Breakfast Bites: The Shot Clock Is Ticking

Alphabet drops $80 billion on AI infrastructure, a Middle East ceasefire holds by a thread, and the most data-dense week of the month begins today.

Rise and shine everyone

Yesterday, a single Tasnim headline claiming Iran had set its agenda to fully block Hormuz sent WTI spiking above $94, the 10-year yield jumping, and the SPX dropping, all in under an hour. Then Trump walked it back. Oil gave half the move back. The S&P closed up ~0.3% for its eighth consecutive positive session, the longest winning streak of 2026. Bonds didn’t fully recover.

Equities are trading the news flow. Fixed income is trading the risk. The divergence won’t hold forever.

Here are three things we’re watching today:

JOLTS at 10am — after ISM Manufacturing hit a cycle high of 54.0, a tight labor print cements the hawkish Fed read and pushes the 10-year toward 4.55%.

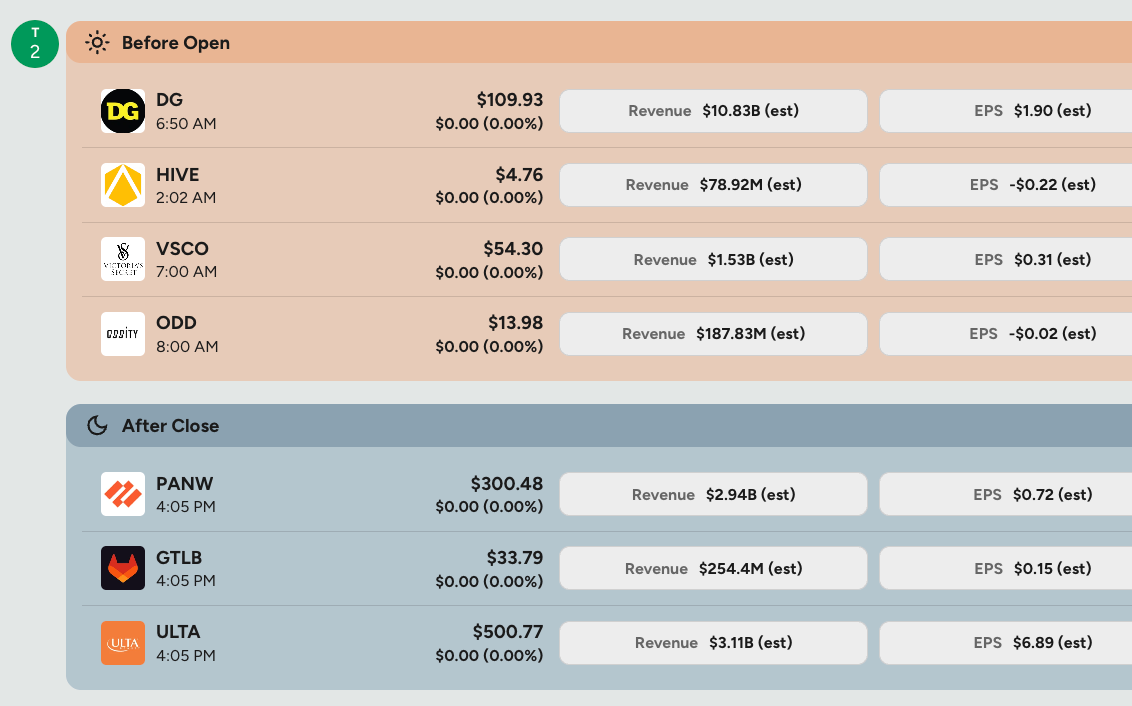

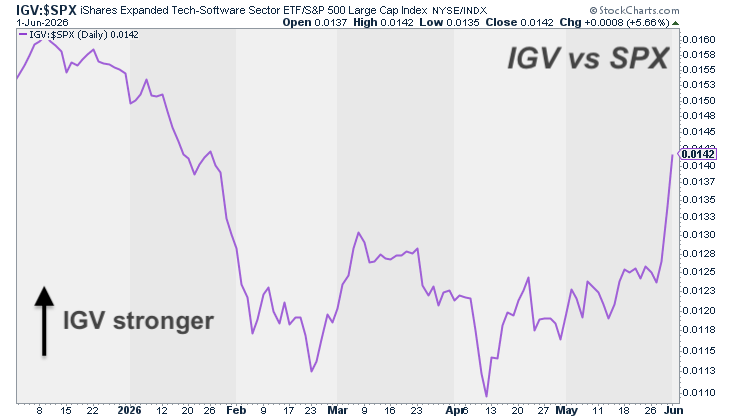

PANW after the close — the first real earnings test of whether yesterday’s 7.9% software squeeze has fundamental support or is running purely on short covering.

