Breakfast Bites: Weak data lifts markets

PPI heats up while Retail Sales cool, setting up softer GDP read; UK’s Budget takes the spotlight; AI jitters grow as SoftBank slides & Nvidia pushes back on criticism; New addition to Watchlist

Rise and shine everyone

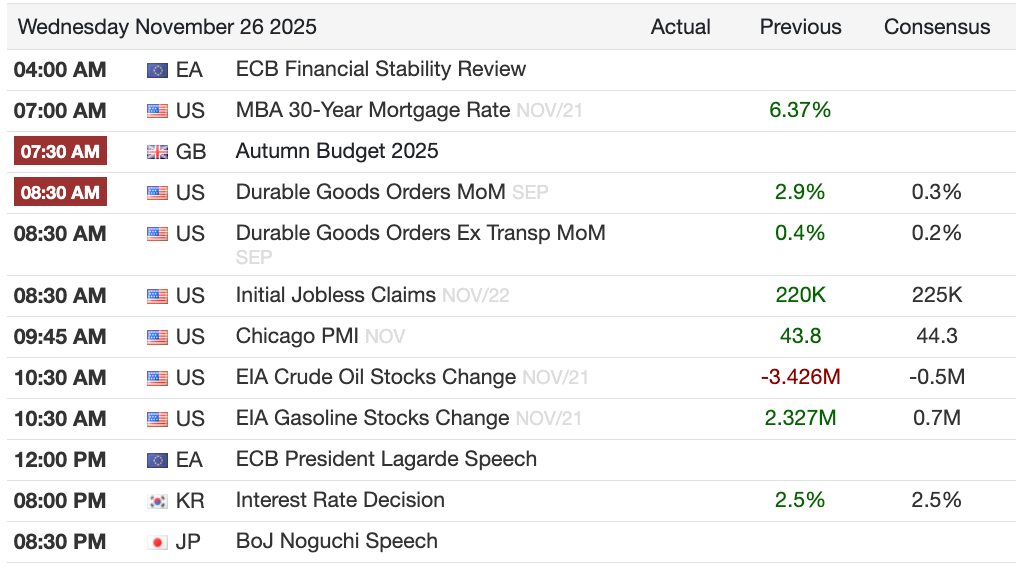

We had a lot of macro data yesterday that led to a positive close. We’re heading into a low liquidity day for the US ahead of the Thanksgiving holiday tomorrow, when US markets will be closed. All eyes are on the UK today, though, as Chancellor Reeves reveals the much awaited budget.

