Five Banks, Two Stories

The Weekend Edition 182: The BoJ and the Fed are highlights for the week

Five central banks meet across six days this week, spanning three continents and almost every point on the monetary policy compass. We have the BoJ and the RBA on Tuesday, the Fed on Wednesday, the BoE on Thursday, and the PBoC on Sunday.

The two meetings that matter are in Tokyo on Tuesday and Washington on Wednesday. Together they represent the sharpest tension in global markets right now: a central bank hiking into political uncertainty with a currency it cannot defend, and a new Fed chair holding rates while the case for tightening builds around him.

The backdrop that binds all five banks is the Middle East conflict, now in its fourth month, which has pushed oil prices higher and complicated the inflation calculus for every major economy. Fiscal policy is pulling in different directions, with Japan leaning expansionary while the US debates the scale of its deficit. Underneath all of it sits the Fed, which has had its rate path repriced almost entirely in a matter of weeks, from a story of cuts to a story of hikes. That shift changes the gravitational pull for every other central bank on this list.

Japan: When a Hike Isn’t Hawkish

The rate hike to 1% is the least interesting thing about this meeting.

With OIS markets pricing it above 90% and 53 of 55 economists in agreement, the June 16 decision is about as close to a done deal as central banking gets. Governor Ueda spent his June 3 speech laying the groundwork, echoing almost word for word the language he used before December’s hike, and several board members followed in quick succession with increasingly hawkish signals.

So the hike lands. The question is whether it means anything.