The ceasefire, or whatever it is — Trump claimed a deal, Netanyahu’s statement mentioned none, and Iran’s MOU text is still unsent; one headline out of Lebanon reprices oil and vol instantly.

I am tactically constructive but not adding high levels of risk here. The shot clock is ticking, and it is not just the Iran deal.

Morning Macro Briefing

The Middle East whipsawed markets before the US open yesterday, and the underlying picture has not meaningfully improved overnight.

Tasnim reported Tehran had set its agenda to completely block Hormuz and activate the Bab el-Mandeb strait. Oil has now had six sessions in the past ten where it spiked 4-5% on a headline and then gave most of it back–that is a market trading noise.

The behind-the-scenes picture is messier. Axios reported Trump called Netanyahu and told him to stop the Beirut escalation. The conversation was not diplomatic. According to sources, Trump told Netanyahu: “You’d be in prison if it weren’t for me. I’m saving your ass.” Netanyahu’s official statement afterward made no mention of a ceasefire and said Israel “will continue to operate as planned in southern Lebanon.” The Dahiya strike never came. Iran’s final MOU text remains unsent.

The story I am watching most closely is Oman. Washington has threatened to sanction and bomb a country that has served as America’s back-channel to Tehran for two centuries. The trigger was an intelligence assessment claiming Oman planned to join Iran in tolling Hormuz. Oman has denied it repeatedly. What it did do: refuse to sign the UAE-led UN statement condemning Iran’s tolling, decline to condemn Iranian drone attacks on its own ports, and its Sultan was the only Gulf leader to congratulate Iran’s new supreme leader.

The US is demanding that Oman pick a side. If Oman tilts toward Iran, it loses Washington. If it explicitly sides with Washington, it risks the country sitting 40 miles across the strait. The back-channel function that made Oman diplomatically indispensable is being destroyed by the exact pressure that needs it most. This is not a small development.

