Breakfast Bites: The $100 breach on Day 10

Crude (Brent & WTI) cross 100; Shut-ins spread, storage fills, and the stagflation clock starts ticking

Rise and shine everyone

Crude Oil blasted past the $100/bbl mark. We’re on Day 10 of the war.

Over the weekend, there were announcements that Iran wouldn’t be attacking any country that doesn’t attack them. This didn’t last long, and by Saturday evening, my friends were reporting multiple shelter alerts in Dubai and Abu Dhabi.

We also had comments from the US administration on not backing down and seeing this oil shock as a temporary spike.

Suffice to say, oil is now pricing in a longer war.

Morning Macro Briefing

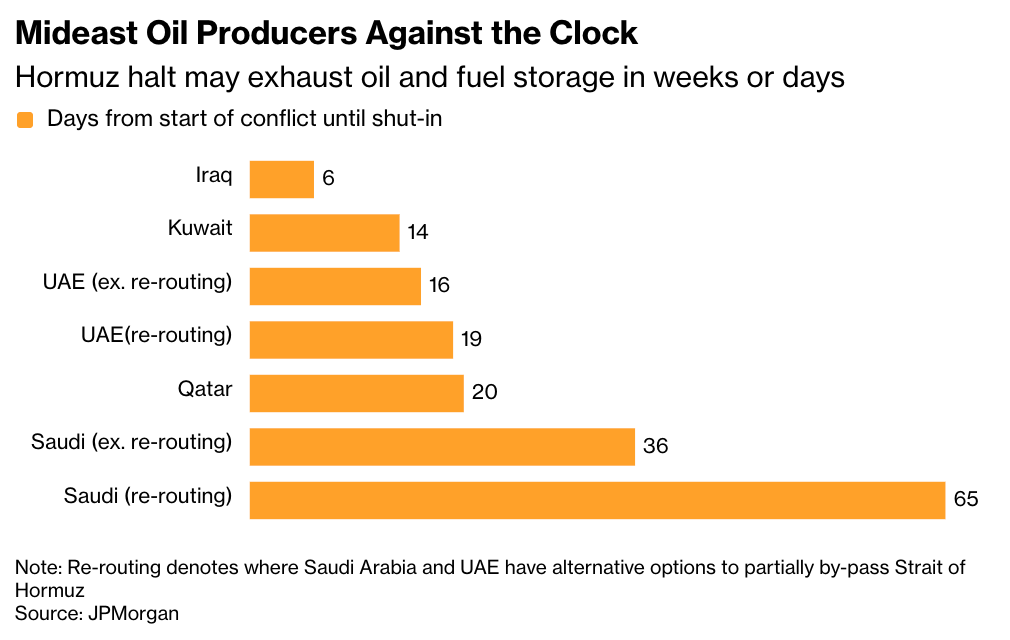

The major issue directly impacting oil was the reduction in production runs (shut-ins) in the Middle East - both Kuwait and Abu Dhabi declared gradually shutting down.

Here’s a summary of where we stand:

Iraq — Rumaila and West Qurna 2 cut by 1.4–1.5mb/d. No pipeline alternatives. Storage at 90% within 3 days. Power blackout compounding the crisis.

Kuwait — Cut started at ~100kb/d, expected to nearly triple. Force majeure declared. All exports go through Hormuz.

UAE — No official volume disclosed. Partially offsetting via 1.5mb/d Fujairah bypass pipeline. Only offshore production is being managed lower, so resuming activities will be easier.

Qatar — LNG fully suspended. Affects ~20% of global LNG supply. Resuming will take 2 week and reaching full capacity another 2 weeks (total 4 weeks).

Saudi Arabia — No production cut yet. Ras Tanura refinery suspended. Diverting crude to Yanbu, but storage pressure building.

The major issue now is the storage capacity. Since the crude oil cannot be moved out of the region, the storage capacities are filling up quickly. Bloomberg has put together some estimates on the runway for shut-ins. We will progressively see cuts in production once we get closer to these numbers.

So there’s definitely the possibility that oil prices could rally further if these cuts start happening.

