Breakfast Bites: The Chip Unwind Deepens

US chip stocks slide into a bear market as the momentum unwind goes global, Netflix disappoints again, and Middle East strikes keep oil bid into the weekend.

Rise and shine everyone

Tech is selling off hard again, and it helps to be clear about why. This is not one story but three stacked on top of each other. Chinese AI startup Moonshot said its Kimi K3 model can rival the best US offerings, reviving memories of last year’s DeepSeek moment. President Xi then all but confirmed at the World AI Conference that AI is joining the list of industries China intends to export deflation through, which strikes directly at the profitability assumptions underpinning the entire AI trade.

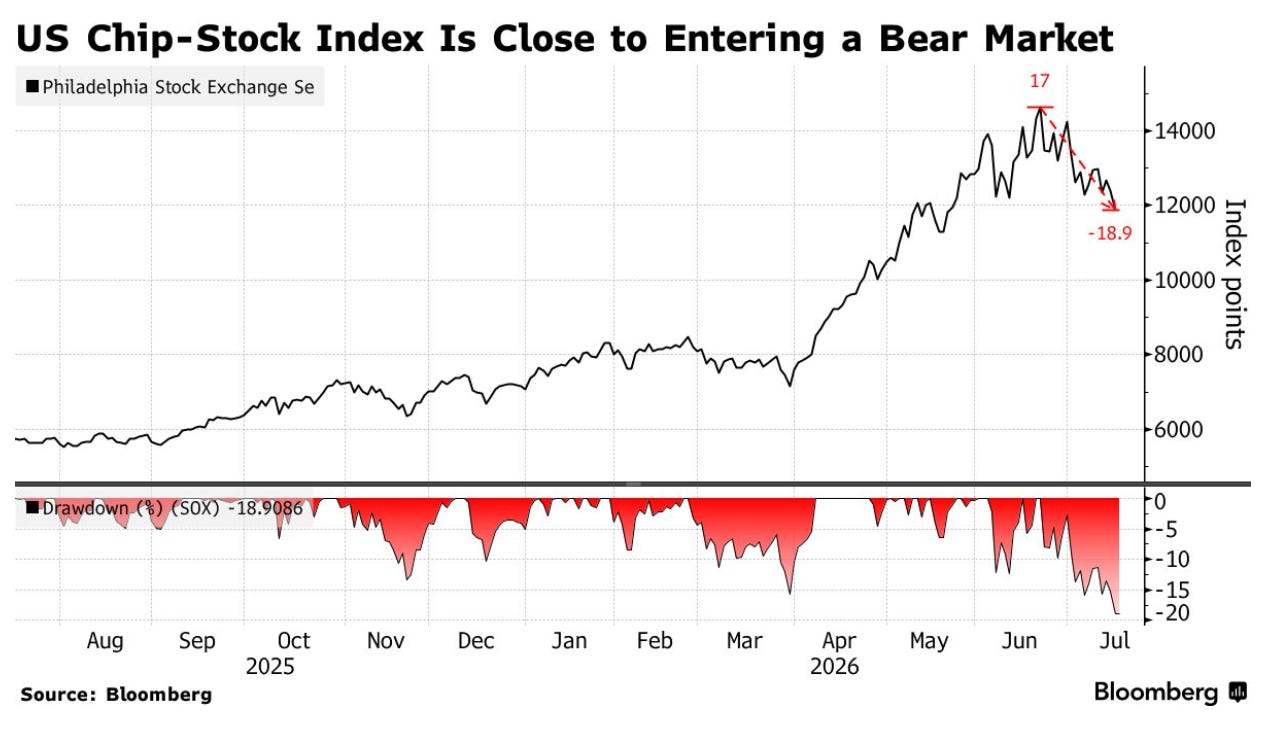

Layer that on top of a momentum unwind that was already underway and positioning that was extremely crowded in semis, and you get today’s tape. Nasdaq 100 futures were down 2.2%, the Philadelphia Semiconductor Index is on the cusp of a bear market, and the Nikkei fell 6% in a rout.