Morning Macro Briefing

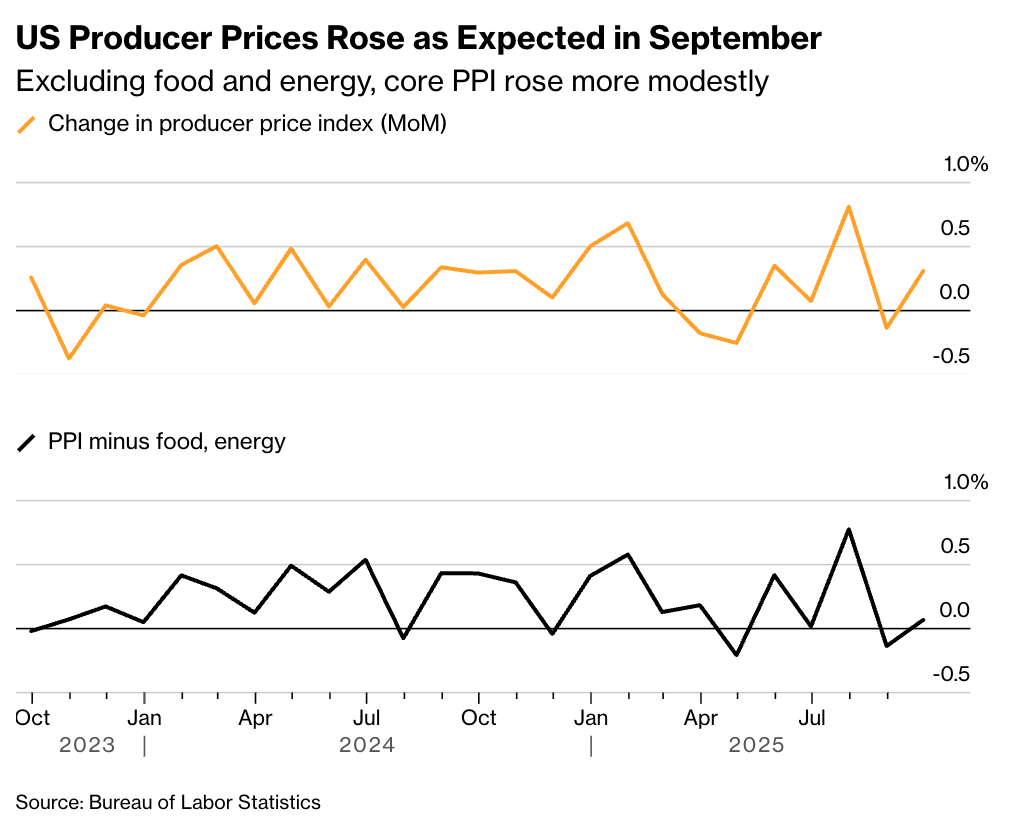

The Macro News was exactly the opposite of what we wanted to see. PPI went up, and Retail Sales went down. So prices are going up, and customers are not buying.

While the PPI reading came out in line with expectations at 0.3% MoM, core PPI cooled marginally, meaning that Food and Energy drove most of the increases. Now, since then energy prices should have reduced, and we know that President Trump rolled back some tariffs on food. So, it’s quite likely that the trend will moderate somewhat.

However, Retail Sales tells us that spending is slowing. The readout for Control Group Retail sales - the number that goes into the GDP - came in negative at -0.1% vs. the expected +0.3%. This means we could see a softer GDP growth number, and it aligns with what most retailers said during their earnings calls: the US consumer is seeing weakness, particularly among lower-income groups.

