Breakfast Bites: The Bigger They Come

Trump’s Beijing trip ends with modest deliverables, Iran back on the front burner, and rates hitting cycle highs into OpEx. Adding a new name to our Watchlist.

Rise and shine everyone.

The summit is over, and markets are getting the Iran reality check that was always waiting on the other side of Beijing.

Trump’s China visit produced agricultural purchase commitments, vague language about stabilizing trade, and some encouragement around a Boeing order. What it did not produce was a semiconductor breakthrough, a credible path to reopening the Strait of Hormuz, or any reduction in Iran war risk. Xi said the right words about wanting Hormuz open. Trump confirmed China wants US oil. Neither of those statements changes anything in the Middle East.

As Trump headed home, he said it was “just a question of time” on Iran, that he would not be “much more patient” with Tehran, and reiterated that strikes on enriched uranium remain on the table. US officials have reportedly already told Israel that fresh action could come almost immediately after his return, and Israel is on high alert this weekend. WTI has crossed $100 a barrel, global yields are spiking, and equities are selling off into today’s OpEx.

Morning Macro Briefing

The rates story is the dominant one this morning. Japan’s 10-year JGB yield jumped more than 10bps to 2.73%, the highest level since early 1997, as markets effectively called Finance Minister Katayama’s bluff on the extra budget denial. A BOJ official warned separately that Middle East-linked price pressures are spreading across a wide range of goods, and April PPI came in at 4.9% YoY against a 3.0% expectation. The wholesale PPI reading is the biggest YoY rise since May 2023, with naphtha prices up 83.2% month-on-month.

Korea’s 10-year yield also jumped 10bps to 4.182%, the highest since November 2023, and the KOSPI fell over 6%, led by Samsung on looming strike concerns.

US Treasuries followed Asian rates higher. The 10-year hit a one-year high of 4.530% and the 30-year reached 5.056%, a 10-month high. Fed futures are now pricing a 50% probability of at least a 25bps hike by December 2026, up from 35% on Thursday and just 1% a month ago.

Today also marks the formal Fed transition. Kevin Warsh officially takes the Chair title, Powell moves to governor, and Stuart Miran steps down. Fed’s Williams said yesterday that policy is “mildly restrictive” and he sees no reason to hike or cut, while Fed’s Barr warned against liquidity rule reductions that would shrink the balance sheet further.

The DXY has cleared its 50, 100, and 200-day moving averages over the past two sessions, driven by hot inflation prints, resilient jobs and retail sales data, and surging energy prices. MUFG noted in its morning note that the rolling correlation between the DXY and the 2-year US rates spread has strengthened notably this week, implying further dollar strength if rate hike pricing continues to build.

WTI pushed above $100 a barrel this morning, trading in a $97.23-100.93 range, with Brent at the upper end of a $106.26-109.68 range. The immediate catalyst was Iranian Foreign Minister Araghchi flagging that contradictory US signals remain the core obstacle, timed almost exactly with Trump’s sharpest public statement yet on Tehran. Goldman’s vessel tracking puts Strait of Hormuz flows at just 5% of normal on a four-day moving average basis.

Precious metals and copper are selling off as the energy-driven dollar catches a bid. Spot gold is down roughly 2% on the session, trading in a $4,532-4,665 range. Silver is being hit hard for a second straight day, falling from a $89.37 peak on Wednesday to a $77.66 low this morning, with the KOSPI-Silver correlation running at around 0.7 amplifying the Korean equity selloff through silver’s high-beta characteristics. LME copper has slipped below $14,000 a tonne.