But here is the thing I keep coming back to. On Thursday, 369 stocks in the S&P 500 rose while 132 fell. This still looks like a violent rotation out of one crowded trade, not a liquidation of everything.

The timing is what makes it dangerous. Tech earnings are upon us, and the market has decided that good is no longer good enough. TSMC printed a record quarter with 67.7% gross margins and raised capex guidance, and its ADRs still fell to one-month lows.

Here is what we are watching today:

The global chip selloff, with SOX entering a bear market, Taiwan in technical correction, and the Nikkei at its weakest in nearly two months

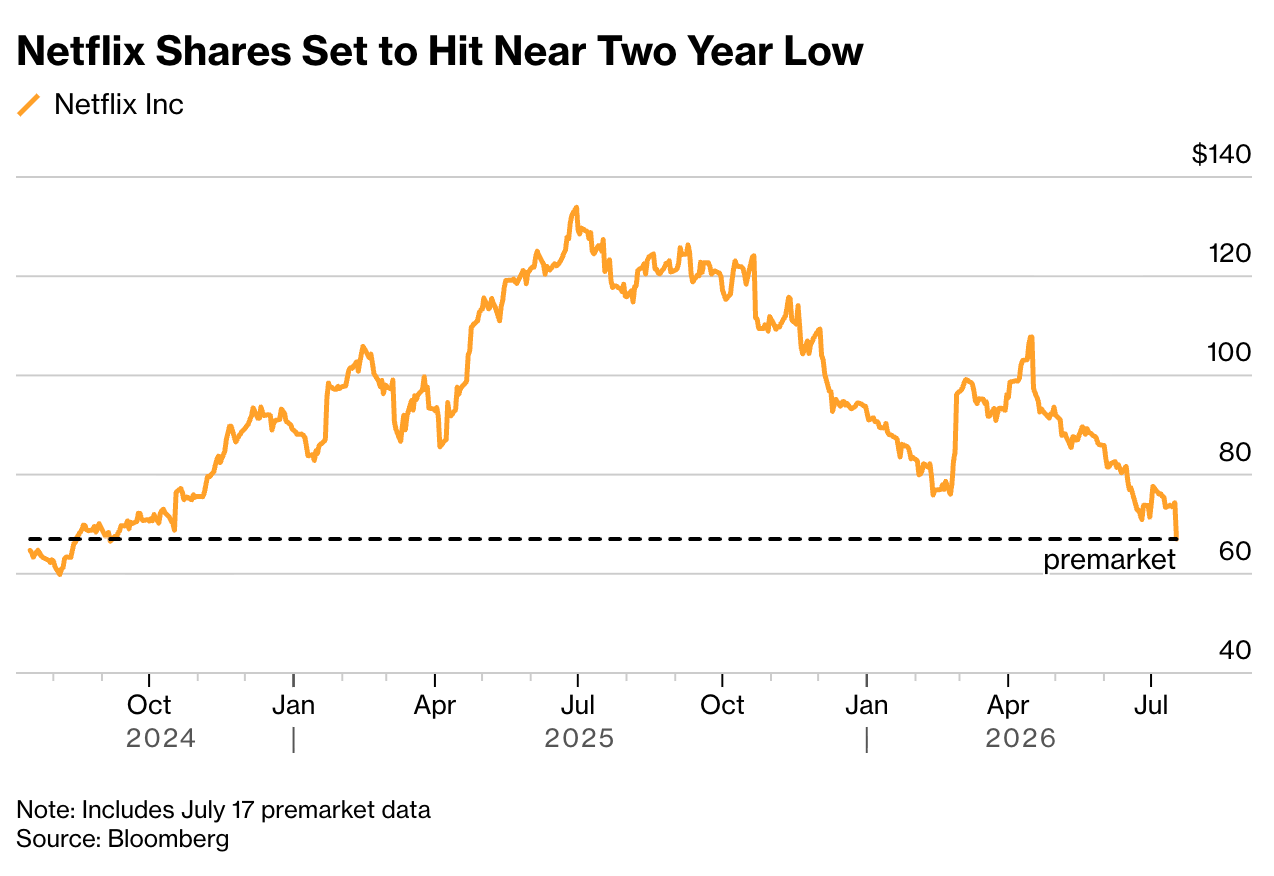

Netflix, down 9.7% premarket after guiding to a second straight quarter of slowing sales growth

