Rise and shine everyone.

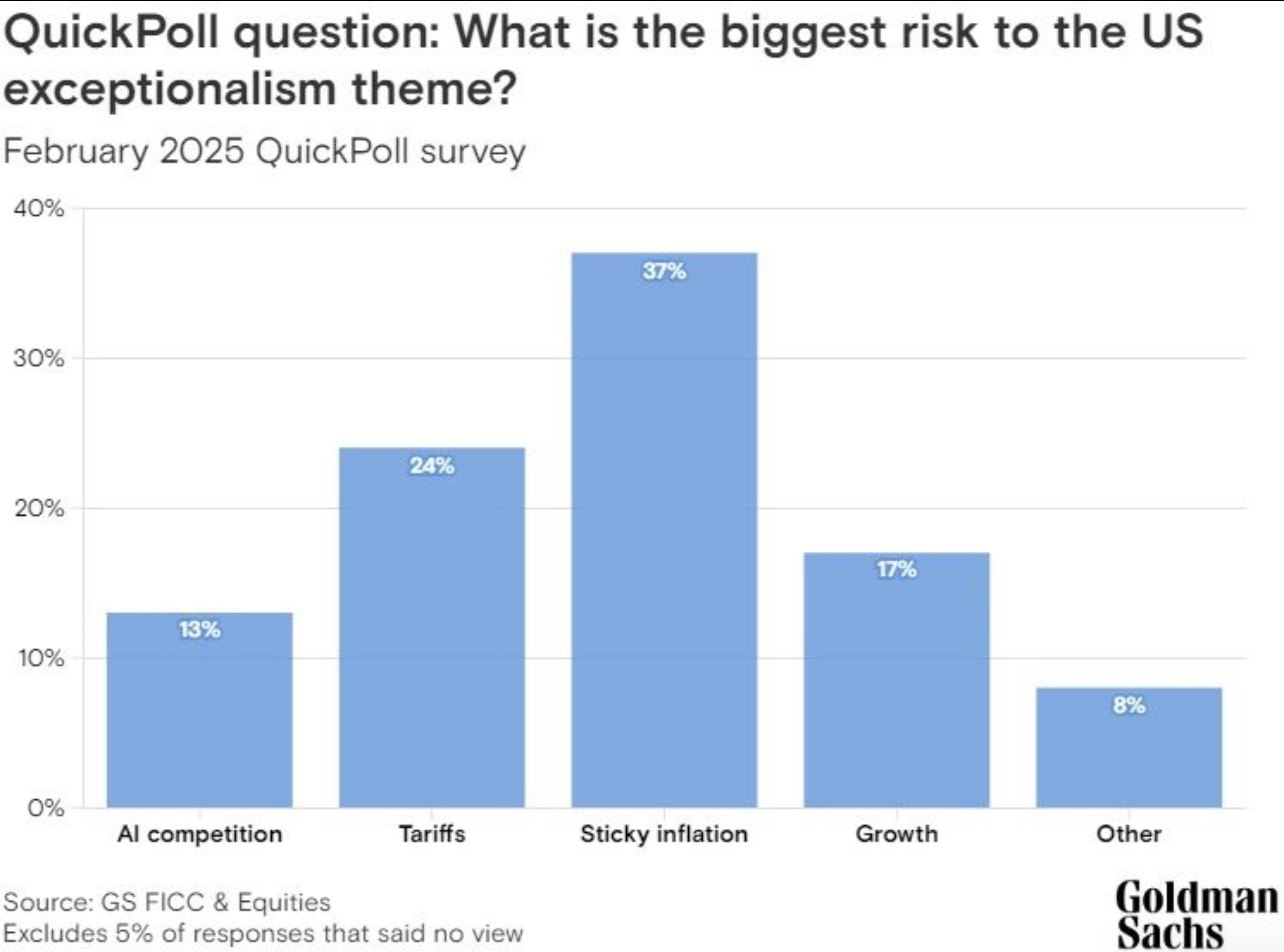

The big news in focus today will be US CPI numbers. A recent poll by Goldman Sachs shows that Inflation remaining sticky is still the number one concern among investors.

In fact, the last Fed statement and yesterday’s testimony from Fed Chair Powell gave us confirmation that inflation continue to remain front and center on the agenda. (CPI preview below)

Fed Chair Powell reinforced a patient stance during Senate testimony, emphasizing “no rush” to cut rates amid resilient growth. He acknowledged that the neutral rate may have risen meaningfully. US futures remain flat, while Treasury yields hold near 4.55% as Powell prepares for a second day of testimony.

