation regime, they are under pressure. In the stagflation scenario, that pressure intensifies.

The divergence logic is straightforward. Countries exposed to the AI supply chain have an export demand boom that partially offsets the energy shock. Countries that are primarily energy importers have no equivalent tailwind and are absorbing the shock with constrained fiscal and monetary capacity. The transition from reflation to stagflation widens this gap further, because stagflation hits import-dependent emerging markets harder and longer than it hits developed markets.

One additional tail risk worth monitoring: if the UK gilt situation deteriorates further, contagion into broader EM sovereign markets cannot be dismissed. A synchronized EM stress event would arrive faster than most investors currently anticipate. We are long Korea and Taiwan and short or underweight the oil-importing EM bloc.

The Bottom Line

We are in a reflation regime that is showing early signs of pressure toward stagflation. In the base case, the positions are clear: short long-end bonds, long energy, long AI and tech, long the EM AI supply chain, defensive hedges in staples and healthcare, short sterling.

But the more important point is the conditional one. This is not structural stagflation. It is war-driven. The inflation has a specific cause, and that cause has a potential end date. When it ends, and we believe the political incentives make resolution more likely than markets are pricing, the fastest-moving trade in the portfolio is long bonds. The peace dividend trade is not being priced. That is the opportunity.

Watch the Strait, watch the labor market, and watch the yield curve. The signal, when it comes, will move quickly.

The views expressed are my own and do not constitute investment advice. ETF references are for illustrative purposes only.

Wow Brilliant, you summed it so well 360* reality of current financial world 🌎