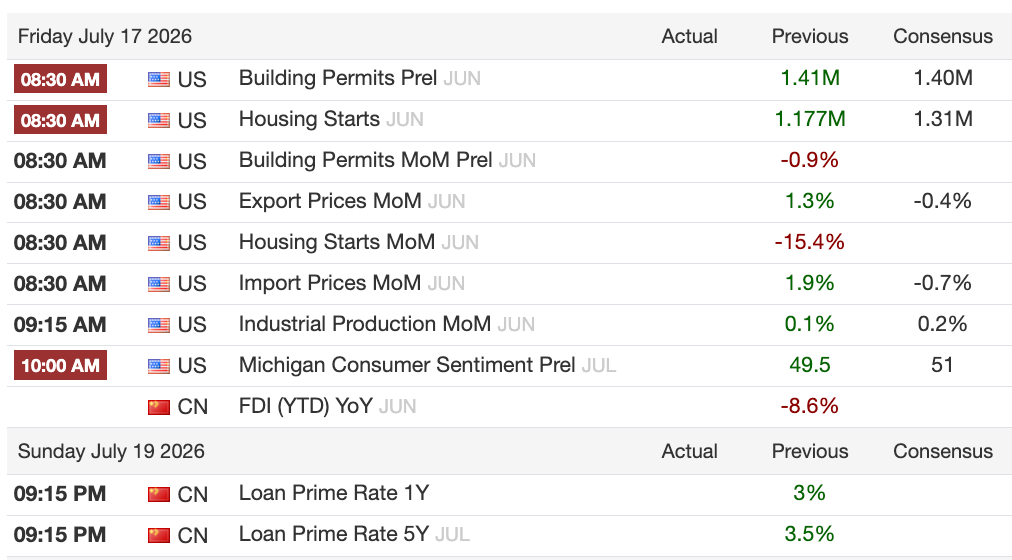

Michigan consumer sentiment this morning, plus weekend risk from intensifying US and Iran strikes with Brent above $85

Below, Goldman’s momentum desk puts numbers on how far this unwind has run and what history says comes next, including the median one-month return after drawdowns of this size. We also cover the specific hedge BofA likes with a payout ratio above 15x, and where I stand on Netflix after the reset.

Morning Macro Briefing

The Middle East picture has not fundamentally changed, but the strikes are intensifying. The US hit Iranian military sites and the civilian maritime control tower at Chabahar, Iran’s only deep-water port with direct Indian Ocean access, while Iran struck targets reported in Bahrain, Kuwait, Jordan and Qatar. The IRGC is reportedly in Yemen pressing the Houthis to close Red Sea access if US attacks escalate, which would put the Bab al-Mandeb Strait and roughly 4 million barrels per day at risk.

Brent is trading above $85 and heading for its biggest weekly gain since April. JPM’s Market Intel desk frames long energy equities and commodities as a Texas Hedge, meaning a position that pays off precisely in the scenario that hurts the rest of your book, and I agree with the logic. Some long energy exposure into the weekend makes sense, but I would not overdo it. This war has been unpredictable to say the least, and sizing matters more than conviction here.

Rates are behaving well despite the oil move. The 10-year yield is down at 4.53% after a soft June PPI, with headline down 0.3% on the month against a flat consensus. Disinflation is doing the market a favor for now, though JPM’s economists still track core PCE in the 3.3% to 3.4% range, so this is progress, not victory.