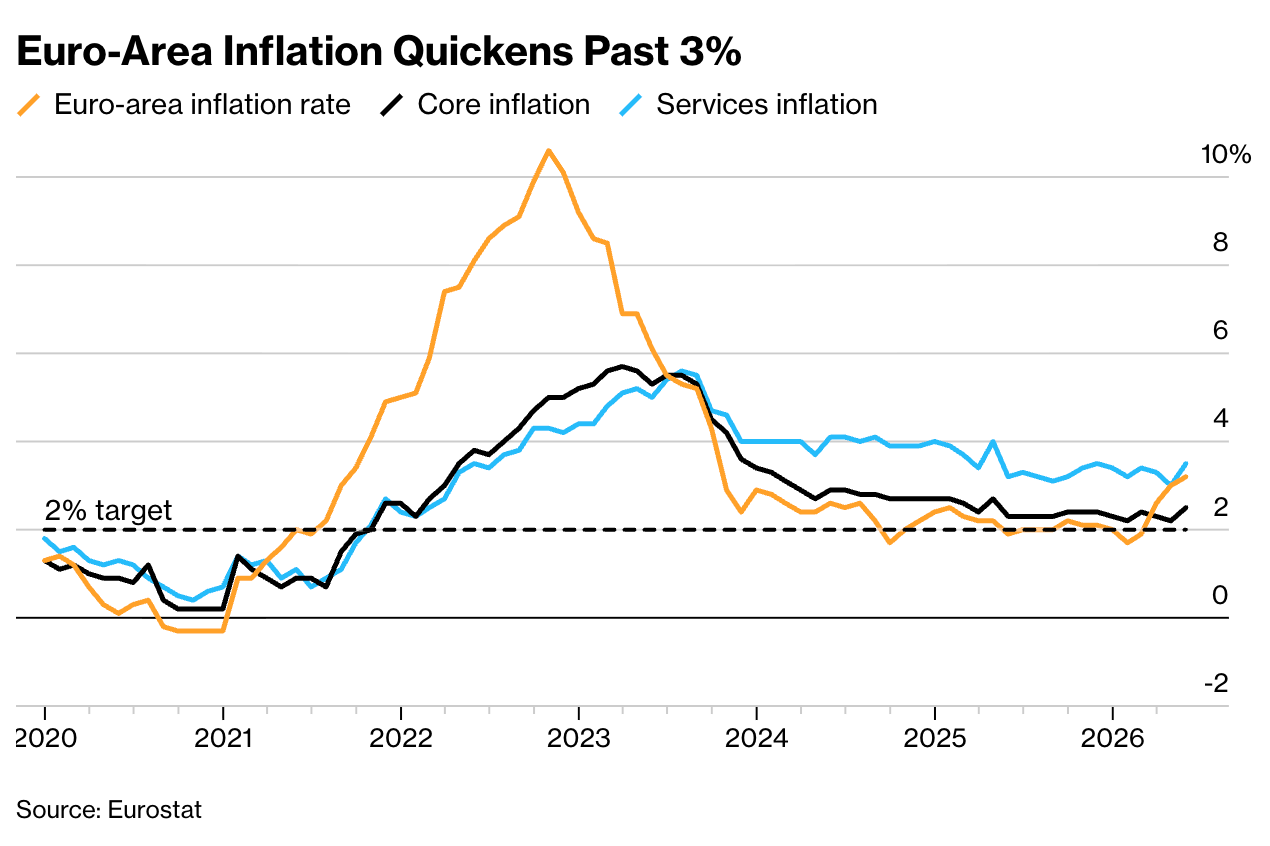

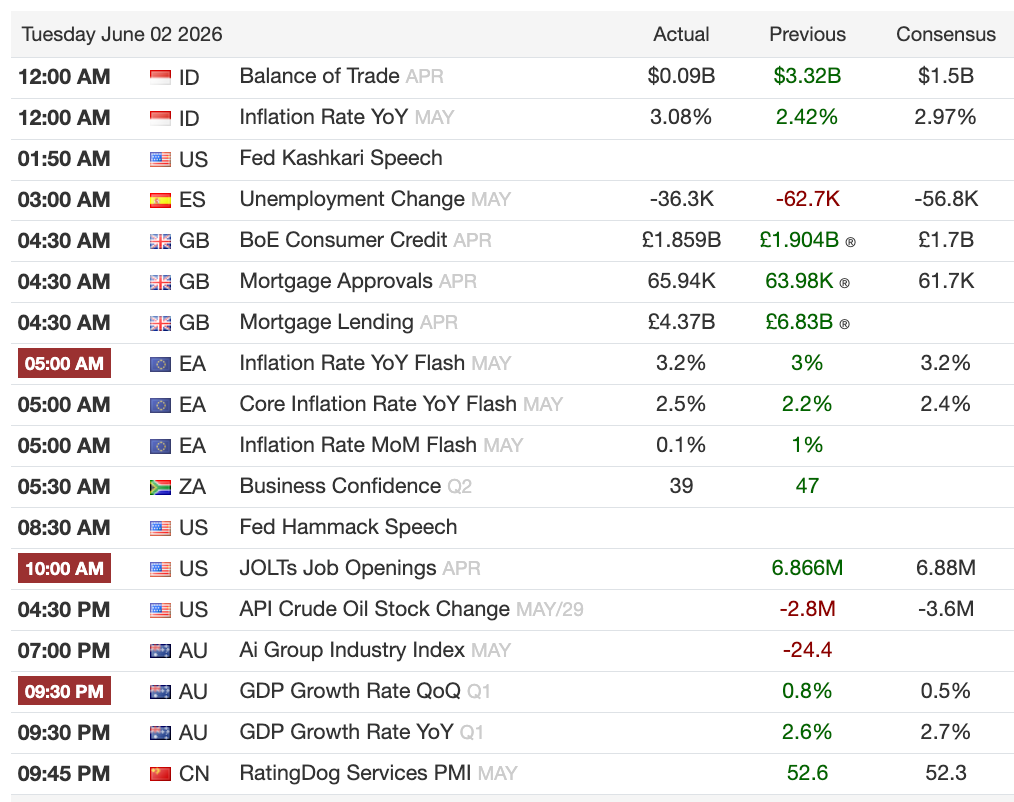

In Europe, inflation crossed 3% for the first time in over two and a half years. Euro-area CPI came in at 3.2% year-over-year in May, core at 2.5%, and services at 3.5%. France, Italy, and Spain all accelerated. The ECB June 11 hike is effectively locked. Isabel Schnabel said it is too early to specify how many more follow. Lithuania’s Simkus said a second hike after June is “more likely than not.” Finland’s Rehn framed it as insurance.

The tension here matters for allocation–the ECB is hiking into the fastest contraction in eurozone business activity since 2023. War-induced energy costs are feeding into wages and services, and the ECB cannot look away. That is not a bullish setup for European assets.

US ISM Manufacturing printed 54.0 in May, a new cycle high. New orders, employment, and the headline all beat. Prices paid fell modestly to 82.1 but remain at historically elevated levels. Supplier delivery times held at elevated readings. ISM respondents noted the Middle East conflict is causing shipment delays, while demand has held up better than expected.

Finally, the US imposed new punitive tariffs of 25% on Brazilian imports, taking the total to roughly 40% for most goods. Bitcoin touched $70,000 in the Asian session after MicroStrategy sold its first BTC since 2022 — Fed’s Kashkari also weighed in, jabbing that bitcoin has had 17 years and he’s still asking “where’s the beef.” Kyiv was struck in a massive overnight attack, with roughly ten people reported killed.

The AI Capital War

