This week we have another busy schedule of earnings releases to watch, with plenty of interesting companies reporting. Before we get to that, let’s talk about the week that was.

Recapping Last Week

Starting off with a recap of the previous week with the scorecards of the S&P 500 and the Nasdaq-100.

Summary of the Stats:

Reporting: SPX 98% done; NDX 94% done

Blended Earnings Growth: SPX -4.15%; NDX +16.94%

Actual Earnings Growth: SPX -4.32% (prior -5.55%); NDX 17.30% (prior +13.35%)

S&P 500 Sectors: Best - Consumer Discretionary; Worst - Energy

The Nasdaq-100 posted much better growth numbers compared to the S&P500. Even the % positive price reaction is higher. The worst sector was Energy Minerals which is only Diamondback Energy (FANG) and the best sector was Industrial Services which is only Baker Hughes (BKR).

This Week’s Earnings

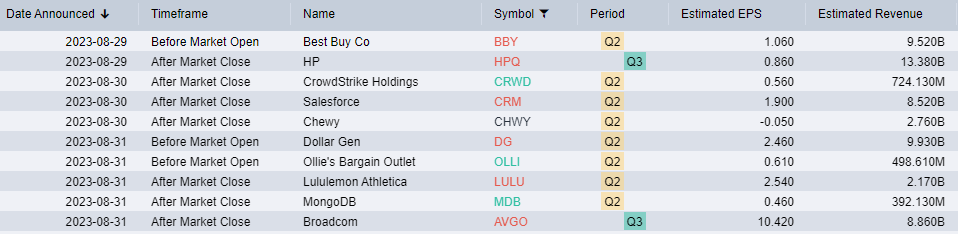

Lululemon (LULU)

Lululemon is still a story stock and I wouldn’t bet against them. We are likely to see some sequential slowdown in earnings this quarter. However, YoY estimates are still +15% for EPS and +16% in sales.

This is being driven by three factors:

Improved inventory management

Stable demand from consumers

Growth in China - 2/3rds of their stores were opened since 2019 and they believe they will see a ramp up in consumption this year

While the first may be true, the second two are suspect. We know that discretionary spending is declining and without discounts, Lulu is likely to see a decline in revenues.

I would be very interested however, to understand how overseas and China is doing. Lulu is trying to maintain a policy of being a premium brand in these countries and is not giving out discounts.

The other update I would be looking out for is Mirror. They have been trying to sell Mirror, the fitness equipment maker, that they acquired for $500m in 2020. They took a $443m impairment in Q4 on this acquisition.

Best Buy (BBY)

Analysts are not expecting a great quarter but, are saying that this may be their trough earnings. While I agree that Q3 may get a bump from back-to-school spending, I don’t think Best Buy sees massive increases in revenue for the rest of the year.

Goods spending has declined significantly and we see that in the PCE numbers. Refresh cycles will become longer and all that pull forward sales during the pandemic will mean lower revenues.

Discretionary items and particularly white goods will likely see muted demand. As will electronics and phones.

Q2 guidance was lowered but full year guidance was reiterated. They did however discuss an increase of $225 million due to employee incentives and back in April they cut in-store employees to manage expenses. I think tough times are catching up on them and we see them turnaround in 2024.

Ollie’s Bargain (OLLI)

Ollie’s raised revenue and guidance last quarter but shares sold off post earnings quite likely because of sympathy selling. They’ve actually managed to keep theft under check better than their competitors and they’ve done a better job holding onto margins. I suppose people realized this because shares have rallied since last earnings.

I would put this on a watch list if we see an ugly sell-off, which could very well be the case again this quarter because of the general retail sell-off we’re seeing.

Analyst estimates are very optimistic with a growth of +177% YoY in EPS estimate and +10.3% YoY growth in revenues.

Chewy (CHWY)

Chewy was on the right track last year. They were expanding their category offerings, adding pet health care and expanding overseas. While all of this still continues, unfortunately the macro seems to have caught up with them. The era of discretionary internet spending coming to a halt has been weighing on them.

Nevertheless, last quarter they did manage to churn out decent results adding to net subscriber growth. But, they also discussed having no margin expansion this year and put out cautious growth estimates. They talked about expanding to Canada in Q3, but it would also seem like these overseas expansions have been weighing on them.

I like this company but I can’t get a good read on them this quarter. Looking at the technicals and the chart, they don’t look constructive and I would hold off on being bullish on them for now.

