Breakfast Bites: The Bounce and the Bill

Iran steps back, AI bounces for a second day, and a trillion dollars of new equity supply is lining up to test the rally.

Rise and shine everyone.

Today’s three things to watch:

Trump’s “1-2 days” deal claim hit this morning alongside an Apache helicopter down near Hormuz, cause unknown, and the Houthis declaring a maritime ban on Israeli-linked Red Sea vessels. Watch oil: Brent is at $93 and each headline moves it.

The Nasdaq cash open is the session’s first real test of whether the AI dip-buy holds. Kospi confirmed +8.2% in Asia with Samsung and SK Hynix leading, but US real money flow at the open is what matters. Futures are up 0.6%.

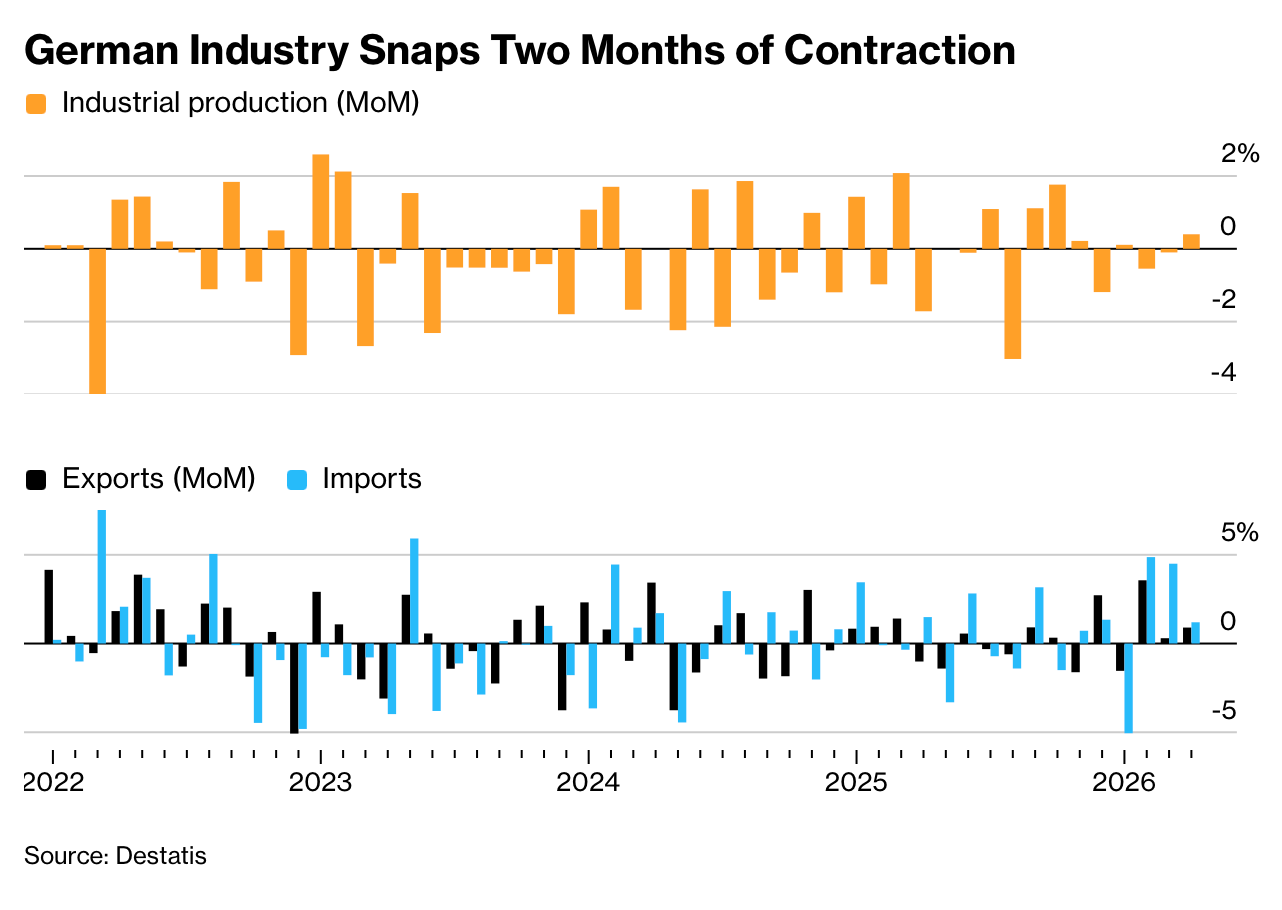

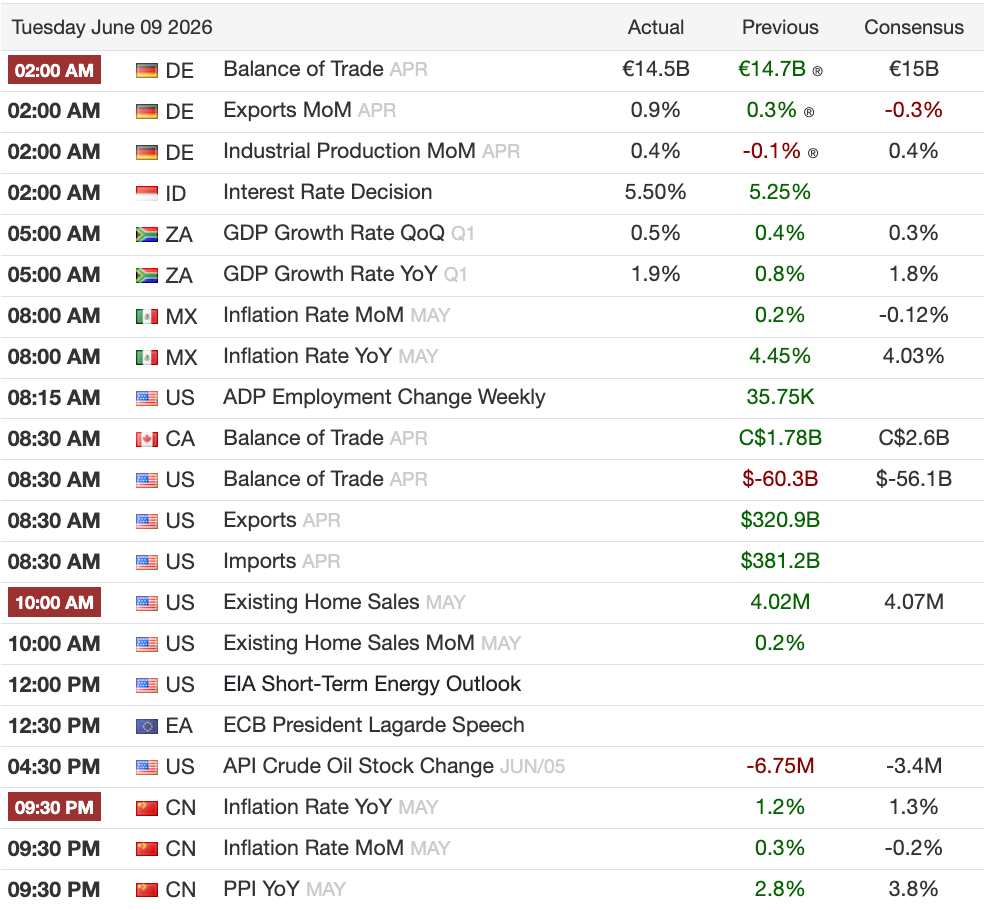

Two data prints landed this morning worth watching: Germany’s April industrial output posted its first gain since the war began, up 0.4%, and China’s May trade surplus came in above $105 billion with exports up approximately 20%. Both give the earliest hard read on how the conflict is transmitting into the real economy.