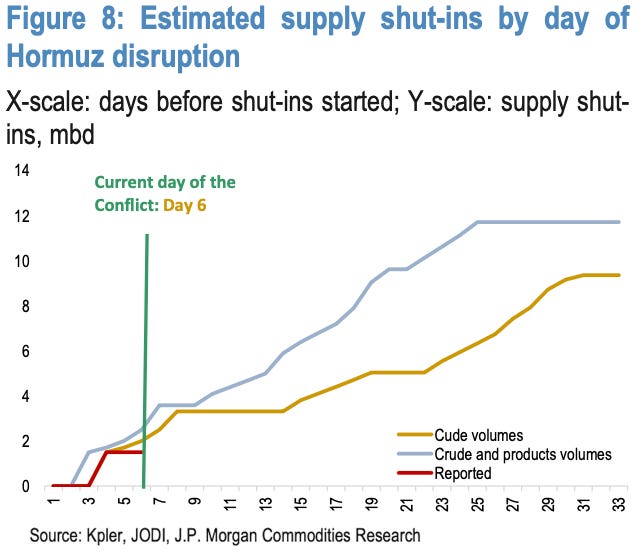

JPM notes that shut-ins will increase progressively by Day 15 (chart below).

Obviously, these are just estimates, but what we need to consider is that should we start hitting those levels of shut-ins, bringing production back online will be a more significant challenge. A relatively short shutdown for crude may be benign. But the longer they remain closed, the more difficult it is to restore. LNG plants require a slow start-up by nature, while refineries take about 2.5 weeks.

And unfortunately, we’re seeing quite a few refineries in Asia starting to shut down and declare force majeure on contracts - meaning they will be unable to meet their supply obligations. This is happening because refineries require a certain level of feedstock to keep running, or else shutting down is a better option.

All these disruptions lead to an inflationary impulse. Gasoline prices in the US have already started to go up. Again, the question will be whether this shock is “transitory”, but once inflation expectations start to go up, we’re likely to see more Central Banks start to take notice. Rate cut bets for the Fed have already been pushed out to September from July.

Friday’s US unemployment report didn’t help. The drop was quite unexpected, but this could be more because of the adjustments made and the recent strikes. But nevertheless, at a time like this, a negative NFP print signifies at least some level of slowdown.

This puts the Fed in a difficult position if inflation starts to ramp up drastically - do they cut because of a slowdown, or hold because of inflation?