Why Now

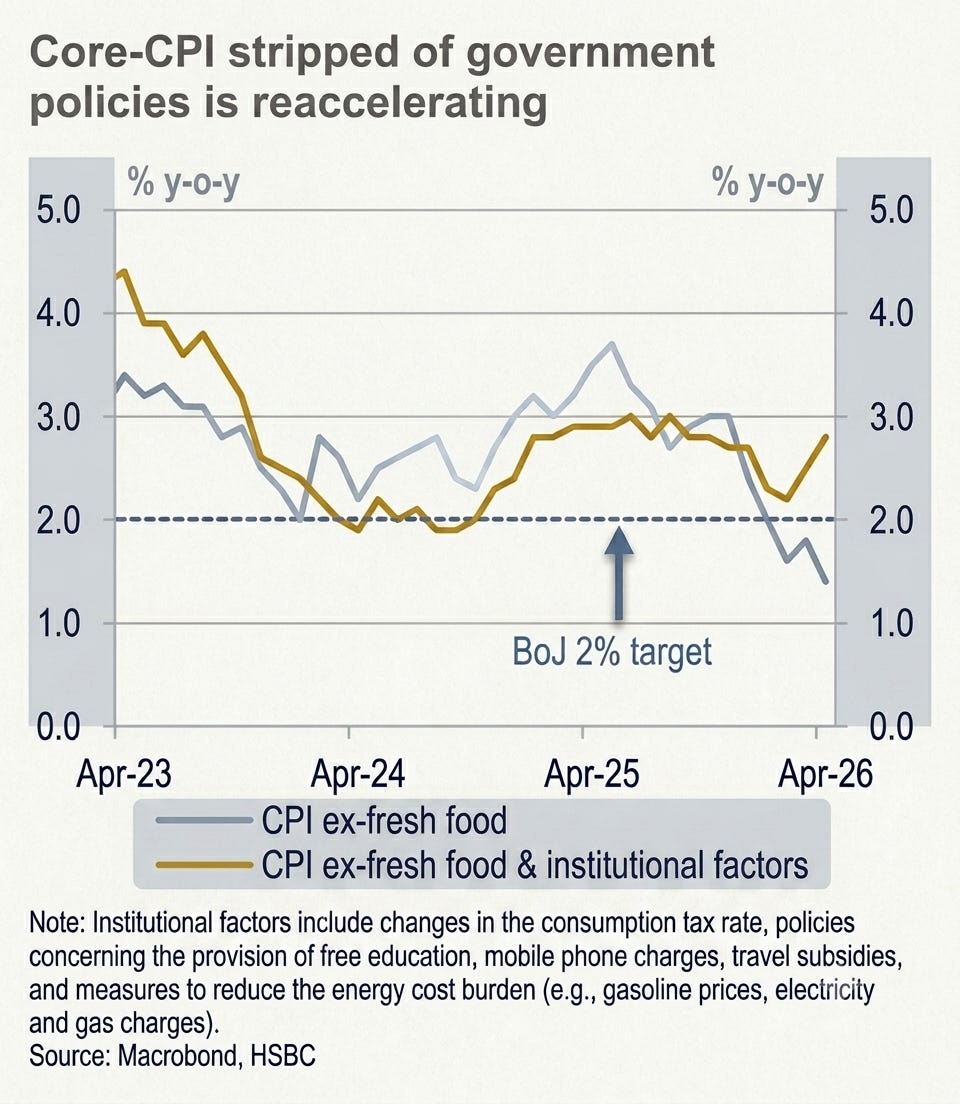

Two forces have converged to make a June hike almost unavoidable. Government subsidies have kept headline CPI relatively contained, but strip those out and core inflation adjusted for institutional factors has been rising steadily since the conflict began, reaching 2.8% year on year in April against just 1.4% for standard core CPI. At the same time, USD/JPY has climbed back above ¥160, a level Japan’s authorities have repeatedly signaled as a line they are uncomfortable with, compounding inflation through import costs and drawing pointed commentary from Washington.