The Yen weakened against the USD. Japan’s 5-year yields neared 1% for the first time since October 2008, while 10-year JGB yields climbed to 1.34%, the highest since February 2011. BOJ Governor Ueda spoke about the “pace” of rate hikes but did not reiterate prior forward guidance on potential increases.

Hang Seng outperformed with a 1.4% gain, leading mixed Asian markets, while EU and US futures remained flat. Australia’s PM Albanese sought a tariff exemption for steel and aluminum after a call with President Trump, but Trump’s trade adviser Peter Navarro criticized Australia’s impact on the US aluminum market. Australia’s Treasurer Chalmers stated that the country would not retaliate if subjected to tariffs, while Japan also formally requested an exemption.

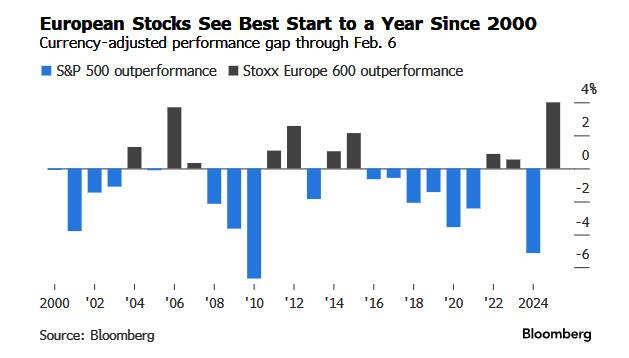

European markets edged higher, with the STOXX 50 reaching its highest level since 2000 and the STOXX 600 hitting a new all-time high. Food & Beverage stocks led the gains, while Oil & Gas lagged. Europe has had the best start to the year in almost 25 years.

US Equity Futures remain muted this morning ahead of the inflation report. Commodities are also seeing a pullback. Oil prices have dipped, partly a reflection of easing Middle East tensions. President Trump had a fruitful discussion with King Abdullah of Jordan, who agreed to take in 2000 Palestinians and aid in talks with other Middle Eastern countries.

