I held off writing this article for this week in anticipation of the Senior Loan Officers’ Opinions Survey (SLOOS) Report. But, the SLOOS really didn’t tell us anything we didn’t already expect. Nevertheless, it’s always important to look into the data and see how trends are progressing.

Companies

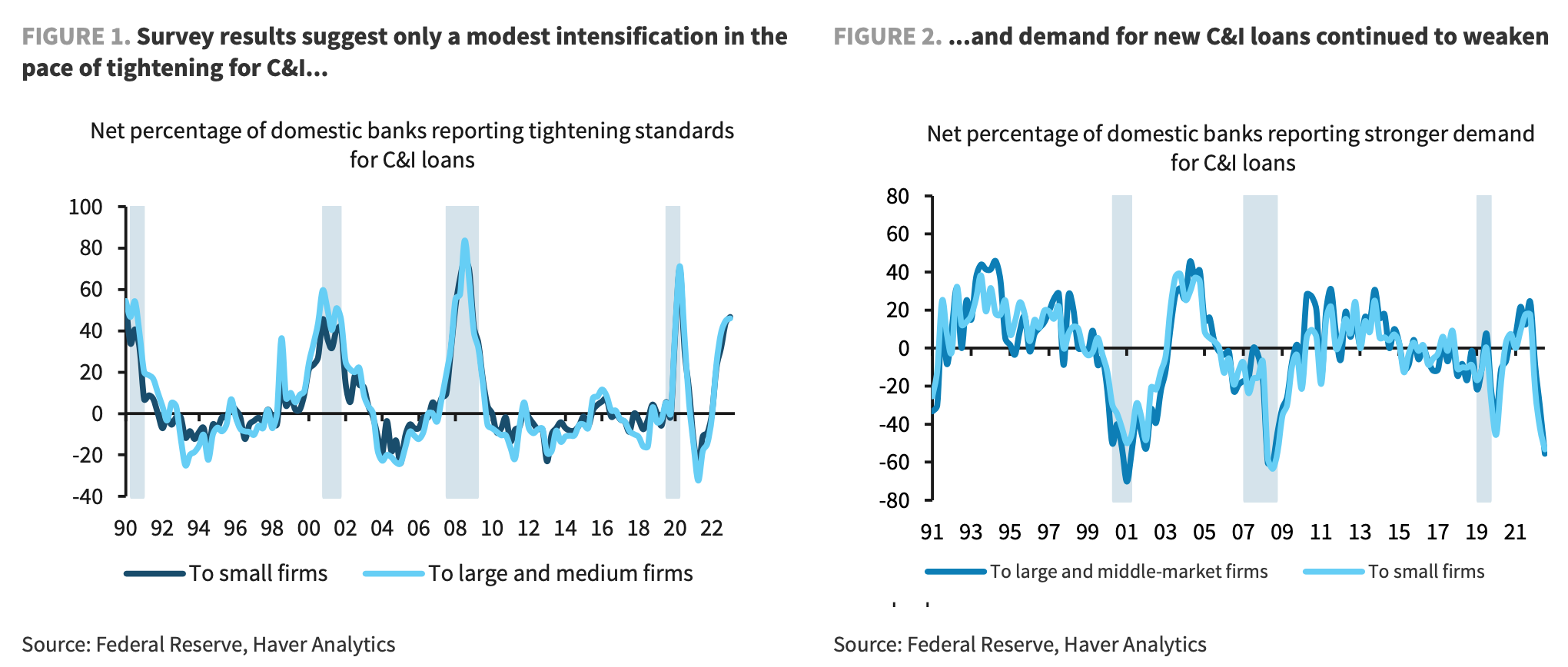

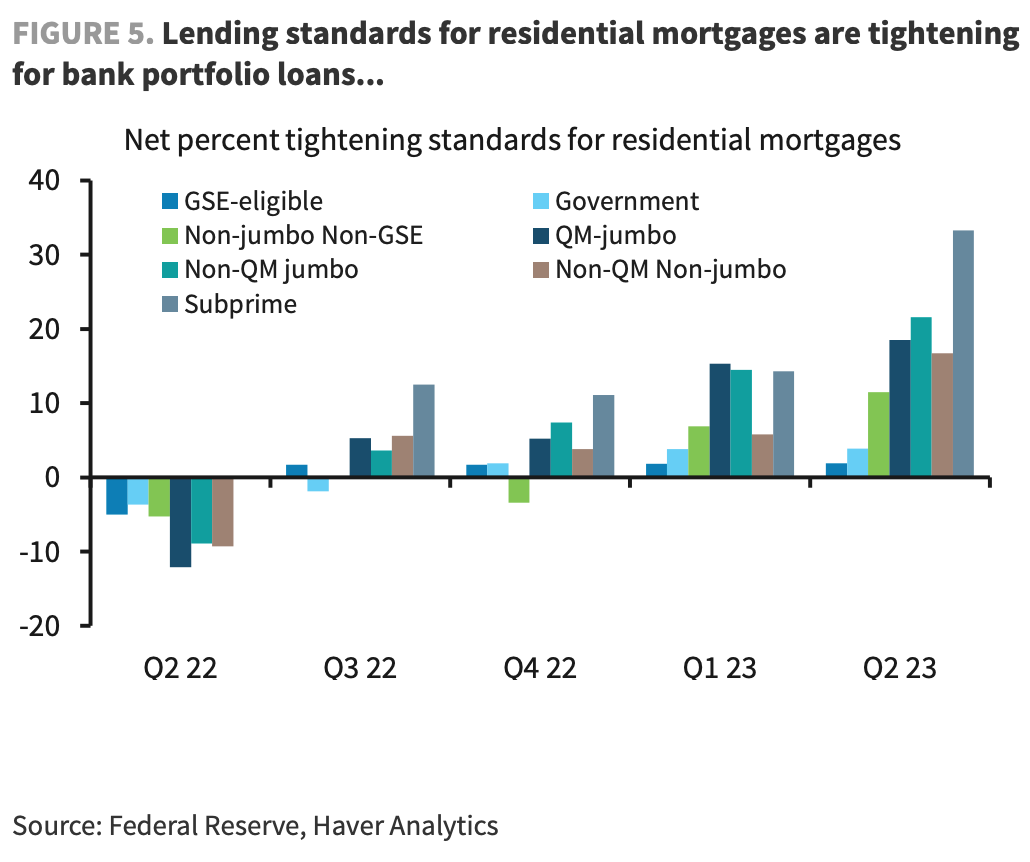

Lending standards have been tightening for a while and after the recent bank collapses, they have tightened further. As also expected, lending standards for smaller companies are tightening further.

While you can’t really make this distinction in the first chart above, the numbers tell you so. The change for large firms was 44.8% to 46% while for small firms it was 43.8% to 46.7%.

The second chart is quite alarming and it shows that loan demand has fallen the most since the Great Financial Crisis. Now, it’s hard to say whether companies are actually pulling back from demanding loans because they don’t need it or want it, or whether it’s because the banks won’t lend to them. Whatever the reasons may be, loan demand falling to these levels combined with tighter lending standards have occurred mostly during past recessions, as you can see from the shaded areas.

Next we look at real estate.

Real Estate and Housing

Mayhem wrote an article on real estate some time back and I wanted to provide an update to what we’ve been seeing since then, particularly in respect to lending conditions and the SLOOS.