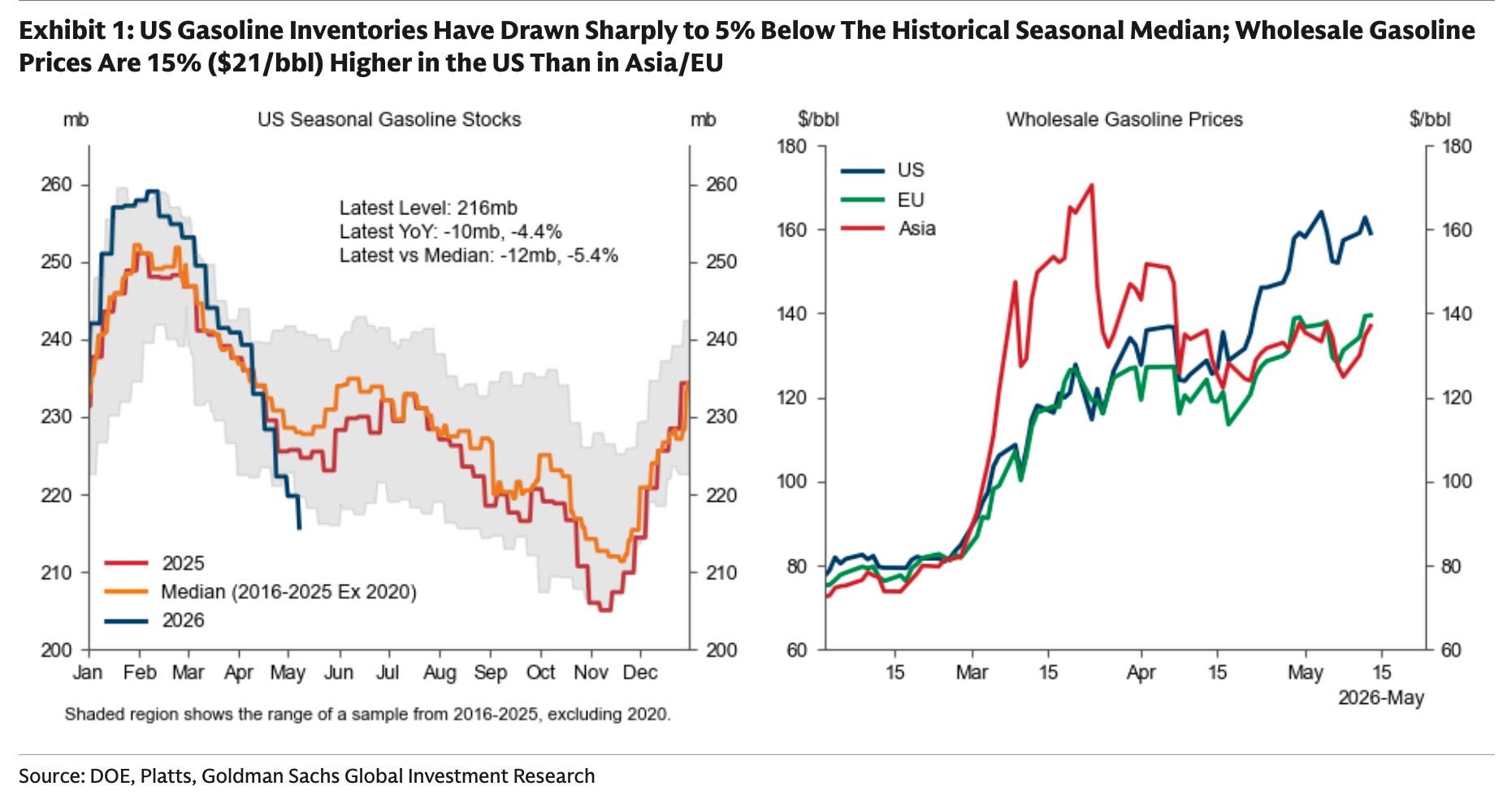

US Gasoline

The US Gasoline Market update from Goldman is interesting. Inventories have drawn at 0.7mb/d since April 1, pulling levels to 5% below the historical seasonal median just as the summer driving season begins. Wholesale gasoline prices in the US are now approximately 15%, or $21 a barrel, higher than in Asia or Europe.