Google’s $80 billion package consists of a $40 billion at-the-market program beginning in Q3, $30 billion in underwritten shares and mandatory convertible preferred offerings, and a $10 billion private placement with Berkshire Hathaway. Goldman, JPM, and Morgan Stanley are running the books. The convertible and underwritten portions are priced tonight.

The stock fell on the news because a capital raise means diluting the existing shareholding base. Normally, I’d be alarmed, but two facts give me comfort:

Berkshire is doing a private placement, coming in before the market. This tells you how much confidence they have in this move.

The capital raise is not a significant portion of their market cap. It works out to be about 1.8% based on yesterday’s market cap.

CFO Anat Ashkenazi said in April that 2027 capex would be “significantly” higher than the up to $190 billion budgeted for 2026. Bloomberg Intelligence’s Mandeep Singh now believes that number could reach $300 billion, which would exceed Alphabet’s operating cash flow. This is not growth funded by earnings. It is growth funded by the capital markets, at scale, by the second most valuable company in the world.

In other news, Anthropic filed confidentially for an IPO yesterday. Revenue run-rate: $47 billion, up from $9 billion at end-2025. Valuation: approximately $965 billion. SpaceX prices next week, targeting $80 billion or more. OpenAI is expected to file imminently.

The competitive dynamic for the IPO queue matters here. As Singh put it, there is only so much capital you can allocate, even in public markets. Alphabet locking up institutional money into TPUs could crowd out SpaceX, Anthropic, and OpenAI. That race has now officially started.