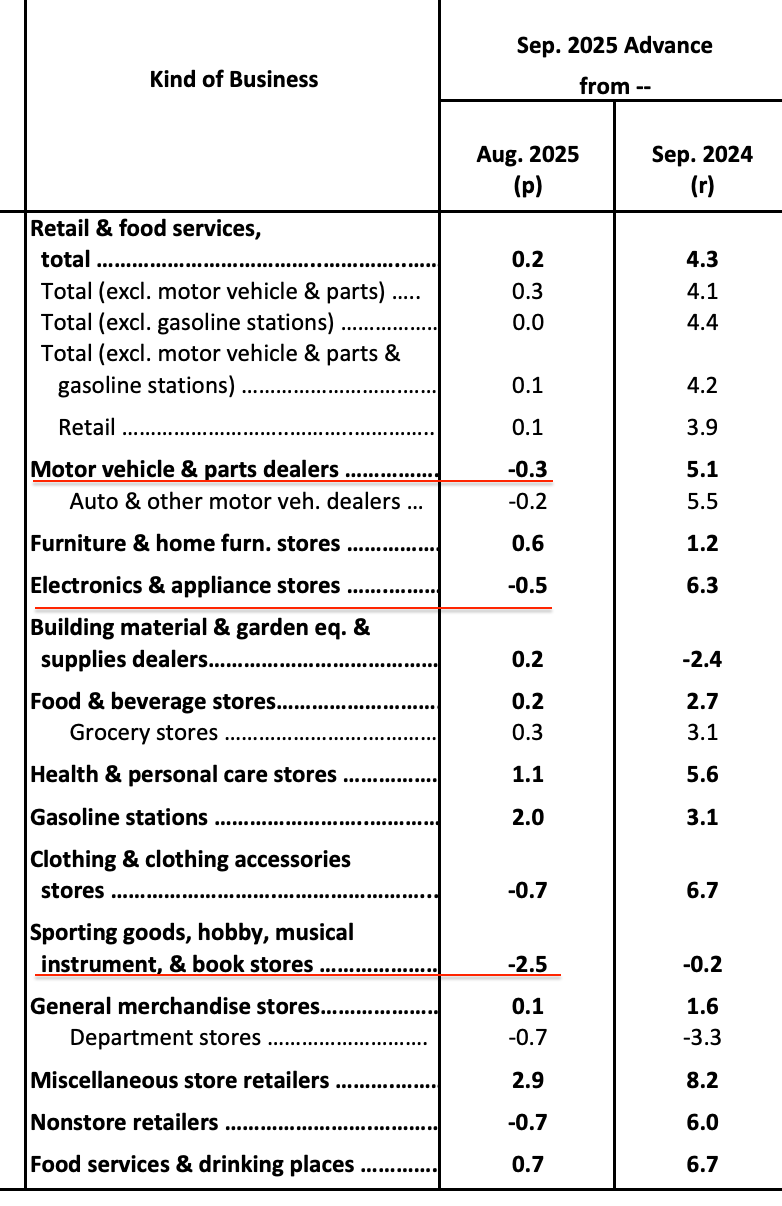

On a sequential basis, we’re seeing a pullback in the more discretionary parts of spending - Motor Vehicles, Apparel, and Sporting Goods, etc.

