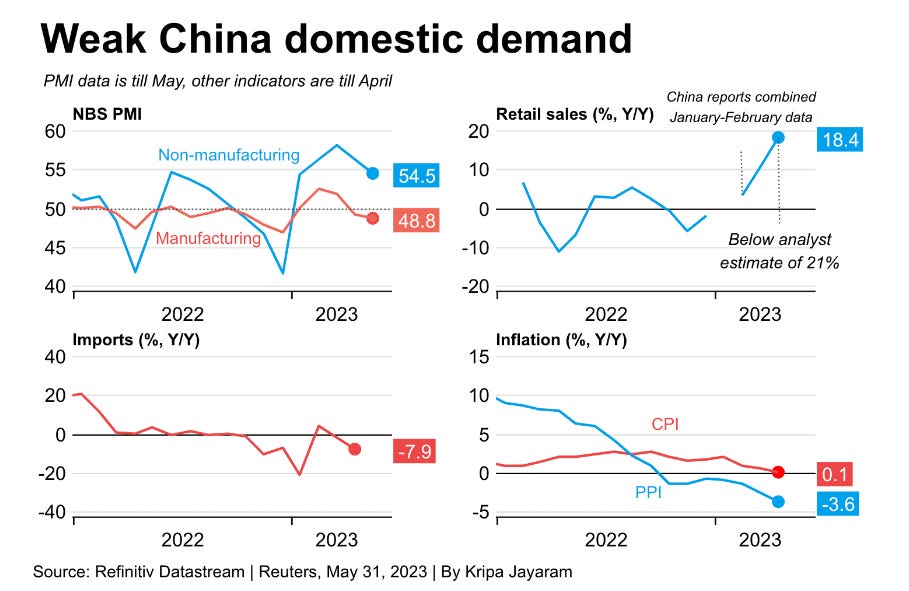

We know that there is a shortage of copper in the world, but as the global economy shows signs of slowing and China’s reopening isn’t quite the growth story that was hoped for, we’re seeing Dr. Copper give the global economy a diagnosis of being unhealthy.

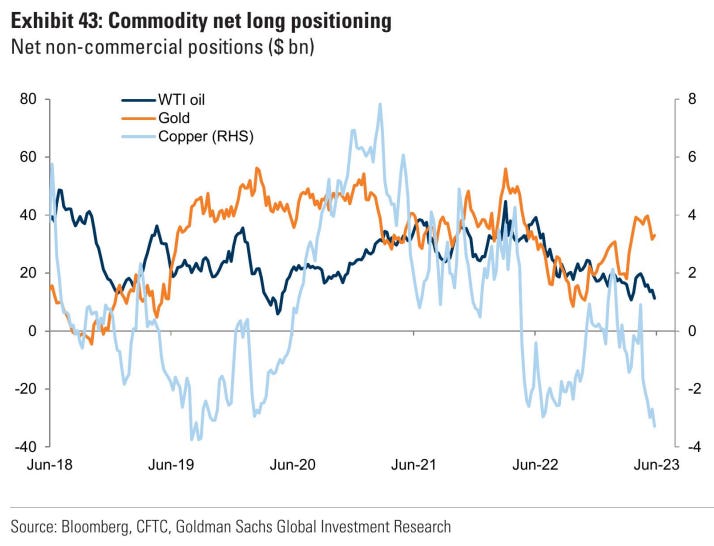

Copper net non-commercial positioning has also dropped pretty significantly

One of the biggest consumers of copper is China for copper wiring in buildings, not to mention infrastructure.

There are two things going on here:

China's own real estate market is in trouble and as a consequence funds from infrastructure is being directed to prop up this market

China was funding a lot of major infrastructure projects in Africa and other countries. They have pulled back on that now.

Post the 2008-2009 crash during the GFC, China pumped in stimulus for their local markets and much of that was directed towards commodities. This is why commodities staged a recovery in 2010. But, at the time, China was growing rapidly and "emerging".

There was a massive tailwind for growth and consumption in that economy. This time is slightly different.

China's reopening is now being led by services. Even the stimulus being pumped into the economy will be to prop up the property market and not exactly being routed for new buildings and infrastructure.