Chart of the Day

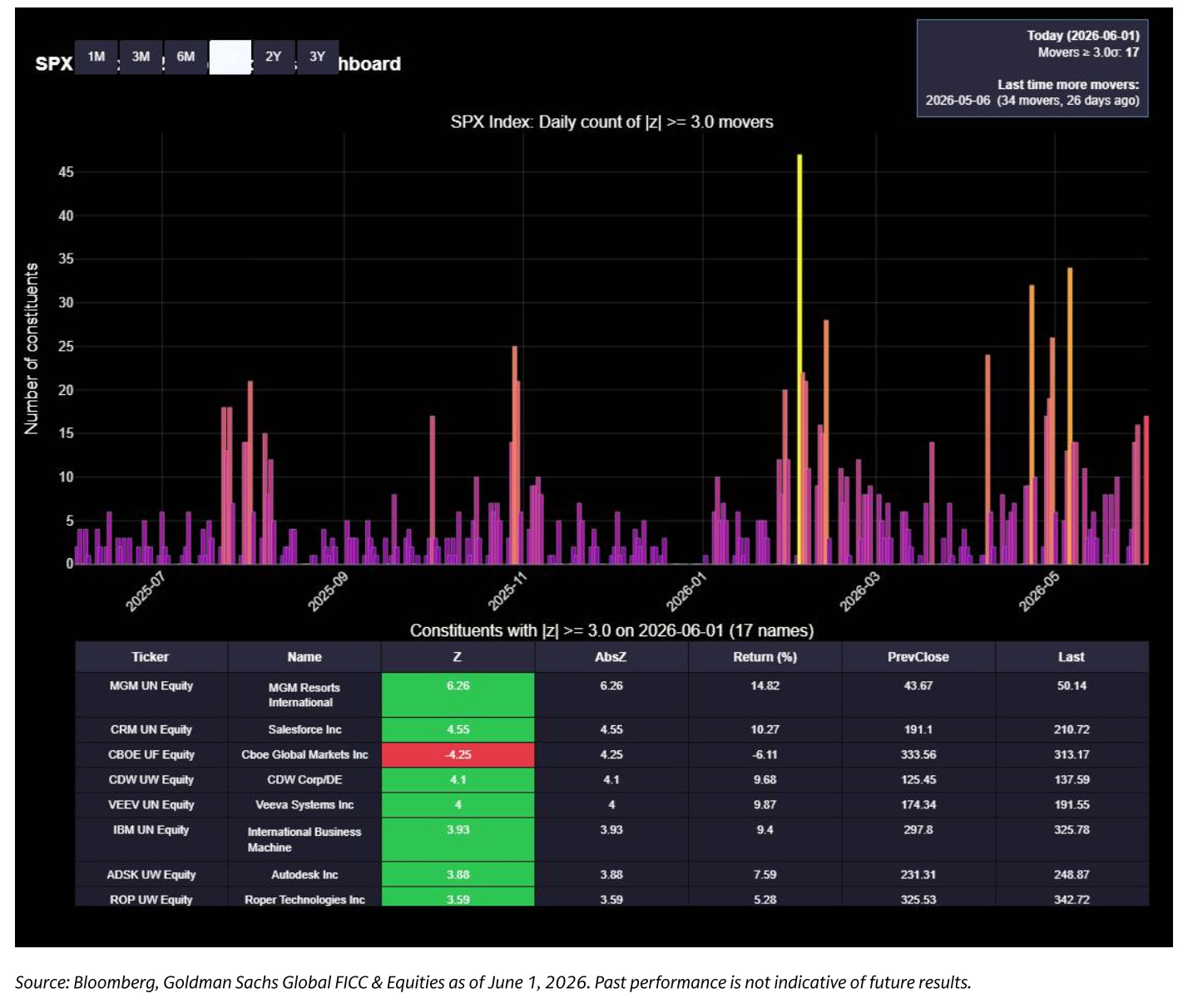

17 S&P 500 constituents moved three or more standard deviations, the highest reading since May 6 when 34 names moved on the same scale. That kind of dispersion is a market repricing individual stories, rotating hard between sectors, and punishing or rewarding positioning.

For investors, it means the index level tells you very little about what is actually happening underneath; the real action is in the cross-currents, and those cross-currents are running faster than they have in weeks.

Calendars

Market Prep

Software was the session’s dominant story. Goldman’s Software vs Semis basket moved 7.45% — its largest single-day move in over a year. IGV finished up 7.9%, 40% above its April lows and effectively flat on the year. LOs rotated hard into software, funded by supply in Megacap Internet and Semis. Momentum fell 3.3% (-1.9z) for a third consecutive session of underperformance, with the Goldman Momentum pair now down more than 5.5% over that stretch.

Jensen Huang’s Computex commentary is what directly led to new life in software. He also reinforced the AI infrastructure spend narrative.

Goldman noted a stat worth flagging: ETFs represented only 24% of the tape yesterday, the 37th consecutive session below 29%. In March, ETFs averaged 37% per day. Individual stock selection is driving this market more than passive flows. That matters for how quickly conditions can change.

There’s not much to consider today other than headlines moving the market. We’re coming into the session slightly subdued because the Middle East situation is seemingly getting messier. So let’s be nimble.