Inflation May Re-accelerate in July's CPI Data

Beneficial base effects rolled off while prices increased

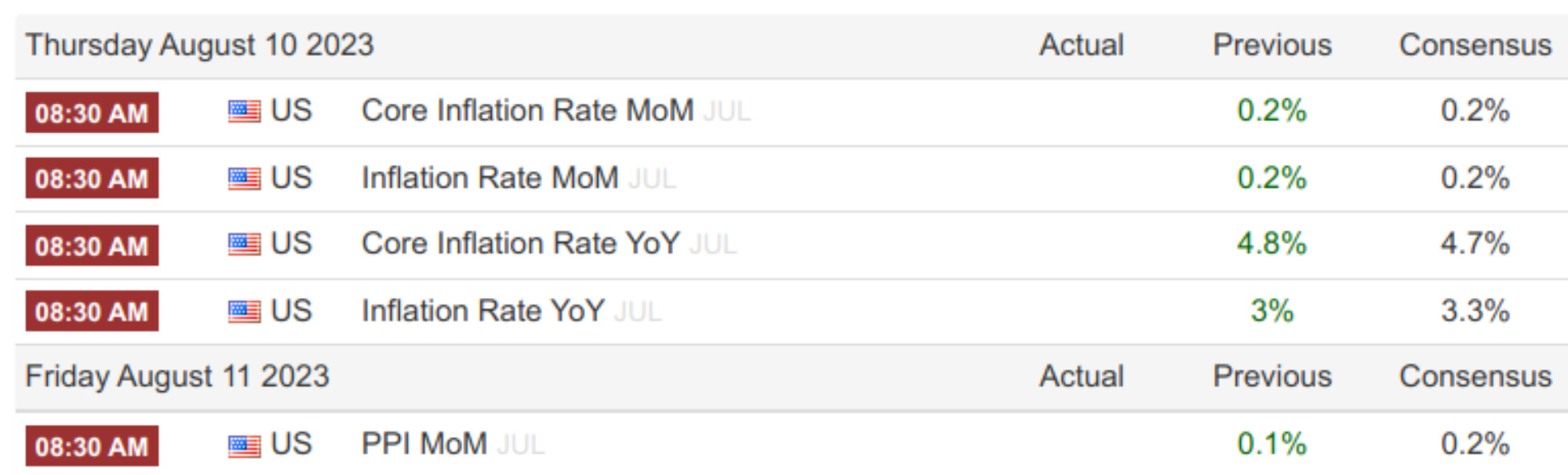

This Thursday we get US CPI data, which will be closely watched by markets that are beginning to anticipate a re-acceleration in inflation data.

Forecasters Expect a Rise in Inflation

The expectation is for a headline year-over-year number of 3.3% vs the prior reading of 3%, but there is some chance it could be a bit higher than that.

Two key concerns come to mind:

The rolling off of base effects that benefited inflation data in Q2 will put a floor in for how much inflation readings may drop year-over-year

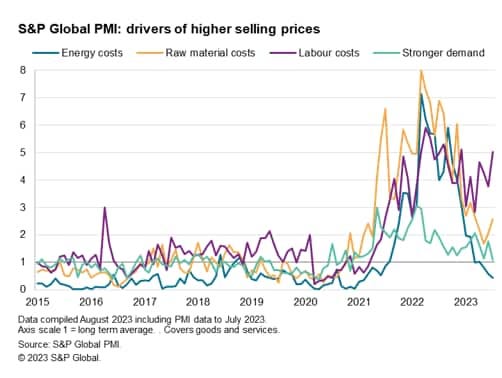

Increasing prices in energy, raw materials, and certain services

One example of this is that NY harbor diesel is running higher, and it often leads US CPI year-over-year.

We expect that we could see inflationary readings closer to what the Cleveland Fed Nowcast is looking for, with a headline reading of 3.42%, core of close to 5%, and month-over-month at about 0.4% for both headline and core.

Prices Rose in July

Looking at July’s commodity pricing we can see a trend of rising prices for many key products, such as wheat, copper, gasoline, and WTIC oil.

Saudi Arabia extended their voluntary production cut of one million barrels per day until September, which may put additional upward pressure on an already tight market.