The Kospi’s +8.2% overnight recovery is the mechanical reverse of the previous leverage flush, similar to what we saw for the Nasdaq last Friday.

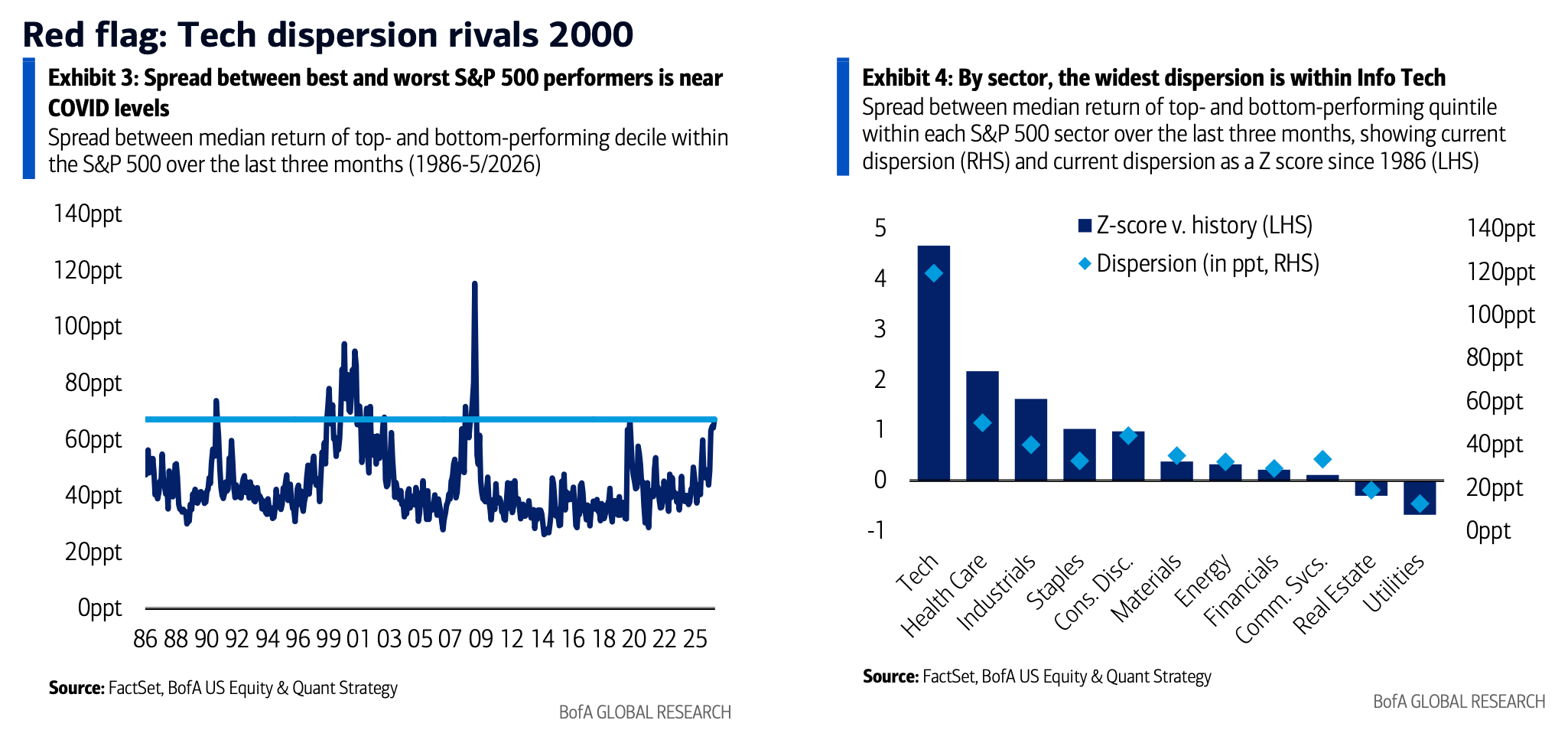

BofA’s Savita Subramanian flagged last week that 7 of her 10 historical bear market signposts are now triggered, matching the average at prior peaks. Tech dispersion within the S&P has reached 120 percentage points between the top and bottom performing quintiles, almost exactly where it was in February 2000.

