Breakfast Bites: Warsh's Sintra Debut

Momentum cools into a quieter open, Fed Chair Warsh steps onto the Sintra stage for the first time, and two desks read the Iran talks in opposite directions, all before payrolls come a day early.

Rise and shine everyone

Yesterday’s rally was real, with the S&P on track for its best quarter since Q2 2020 as stretched mega caps, Google, Amazon, Microsoft, bounced hard off key technical support. But that was a systematic squeeze working through positioning, not a fundamental verdict on anything. Futures are giving a little of it back this morning, and that is momentum unwinding, not a change of heart.

The bigger event today is Fed Chair Warsh stepping onto the policymaker panel in Sintra this morning alongside Lagarde, Bailey and Macklem, his first international appearance since chairing his first FOMC in June. His style is famously light on forward guidance, and that is exactly the problem for a market pricing only a 35% chance of a July hike and 65% by September.

Say one hawkish word about price stability against a backdrop of 3.4% core PCE, and the dollar has real room to run. Sitting behind Warsh is an Iran picture that depends entirely on who you are reading. The WSJ and Goldman call the Doha talks constructive, while JPMorgan’s own says Iran has ruled out the Qatar meeting altogether.

That gap alone tells you the crude and dollar trade is more fragile than yesterday’s tape suggested.

Here is what we are watching today:

Fed Chair Warsh’s Sintra debut, his low-guidance style, and what it does to July and September hike pricing

The split read on US Iran talks and what it means for crude and the Strait of Hormuz risk premium

Positioning into Thursday’s payrolls, pulled forward a day for the July 4 holiday, and a holiday-shortened week that closes Friday

In the Macro Briefing, I walk through JPMorgan’s own scenario grid for Thursday’s jobs report, a 40% base case for a 100k to 130k print and exactly what that does to the S&P. In Market Prep, I lay out the level Morgan Stanley now has on the index for its base case, 8,300, and why the broadening trade away from crowded Semis and hyperscalers is the more interesting story than another AI headline. Full breakdown, levels, and what we are trading below.

Morning Macro Briefing

The tone on US-Iran talks is cautiously constructive but genuinely unresolved. The WSJ and Goldman call today’s Doha talks constructive, with shipping through the Strait of Hormuz picking up, while JPMorgan says Iran has ruled out that Qatar meeting entirely. When two well-sourced desks disagree on whether a meeting is even happening, this is not the moment to chase the peace-deal narrative in crude, and a small hedge stays warranted until Doha produces something concrete. Oil seems to agree with the former, as we see further pullback in prices, closing in on pre-war levels.

Fed Chair Warsh’s Sintra appearance is his first international one since chairing his first FOMC in June, where rates held at 3.50 to 3.75%. His reputation is for low-information, reduced forward guidance, so the market treats July as strategy-dependent rather than data-dependent, with futures pricing a 35% chance of a hike this month and 65% by September. With core PCE at 3.4% and Thursday’s jobs report still to come, any pushback against hike pricing would be a genuine surprise and skews dollar risk higher, so watch DXY off his remarks.

Morgan Stanley separately expects both headline and core PCE to decelerate from here as tariff pass-through fades and oil’s retreat feeds through to core goods. Its own late-June consumer survey found 67% of respondents cite grocery prices as a strain, though 22% said their ability to cover monthly expenses has actually improved from a year ago, an underappreciated crack in the consumer-is-cracking narrative.

The ECB chorus around Warsh was uniformly dovish, with Wunsch, Kazaks and Demarco all downplaying the case for further hikes while Nagel struck a more balanced tone. None of it moves the euro much on its own, and Warsh matters more for EUR/USD this week than anything coming out of Frankfurt.

The JPY sits at its weakest level in more than 40 years, with USD/JPY around 162.7 and grinding toward 162.40 per Goldman. Japan’s top currency official, Mimura, has stayed quiet, though he noted the US has raised no objection to intervention, which reads as tolerance of the weak yen for now rather than active resistance. The real intervention risk is backloaded to after Thursday’s payrolls and Friday’s holiday, once liquidity improves enough for any action to actually work.

