We’ve decided to start a new weekly feature called “Quick Picks”. We’ll look at companies and pick a few stocks to watch and possible buy or sell. We will do very quick reviews on the companies and we’ll be looking for:

A specific catalyst (news, events etc.)

Fundamental changes

Technical set-up

Longer term macro set ups

We could pick a stock based on one or all three of the above and we will make a note of the timeframe as well, i.e., whether we view them as long-term investments or shorter-term swing trades.

We hope you will enjoy this series that we intend to put out every Tuesday or Wednesday, and it gives you a list of ideas to build your portfolio.

One reason we were looking forward to an earnings recession is not because we’re perma-bears but, because we were hoping for this sell off on earnings which would give us opportunities to buy some good businesses at a fair price.

Long Fortinet (NASDAQ: FTNT)

We believe that Fortinet presents both a long-term investment and swing trade opportunity based on the technicals and macro backdrop of increasing cybersecurity attacks, regulation, and as a result need for perimeter protection.

The firewall-centric cybersecurity vendor disappointed with its recent earnings, attributing the softness to deferred billables and a tough macro environment. The company has also struggled with some severe security issues in its flagship firewall products of late.

Investment Thesis

We feel their edge in perimeter security, their recent focus on scaling into data center-level network protection, and their growing monetization of services as an add-on for equipment are all positive catalysts.

With cybersecurity attacks growing in size and sophistication, perimeter security has become paramount.

New regulations and client requirements also encourage customers to purchase upsold offerings, such as subscriptions to enhance firewall protection, creating a durable services revenue stream.

Cybersecurity is an attractive allocation for investments within the more durable parts of tech, that have become more like a utility than a discretionary expense, in that security is a necessary part of doing business in 2023.

Risks

Billing cycle deferrals turn into canceled transactions, and depress revenue for the remainder of 2023.

Encroachment by competing vendors, diminishing market share.

Loss of confidence by clients impacted by severe security vulnerability that affected 500,000+ firewalls.

Trouble breaking into enterprise data center firewall space diminishing returns on recent technological investments.

We would look at this as two opportunities wrapped into one. A swing trade and an investment.

Current pricing vs key levels is an attractive risk-to-reward setup for either timeframe in our view.

For a swing trade we would be getting long here with a position that is no greater than 20% of total portfolio allocation, just under $58, and putting a stop in at $55.40. Should the stock stabilize there and begin to move higher, then we’d put a 3% trail stop in place to protect our position. That means that a stop out should help to limit total portfolio downside to about 1% (assuming there isn’t a materially adverse change outside of trading hours).

We would exit our swing trade at $72 or after two and a half months, so as to be out before the next earnings.

The investment would be something that we would buy a starter in today. We would continue to add to it, averaging in every two or three months and plan to hold it for a period of 3-5 years, as we believe that cybersecurity is a long-term opportunity and this is an attractive entry point to begin building a long-term position in FTNT.

