Breakfast Bites: Tech Trade Loses Its Footing

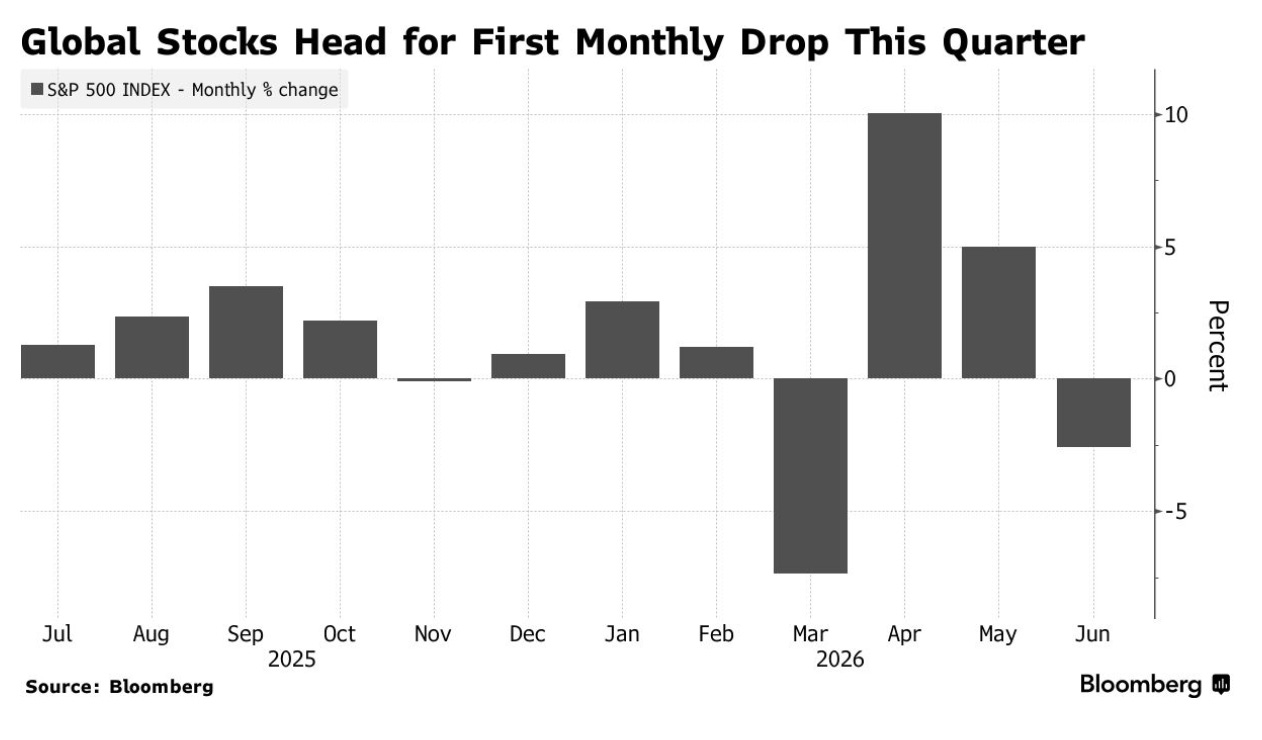

Global equities head for their first monthly decline of the quarter as the AI hardware narrative cracks, oil slides, and macro data offers little cover.

Rise and shine everyone

A quick correction from yesterday’s edition: I attributed Natasha Kaneva’s oil price outlook to Goldman Sachs. She is JPMorgan’s head of global commodities research. Apologies for the error.

Global stocks are heading for their first monthly decline of the quarter, and the unwind is happening fast. The AI trade, which looked nearly unassailable through May, is now cracking from multiple directions at once. Apple’s announcement of 16-24% price hikes tied to memory shortages landed badly, reading less like pricing power and more like a demand headwind for the chip cycle.

The macro backdrop doesn’t offer much of a floor. The final Q1 GDP estimate was revised up 0.5pp to 2.1%, but the quality of that growth matters. Consumer spending was lower. The revision came from a contraction in imports, arithmetic improvement rather than real economic strength. Core PCE printed at 0.32% month-on-month, in line with expectations.

The tech selloff that began on June 3rd now has a self-reinforcing character. Goldman’s desk describes a “circular liquidity trap” in which coordinated selling across Mag7, gold, Bitcoin, and SpaceX has become self-perpetuating. Microsoft is tracking its worst month since December 2000.

