Breakfast Bites: The Relief That Wasn't

400M barrels hit the market, Brent crossed $100, and Iran hit Dubai. The off-ramp is not here yet.

Rise and shine everyone

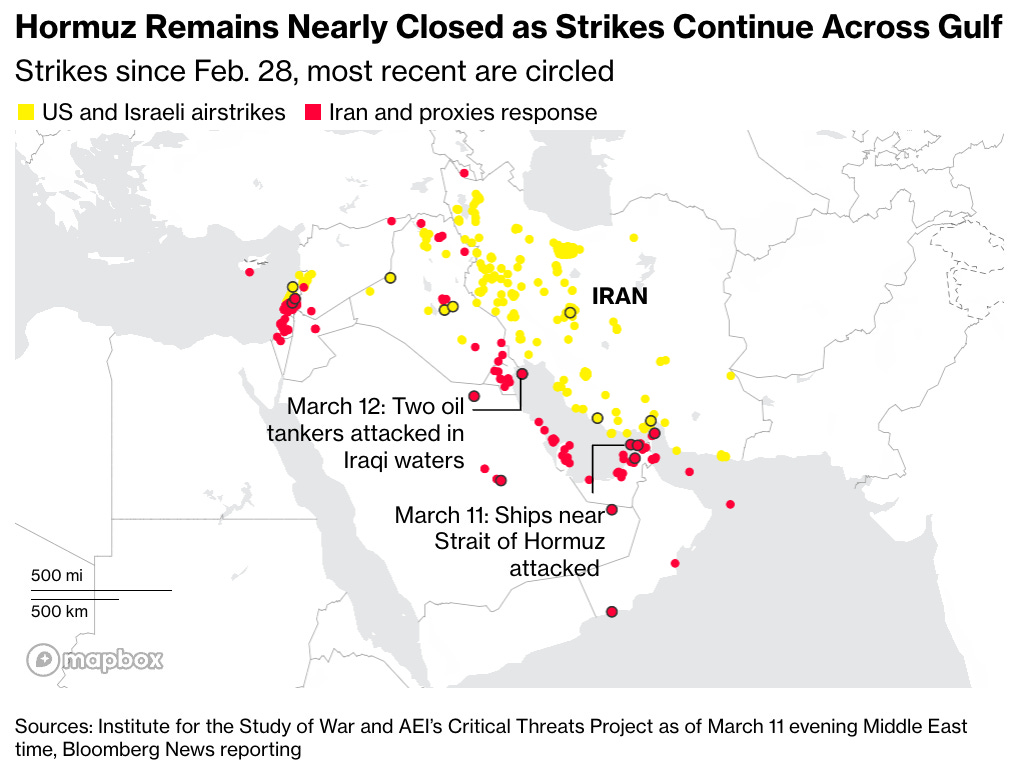

The IEA released a record 400M barrels of emergency oil on Wednesday and Brent crossed $100 anyway. Buy the rumor, sell the news. Markets had already priced in the relief, and then Iran struck Dubai overnight, drones hitting Creek Harbour while Goldman Sachs and Citi told staff to stay home.

The IEA called this the largest oil supply disruption in the history of the oil market, with 7.5% of global output affected. US Treasury auctions are softening, rate cut expectations are being repriced out across the curve, and energy costs have not even begun to fully flow through into the inflation data yet. This is no longer a war at the edges of the Gulf.

Morning Macro Briefing

Trump gave mixed signals on timing. He told Axios there is “practically nothing left to target,” then told a crowd in Kentucky “we don’t want to leave early.” Iran’s President Pezeshkian laid out Tehran’s ceasefire conditions publicly for the first time: firm international guarantees against future aggression, plus reparations. US and Israeli officials are privately saying this runs weeks, not days.

CPI yesterday came in broadly in-line with Core CPI MoM at +0.22%, and it was almost entirely sidelined by war headlines. The print captures February pricing before the Strait closed, before oil surged, and before the conflict injected a structural energy shock into the forward inflation picture. The Fed is in a difficult spot. It cannot cut into an energy-driven inflation surge, and it cannot hike into a growth shock. JPM’s Feroli estimates oil sustained well above $100/bbl equates to a 60bp drag on US GDP and a 40bp increase in headline CPI. The data that actually matters is March and April.

Speaking of rates, no cuts are now priced from any of the five major central banks meeting next week, the Fed, ECB, BoE, RBA, and BoC. The RBA has gone further, and is now seen as a potential hiker after Australian consumer inflation expectations jumped to 5.2%, the highest reading since 2023. The easing cycle is effectively on hold globally until there is clarity on where energy prices settle.