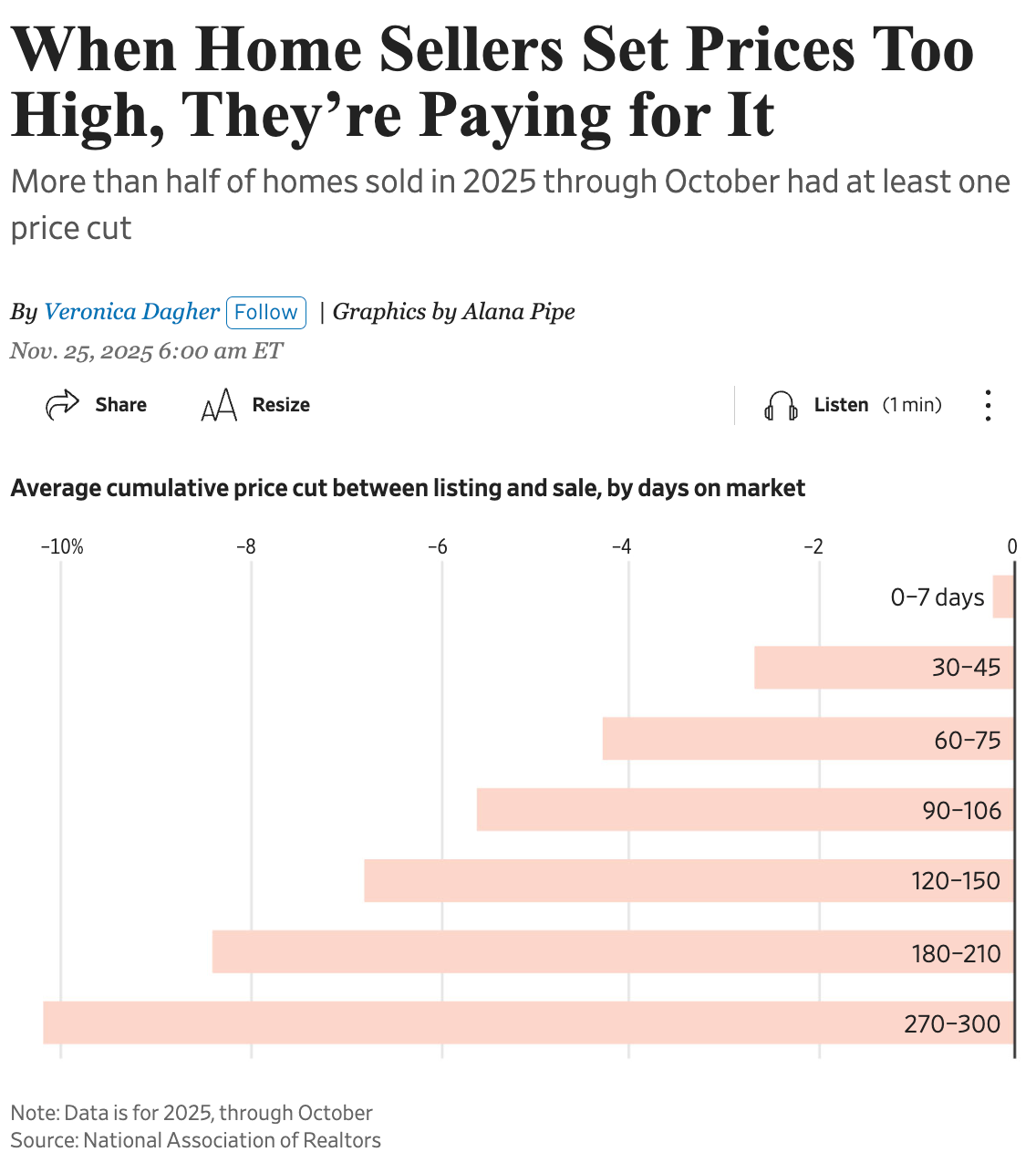

Home prices also continued to cool in Sep, rising 1.3% YoY vs. 1.4% in August, marking an eighth consecutive month of slowing as buyers gained leverage. Higher rates are certainly weighing on the homebuyers and home sellers (see Chart of the Day below). This, however, is relatively good news for the CPI because it means shelter prices may soon start to inch down, pulling the CPI reading down with it.

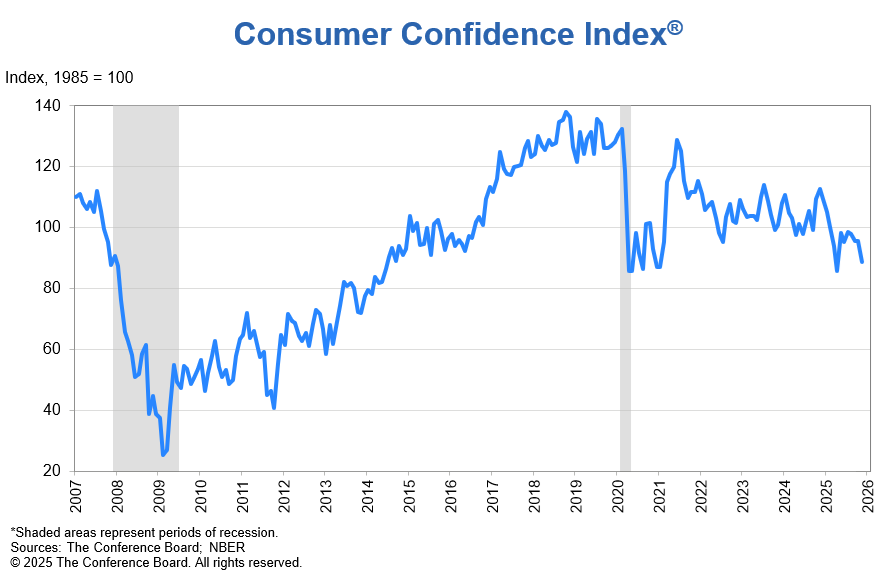

To top all of this off, we got the Conference Board Consumer Confidence Index® release - the headline fell 6.8 points to 88.7 from 95.5. Both the Present Situations Index and the Expectations Index weakened, with the latter staying below the recession-signalling threshold for the 10th straight month.

Markets also took note of fresh headlines around peace efforts in Ukraine, with some US officials sounding constructive even as the Kremlin remained non-committal.