China is the underpriced macro story beneath the AI noise. The PBOC just made its biggest weekly net cash injection since January 2023, and the Loan Prime Rate decision is due Sunday. Beijing supplying liquidity while its AI champions export price deflation is a combination worth noting, because it hurts Chinese AI names too. Zhipu fell 25%, and the Hang Seng AI index is at a near two-year low.

Gold is holding just below $4,000, only a few dollars from its late June lows, and silver at $55 is back to early December levels. I keep the long gold bias from the watchlist, but I want to see the late June low hold. A clean break below it turns me patient rather than aggressive on adding.

Michigan consumer sentiment is out this morning. The consumer has looked resilient all through earnings season, with United, JPM’s read on retail sales, and the insurers all pointing the same direction. A strong sentiment print supports the consumer-facing trades where positioning is still light, which is exactly where rotation flows are heading.

Chart of the Day

US chip stocks are entering a bear market. The Philadelphia Semiconductor Index is roughly 20% off its highs and set to extend Thursday’s losses, yet it is still up 68% this year. That gap between the drawdown and the year-to-date gain tells you what this is - a crowded trade being forcibly de-risked rather than a fundamental collapse, because the fundamentals just printed a record quarter at TSMC. The index is the cleanest single expression of the market’s AI capex anxiety, and until it stabilizes, rallies elsewhere in tech will struggle to hold. I would not buy this dip yet. The signal to watch is a day when semis fall and the index closes flat or up, which is what Thursday’s breadth already hinted at.

Calendars

A quiet calendar into the weekend, with Michigan consumer sentiment this morning the main US release and China’s Loan Prime Rate decision due Sunday.

Market Prep

Thursday’s session was weaker than the headline suggested for tech. The S&P 500 closed down 0.5% at 7,533, but the Nasdaq 100 fell 1.6% while the equal-weight index rose 1%, and VIX pushed up to 16.66. This morning, Nasdaq futures were down as much as 2.2% and S&P futures 1.1%, with the semiconductor ETF off 4% premarket, though all three have recovered a little as of this writing.