Mexico wants a 16-year extension to USMCA, and the required six-year formal review of the agreement begins today. Given this uncertainty, we’d avoid exposure to autos, and stay neutral Mexico.

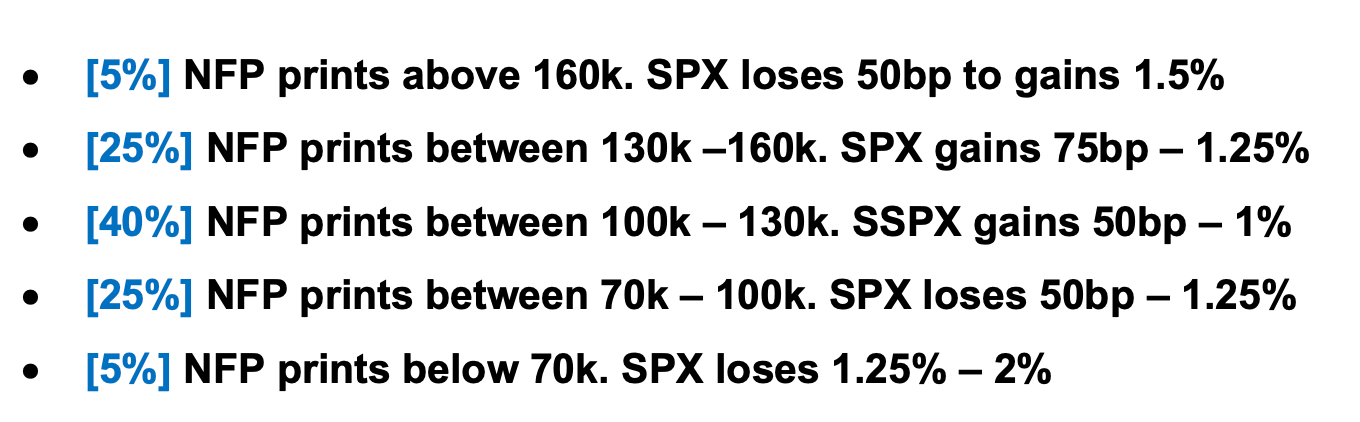

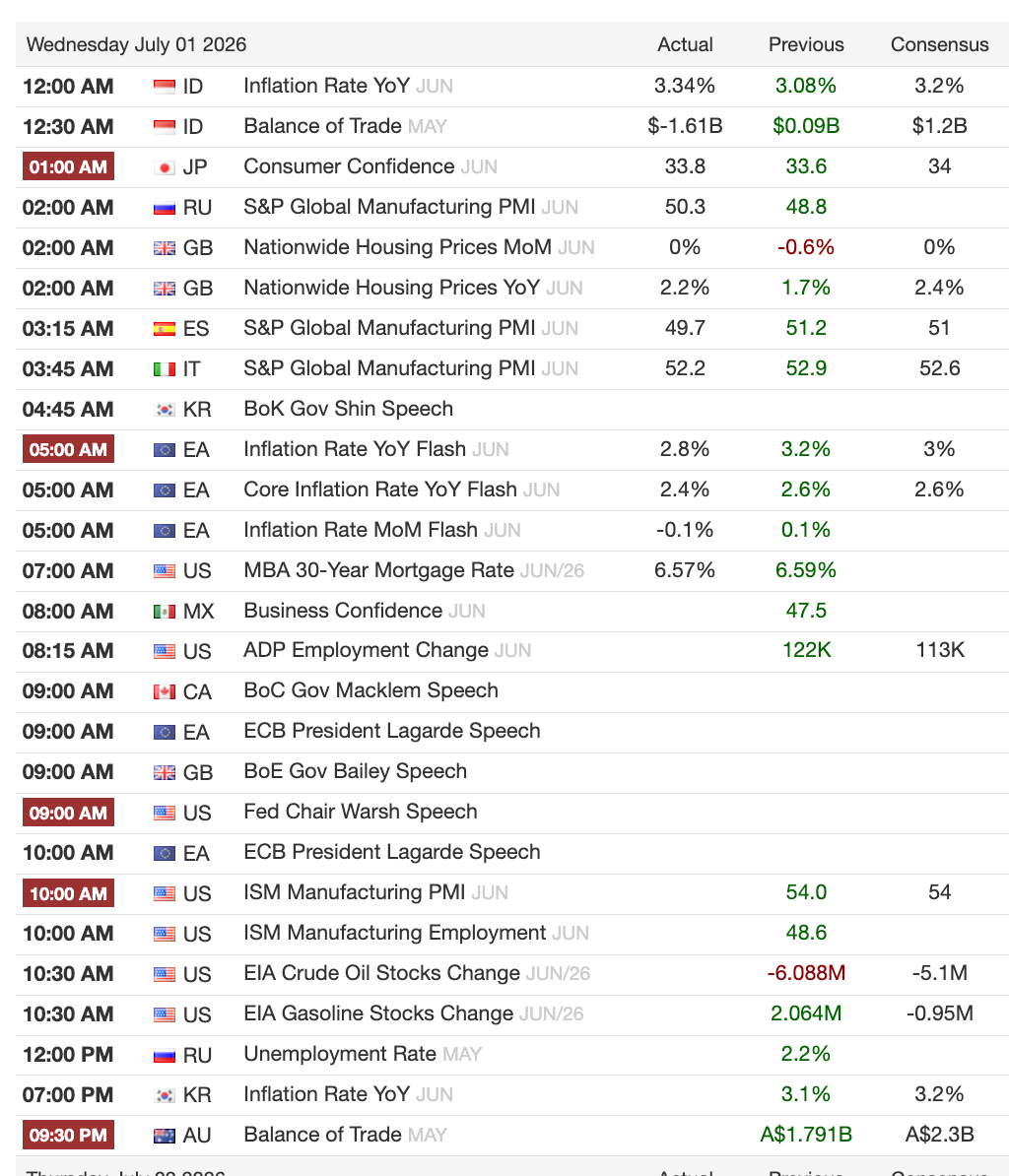

Yesterday’s JOLTS report beat expectations, with job openings at 7,594k versus 7,296k consensus, meaning firms are looking to hire. A stable quits rate suggests workers are not rushing to leave jobs for better ones, and stable layoffs mean firms are not aggressively cutting headcount, though consumer confidence came in softer at 91.2 and the labor differential fell to its lowest level since 2021. Today brings ADP, ISM manufacturing and Challenger job cuts, all previews for Thursday’s main event, where JPM sees 125k jobs added against a 110k street estimate and 172k prior.