Any meaningful interruption in supply could also push oil prices quite a bit higher as the SPR is not able to buffer such an event for very long. Because oil is interconnected with just about everything in the global economy, a rising price of oil tends to push up other prices as well. A risk we continue to monitor carefully.

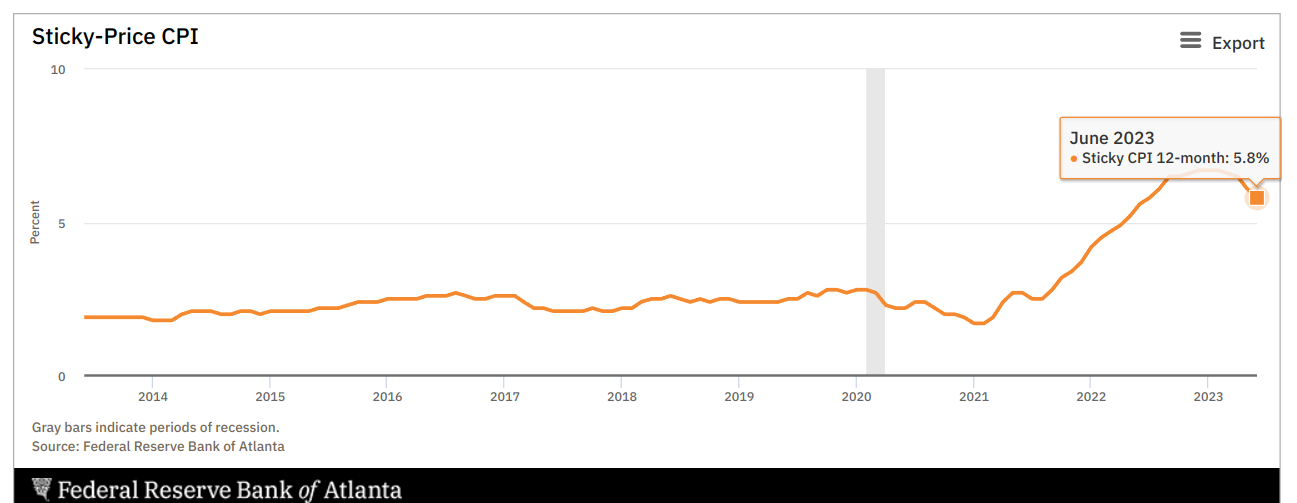

Core Inflation Measures Remain Hot

Sticky-price CPI remains quite elevated, at 5.8% for June, based on the measure from the Atlanta Fed. The basket of prices focuses on slower to move components of inflation, giving a better idea of just how much they are moving without the more volatile components adding noise to the data.

Now let’s take a close look at some of the other potential drivers for July inflation data showing a re-acceleration.