US retail gasoline stands at $4.6 a gallon, just $0.5 below its all-time high, and US retail diesel is at $5.6 a gallon, $0.2 below its own record. Goldman explicitly flags that the probability of US oil export restrictions rises with retail prices, and while that is not their base case, it belongs on the risk radar heading into a summer driving season with Hormuz still under siege.

The UAE’s accelerated West-East pipeline project would eventually add bypass capacity of around 1.5mb/d, but completion is not until 2027.

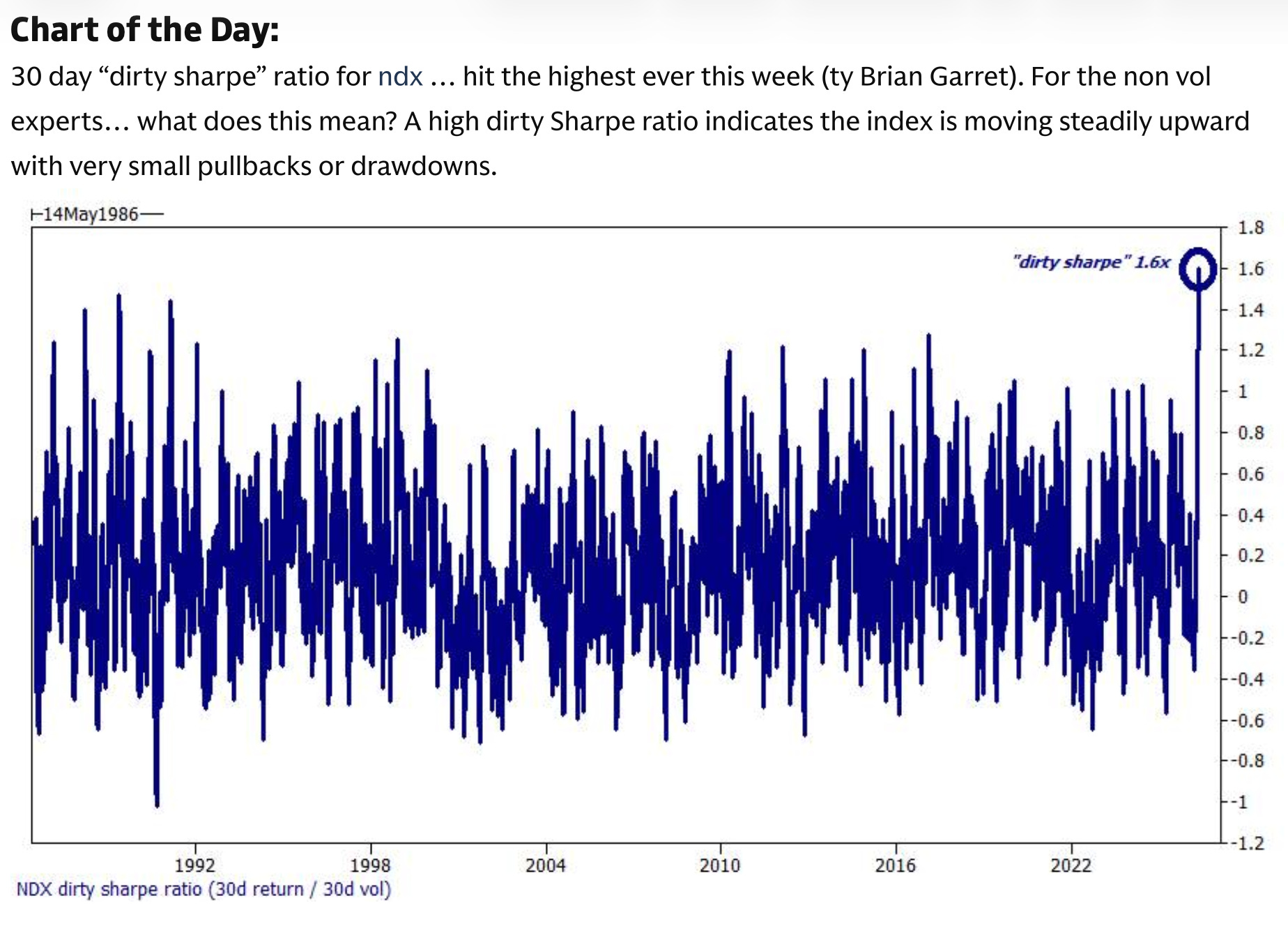

Chart of the Day

The chart is from Goldman’s May 14 mid-day note and shows the NDX 30-day dirty Sharpe ratio since 1986, which hit an all-time high of 1.6x this week. A high dirty Sharpe simply means the index has been grinding steadily higher with almost no pullbacks or drawdowns — the smoothest, most relentless rally in the dataset.

The read for traders is counterintuitive. An extreme reading at this level is not a sign of healthy, broad-based conviction; it is the fingerprint of negative gamma mechanics, forced buying from leveraged ETF rebalancing, and institutional FOMO all converging at once. Nomura estimates a 2% selloff triggers $60.8B of forced delta selling from the combined index options, leveraged ETF, and vol control complex; a 5% move triggers $187B. Today’s OpEx is the first clean window for that process to begin.

Calendars

No earnings of note.

Market Prep

US equity futures are trading down 0.6% to 1.4% ahead of the open, with the Nasdaq 100 underperforming. The session will be shaped by three overlapping forces: the rate shock, weekend Iran risk, and the OpEx mechanics that Nomura has been flagging all week.

Nomura’s McElligott has been the clearest voice on the positioning fragility. Call skew on the SPX and QQQ is at the 100th percentile, while put skew has collapsed to the 0th percentile. This is the structure of a market where almost everyone who missed the rally has been panic-buying upside calls rather than owning the underlying, and the distribution of pain on a reversal is asymmetric.

The leveraged ETF complex sits at $179B of AUM, with roughly 85% concentrated in tech, semis, and Mag7, and generated an estimated $100B of equity buying over the past month from daily rebalancing alone. The same mechanism works brutally in reverse: a 2% down day generates an estimated $60.8B of forced selling; a 3% day generates $97.7B; a 5% day generates $187B.