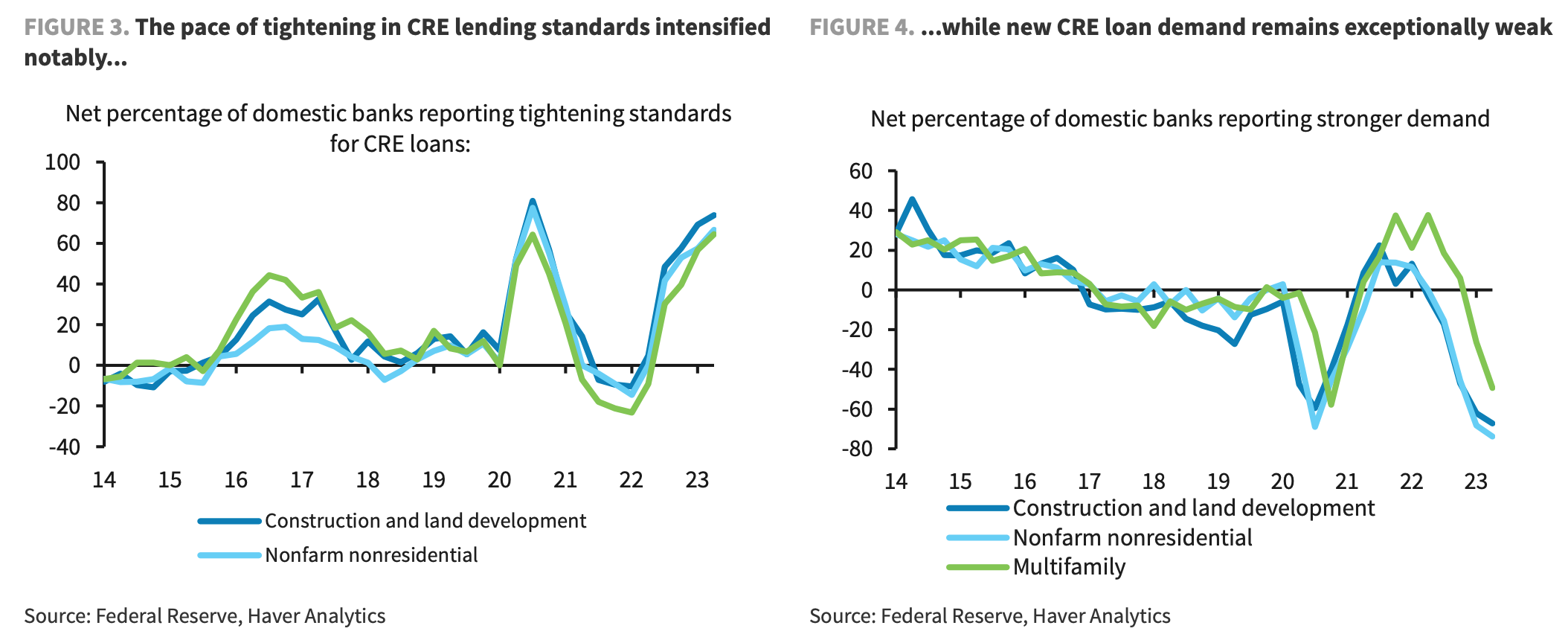

We’ve been hearing a lot of chatter about the state of commercial real estate. In fact, there were special questions in this time's SLOOS focusing on CRE.

CRE lending conditions

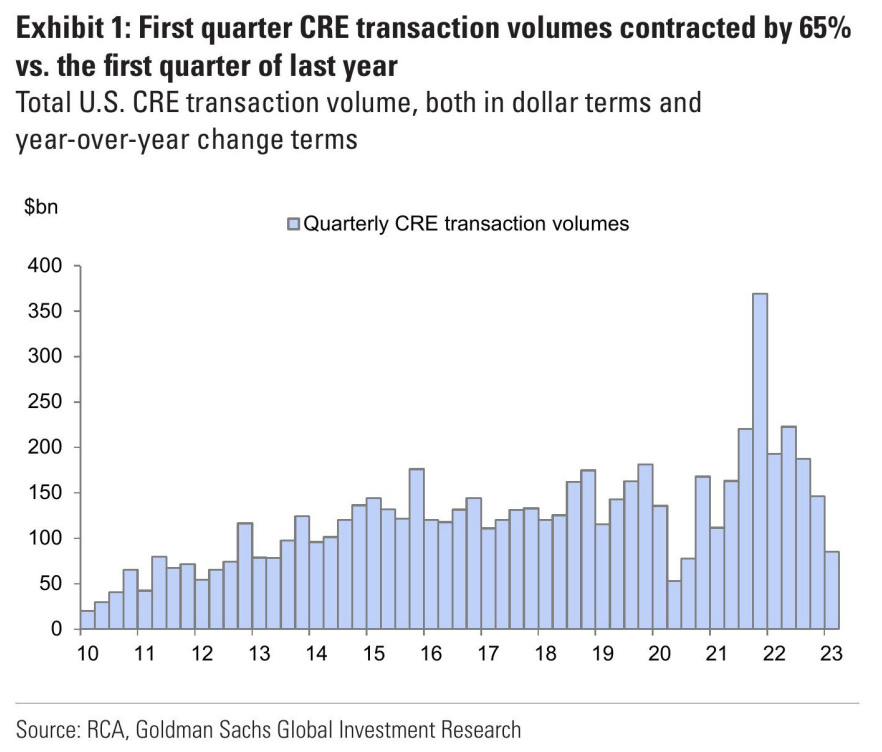

As with corporate borrowers, lending conditions have tightened and loan demand has dropped.

As a consequence of this, there have been fewer CRE transactions.

