Breakfast Bites - The Fed signals Stagflation

The Fed, BoE, PBoC and Riksbank all hold on rates

Rise and shine everyone

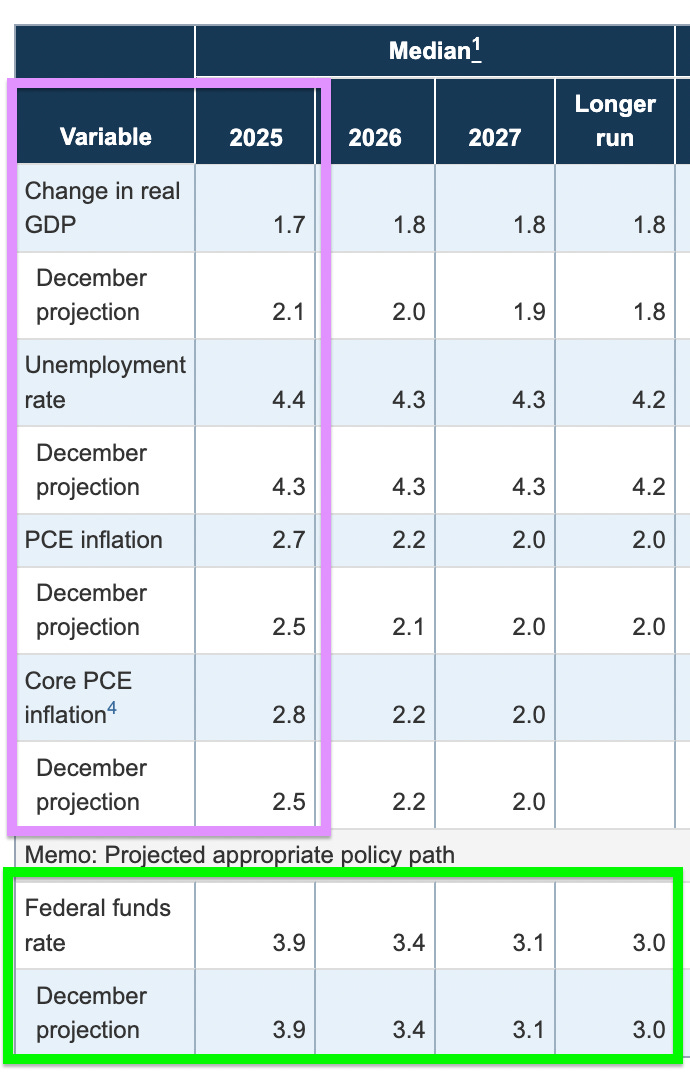

The Fed meeting is over… and we got quite a few changes, even if we didn’t get a change to rates. The Summary of Economic Projections (SEP) showed an increase in inflation and a decrease in growth - the classic definition of Stagflation.

The Fed also decided to slow the pace of QT from April by lowering the monthly cap for redemption of treasuries from $25B to $5B, this is in response to signs of tightness in money markets, even though reserves remain ample for now.

The biggest takeaway from the press conference was “uncertainty”. Chair Powell emphasized the “elevated level, heightened level” of uncertainty that’s stemming from the new administration’s policies. Tariffs, of course, featured significantly during the press conference as well and there’s no doubt that the Fed thinks tariffs are are driving inflation to a large extent.

There were no changes to rates, and although GDP growth projections have been lowered, the Fed doesn’t see the deceleration as enough of a threat to actually step in and cut rates. I suppose some of that is being balanced with the slowdown in QT.

For what it’s worth, the Fed does seem worried about inflation, and near-term inflation expectations, and this will likely mean that we’re not getting drastic rate cuts unless we see that the tariff inflation is transitory.

Moving on to the other two major rate decisions - China and the UK.

China had their first Loan Prime Rate Decision after all the recent policy changes announced. As expected they’ve continued to hold rates steady. We’re seeing the markets in Hong Kong underperform.

The Bank of England also held rates steady, even though the previous UK GDP reading came in lower than expected and growth is forecasted to slow to recessionary levels. Earlier this morning we got payroll data - the unemployment level remain unchanged, and as did base wages.