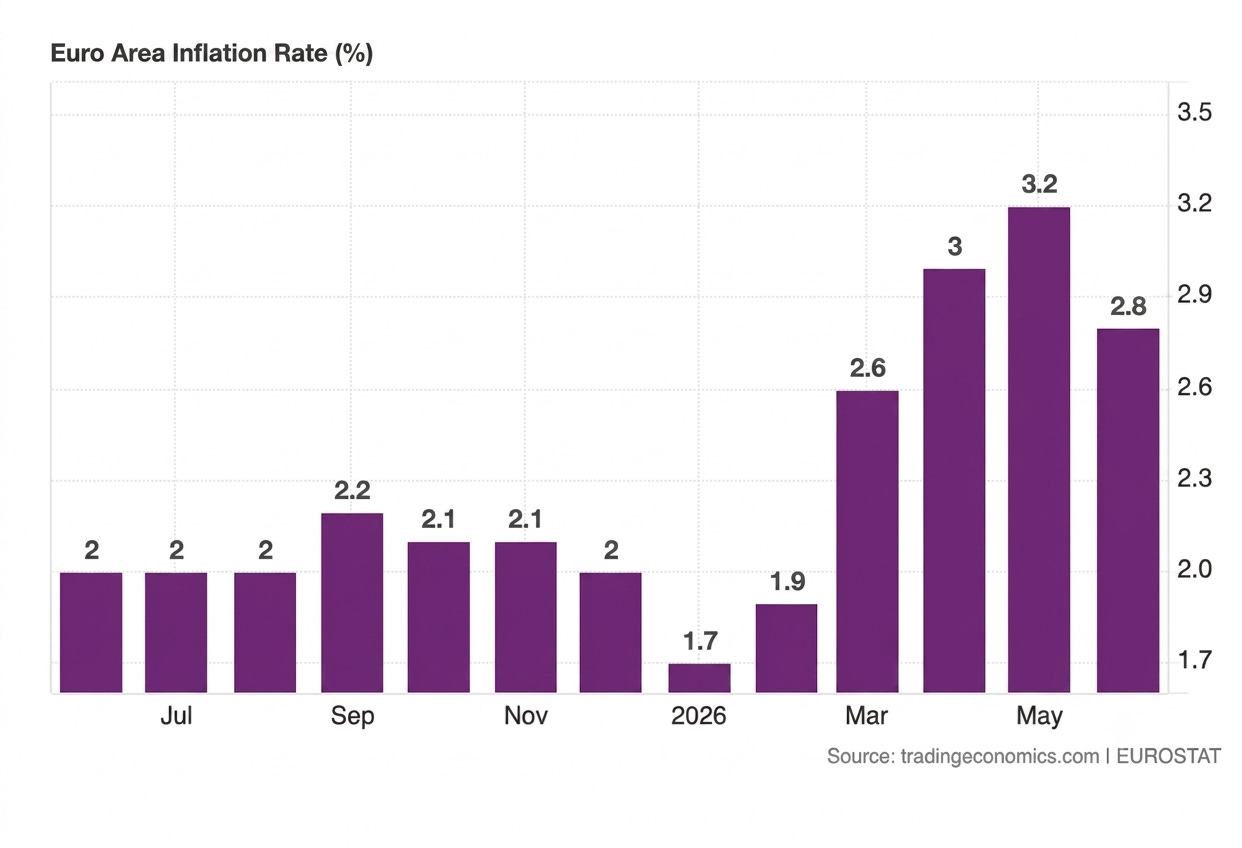

Asian PMIs disappointed broadly, though Korea’s chip exports accelerated and Japan’s Tankan beat estimates, with markets still pricing only a marginal chance of a late-July BOJ hike (we don’t expect a hike so soon). European manufacturing firmed at the core, with Germany and France both back in growth, while the periphery diverged as Spain and Poland stayed in contraction. EA inflation also moderated as oil prices started to decline last month. This gives us a positive outlook on European equities.