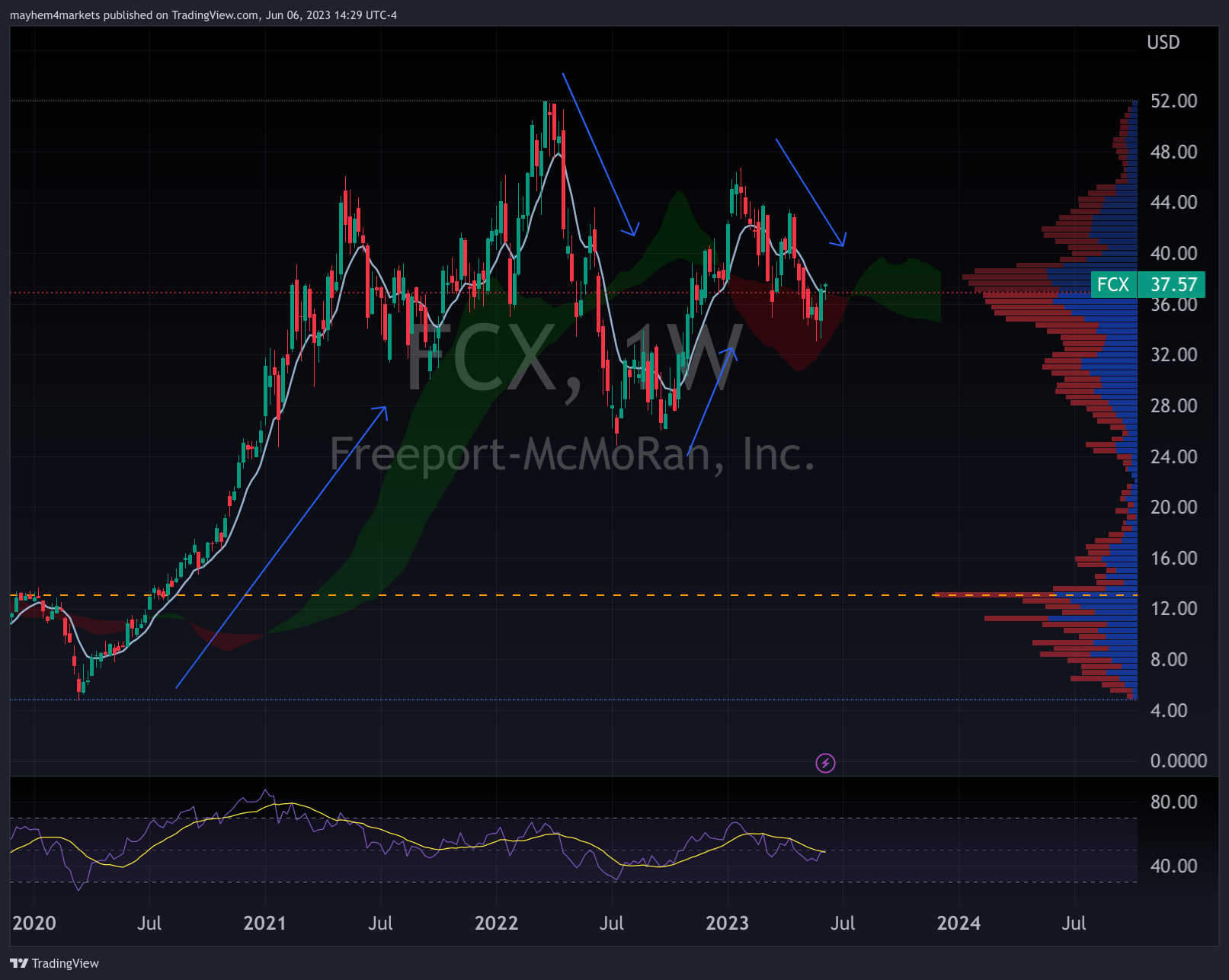

Freeport-McMoRan

Last quarter’s earnings from FCX was interesting. Volumes were down significantly but, costs were up and realized prices also declined. That’s three strikes against their copper division. They’ve struggled with weather, civil unrest and labor shortages.

They do see higher volumes for the rest of the year but they are budgeting $7B in Operating cash flows based on $4 per pound. A 10c change in copper prices impacts their cash flows by $315m, and that’s a number to remember.

It also helps to explain the positive correlation being so tight for FCX (black) vs the price of copper (red), which is currently at 0.79 over a 20-day period.

The technicals for both copper and FCX look like they are weakening here, with a recent countertrend bounce providing a potentially interesting opportunity for a starter position if we see a break below the 8-week exponential moving average on a closing basis.

That starter could potentially be added to should we see a break below the high volume node that price is within (crossing below $33.50).

Key downside support levels to watch as potential points to exit are $28 and $24.5.

To manage risk we would look at exiting if it the stock closed above the close by high volume node or the 8-week exponential moving average.

This is a high risk trade idea because the stock is a high beta cyclical, which means its trading range may be larger on a daily basis than the average S&P 500 stock.

Another risk to be aware of is that the company reports earnings again on July 26th. Earnings would an event where risk management ahead of, during, and after would be important to consider.

With that in mind we would be looking for this trade to potentially play out over a period of three or four months, into the back half of this year where we believe the economy is likely to slow further or even experience a recession. If it does not, we would close the trade, even if risk management didn’t pull us out or price targets were not hit.

That way we can have capital available for another idea.