Breakfast Bites: Warsh Day

Kevin Warsh is sworn in at the White House this morning, Turkey burns through $10 billion in thirty minutes, and Japan rips into a long US holiday weekend.

Rise and shine everyone

US Markets are looking to stage a comeback going into a long weekend. Monday is closed for memorial.

Markets are seeing some relief, as negotiations on the Middle East front have seemingly progressed. However, Iran is adamant on a toll, and have been in negotiations with Oman on this. President Trump is not open to the idea. Crude is moving higher on this.

Turkey burned through $10 billion in reserves in roughly thirty minutes, and that pace of intervention is not one a central bank can sustain for long. The political backdrop has deteriorated sharply, and the emergency policymaker meeting today will need to do real work to stabilise confidence. TRY and Turkish CDS are the variables to watch for any spillover into broader EM.

Three things we’re watching today:

Breakdown in Middle East negotiations if the toll issue is not resolved

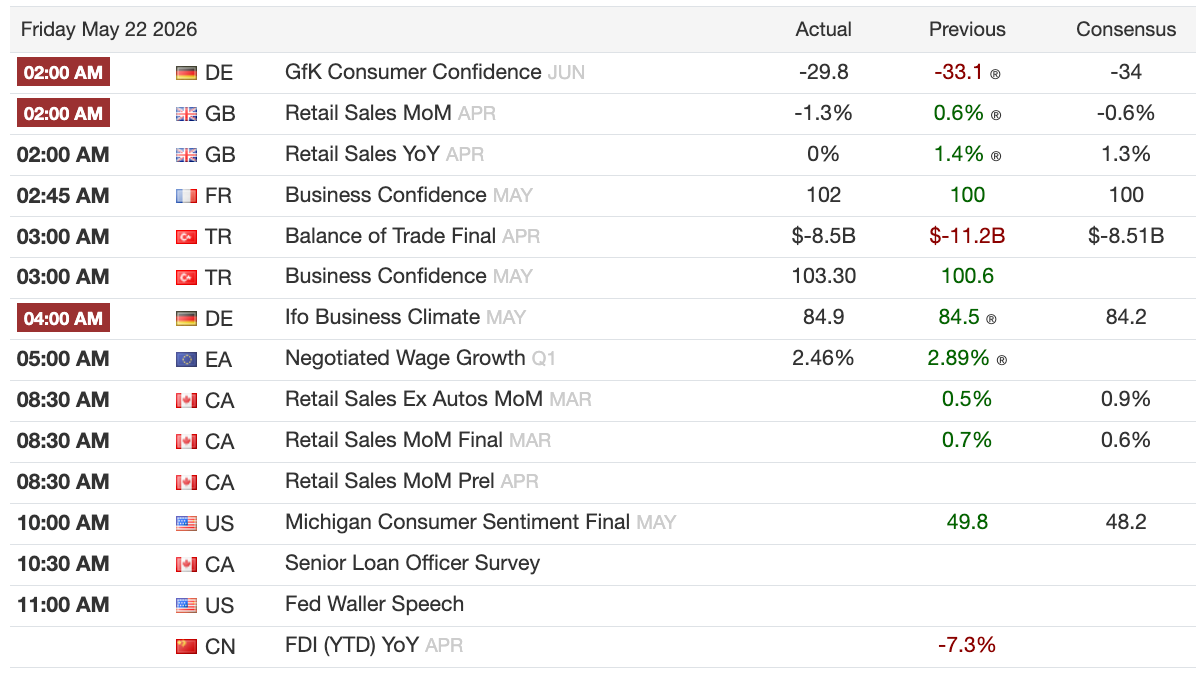

Final University of Michigan Sentiment reading at 10 am ET - Walmart’s earnings showed us poor retail sentiment

Kevin Warsh is being sworn in as Fed Chair at the White House at 11 am ET today, with President Trump hosting the ceremony. I

Morning Macro Briefing

Yesterday, we saw some relief as President Trump suggested that they were closer to a deal on Iran. There is, however, the issue of the Strait Toll. There was news that Iran and Oman have been negotiating a tolling mechanism for the Strait. President Trump obviously didn’t like this, since no one should have control over these waterways.