The QT Problem

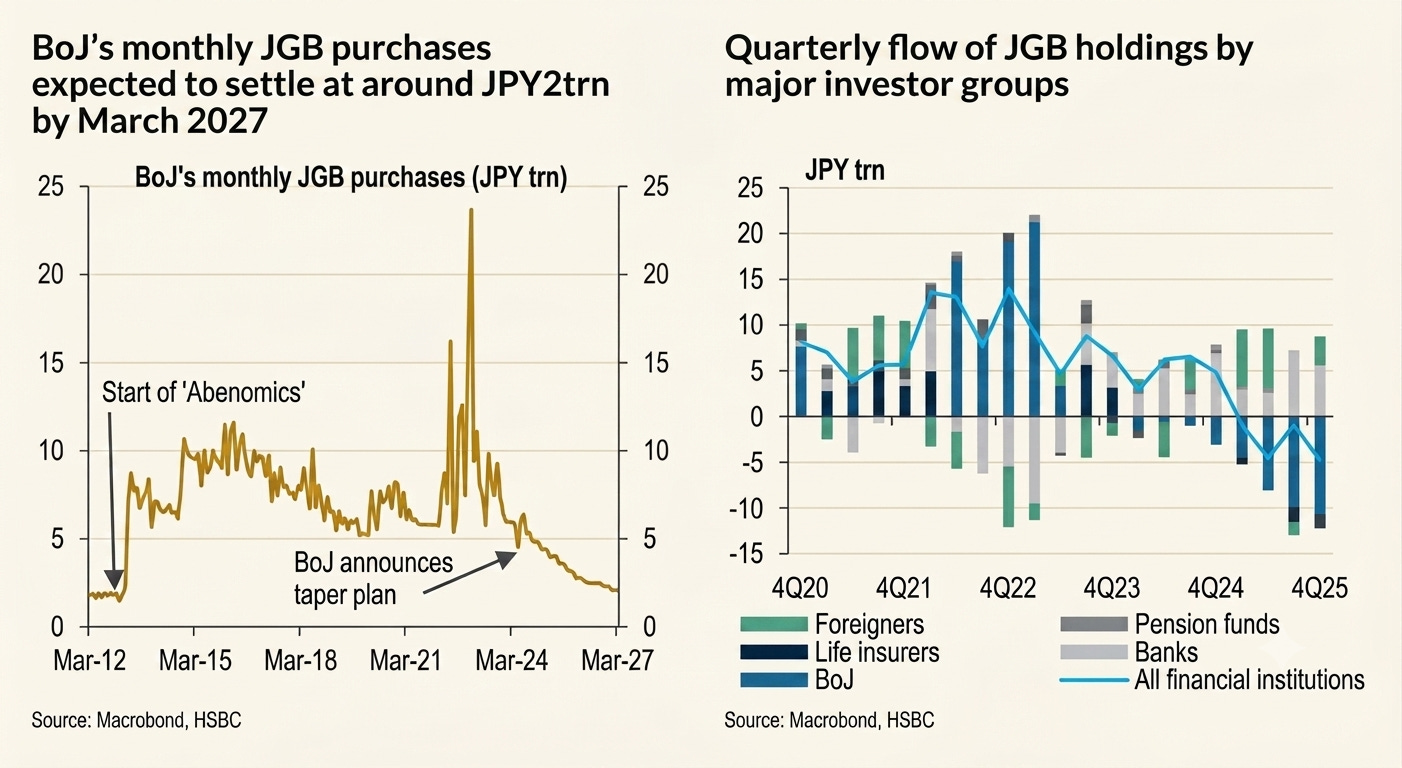

Multiple media outlets are reporting that the BoJ is leaning toward halting further bond purchase reductions after March 2027, keeping monthly JGB purchases at around ¥2.1 trillion. I think this would be a mistake in terms of signaling. If the bank raises rates with one hand while stepping back from balance sheet normalization with the other, the net read is dovish, placing enormous pressure on December’s meeting to compensate.

There is also a political dimension that cannot be ignored. A decision to freeze QT alongside the Takaichi administration’s expansionary fiscal agenda risks cementing a narrative that the BoJ is willing to accommodate rather than confront. That is the last message a central bank trying to defend the yen needs to send.

The Politics

Prime Minister Sanae Takaichi is a well-known reflationist who built her political career arguing against premature monetary tightening. Since her administration took office last October, hike expectations and yen weakness have paradoxically moved up together, suggesting markets believe the BoJ will be forced into larger hikes later rather than gradual ones now.

Into this environment steps Toichiro Asada, the newest board member appointed by the Takaichi administration in April. He is an academic economist with a history of advocating reflationary policy, and he has never voted before. If he dissents against the hike, markets will read it as evidence that political influence over the BoJ is growing, which would be bad for the yen and JGBs simultaneously.

Adding to the complexity, Governor Ueda is hospitalized. Deputy Governor Himino will chair the meeting while Uchida takes the press conference, an unusual configuration that adds communication risk at exactly the wrong moment. The Japanese government also retains a legal right to request that any vote be deferred, a power used exactly once since 1998. Most analysts put the probability of it being exercised below 10%, but in a week where the communication chain is already fragile, the tail risk matters.