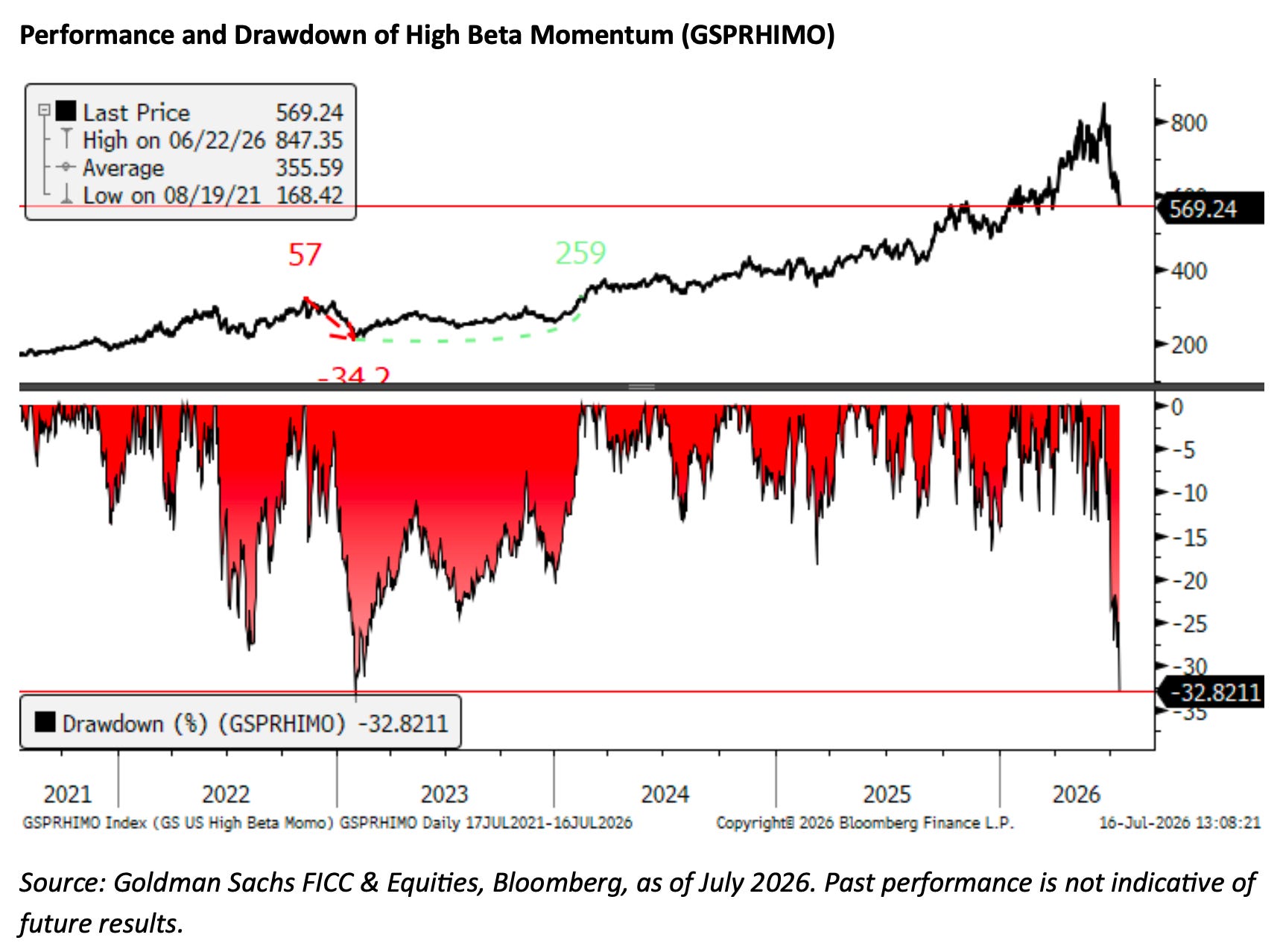

Goldman’s momentum pair, GSPRHIMO, is now down 33% from its highs and up only 12.5% on the year after peaking above 60% less than a month ago. Their desk thinks we are in the later innings of the unwind, with momentum exposure on the prime brokerage book down to the 77th percentile over one year. History leans the same way, since one-month drawdowns beyond 20% in this factor have produced median forward returns of 3.7% over one week and 5.8% over one month. The caveat is that exposure is still at the 95th percentile over five years, so a capex disappointment this earnings season could extend the pain.

Korea adds a structural wrinkle. Regulators banned new single-stock leveraged ETF and ETN listings after 18 products tracking Samsung and SK Hynix amplified price swings, and the Kospi is closed for a holiday today with Japan off Monday. Goldman’s derivatives desk likes owning Monday QQQ options as a cheap look at how Korea reopens Sunday night, a sensible way to own the event rather than guess it.