We’ve discussed this before… there will be many countries that don’t like this because it sets a dangerous precedent for other similar waterways, such as the Strait of Malacca. This maritime chokepoint between the Indian and Pacific Oceans carries about 25% of globally traded goods and nearly 80% of China’s imported oil.

Turkey is the shock of the morning. A court ruling removed the leadership of the Republican People’s Party, the main opposition to Erdogan, prompting CHP head Özgür Özel to call it a coup and triggering immediate market panic. Turkey’s central bank burned through approximately $10 billion in reserves in thirty minutes, and an emergency meeting of senior economic policymakers has been convened to stabilise markets. The opposition is appealing to the Supreme Court. Turkey has been threading a narrow path on market confidence, and this is precisely the kind of political rupture that tests whether that confidence is structural or conditional. I doubt this resolves cleanly over a long weekend.

The Warsh Question

Warsh arrives at the Fed at a genuinely uncertain moment in the policy cycle. Labour market resilience is fraying at the edges. Inflation has made progress without fully clearing. And the new Chair comes in under close political scrutiny, having made hawkish noises in the past while also carrying a history of cooperation with Treasury.

The question markets will spend the coming weeks trying to answer is whether Warsh is hawkish on inflation or hawkish on Fed independence. Those are different things with different policy implications. Hawkish on inflation means the front end faces continued upside rate pressure even if growth softens. Hawkish on independence means Warsh may be more willing than the initial read suggests to cut once conditions warrant, as long as he controls the narrative around why.

Today’s ceremony tells us almost nothing. His first FOMC meeting is where the signal will be clearest. Until then, watch his language on labour market conditions and watch whether he frames the PCE path as a ceiling or a floor.