What It Means for Investors

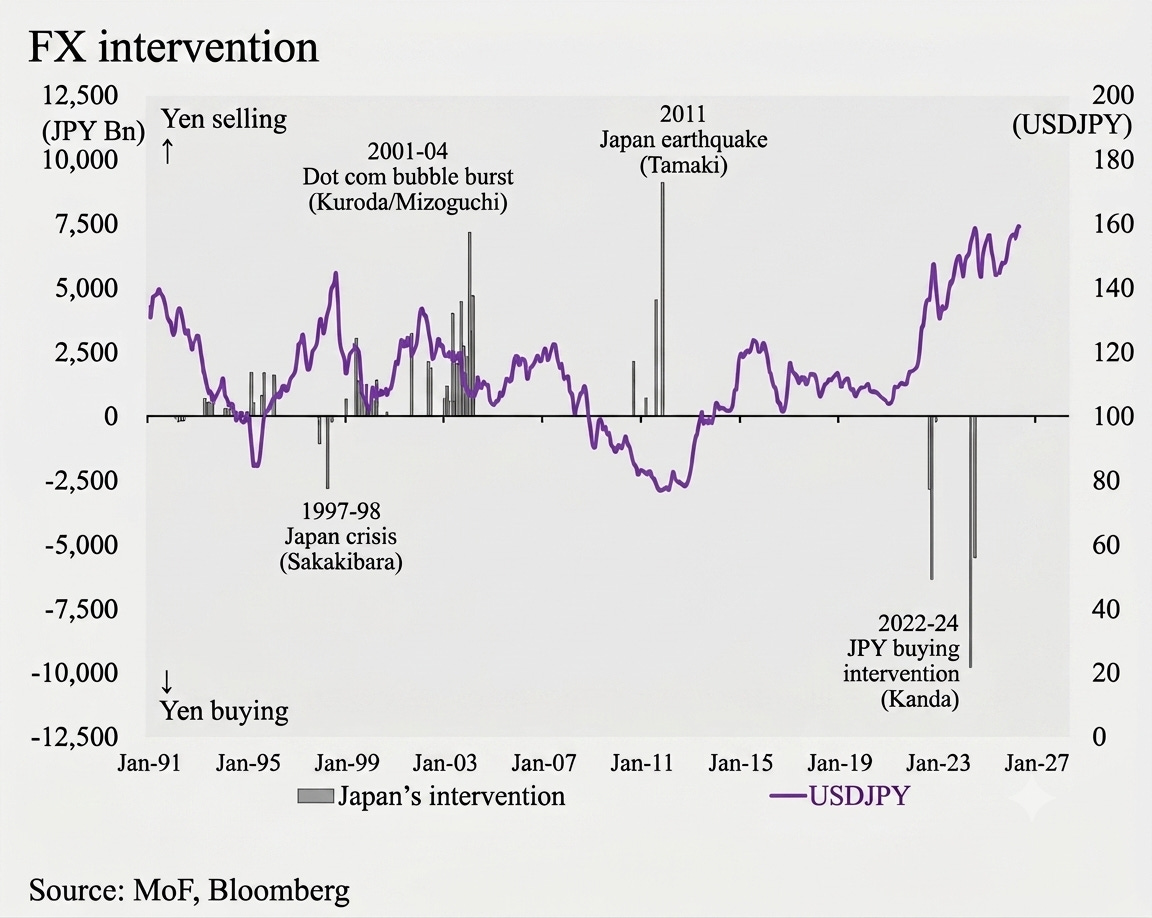

The dynamics that produced the dramatic yen rally in July 2024 are entirely absent here. Back then, both the hike and the intervention were surprises, and weak US jobs data pushed the Fed toward cuts simultaneously. This time the hike is priced, intervention is anticipated, and following the strong June 5 jobs report the Fed is being priced for hikes, not cuts.

This is a poor risk/reward setup for Japanese equities. The downside scenario, a taper pause that reads as dovish, a stumble in communication, or an Asada dissent, carries real correction risk for a market heavily concentrated in AI and semiconductor names. Watch the press conference more than the decision, and watch the yen, not the Nikkei, for the real signal of how this week is being read.

The Fed: Patience or Paralysis?