Also read The Weekend Edition for Global Impacts ⤵️

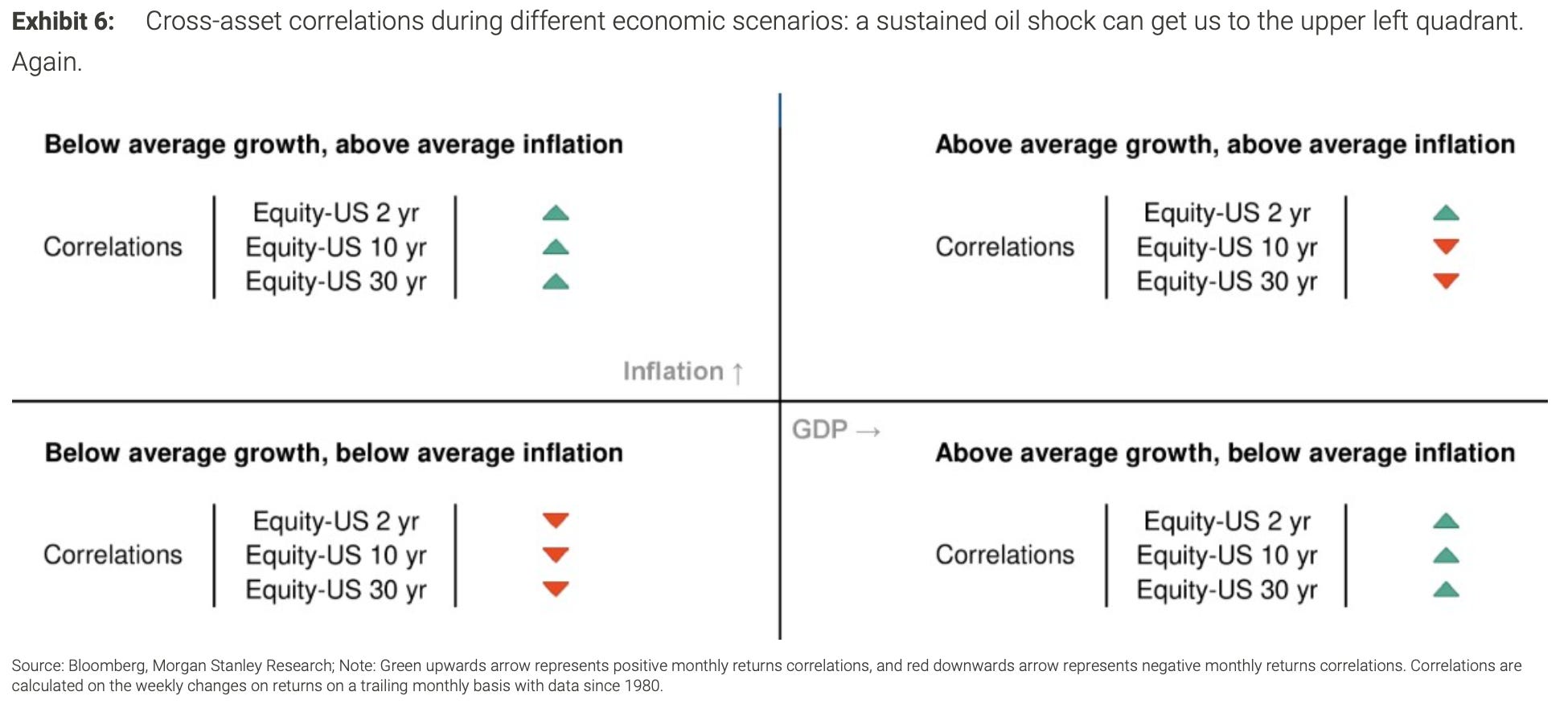

Chart of the Day - X-asset correlation

Great chart on cross-asset correlations. We’ve been talking about the potential for stagflation - lower GDP; higher inflation - shown in the upper left quadrant.

Normally, bonds act as a hedge when stocks fall. But that only works when inflation is falling too, giving central banks room to cut rates and letting bonds rally. In stagflation, the central bank can’t cut rates because inflation is still a problem. So bonds stay under pressure while stocks are also falling.

Both assets lose at the same time. There is no offset, no safe corner to hide in. The entire logic of a balanced portfolio breaks down.

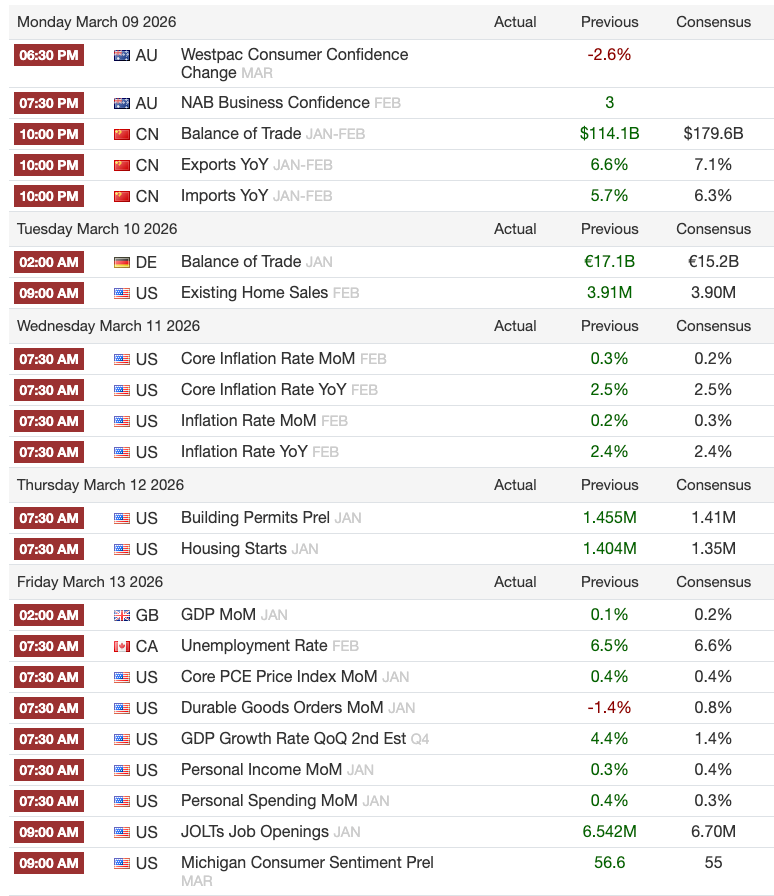

Calendars - The Week Ahead

We get CPI and PCE readouts this week. We also get Prelim UoM sentiment numbers, although the impact of the war would likely not show up.