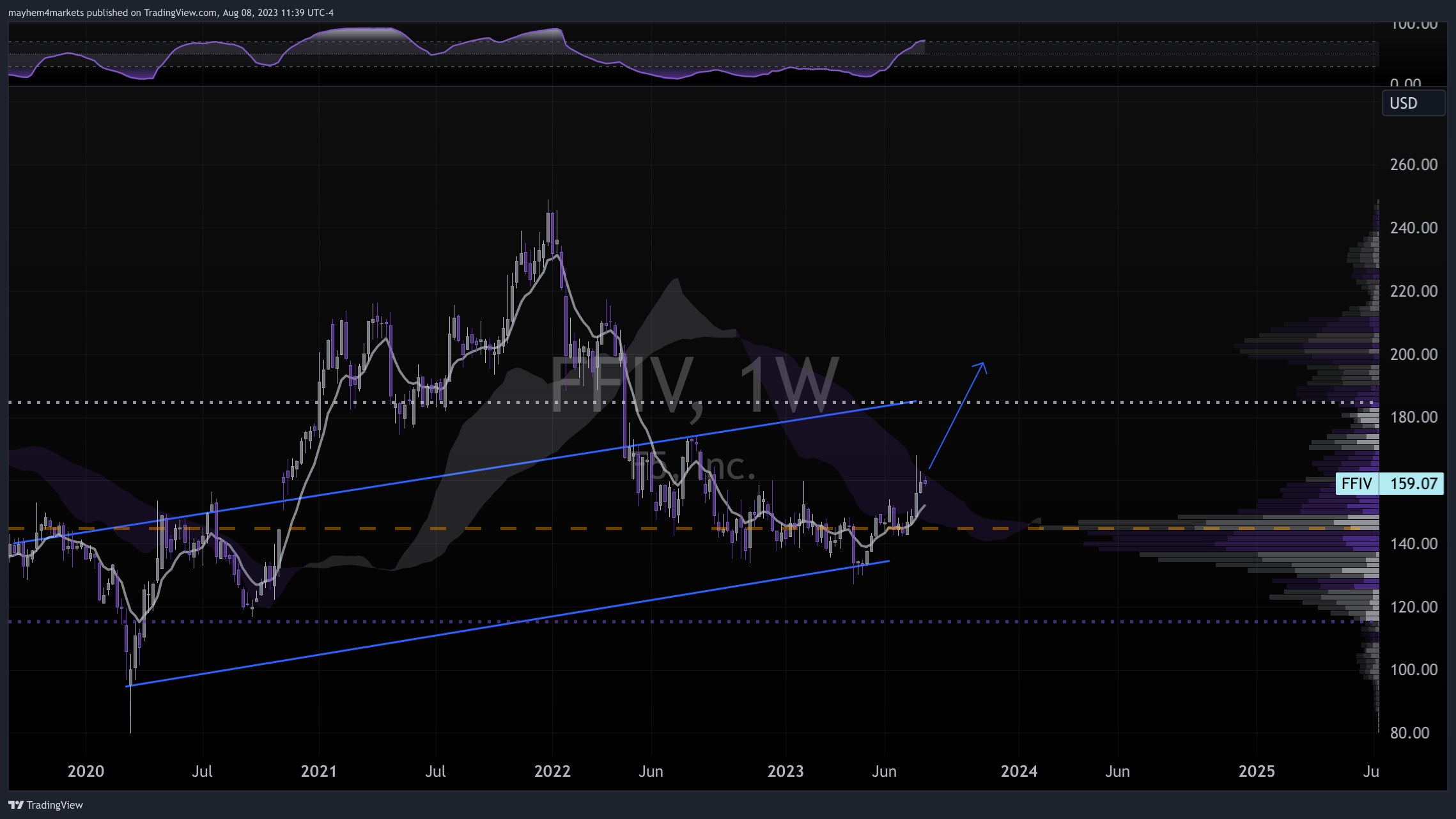

Long F5 Networks (NASDAQ: FFIV)

This cloud cybersecurity solutions provider handily beat earnings estimates. We believe it represents both a swing trade and longer term investment opportunity due to a set of circumstances that is quite similar to Fortinet — a discounting that we believe makes allocation into shares attractive at current pricing.

Investment Thesis

Cloud security space is fast growing and part of critical infrastructure protection

Investment in defending cloud applications is likely to grow significantly over the next several years

F5 counts Fortune 100 firms like Microsoft, Amazon, and Google among their core clients.

The company has a massive opportunity within securing parts of the cloud, and they are only beginning to see that potential fully unlocked.

F5 also made a very smart strategic acquisition of a web software company called NGINX that unlocks a lot of vertical integration potential and licensing opportunities.

Risks

Outflanked by competition — though that is hard to imagine at the present juncture.

Cloud providers begin to build-in their own proprietary cloud application hardening capabilities, dumping F5.

Management fails to keep pace with the rate of change in technological innovation, causing moat erosion.

We would be interested in FFIV as a swing trade or a long-term investment. We would look at entering the position on a closing break above the Ichimoku cloud, and setting my stop at exponential 20-week moving average.

We would exit the swing trade if shares rose to $200 or after two months, whichever comes first as earnings are in late October.

For an investment we would begin allocating on a breakout of the cloud with 1/4th of our total position and scale in from there over the remainder of 2023, and then adding as we have free cash for that allocation. Like FTNT, the time horizon would be 3-5 years.

Long Gasoline (ETF: UGA)

The next trade is more of a short-term tactical trade based on the current macro environment. We’ve been discussing rising oil prices and with that comes an increase of gasoline prices. Crack spreads for gasoline are still strong, driving up prices and the inventories still remain low.

The futures curves is in backwardation which gives these ETFs a time gain instead of time decay because these ETFs usually buy the front-month contract and roll off the last contract.

We would look at this as a two months swing trade with a take profit level of $75 and a stop loss at $67.

Long MP Materials (NYSE: MP)

We would view MP Materials as a longer term thematic macro pick.

MP Materials is a rare earth mining company based in the United States. The company owns and operates the Mountain Pass mine in California, which is the only rare earth mining and processing facility in the United States. It’s one of the few SPACs that have been successful and that too back by Chamath Palihapitiya. But, I’m prepared to overlook this fact as he dumped most of his shares after the SPAC merger.

Q2 Earnings update: The company beat EPS and Revenue estimates but… EPS was $0.09 but down -66.7% QoQ and -79% YoY. Revenue came in at $64m down -33% QoQ and -55% YoY. These are ugly numbers and they were mainly on lower product prices, which the company has no control over.

Investment Thesis

Despite the technical problems in the chart, MP Materials has some strong fundamentals:

As the only rare earth mining company in the United States, it has a near-monopoly on the supply of rare earth elements, which are crucial components in a wide range of high-tech products, including smartphones, electric vehicles, and wind turbine. There will be a demand supercycle for rare earth.

Given that the majority of rare earth is mined in China, supporting MP Materials is a matter of national defense for the US. The future of electrification depends in large part of rare earth magnets and the US will need to secure a solid source of supply.

MP Materials has a relatively stable balance sheet which continues to get stronger with higher volumes of production. Pricing is also important. A minimum level of pricing is required to make sure the mining is profitable. This is becoming stronger. Even if China wants to dump rare earth production to lower prices, this is not sustainable.

More companies are becoming environmentally conscious and are looking to move away from the “dirtier” Chinese production.

MP Materials has completed their Stage II and expect to ramp up production in 2023, with 2023 on the horizon.

With the advanced state of production facilities, they are becoming self-sufficient. Furthermore, any new miners coming online will also MP Materials to process their raw materials, at least for a while. This is an important catalyst.

Risks

The move to EV might be slow and companies may continue to procure from China at lower costs.

Debt levels still remain high and the ramp up in production may take longer than expected. Free Cash Flow is still minimal and the Valuation is still high at 31 NTM P/E and EV/EBITDA at 18.7x. They are however, EPS positive.

This could mean the growth in share price takes longer than expected.

We are entering a global macro slowdown, and this part of the cycle is not always favorable for materials. While EV related stocks have been generally resilient and the strength in demand should offset this, the stock could still get beaten down, as we saw back in October.

As far as the chart is concerned, this looks like an area of value and the stock seems to have a floor at $20. We would look to start a position and accumulate at these levels. The company seems to be shaking off it’s bad earnings report and even in a down day like today, it’s slightly green.

Great idea to do this! I like the concise risk / reward and background write up. thanks