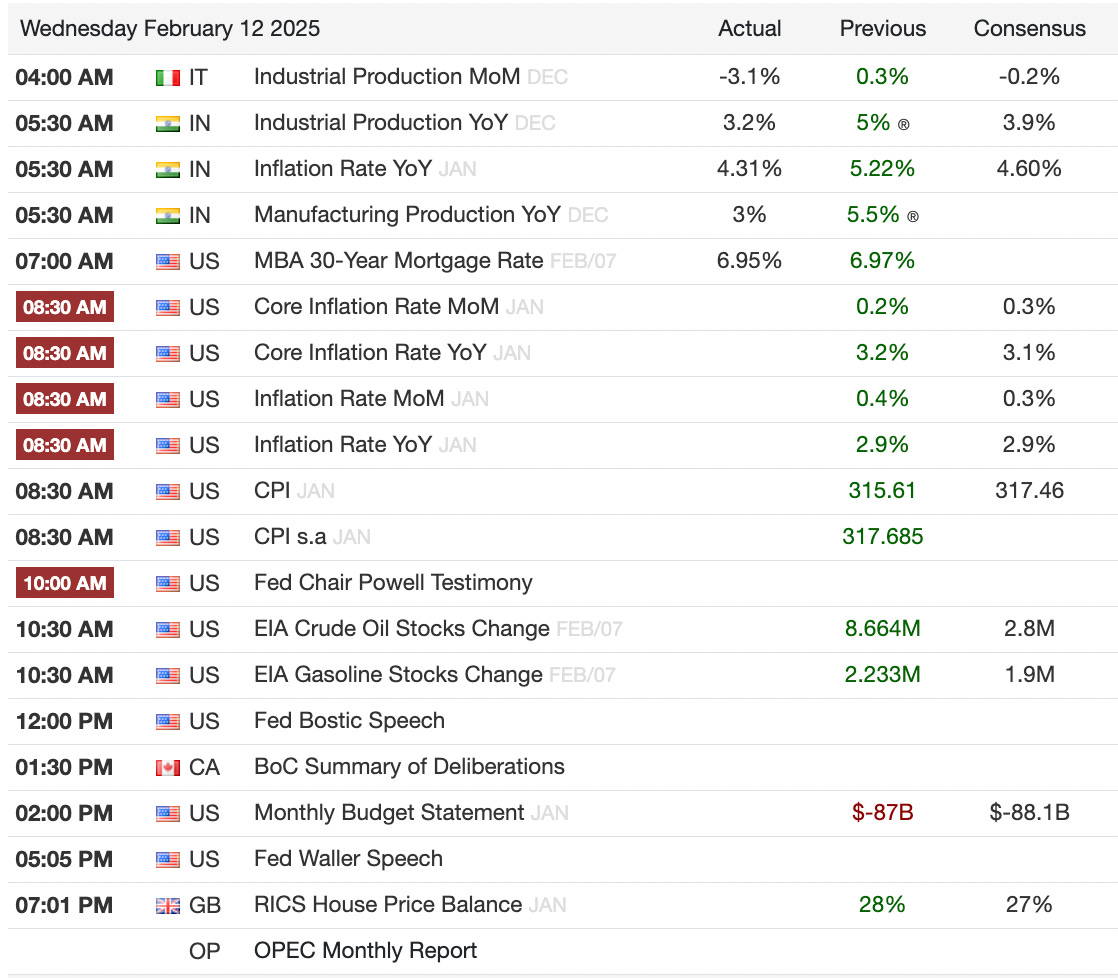

US CPI Brief Preview

The Estimates:

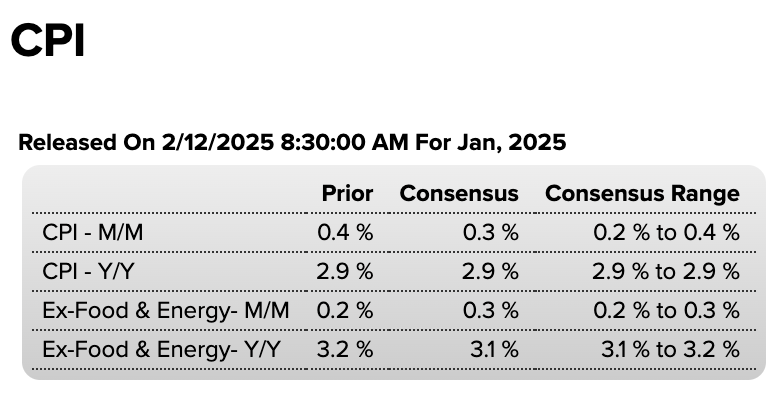

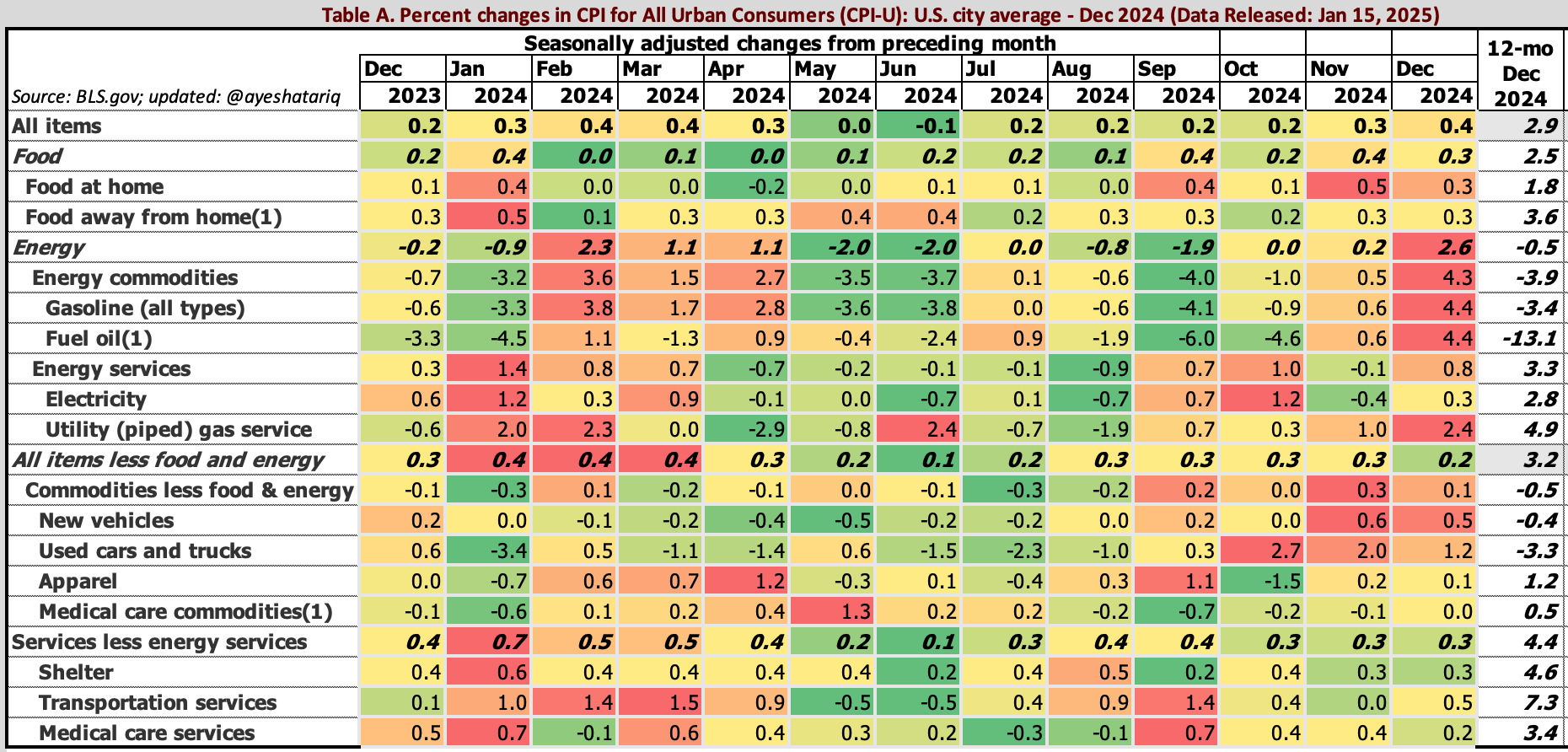

January’s CPI should show a slight decrease in the headline number because of favorable base effects. However, the trend still remains largely sticky to the upside.