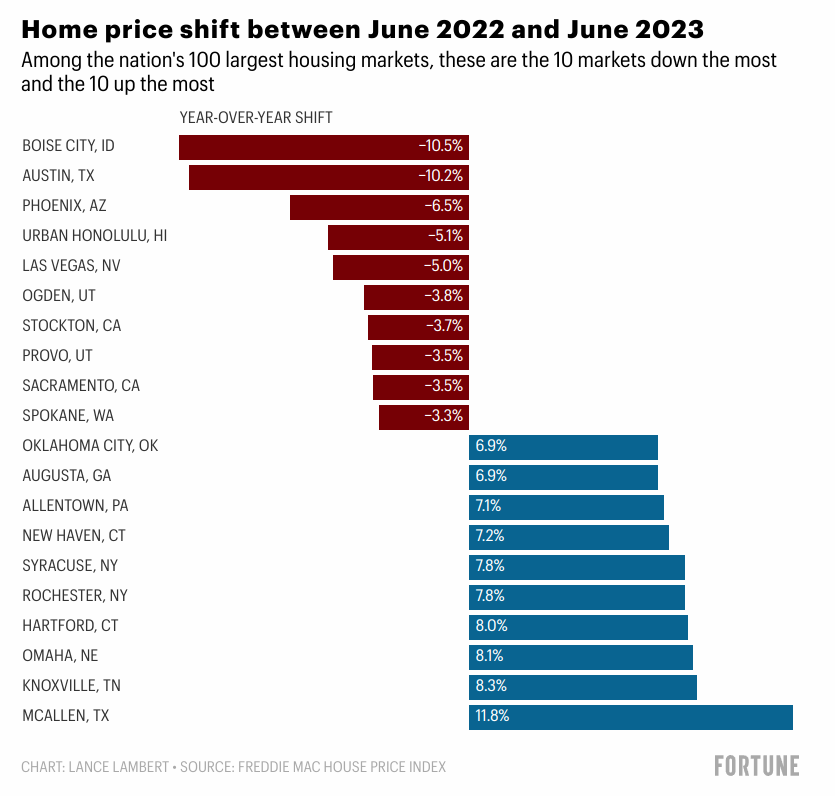

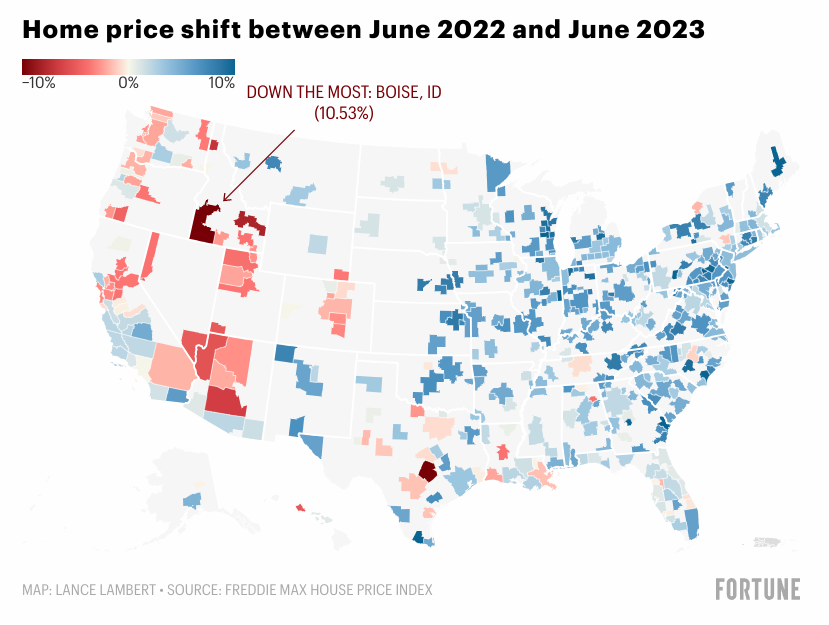

Home Prices Continue to Show Strength in Key Regions

Much of the durability within core inflation has been driven by services, and housing is the largest component of CPI, where prices are a bit of a mixed bag across the country year-over-year.

Much of the gains have been on the east coast and the losses on the west coast.

When looking at an aggregate US national home price index, however, like S&P/Case-Shiller, we can see that in 2023 there has been a re-acceleration of prices. Because the shelter component of US CPI tends to have a lag of about 5-6 months, we expect that we’ll start to see this re-acceleration of prices impact US CPI over the next several readings.