The Swiss National Bank (SNB) lowered rates by 25bps to 0.25%, citing subdued inflation and economic uncertainty. The Swiss franc weakened, while Swiss bonds outperformed, with 10-year yields declining by 4bps.

Meanwhile, the Riksbank kept rates steady at 2.25%, as expected, but highlighted risks from global trade tensions and geopolitical instability. The Swedish krona initially dipped before recovering.

Finally, we saw rate cut expectations increase in Australia - causing the ASX to jump by 1.1%. Australian jobs data came in weaker than expected and the market is now pricing in a higher probability of a cut for the next meeting in April, ahead of their Federal Elections in May.

US Equity Futures are pulling back this morning after yesterday’s surge post the Fed rate decision. The next major event now will be the April 2nd global tariff announcements. This is what’s driving a lot of decision-making because we’re still uncertain of what these announcements will look like, at this stage.

Chart of the Day

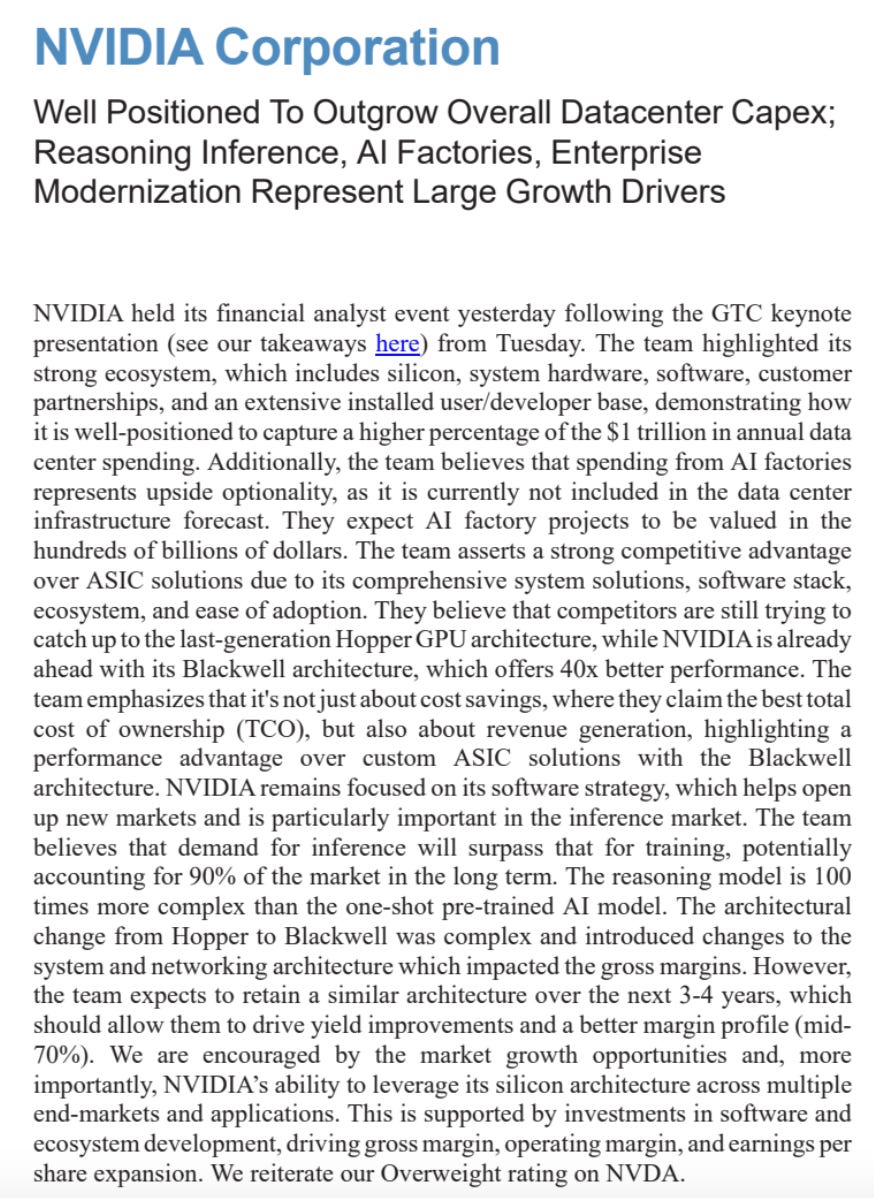

Here’s a summary of JP Morgan’s note on Nvidia, post the GTC event.