To make matters worse, USTR Greer has formally confirmed Section 301 investigations into 16 trading partners, including China, the EU, Mexico, Vietnam, India, and Japan. The aim is to conclude before the existing Section 122 tariffs expire on July 23-24. Markets have largely shrugged for now, assuming this is a replacement rather than an escalation, but the direction of travel is clear. Another layer of cost pressure on top of an already overwhelmed macro picture.

From JPM’s APAC Macro Conference in Singapore, the takeaways are worth sitting with. Geopolitical risk from Iran has now overtaken tariffs as the dominant near-term investor concern. Even a short conflict risks producing a material macro shock through lingering elevated oil prices and higher Treasury yields.

The Fed’s independence remains intact, but rate cuts are unlikely while inflation risks are elevated. Fiscal and AI investment dynamics are seen keeping rates higher than markets expect. And AI buildout is expected to be inflationary well before it delivers any productivity dividend. On the political side, the 2026 midterms are coming into view, with the House seen as likely to flip to Democrats as energy affordability becomes the defining pocketbook issue.

Chart of the Day

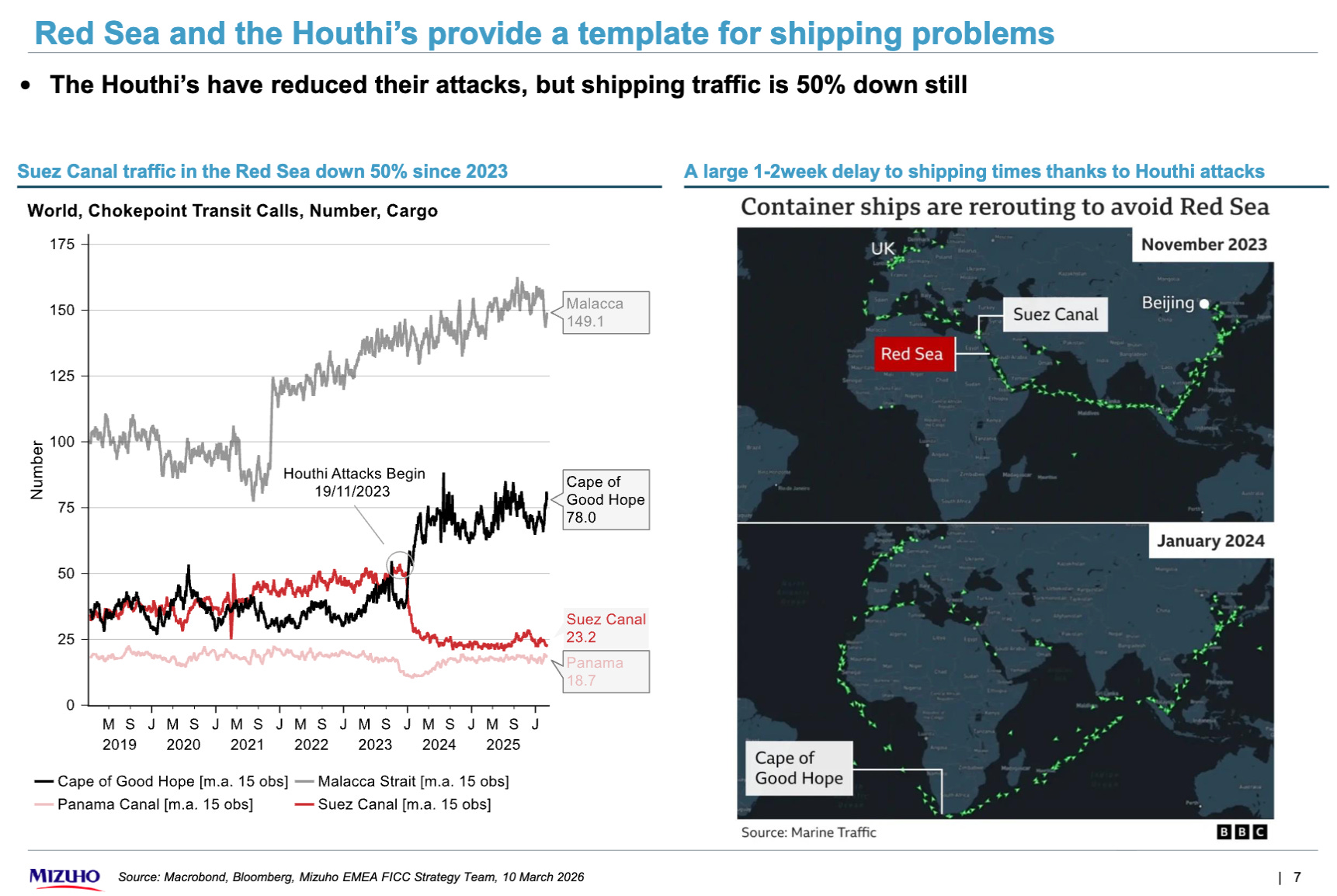

The Red Sea is the template nobody wanted to use again. Even after the Houthis reduced their attacks, Suez Canal traffic remains 50% below 2023 levels, with Cape of Good Hope rerouting adding one to two weeks to shipping times and largely staying that way.

The Strait of Hormuz is a far bigger chokepoint, handling roughly 20% of global oil and gas, and the insurance market, refinery run rates, and shipping decisions that repriced on day one will not snap back the moment a ceasefire is announced.

The Red Sea experience tells us that even the best-case scenario from here leaves global trade flows disrupted well into the second half of the year. Markets are not pricing that yet.

Calendars

Earnings today: ADBE, DG, DKS, LEN, ULTA.

Market Prep

Yesterday in the US was another session with no conviction. The SPX slipped fractionally, the NDX barely held, and small caps underperformed. Cyclicals and Mag 7 held up better, with some short covering adding a bid to high short interest names. The worst performing areas were retail, staples, housing, and airlines. Gold gave back some ground to around $5,176 as dollar strength competed with the safe-haven bid.

Asia closed sharply lower overnight. The Nikkei fell 2%, and most of the region followed, with only Shanghai managing to avoid losses greater than 1%. US equity futures were down around 0.9% during Asian trading and remain under pressure heading into the open.

European markets opened lower this morning, with most major indices in the red. The exception was the energy-heavy Scandinavian markets (Sweden, Finland, Norway), which got a lift from rising oil prices. Brent briefly pushed back above $100 as two oil tankers were attacked and onshore storage facilities in Oman were hit. The DAX was the notable underperformer, off over 1%.