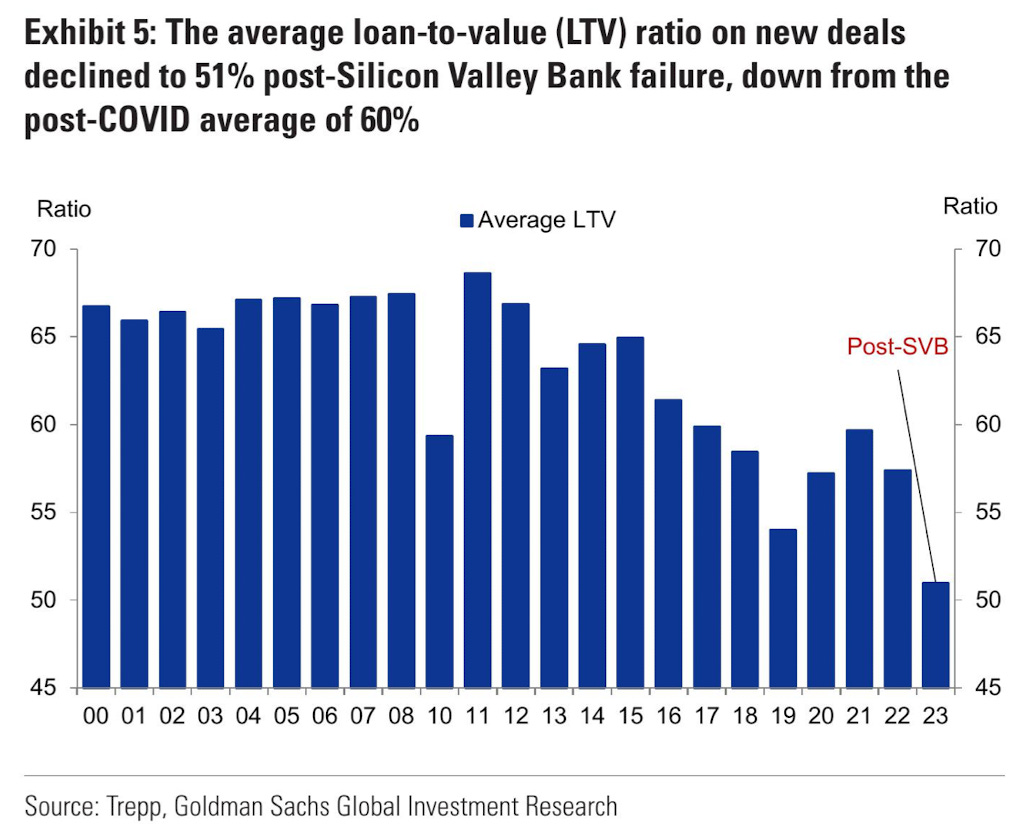

Banks are asking for better and higher collateral values, i.e., the size of the loans are lower compared to asset value, higher proportion of cash flows for payments (debt service coverage levels), and tighter conditions in general.

The average loan-to-value is now 51%.

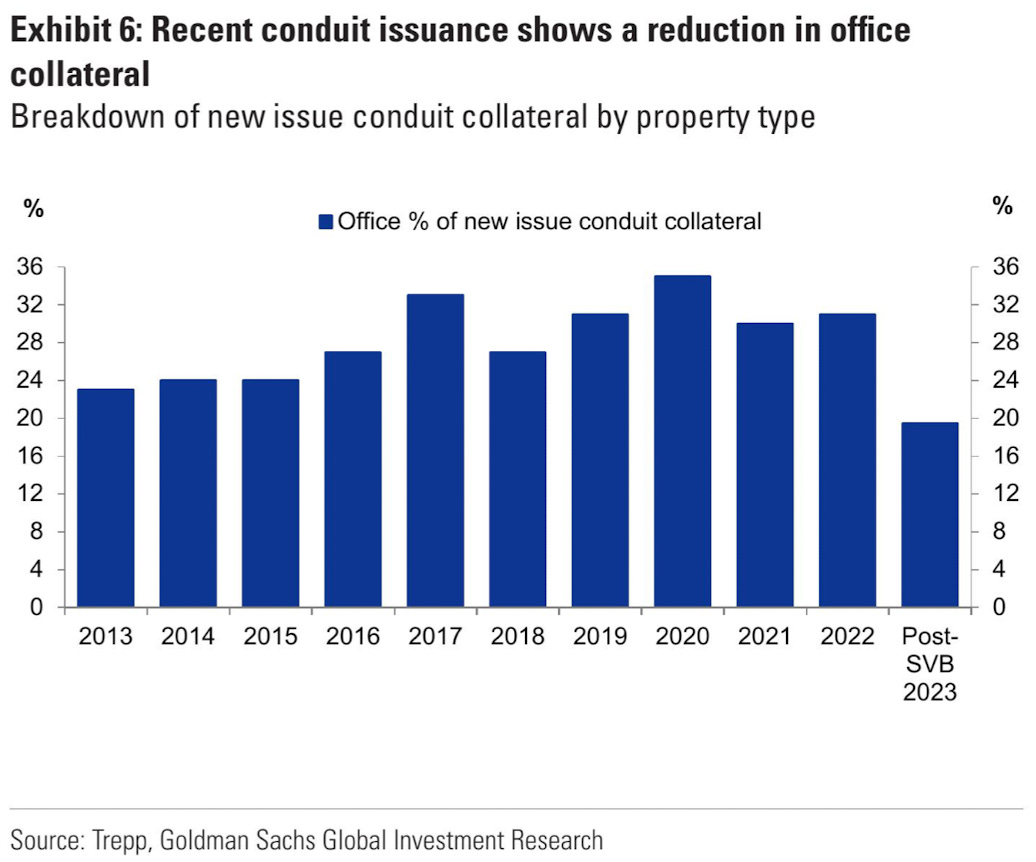

And because office buildings are now being seen as a major risk, fewer office properties are being taken as collateral.

