Breakfast Bites - Triple Witching OpEx

President Trump takes a pause for 2 weeks on the Middle East

Rise and shine everyone.

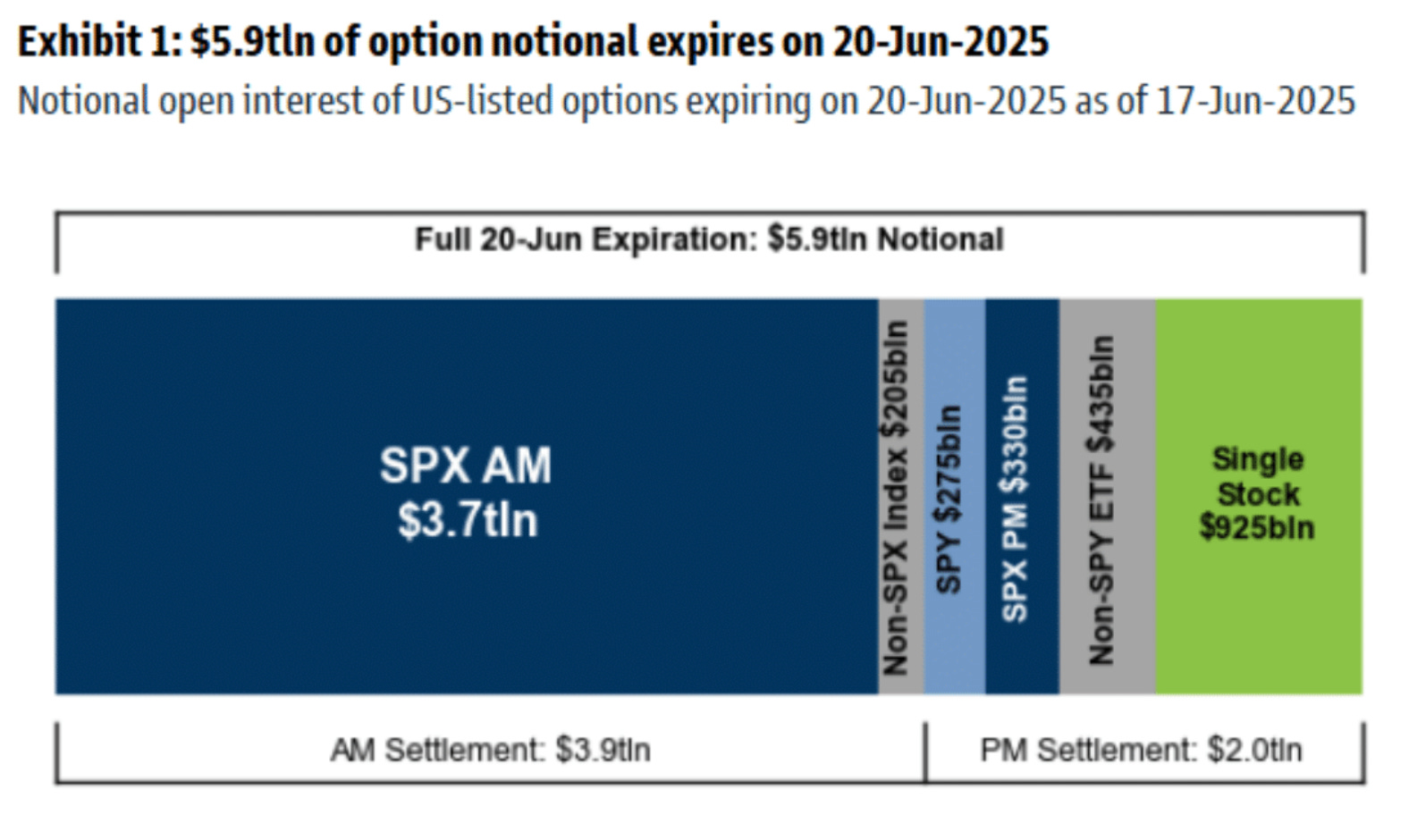

It’s OpEx Friday, and triple witching at that. According to Goldman Sachs, $5.9T in notional expires today, “including $4.0 trillion of SPX options and $925 billion notional of single stock options. This options expiration will be the largest June expiration on record.”

This week’s Fed meeting didn’t bring us any big surprises in terms of projections for rate cuts. The projections showed an increase in inflation forecasts and a decrease in GDP growth forecasts, the median projection for rates remained the same. Interestingly enough though, the dot plot showed 7 members now think there should be no rate cuts this year, this is up from 4 in March.

The market is pricing in optimism that tariff levels will reduce from the initial reciprocal levels that were announced in April. At these lower levels, the tairffs can be absorbed through the supply chain, limiting consumer price increases. That, in turn, could translate into more benign inflation data—giving the Fed room to cut rates.

Markets are still choppy though, as we wait for a decision on how the US will proceed about the conflict in the Middle East. The situation hasn’t escalated as such but, it hasn’t calmed down either.

Oil prices dropped sharply by 3% during early Asian trading as markets responded to tentative signs of de-escalation in the Middle East. US equity futures, led by the Nasdaq which rose 0.9%, rebounded strongly and erased the losses seen over the past 24 hours.

The rebound followed President Trump’s statement offering a two-week window to decide on direct military action against Iran. The delay is being seen as a potential opening for diplomacy to resolve tensions around Iran’s nuclear program, particularly fears surrounding the Fordow facility.

Gold prices also pulled back, down around $100 from Monday’s highs, as markets leaned into a more risk-on stance. There’s a sense that a peaceful resolution between Israel and Iran may still be possible, calming some of the geopolitical nerves that had driven haven demand.

Asian equities were upbeat, with the Kospi and Hong Kong markets both outperforming. Kospi surged 1.2%, continuing its strong rally since the June 3rd presidential election. The index broke through the 3,000 level, reaching highs not seen since 2021.

In FX markets, most major currencies regained some ground against the US dollar, with the exception of the Japanese yen, which remained relatively strong.

Chart of the Day - SPX Gamma from GS

“We think there’s currently close to $15bn of gamma in the market, and a high concentration on strikes slightly below the market’s current level – so we think the chart below does a good job of illustrating the shape of the S&P dealer gamma curve (dealers get longer on selloffs / less long on rallies), but just by a much smaller magnitude (our model likely underestimates the amount of dealer long gamma driven by OTC products that supply dealers with short-dated optionality). We expect this dynamic to shift post month-end – mainly as a result of 1) the rolling of big quarterly listed positions, and 2) re-striking of overwriting products that will then be above spot.” - GS

Calendars

(news taken from Reuters, FT, Bloomberg; Calendar from Trading Economics)

Why does the AM always have such a high amount? Also it looks like the AM is about 2/3 of the total for the day, so by 9:30am EST 2/3 of the options have expired? Thanks