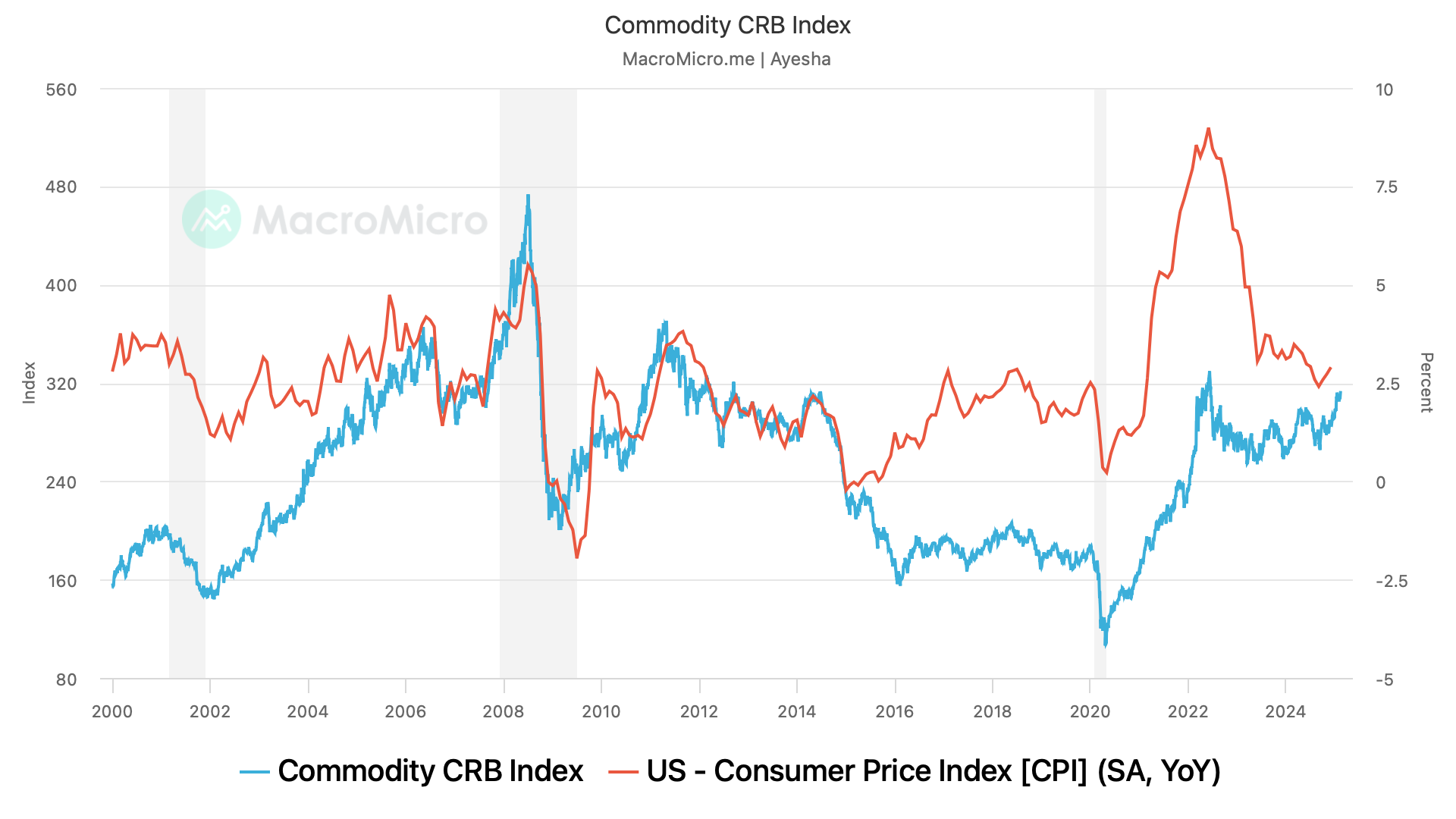

We’ve been seeing commodity prices increase over the past few months, and it should come as no surprise that MoM numbers increased to 0.4% from 0.3% in the previous month. While this was largely driven by energy prices, food inflation also continues to be sticky. As we can see below, there is a correlation between the two. ⤵️

Core inflation is also expected to pick up on month on month but moderate at the headline level to 3.1%, the lowest number since April 2021. The drivers are expected to be Autos (New & Used) and Shelter Inflation, which in turn is expected to be driven by OER & Lodging away from home.

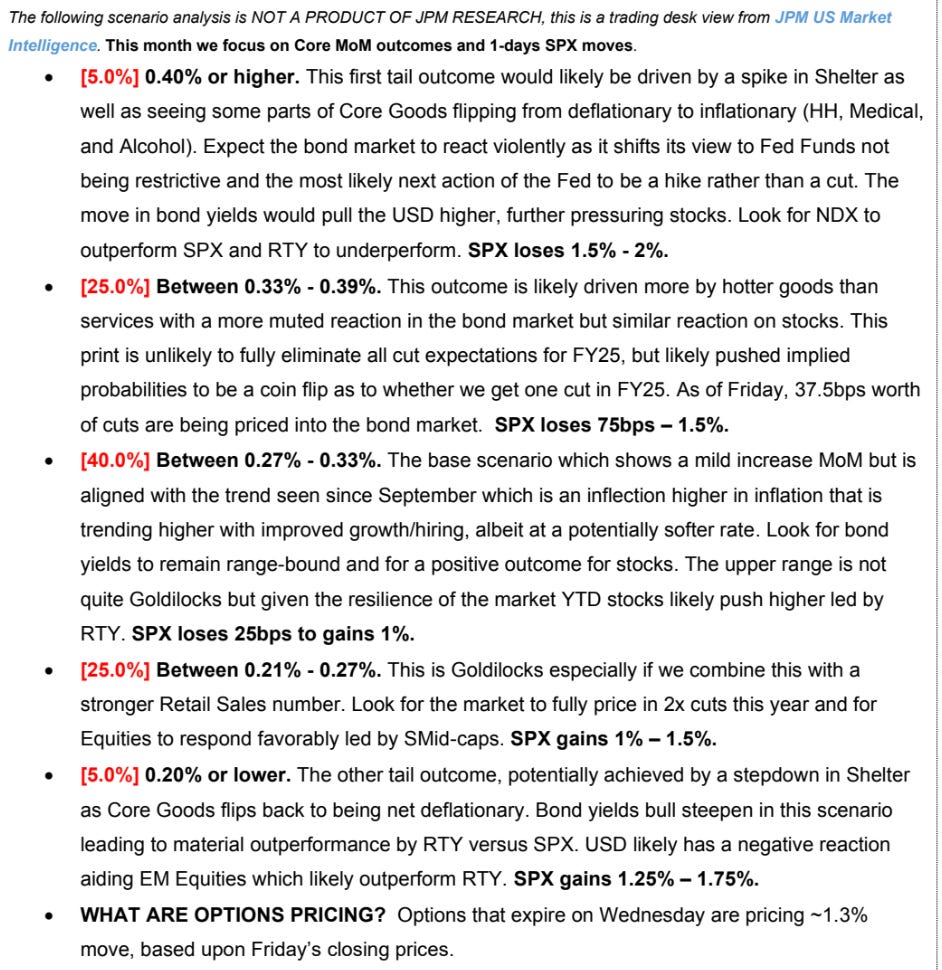

JPM’s SPX moves matrix tells us that we need to see MoM core inflation above 0.33% or lower, to see gains in the S&P 500.

What We’re Watching

8:30 am ET: US CPI Inflation

10 am ET: Fed Chair Powell’s Testimony

Earnings: Vertiv, Cisco, CVS, and Robinhood

Calendars

(news taken from Reuters, FT, Bloomberg; Calendar from Trading Economics)