European rate markets have shifted sharply, with Bund and gilt yields rising as easing expectations collapse entirely.

On US rates, the curve continues to sell off, and the USD is grinding higher, both reflecting the same dynamic: the war is tightening financial conditions through the commodity channel. People came into this conflict positioned long the 2Y and 5Y expecting cuts, according to GS. That trade got hit hard, and most have responded by adding on the dip rather than cutting. The 10Y sits just above 4.20%, and yesterday’s auction was soft, with demand at the weaker end of recent history.

In FX, USDJPY is back above 159 with no intervention warnings yet from Japanese officials. The Indian Rupee hit a fresh record low against the dollar at 92.41. The euro is weakening toward $1.15 as oil prices increasingly dominate currency moves.

Oracle’s earnings gave Infrastructure a fresh bid and the NVDA/Nebius $2B partnership added to the momentum. Software continues to lag semis for a third straight session as questions about demand durability linger. Airlines remain the most interesting tension in the market: demand is genuinely strong, with UAL posting its biggest booking day by revenue ever, but the fuel cost math is brutal, and guides will get cut.

A new stress point has emerged in private credit. Morgan Stanley is reportedly limiting redemptions on a private credit fund, and the chairman of Partner Group warned that default rates in private credit could double. JPMorgan and Cliffwater are reportedly facing similar redemption pressure. This is worth watching carefully as a second-order pressure point in an already fragile risk environment.

The overall posture has shifted to tactically bearish. Positioning is still broadly neutral, which means the de-risking has further to run if headlines deteriorate. The SPX is about 3.2% off its highs, with a full correction scenario putting the index around 6,270.

My Take

The market is still oscillating between the off-ramp trade and the prolonged disruption trade. Today, with Dubai actually being struck, we are in genuinely new territory.

The IEA calling this the largest oil shock in market history is not a throwaway line. The 400m barrel release was the high end of expectations and oil still went up. A ceasefire is a condition for recovery, not recovery itself. The insurance markets, refinery run rates across Asia, the shipping reroutes, none of that snaps back overnight.

I am watching the dollar carefully. It is strengthening on inflation fears, which is compressing the traditional safe-haven bid for gold. I think that is temporary.

The Section 301 tariff news is a slow-burning addition to an already overwhelmed market. It will not move things dramatically today, but it is another layer of cost that businesses and consumers will absorb on top of an energy shock.

I’ve highlighted a few sectors - both longs and shorts - that are worth watching in our tactical watchlist below.