What We’re Watching

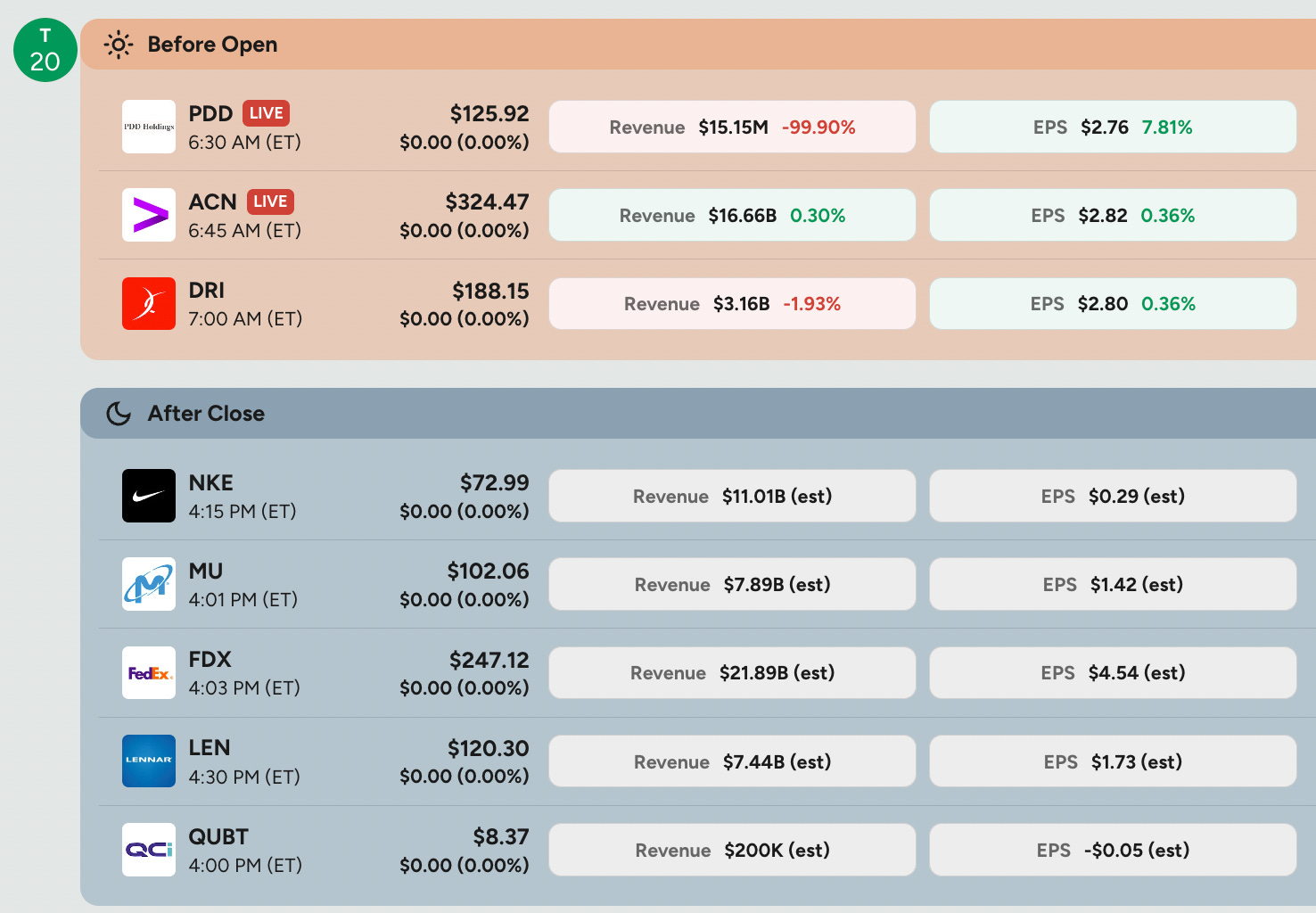

Earnings after the close - FedEx, Nike, Micron, and Lennar

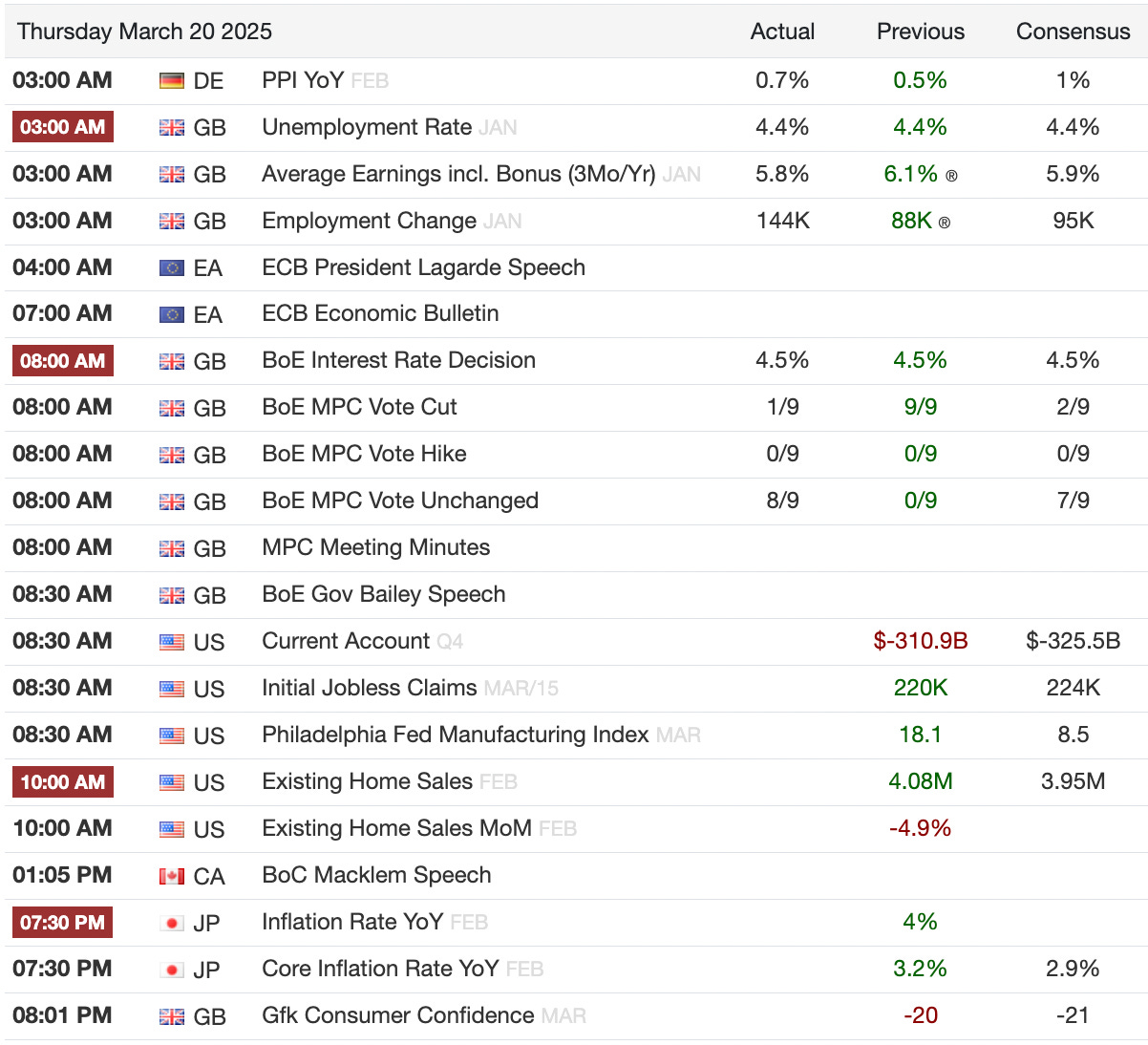

Japan’s Inflation release at 7:30 pm ET / early morning in Asia

Calendars

(news taken from Reuters, FT, Bloomberg; Calendar from Trading Economics)