Another point to note is that for roughly twenty years, buybacks shrank the supply of shares available to investors, and that structural tailwind helped push equity prices higher. That era is reversing. Hyperscalers are now issuing equity to fund AI infrastructure, and behind them sits roughly $1.1 trillion of new supply from SpaceX, OpenAI, and Anthropic, all rushing to market in the same window. This is effectively diluting the market to some extent.

Goldman’s Tony Pasquariello is still calling for 8000, and I don’t think that’s wrong. But his recommended posture says something: stay long equities, and buy put protection on the downside. A 3-month hedge on the S&P 500 costs under 2% of your position right now. For a market that has run this hard, that is cheap insurance.

Morning Macro Briefing

Israel and Iran exchanged ballistic missiles over the weekend then agreed to a halt on Monday. Trump told reporters Tuesday he is in the “final throes of what will be a very, very good deal,” expecting an outline within one or two days. Iranian President Pezeshkian said his country has “neither abandoned the battlefield nor the negotiating table.”

A US Army Apache went down near Hormuz with cause still unclear. The Houthis declared a maritime ban on Israeli-linked vessels in the Red Sea and launched a missile barrage at Israel. Brent fell 1.3% to around $93, but commercial traffic through the Strait remains thin and inventory buffers across petroleum products are running down fast.

German industrial output rose 0.4% in April, the first gain since the conflict began, driven mainly by construction. The economy ministry called activity “fairly subdued,” and April factory orders released Monday fell more than expected with sharp declines in autos and electrical equipment. ECB tightening expected this week adds another headwind.

China’s May trade surplus topped $105 billion, with exports up approximately 20% led by high-tech electronics and AI-related goods. Rare earth exports to Japan fell more than 80% year on year, and the US is reportedly pressing Beijing to restore supplies. The PBOC fixed the yuan at its strongest level since February 2023.

South Korea is launching on-site FX inspections to curb speculative won trading; the won added 1.2% on Tuesday after a 2% Monday rally. The 10-year Treasury yield sits at 4.55%, down 2 basis points. Gold holds near $4,340, with Citi cutting its 3-month target to $4,000 on Fed hike risk. Remember, as long as Central Banks remain hawkish, Gold is likely to remain under pressure.

Chart of the Day

The spread between the best and worst performing quintiles within S&P Information Technology has reached 120 percentage points over the last three months, almost exactly where it sat in February 2000. The median stock in today’s top quintile has gained 108% over three months; in February 2000 the equivalent figure was 119%, and the median 12-month forward return from that cohort was -57%.

Tech fundamentals in 2026 are healthier than 2000 on leverage and capital intensity. But hyperscaler capex as a share of operating cash flow is forecast to approach 100% this year, up from 40% in 2023. Extreme dispersion in a cycle where cash flow is being consumed rather than returned is a different proposition from healthy rotation.

Calendars

Market Prep

Nasdaq 100 futures are up 0.6%, with Kospi leading Asia at +8.2% on Samsung and SK Hynix strength. Nikkei gained over 2%. The ASX fell for a third session with minimal AI exposure to cushion the blow. Stoxx 600 is roughly flat. The S&P 500 enters Tuesday having shed 2.64% last week, giving up over $2 trillion in market cap on Friday alone.