Market Prep

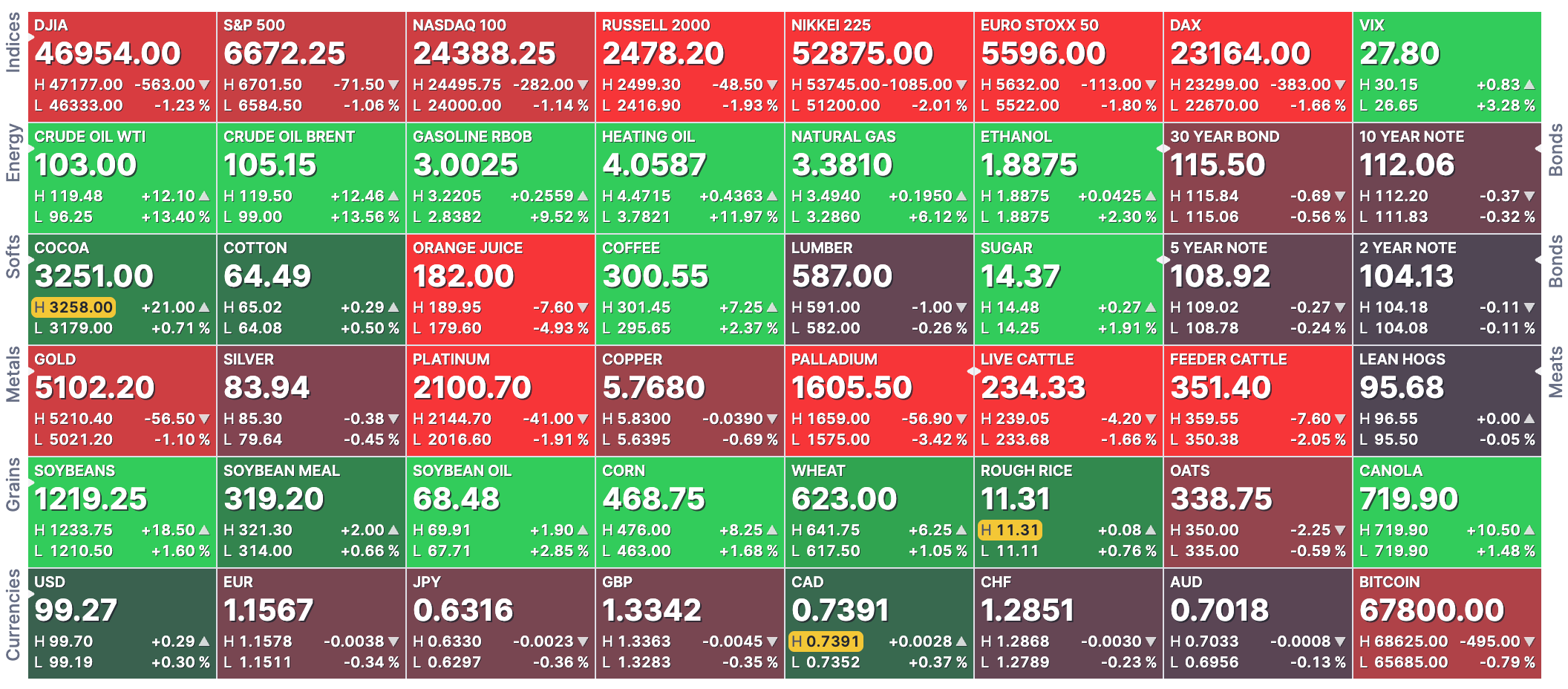

Not surprisingly, markets are red across the board.

As oil spikes drastically, markets have less time to adjust to that shock. Asia took a heavy beating this morning. South Korea triggered the circuit breaker, falling below -8%.

Energy and Equities are not the only assets on the move.

Aluminum prices on the London Metal Exchange hit their highest level since March 2020, reaching $3,544 per metric ton, driven by supply concerns stemming from the US-Israel war against Iran. The Strait of Hormuz disruption accounts for roughly 9% of global aluminum production, with Qatari Qatalum shutting down and Aluminium Bahrain declaring force majeure on shipments.

Gold saw a pullback this morning. Interesting that the metal is seemingly losing its geopolitical premium. One thing to highlight is that there was an article in Bloomberg about gold being sold at a discount because people can’t get it out of the UAE, the second biggest exporter of gold worldwide.

If that’s the case, that’s very stupid. Gold is the one thing that you actually can hold on to, and people want in times of distress. So I’m not sure what people are thinking.

USD is moving in lockstep with oil, understandably. We discussed this - commodities are priced in USD, and it’s pushing the dollar higher.

Let’s look at the oil price movement, though… it spiked and then gave up some of its gains once there was headline news that G7 countries are reportedly considering releasing 400 million barrels of oil.

Note: “Considering”

That’s all it took for a drastic move lower. In fact, I’m yet to find confirmation that there has been a release.

So as long as the Middle East situation persists, we will continue to see significant volatility, so it’s best to be prudent.

My Take

Oil spiked and then gave up much of its gains once there was unconfirmed news on SPR releases.

This tells you how precarious the situation is right now. Headlines are coming in, confirmed or unconfirmed, and prices are making sharp moves. This is not a market to try to catch a trade with any significant volume.

The likelihood that oil goes up further from here is high - I made this case in the Macro Brief above. However, the path it takes from here may not be linear. And given that most asset classes are responding strongly to oil prices, we will see volatility in equities as well.

If there’s been a time to sit on your hands, it’s now!