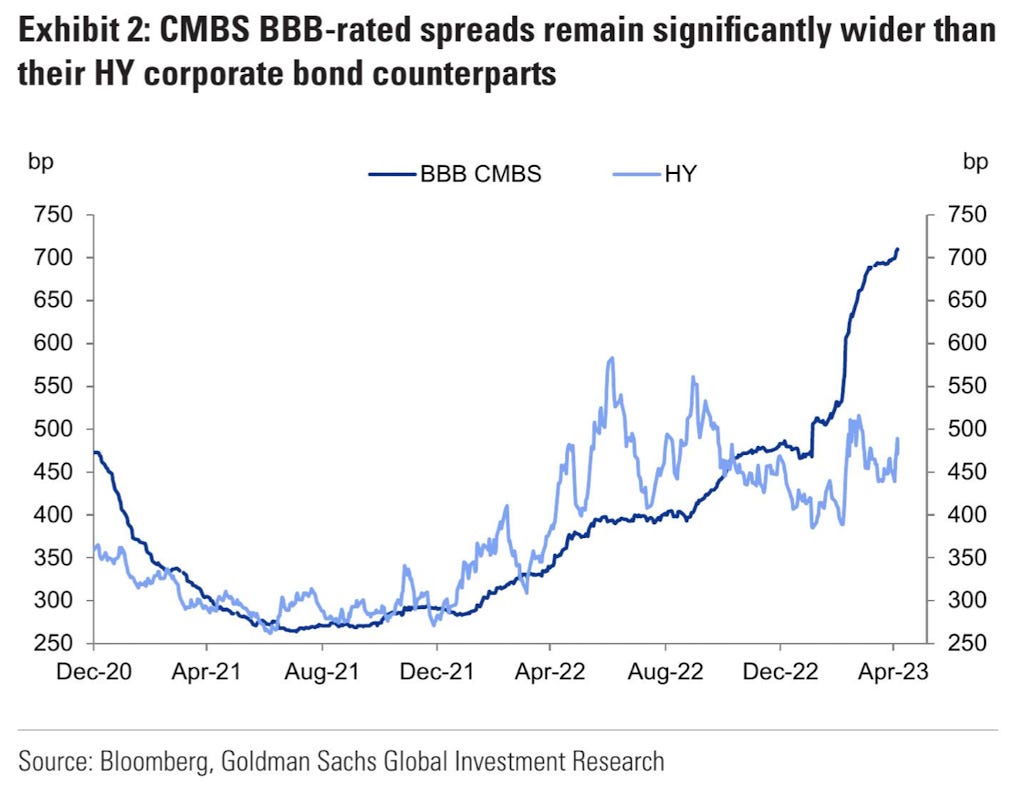

Loan Pricing

Loan pricing for the commercial real estate sector certainly remains high when compared to companies. If we look at the spreads of High Yield Credit (HY), which is perhaps the costliest form of corporate debt, and compare them to Commercial Mortgage-Backed Securities (CMBS), we see can see the difference.

Even a similar grade of CMBS (BBB-rated) is priced much higher than HY.