All eyes are on Chancellor Reeves’ Autumn Budget. She is expected to raise close to £30B through a series of smaller peripheral tax adjustments, leaning heavily on fiscal drag rather than headline tax changes. Markets will be watching the OBR forecasts and the new gilt remit closely, especially with productivity expected to be revised down by 0.2 to 0.3 percentage points. The sequence kicks off with PMQs at 07:00 ET, the statement at 07:30 ET, and the OBR outlook and gilt remit at 08:30 ET, followed by the press conference at 09:30 ET.

The Yen continued to firm as reports suggested the BOJ is preparing for another rate hike to 0.75% as early as December, with OIS now pricing a little above 50% odds for that meeting and nearly 86% for January. Japan’s yield curve flattened, and the 40-year JGB rallied after a solid auction. Meanwhile, PM Takaichi doubled down on her growth agenda, committing ¥1T to SME wage support and urging firms to raise base pay above inflation.

The Kiwi dollar jumped 1.3% after the RBNZ cut by 25bps to 2.25% but signaled the easing cycle may be near an end. Risks are now viewed as balanced and forward indicators point to recovery, although the bank left room for one more cut in 2026.

Momentum continues to build around ending de minimis import tax exemptions globally, following the US move to eliminate its own $800 threshold. The UK, EU, Australia, New Zealand, Singapore and now Japan are all exploring similar action, raising questions about the next wave of tariff adjustments.

Chart of the Day

We saw the national index showing a cooling in home prices, and here’s some more nuanced data from the WSJ that shows that home prices see a cut, the longer they stay on the market. So basically, there is an affordability issue, and sellers are not getting their asking prices.

Calendars

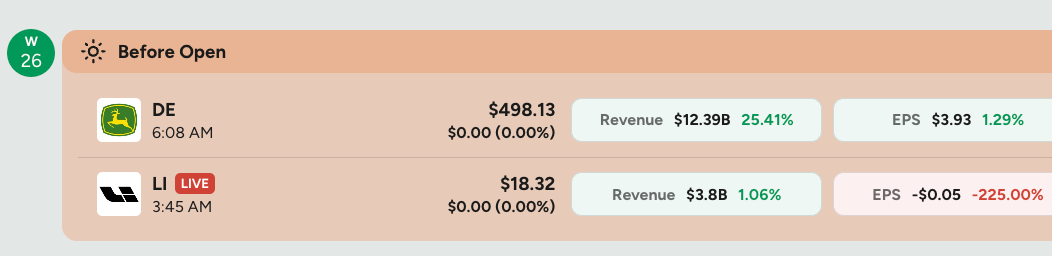

Market Prep

While the data releases in the US may have been stale, they led to the market pricing in a higher probability of a Fed cut because of a weaker consumer. The markets opened lower but quickly reversed course to rally higher.

Nvidia, however, saw some selling pressure. Michael Burry not only started his Substack but doubled down on his arguments against the company. In response, Nvidia released a memo to sell-side analysts to refute the claims. This kind of had the opposite effect of what you want to see. By addressing the concerns, Nvidia may have signaled that there is something to refute. Market sentiment can often be quite odd.

The price did recover by the end of the day, but look at this monthly chart below. It looks quite ugly. We’ll need to see how this plays out, but for now, there seems to be some actual selling pressure.

AI concerns linger

SoftBank’s roughly 10% drop, after falling as much as 11% intraday and down an estimated 44% since late October, is turning into a broader signal that Japan may again be leading a reset in global tech expectations. The move reflects growing concern around model competition and the heavy, circular financing behind AI data centers, raising fresh questions about whether the 2025 AI infrastructure cycle still has momentum or is starting to look late stage.

Meta’s plan to spend billions on Google’s TPUs suggests a shift in loyalties and reinforces Alphabet’s push toward a more integrated Gemini 3 stack. But Alphabet still depends on Nvidia, whose GPUs remain the dominant and known supply base for both training and customer workloads, which means TPUs and GPUs stay linked rather than competing head-to-head.

Continue reading for my take and the updates to our daily tactical watchlist. We’re adding another new name today.