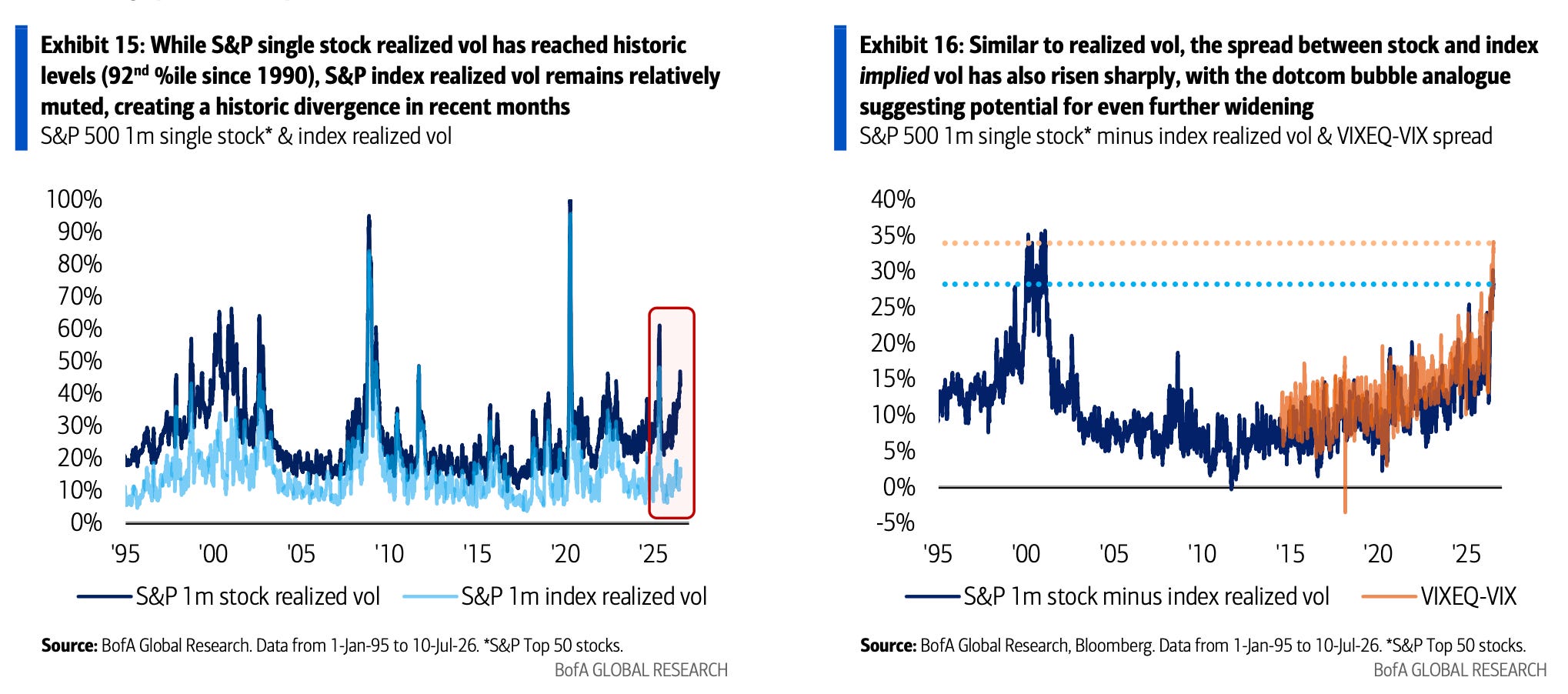

BofA’s volatility team frames the bigger risk. Single stock realized vol has reached levels last seen in the late stages of the dotcom bubble, while index vol stays muted because near-record low stock correlation, driven by semis de-correlating from everything else, suppresses it. If correlation snaps back, index vol jumps, and they like VIX call spreads with max payout ratios above 15x as the hedge. That is the trade I would fund with profits from the energy book rather than sell equities outright.

Netflix is the single-stock story of the morning, down 9.7% premarket after guiding Q3 revenue to $12.86 billion against a $13.01 billion consensus, the second straight quarter of slowing growth. The quarter itself was fine, with revenue of $12.6 billion and margins ahead of guidance. The problem is trust, since moving engagement disclosure from twice a year to annual while telling investors engagement is healthy invites exactly the skepticism it got. Goldman keeps a Buy with a $110 target against a $73.68 close, but with the stock down more than 40% over a year, I would let the reset finish before stepping in. This is now a show-me story into the next two quarters.

Three things to watch from here. Michigan sentiment this morning, where a firm print reinforces the rotation into consumer names and supports our XLY long. The weekend in the Gulf, because Houthi action against the Red Sea is the escalation that would actually move the oil and rates complex, and it is why I keep some energy exposure into Friday’s close, sized modestly. And Sunday night, when China’s LPR decision and Korea’s reopen give us the first honest read on whether this chip unwind has another leg.