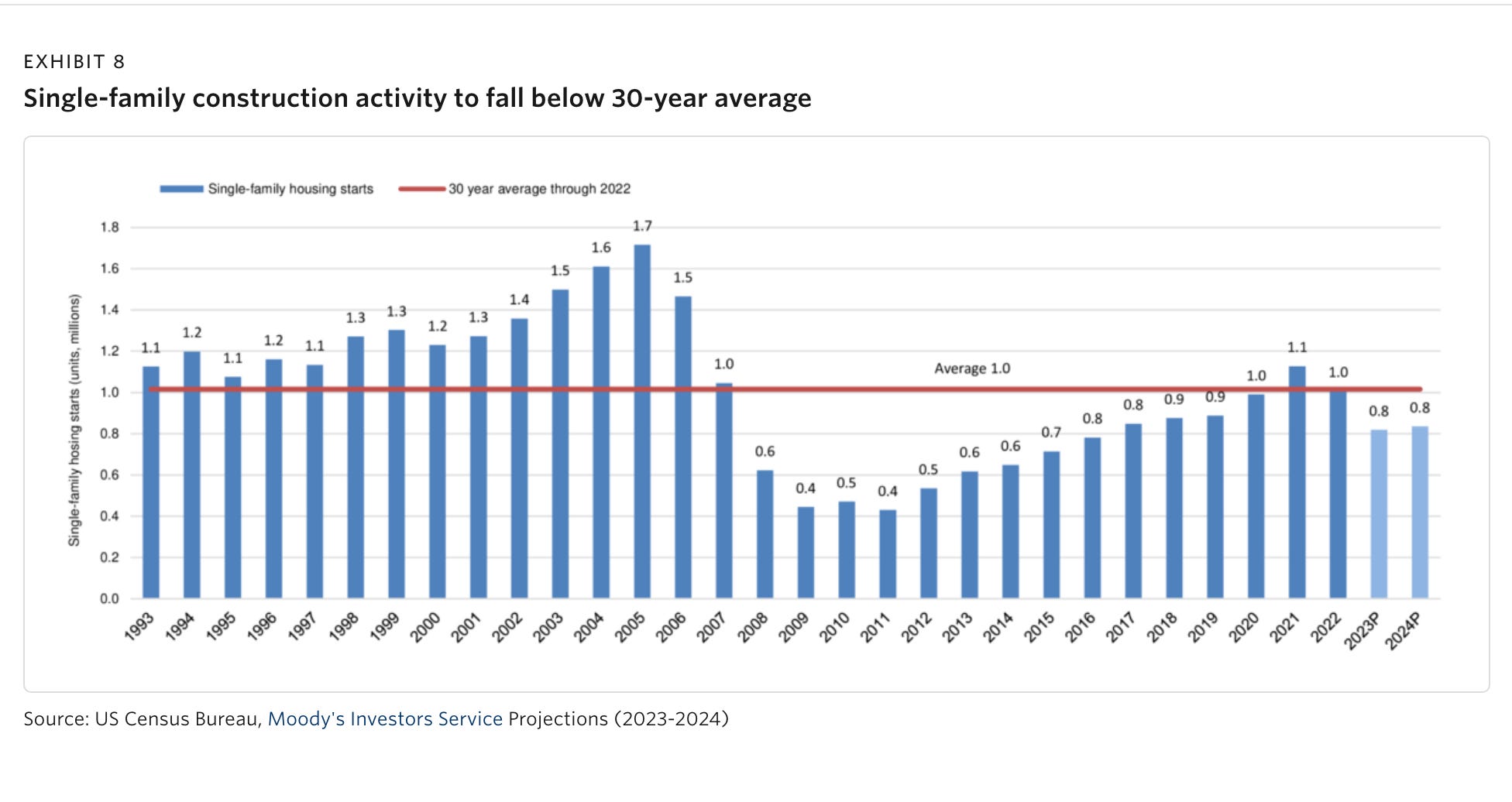

Construction Loans

Construction loans are also declining. The problem with pure construction loans is that during the construction phase there are no cash flows or collateral so they are definitely more risky and more costly. Again, whether it’s the companies passing on the projects or the banks not lending, the end result is the same - we’re seeing construction activity fall off significantly.

This however, presents a conundrum. The Fed sees a bubble in the housing market, which they want to pop. Unfortunately, the housing market in the US already has a shortage - part of the reason prices remain elevated. And with single-family construction declining, we’re going to see even further shortages. This is bound to keep prices somewhat high over the next few years.

Residential Lending Standards

Finally, residential lending. We all know that mortgage lending has declined but so has home equity lines of credit (HELOCs). The January SLOOS report had already emphasized the issue of HELOCs and it just seems to be getting worse. This stems from the time of the Great Financial Crisis when asset values fell so drastically that no equity was left in the homes. Banks certainly don’t want to be burned again.

And here’s perhaps how the Fed hopes to pop that housing bubble. Demand will be destroyed because of the unavailability of mortgages or the high cost of mortgages and the elevated prices due to the shortage in housing will price potential homeowners out of the market.