Chart of the Day

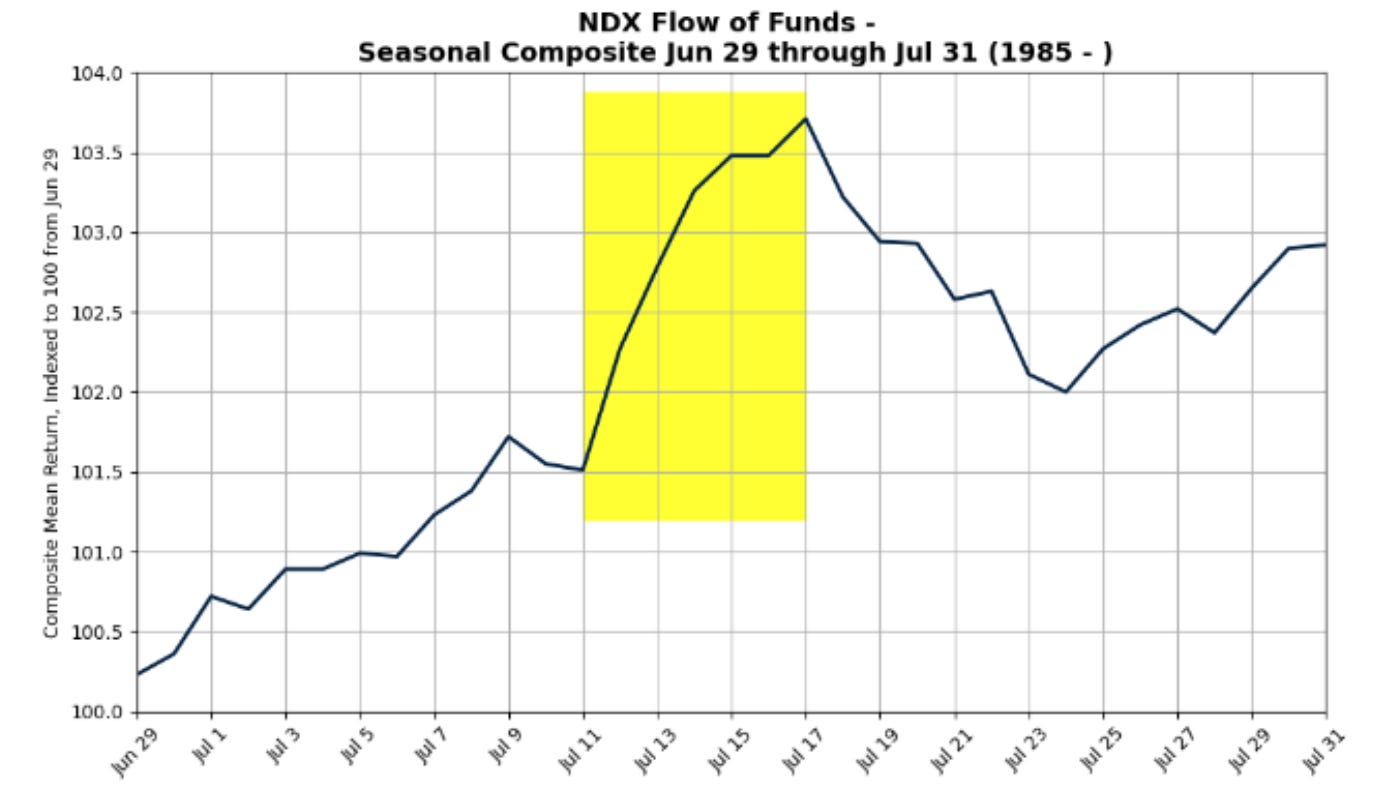

Goldman’s desk flagged this one, and it is worth carrying into the holiday week. While the S&P has historically ramped in early July, the Nasdaq 100 has tended to trade sideways to moderately higher to start the month, only really picking up steam mid-month and peaking around the 17th, with July 3rd itself historically the second-best seasonal day of the year for the S&P.

With volumes already 20% below the 20-day average into the holiday, thin liquidity means whatever move shows up this week will likely be larger than the news justifies.

Calendars

Today is the real event day of a short week, with Fed Chair Warsh’s Sintra remarks, ADP employment, ISM manufacturing and the start of the formal USMCA review all landing before Thursday’s payrolls arrive early for the July 4 holiday. Friday is a US market holiday, so positioning has to be squared away by Thursday’s close.

Market Prep

Yesterday’s session was a mega-cap mean-reversion trade dressed up as a broad rally. The S&P is tracking its best quarter since Q2 2020, but breadth was poor, with roughly 300 S&P names down on the day even as the index gained 75bp and the Nasdaq 100 led at plus 165bp. Goldman’s high-beta momentum basket rallied 310bp on the day and 7.7% over two sessions, fully reversing Friday’s worst single-day momentum drawdown, while its hyperscaler basket underperformed even as the broader AI trade ripped, a divergence that lines up with Morgan Stanley’s thesis that Semis and hyperscaler crowding is due to fade.

Futures sit a touch above unchanged this morning, with the S&P, Nasdaq and Russell all around plus 0.1%, the 10-year at 4.365%, WTI at $70.85, gold at $4,020 and the VIX at 17.59. Credit spreads have widened for five straight weeks, the longest streak since 2022, though that is issuance-driven rather than genuine stress.

Positioning data from last week shows a genuinely risk-on tilt, with equity ETFs taking in $33.9bn of inflows even as broad AI-themed ETFs saw outflows, another sign capital is rotating within the AI trade rather than piling into it. CTAs trimmed S&P and Nasdaq longs after a momentum signal breach but remain significantly long equities overall, while leveraged funds cut S&P and Russell shorts even as they added to Nasdaq shorts, a real divergence in how fast money is expressing the broadening debate.