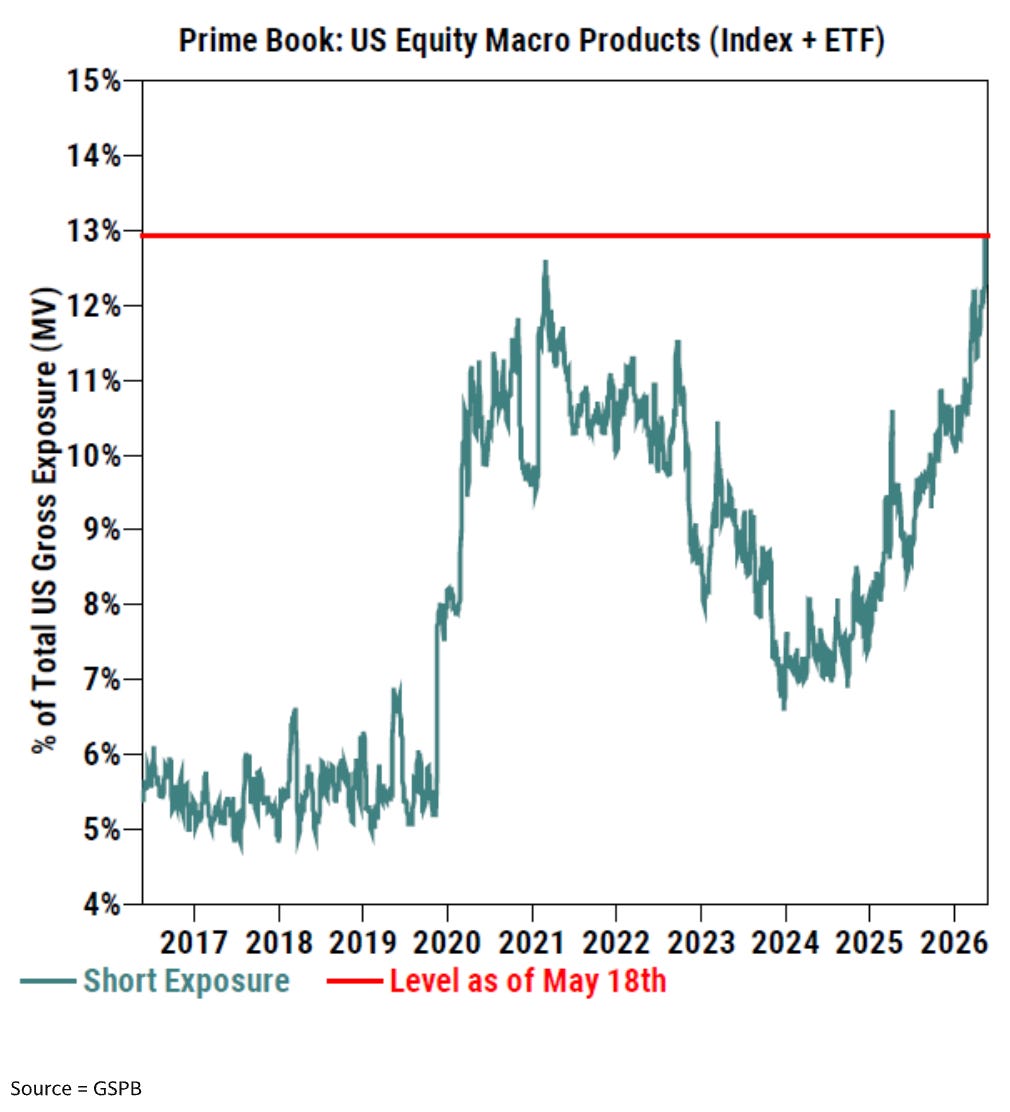

Chart of the Day

Hedge funds have pushed US index and ETF short positions to a 10-year high because they are anxious about geopolitical friction, interest rates, and oil. Rather than risking losses on individual stocks, these institutional investors are using broad market products to hedge their portfolios against macroeconomic shocks. This crowded positioning has created a coiled spring effect, meaning any positive news could trigger a violent short squeeze and send the major indices ripping upward.

Calendars

Market Prep

Asia trade was quieter today than yesterday but broadly positive, with Hong Kong up 1.2% and the Nikkei extending its run with a further 2.7% gain after Thursday’s 3.5% surge. The Japan story is increasingly about SoftBank, which added another 12% today on top of yesterday’s 20% rally, with ARM up 16% in tandem.

Lenovo put up 15% after FY26 earnings beat on every metric, with AI-related revenue continuing to accelerate. AMD’s CEO Lisa Su, speaking from Taiwan, told partners to ramp faster and said she expects the overall CPU market to grow more than 35% annually for the next five years. That is a structurally bullish signal across the entire semiconductor supply chain.

US equity futures are modestly positive heading into the open, carrying Asian momentum while wrestling with a roster of live variables: the Warsh ceremony at 11 am ET, the Turkey situation, no Iran resolution, and the long weekend ahead. The path of least resistance into the close is cautious position management rather than new risk accumulation.

Seeing new tactical short positions on the US dollar against the Japanese yen at a spot rate of 159.10 with a downside target of 156. The currency pair has once again reached critical intervention territory near the 160 threshold, where the Ministry of Finance has historically acted to cap yen depreciation. Analysts anticipate that potential state intervention, combined with a forecasted interest rate hike at the upcoming June Bank of Japan meeting, will provide marginal support for the yen.

While broader macroeconomic fundamentals remain challenging for the Japanese currency, the current risk-to-reward profile highly favors positioning for a near-term downside reversal. The primary risk to this trade is that the global markets may continue to drive inflation concerns based on elevated oil prices.

Retail sentiment faced pressure after Walmart fell 7% on commentary regarding strained consumer budgets. However, the broader retail sector proved resilient as solid earnings reports allowed other names to squeeze shorts significantly. This price action contributed to a highly charged atmosphere where prominent rolling tech short baskets jumped as much as 6% during the day.

I wouldn’t mind taking a position in Walmart here, even though we may have to wait for a recovery.