Breakfast Bites - Trade talks and Middle East tensions

CPI and 10Y auction went well; PPI and 30Y auction today

Rise and shine everyone.

Yesterday’s US CPI surprised to the downside, and the market seemed to celebrate that a little too early. Much of the readout was quite basic, and as we discussed yesterday, energy deflation was the major driving force. There wasn’t a big move in Shelter Inflation, and Food Inflation seems to have moved up again.

Yields, however, moved lower, and that carried through to the 10Y auction, which wasn’t as bad as feared. We have the 30Y auction today, and it’s looking far more optimistic than the last one. Markets are also pricing in a softer Fed at the shorter end, given the benign CPI print. I still think that we’re going to see the effects of tariffs in July - either the release in July (June numbers) or the release in August.

Trade talks also seemed to have been going well with China, as posted by President Trump, but later on we heard from Lutnick and Bessent that there was still some ways to go. Bessent also delivered his testimony to Congress. I caught a little bit of it live, and there seems to be a lot of questions surrounding the One Big Beautiful Bill and the repercussions of that.

One interesting update - Bessent said his 3-3-3 plan (3% deficit; 3% GDP Growth; 3 million BOE energy produced in the US) is targeted for the end of this Presidential term. For some reason, I remember that the target was the 3rd year of the current presidency, but now we have an update.

US Equity Markets sold off into the close, and futures continued to sell off overnight. We’re not below the 6000 mark on the S&P 500 futures. Trade tensions and Middle East Tensions seem to be weighing on markets.

President Trump announced that the US will issue “take it or leave it” tariff proposals to several trading partners within the next two weeks, signaling a shift to a more aggressive trade stance. This move follows the end of a 90-day tariff pause and aims to pressure countries into quick agreements on revised trade terms. While some partners may receive deadline extensions if they’re negotiating in good faith, the administration is preparing to act unilaterally if talks stall.

We saw oil spike yesterday, but is giving up its gains today. The US Embassy in Iraq was asked to evacuate non-essential personnel because of heightened security threats. It would seem they are also evacuating Kuwait and Bahrain. Apparently, Iran’s Defence Minister Aziz Nasirzadeh warned earlier today that Tehran would target US bases in the region if nuclear talks collapse and tensions with Washington escalate into conflict. Tensions eased slightly after reports that US envoy Witkoff will meet Iran’s foreign minister in Muscat on Sunday.

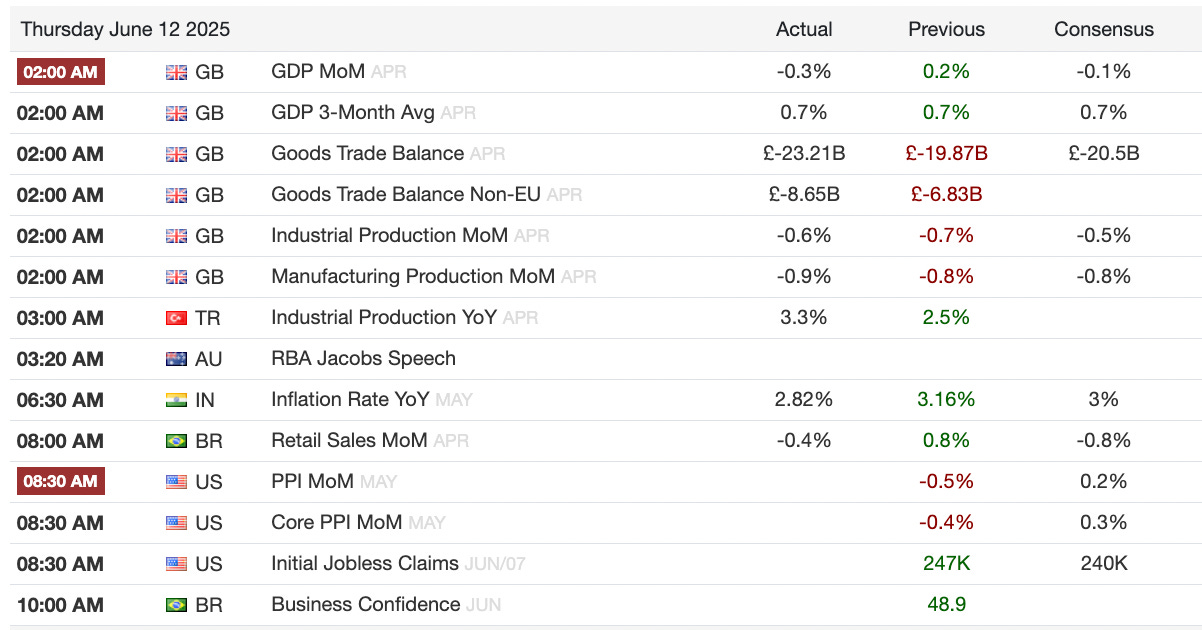

In the UK, economic data came in weak, with disappointing GDP and production growth and a worsening trade balance, despite new trade agreements with India and the US. The Chancellor is facing increased scrutiny following the large spending commitments announced in the triennial review, and analysts now widely expect tax hikes. Gilt yields have slipped, while the FTSE managed to hold flat and outperformed its European peers on rising hopes of a Bank of England rate cut.

And finally, Oracle raised its fiscal 2026 revenue forecast, with CEO Larry Ellison citing “astronomical and insatiable” demand for data center capacity and noting that the company is facing no GPU supply constraints. The stock is up over 7%.

Market Outlook

We may see some choppiness because of trade talks, but Middle East tensions are subsidising and PPI is coming up at 8:30 am ET, and if the disinflationary trend continues, we’re probably going to see the market buying stocks again.

What We’re Watching Today

8:30 am - US PPI

1 pm - 30Y auction

Adobe earnings after the close

Chart of the Day - Global growth set to slow

Calendars

(news taken from Reuters, FT, Bloomberg; Calendar from Trading Economics)