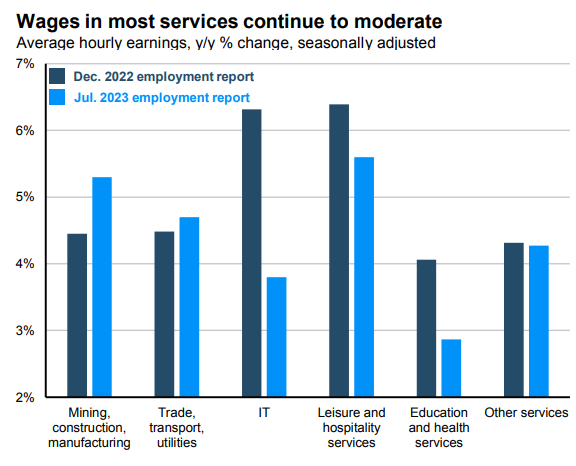

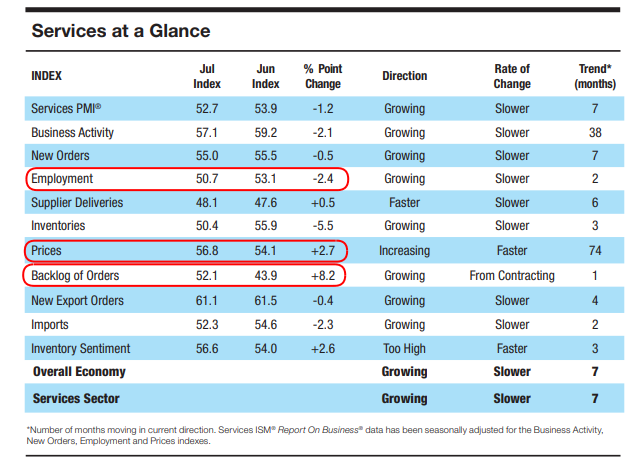

Labor Market Remains Structurally Tight

Another area that has lent upside to prices has been wage growth in the services industry. Fortunately that growth is showing some signs of moderation.

We can see why within US Services PMI data, as the demand for employment has slowed. On the other side of the equation, however, prices and backlogs are on the rise, and those rising prices could impact consumers.

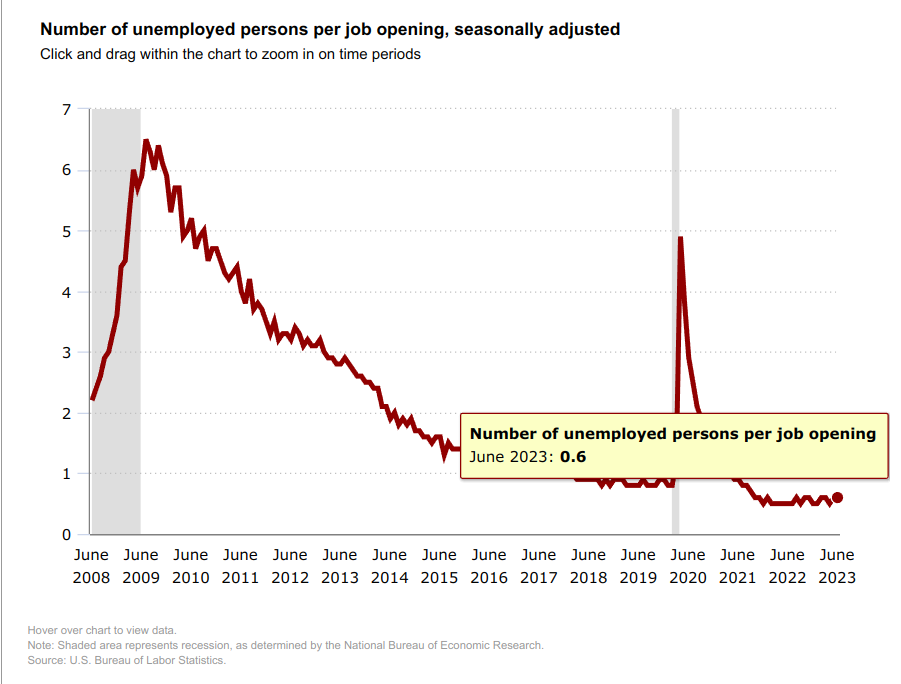

The labor market remains structurally quite tight as well, as there is about 0.6 unemployed persons per job opening based on the latest data. Until this tightness is alleviated, wage growth is likely to remain above long-term trends.