The VIX is higher today but still below 20, meaning the market has not yet priced a serious escalation scenario, and McElligott’s framing is that the current “Spot Up, Vol Up” dynamic eventually flips to “Spot Down, Vol Up” as a trickle of profit-taking turns self-reinforcing. NVDA earnings on May 20 may provide a brief steadying force heading into next week, but it does not change the mechanics today.

Three things to watch into the close: whether the 10-year yield holds above 4.5% or a flight-to-quality bid pulls it back, whether WTI sustains above $100 or rolls over on any softening in Trump’s Iran rhetoric, and whether the Nasdaq holds the 29,000 area through the expiry window or whether the afternoon delta unwind accelerates the move.

My Take

The Trump-Xi summit was priced for transformation, but delivered a press release. Agricultural purchase commitments and a possible Boeing order are not the structural reset that pushed megacap tech to record highs on Thursday, and with no semiconductor clarity and no Hormuz progress, the single most important overhang for rates and inflation is exactly where it was a week ago.

Something to focus on more than Iran in the near term is the liquidity plumbing. The TGA drawdown from roughly $1.007T to $839B injected over $160B of QE-like reserves into the system in recent weeks, quietly amplifying a rally many attributed to earnings. As Treasury rebuilds the TGA through bill issuance in the weeks ahead, that support reverses mechanically, and the question of whether this rally was genuinely earnings-driven or simply riding Washington’s balance sheet becomes very uncomfortable very fast.

The rates repricing is now the primary risk for equities, with Fed hike pricing moving from 1% probability a month ago to 50% this week, not because the FOMC changed its guidance but because hot CPI, hot PPI, a 4.0% Atlanta Fed Q2 GDP nowcast, and $100 crude are forcing the market’s hand. Hiking into a supply shock is a sequencing that historically ends very badly.

I am heading into the weekend watching the long end and oil closely. Below the paywall, I am adding a new ETF to the Tactical Watchlist.