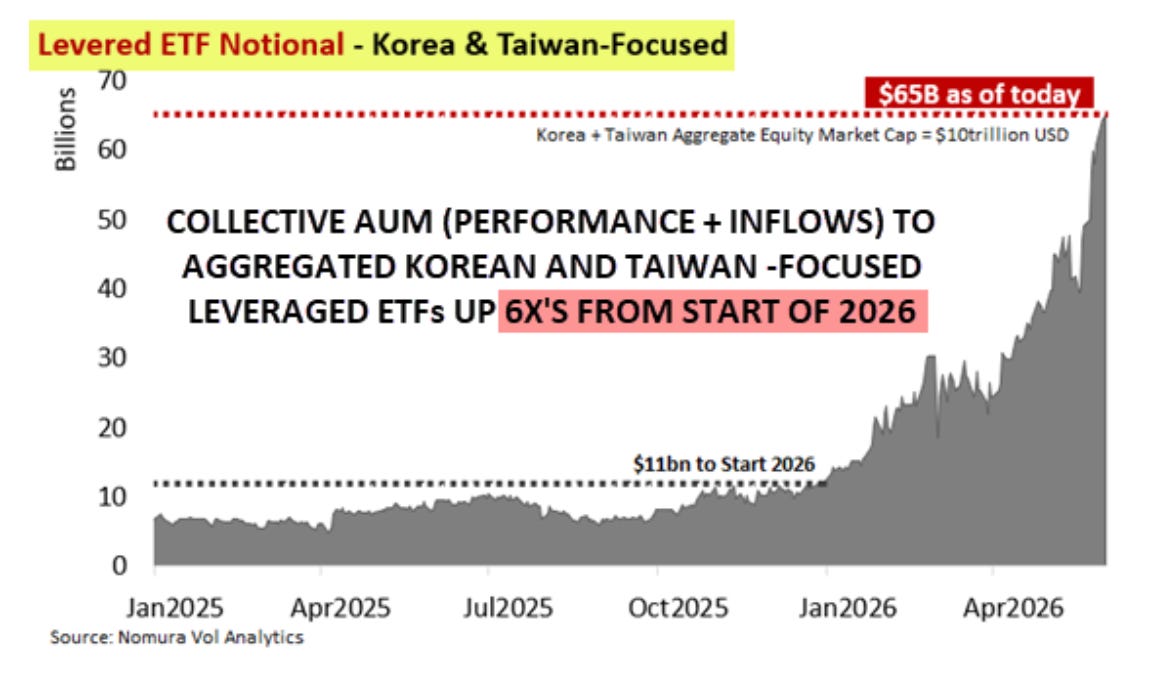

Friday’s selloff was mechanical, not fundamental. Leveraged ETFs tied to Korean and Asian tech names had grown 6x since January to $65 billion in assets. These products are designed to automatically sell when markets fall to maintain their leverage ratios, and that forced selling, estimated at $51.6 billion on Friday alone, overwhelmed normal buyers and sent the Nasdaq down 5%. Today’s Kospi recovery is largely that process running in reverse.

For roughly twenty years, buybacks shrank the supply of shares available to investors, and that structural tailwind quietly helped push equity prices higher. That era is reversing and hyperscalers are now issuing equity to fund AI infrastructure, with Alphabet already done and Meta reportedly next. Every new share issued is supply the market has to absorb, capping upside in the very names that have led this rally. Nomura’s Charlie McElligott calls this de facto call overwriting on their own stocks, and behind the hyperscalers sits roughly $1.1 trillion of additional AI-linked supply from SpaceX, OpenAI, and Anthropic all rushing to market in the same compressed window.

The options market was also flashing warning signs before Friday. Investors were paying more to bet on stocks going up than going down, an unusual setup that historically does not end well when new supply hits. Goldman’s prime brokerage data showed hedge funds heavily crowded into the same long positions with minimal short hedges.

On the corporate side: OpenAI’s confidential S-1 is filed with Goldman and Morgan Stanley running the deal, timing still open. GSK agreed to acquire Nuvalent for $10.6 billion in oncology. Apple used WWDC to lay out its next-generation AI platform, but the market was far from impressed.