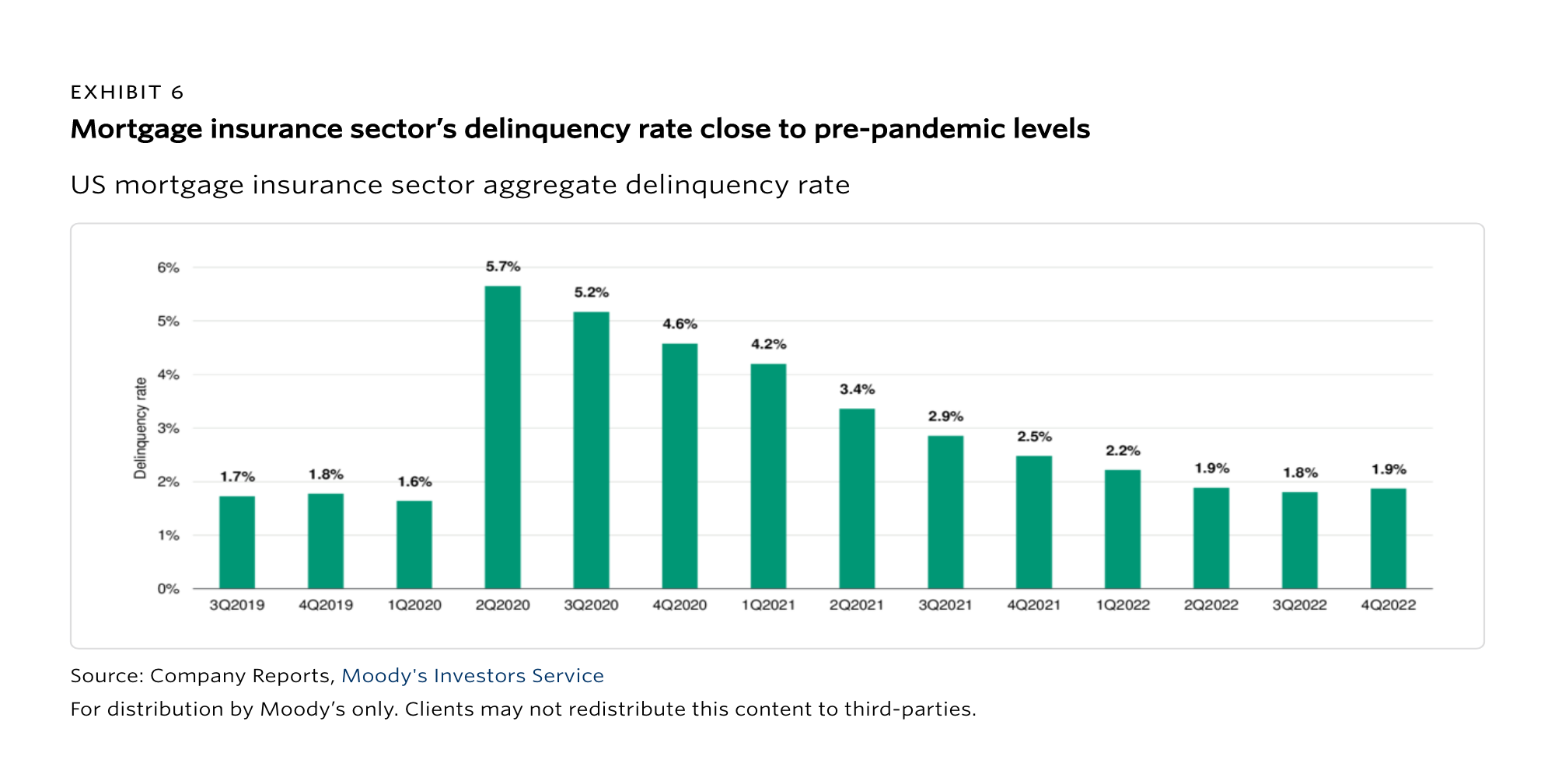

Delinquencies and Defaults

Finally, let’s look at delinquencies and defaults.

Mortgage delinquencies, while still very low by historical standards, are beginning to inch up. This is not surprising given that inflation still remains sticky, so the burden of mortgage payments are increasing.

We have further issues coming up that is likely to exacerbate this situation. The Emergency Measures during the pandemic are all going away. We’ve discussed changes to medical care and the SNAP benefits. Add to that now student loans will have start being repaid. All of this is sure to create further burden on the consumer who has a mortgage.