Dollar General (DG)

The “Dollar” stores are not having a good run. Dollar Tree reported disappointing results this quarter and seeing as how Dollar General is weaker than Dollar Tree, I don’t have high hopes for them this quarter either.

Last quarter, they posted a double miss and guided down. They also suspended their buybacks where the expectation was for at least $500m. They announced a reduction in store openings to cut capex given that they already have $7.2B of debt on the books. They’ve also been doing a lot of promotional activity which leads to lower margins. So, they recognize the issues and they are trying to improve.

The stock hit a 52-week low and since then has not really recovered. They have been downgraded to a HOLD by most analysts and this quarter EPS estimates are -16.9% YoY.

I suspect this quarter they discuss an increase in theft as well, just like the other retailers have been doing.

I think with these companies we just to ride out the storm before we can think about buying because cheap can always get cheaper.

Hewlett-Packard (HPQ)

The street expects sales to begin increasing again quarter-over-quarter, but at a modest pace. This still leaves the company below last years top and bottom line based on current expectations with Q3 EPS expected at $0.86 vs $1.04 last year and revenue of $13.3B vs $14.6B last year.

The entire PC industry has seen a staggering slowdown year-over-year that’s expected to bottom out and reverse in Q3. HP’s earnings will be interesting to watch for signs as to how it may be stabilizing here. Sales have been aggressive from HPQ and their peers over the last several months, which may mean an increased top line but decreased bottom line.

Crowdstrike (CRWD)

Estimates are for flat quarter-over-quarter earnings growth, but modest sales growth. Year-over-year expectations, however, are more impressive. Crowdstrike made $0.36 during 2022 Q3, and this year analysts are projecting $0.56 EPS. Revenue is projected to grow from $535M in Q3 2022 to $724M in Q3 2023.

Crowdstrike spends aggressively on R&D, but manages to have a sizable free cash flow margin. The company maintains a competitive advantage in XDR. With cybersecurity threats are on the rise, becoming more sophisticated, and dangerous, we feel that there are tailwinds for Crowdstrike’s offerings and the entire space. This earnings report and any guidance will give us further clues as to just how strong demand is for cybersecurity as a service.

Salesforce (CRM)

Salesforce is expected to grow from $1.19 EPS in Q2 of 2022 to $1.90 in Q2 of 2023, with revenues rising from $7.7B to $8.5B. Backlogs are expected to grow by about $2.9B year-over-year. The company is seeing slowing growth in the US by 1.2% year-over-year. Though growth in the UK (+7% year-over-year) and Canada (+3.6% year-over-year) are helping to offset that.

Salesforce continues to invest aggressively in AI, including both for its own technology and in startups within the space. The company recently forecast that AI could help to drive $194B of online sales using predictive technology to and generative tools to increase sales.

Broadcom (AVGO)

Broadcom is expected to report $10.43 EPS vs $9.73 in Q3 of 2022. With revenue expected to come in at $8.85B vs $8.46B. Wireless and wired infrastructure are expected to lead sales growth with industrial and automotive as well as enterprise storage lagging.

AI is contributing to up to 15% of semiconductor sales, up from 10% FY2022 and expected to increase to over 25% during FY2024. Wireless demand is also likely to increase as we see the iPhone 15 launch approach. We may hear about both subjects as a part of guidance.

MongoDB (MDB)

Analysts expect EPS of $0.46 vs -$0.23 Q2 2022, with revenue growing to $394M from $304M during the same period year-over-year. Subscribers are expected to grow from 37,000 to 44,469 during the same period. Backlog value is expected to be approximately $54.5M, falling slightly quarter-over-quarter from $57.9M.

The company’s database structure is well-suited for deep learning and large data sets, offering greater scalability and better cost containment. MongoDB also recently introduced end-to-end encryption to their platform as they attempt to address a growing need for both security and privacy by companies using their products. Their earnings will provide valuable insights into not only the company’s health, but also for the demand for commercialized database storage, a heuristic for how much tech’s storage needs are growing.

In Closing

Next earnings season’s peak may be well ahead of us, however there’s plenty of excitement ahead this week as we have many companies to watch, both for their own earnings and how their earnings reports, conference calls, and guidance may impact market sentiment and give us clues on their industries, sectors, and the broader economy.

If you have any questions or feedback, let us know in the comments below. Have a great week!