Nike and Constellation Brands reported yesterday, with Nike’s China struggles a recurring theme, while FactSet and General Mills report today ahead of the July 14 unofficial earnings kickoff.

JPMorgan maintains its Tactical Bullish call into earnings season, keeping a Tech and Cyclicals barbell with Healthcare added as a low-correlated long, favoring Airlines, Banks, Homebuilders, Retailers and Transports while avoiding Autos on USMCA risk, and suggests July-expiry S&P puts as a book hedge.

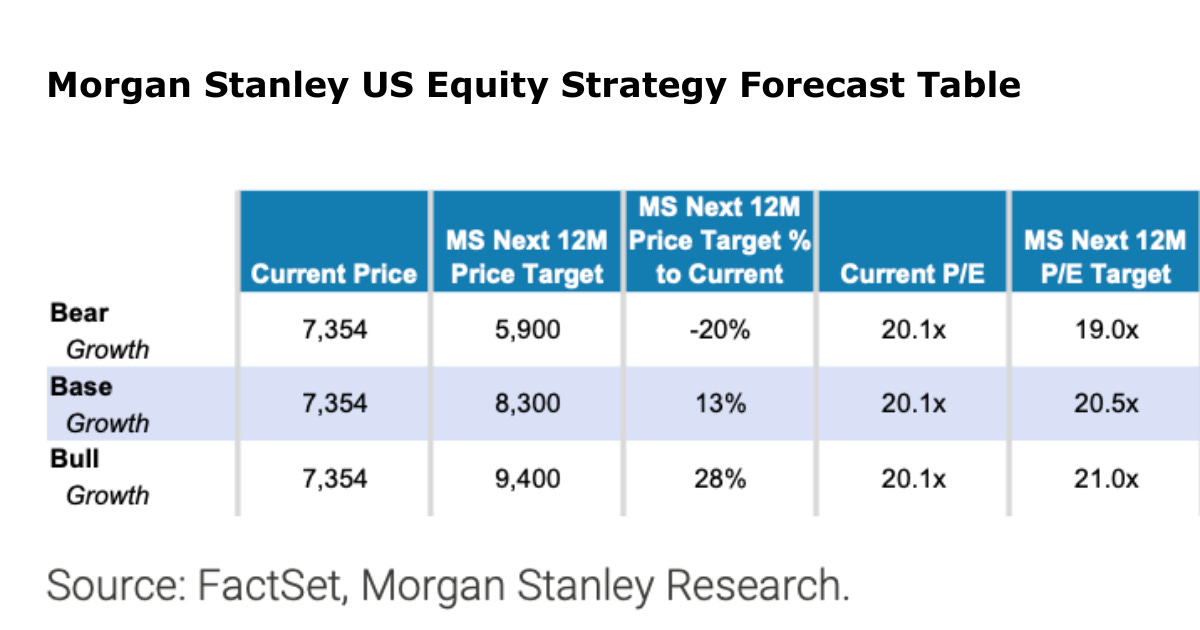

Morgan Stanley’s base case now puts the S&P 500 at 8,300 over the next twelve months, a 13% move from Tuesday’s close, built on the median stock posting its fastest earnings growth since 2021, with Consumer Discretionary Goods, Transports and Regional Banks its preferred way to play that broadening over crowded Semis and hyperscalers. The one risk it flags is liquidity, since a shrinking reverse repo facility and slowing Treasury buybacks are tightening conditions just as the market needs more of it.

That liquidity risk already has a number attached. MS’s own funding-cost gauge, AXW futures, sits more than two standard deviations above its trailing 12-month range, a stretch that has historically preceded mean reversion in the S&P, and the firm sees upside capped until the Fed or Treasury eases the squeeze.

Three things to watch into the close. Fed Chair Warsh’s actual words in Sintra and how DXY reacts matter most, since a hawkish lean against 3.4% core PCE has real room to run. Whether the Doha Iran meeting happens at all today is the second, given JPMorgan and Goldman are reading the same situation in opposite directions, and Thursday’s payrolls print against JPMorgan’s own 125k call is the third, arriving a day early to close out a week that has already asked the market to digest more than usual before the holiday.