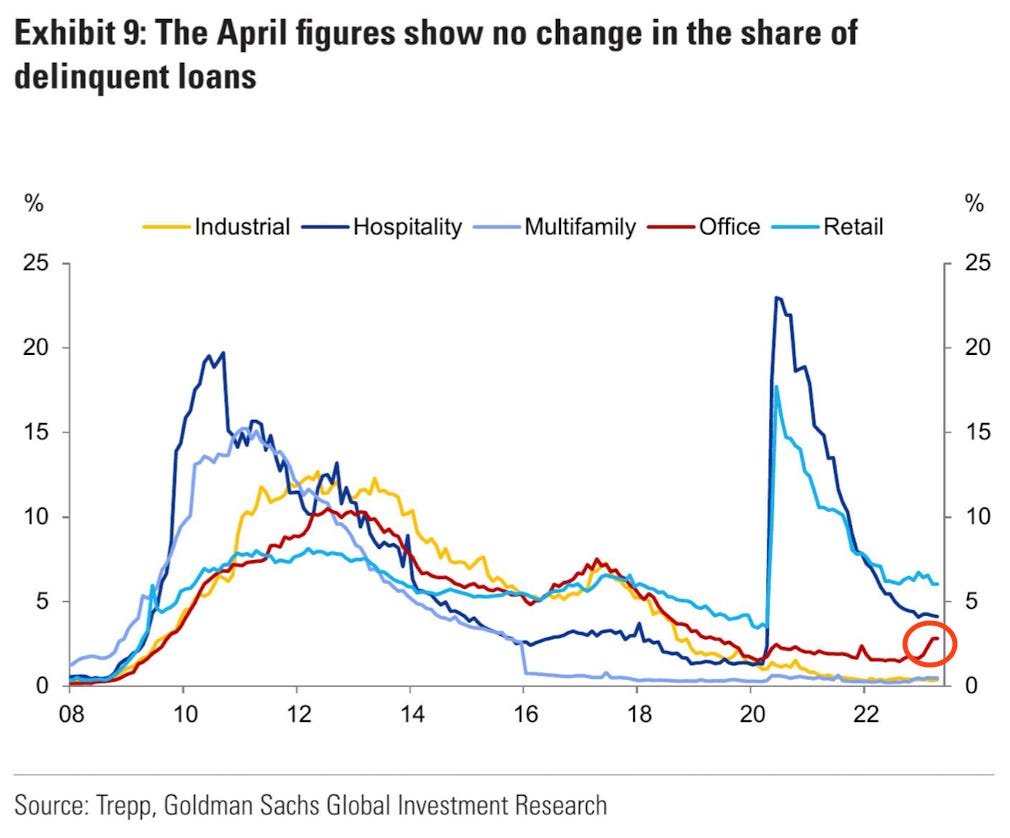

Finally, we have commercial property delinquencies. Most remain at historical lows, as you can see in the chart below. However, if you look closely, office properties are starting to show signs of trouble.

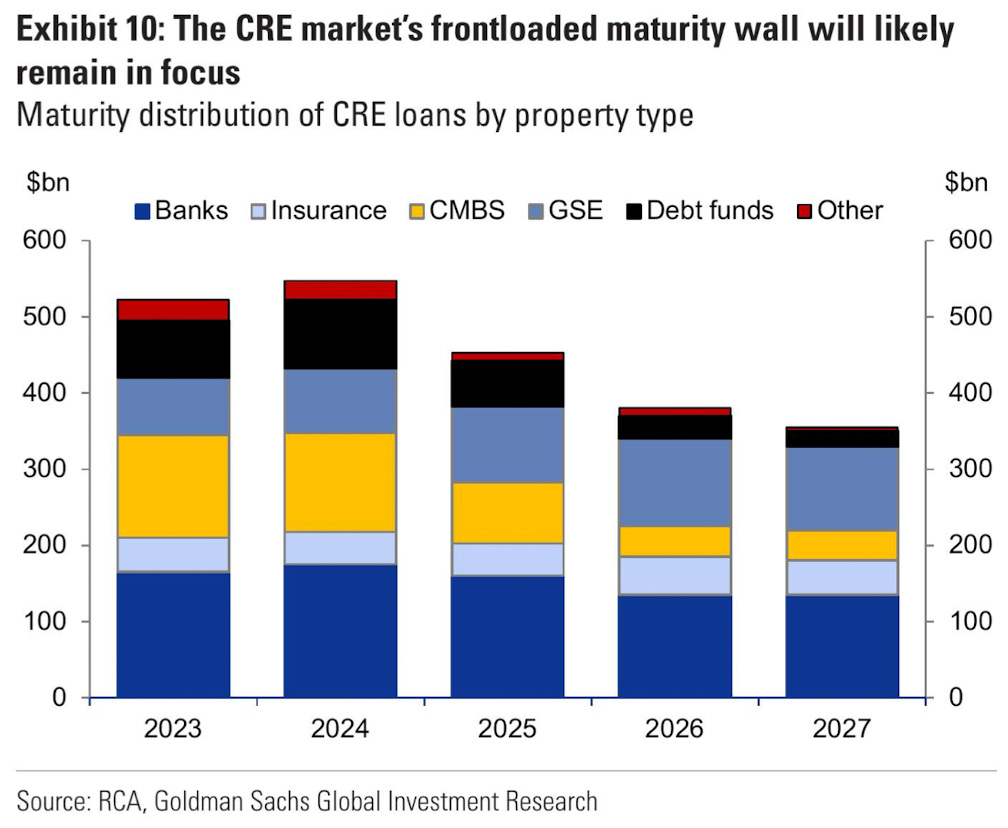

The biggest concern with these loans is that many of the these loans are now coming due.

After the 2008-2009 crisis, many of the CRE loans started to get refinanced between 2011 and 2013, most for 10 to 12 years. Many of these loans are now coming due and it remains to be seen what the banks will consider in terms of refinancing or restructuring.

As you can see, about $1.1 trillion (perhaps more by some estimates) is coming due between 2023 and 2024. What more is that 43% of these loans have floating rates of interest, according to an article from Bloomberg.

Closing Thoughts

We are likely to face a challenging situation in the commercial real estate market. With occupancy falling and rents declinings, I don’t see how these property owners can make their payments, let alone negotiate terms with their banks for refinancing or restructuring. Not to mention, asset values have been falling because rates have been rising so, collateral values are lower. The property owners will either need to top up their collateral with cash (which they likely don’t have) or add more property.

This is a market everyone has their eye on now, and so do we.