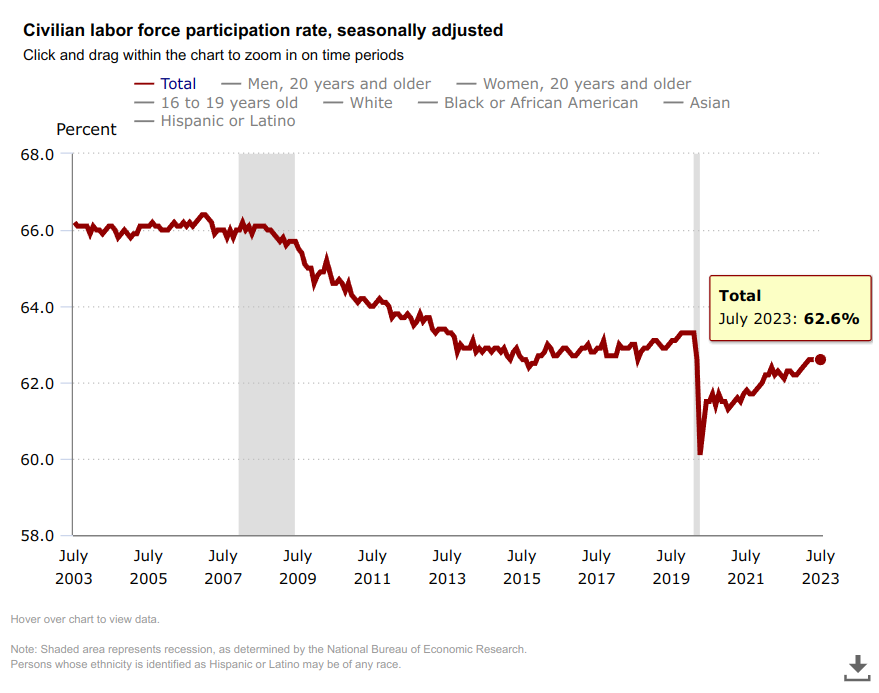

The structural tightness is driven primarily by a very low labor force participation rate. Many 55 and older works retired during COVID and have not returned to work. Chair Powell spoke about concerns regarding early retirement and low labor force participation in those age groups during an earlier Fed press conference, identifying it as an area of concern for the central bank.

Because of this tightness, we re-emphasize that until unemployment rises, we aren’t likely to see hourly earnings growth fall much, and that could also put a floor under US CPI due to the cost push inflationary impacts.

Globally, we can see that labor costs are actually on the rise again, which is another factor that could have an impact on US prices — from any importation of cost push inflation globally.

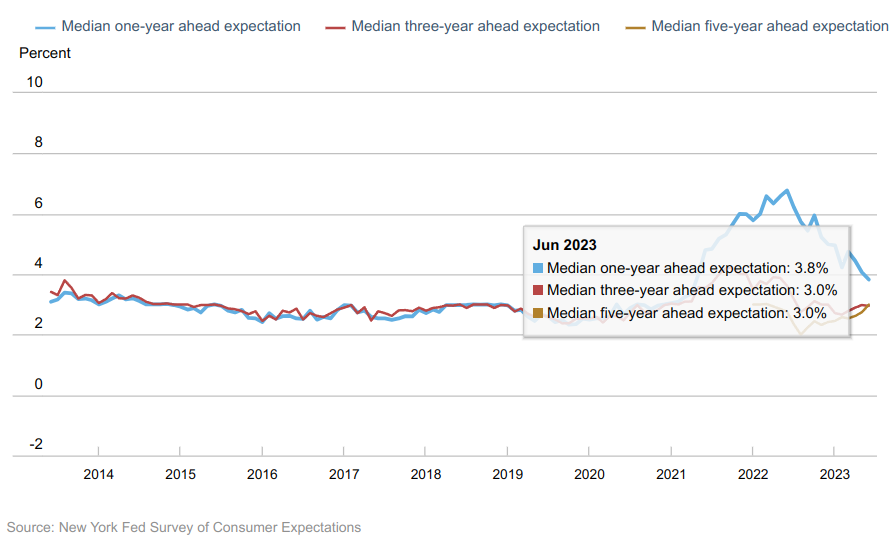

Divergent Views Among Consumers vs Investors

Consumers appear more sanguine about inflation, with one year expectations continuing to fall to 3.8%. Though we do see three and five-year expectations creeping modestly higher to 3%.

Investors seem to be growing a bit more concerned about the potential for inflation as well, piling into TIPS for the first time in a year. TIPS are Treasury Inflation Protected Securities, and inflows tend to happen when there is a heightened concern about rising prices.

Seeing these inflows by investors as consumers become less concerned illustrates the contrasting opinions between the two groups. Whereas consumers are seeing some benefits from slowing inflation, investors are looking forward to the potential of it re-accelerating.

In Closing

We believe that the path towards lower inflation is likely to be rocky. Uneven progress is a theme we should become more acclimated to as the year goes on and we see a resilient economy and demand pressure continue to keep prices more elevated than what the Fed would want to otherwise see.

The mantra of “higher for longer” is beginning to become more applicable as we push right back into a period of concerns regarding inflation prevailing over recession in the near to intermediate term.

Both Ayesha and I will continue to monitor this situation and report on our research and the implications it has on investments and long-term trading as we move throughout 2023 towards its conclusion.

As always if you have any questions or feedback please let us know below in the comments!