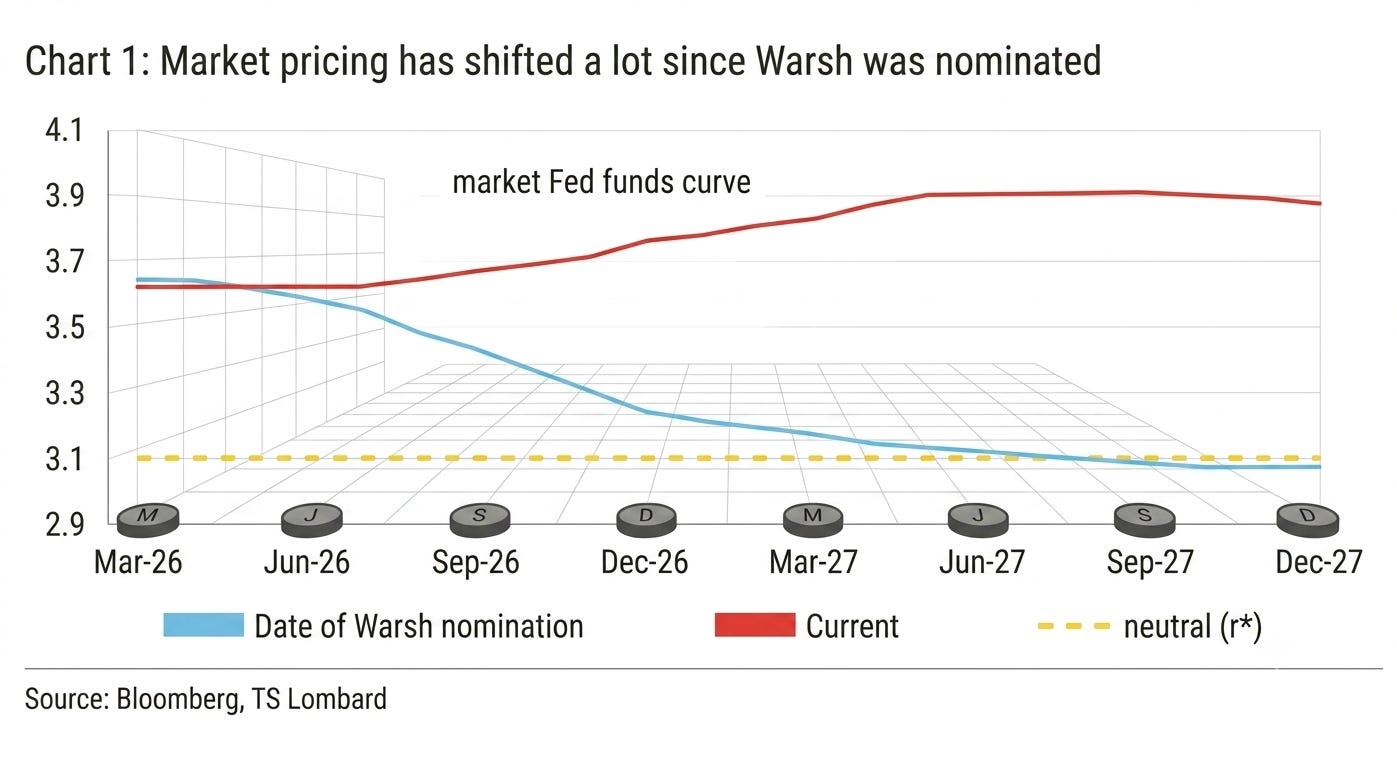

Kevin Warsh chairs his first FOMC meeting on Wednesday, and the world he is walking into looks nothing like the one he was hired to manage.

When Warsh was nominated, markets were pricing the Fed for cuts. The assumption was that his job was to deliver rate reductions the administration wanted while using his hawkish reputation as cover. That assumption has been completely destroyed, with the same swaps market that was pricing three cuts at the start of the year now pricing a hike by year-end.

The Data Changed the Story

Inflation has run above the Fed’s 2% target for five consecutive years, and the direction of travel has recently worsened. The Middle East conflict has added roughly a percentage point to headline prices through energy costs, supercore services inflation has reaccelerated, and the May jobs report delivered a clear beat with payrolls comfortably above estimates and unemployment holding at 4.3%. A strong labor market on top of stubborn inflation closes the door on the transitory argument several FOMC members had been clinging to.

The Warsh Dilemma

Despite his reputation as a hawk from his earlier FOMC stint, Warsh has spent the past several years constructing arguments for lower rates, centered on the idea that AI-driven productivity gains allow the economy to expand without generating capacity pressures. The theory holds that the neutral rate is lower than the Fed thinks and current policy is therefore more restrictive than it appears. It is a seductive argument, but it is hardest to defend when payrolls are accelerating and inflation is running at 3%.

What Warsh actually does this week is hold rates. The dot plot, however, will almost certainly show fewer cuts penciled in for 2026 and some dots pointing to a hike this year. Whether Warsh endorses that shift in his press conference or tries to soften it will define how this meeting is read by markets.

What It Means for Investors

Equity valuations are stretched and leveraged positioning in AI-related names is elevated. The repricing of Fed expectations that began Friday, when the S&P fell 2.6% and the Nasdaq 100 fell 4.8%, has not fully worked through the system. A hold with a hawkish dot plot is the most likely outcome, and that is not what markets are positioned for.

The question is not whether Warsh hikes this week. He does not. The question is whether he signals they are coming, and on current data he can no longer credibly pretend they are not.

What This Week Tells Us

This is a week that will tell investors a great deal about how the next 18 months unfold. Japan is hiking into political uncertainty with a yen that will not stay strong regardless. The Fed is sitting on its hands while the case for tightening builds under its new chair.

The common thread is that the easy part of the global rate cycle is over. Synchronized hiking and the expected synchronized cutting that followed have given way to something messier: genuine divergence, with each central bank making difficult calls where the margin for error is thin.

For global investors, the key variable to watch is not any individual decision this week. It is whether rising Fed hike expectations, a weakening yen, and stubborn inflation can coexist without triggering the kind of cross-asset dislocation that compressed volatility has been masking. Friday’s equity selloff was a warning shot. This week’s meetings will determine whether it was the start of something larger or simply a moment of recalibration.

This newsletter is for informational purposes only and does not constitute investment advice.