Here is what we are watching today:

The AI hardware narrative at its inflection point, with Apple’s memory-cost hikes raising serious questions about the durability of chip demand

Oil’s continued slide and what contango in front Brent spreads is signaling about the physical supply picture

The breadth rotation underway in US equities, as money moves away from mega cap tech and into cyclicals and rate-sensitives

Morning Macro Briefing

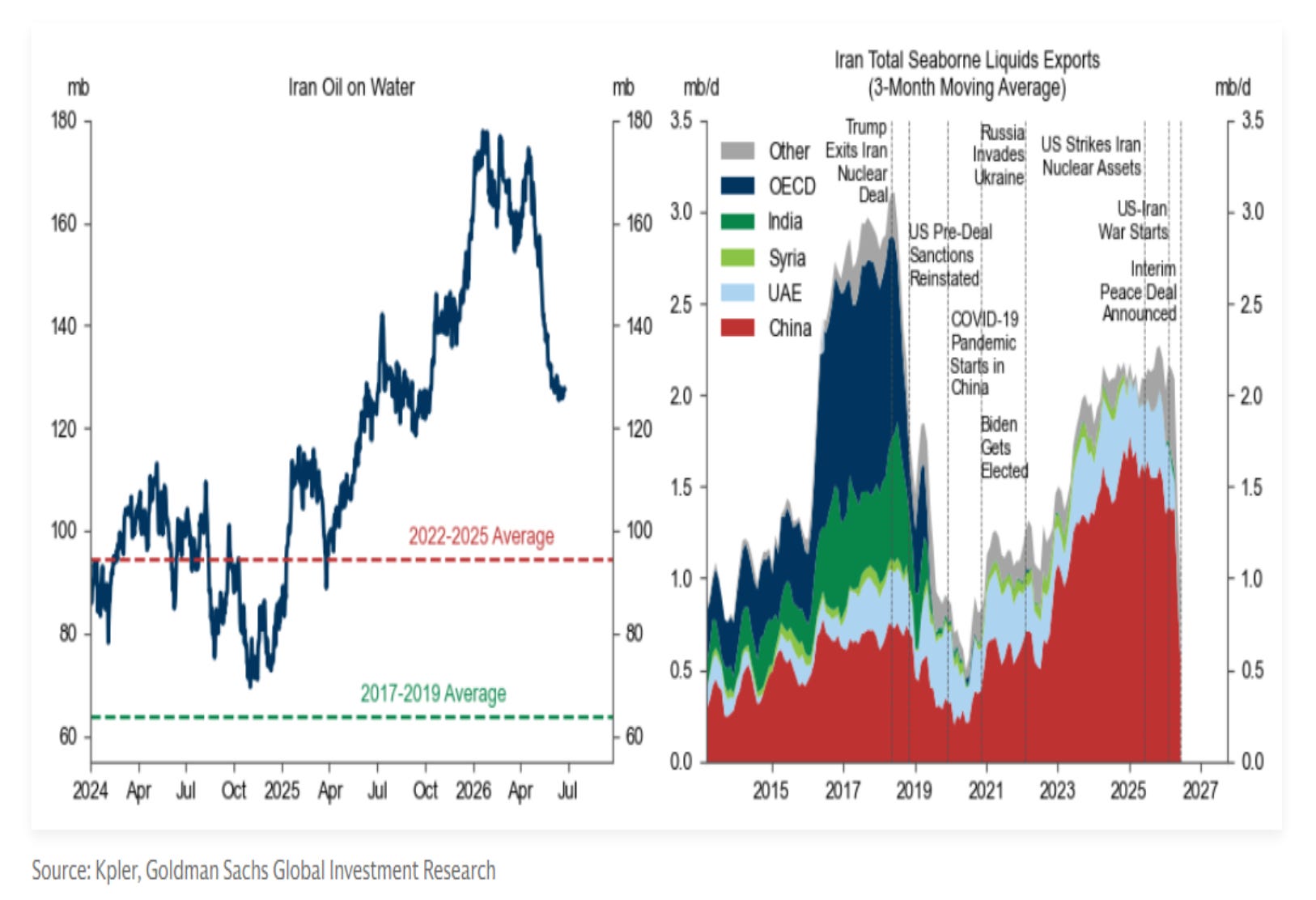

Iran attacked a Singapore-flagged cargo vessel in the Strait of Hormuz on Thursday. South Korean vessels have been exiting the strait, with 8 more confirmed overnight, adding to 5 on Thursday and 2 on Wednesday. Despite all of this, Brent crude is sliding more than 3% to trade below $73 a barrel. Oil is telling us the market does not believe this escalates into a meaningful supply disruption. Iran’s negotiating position only weakens as prices fall.

Ukraine executed its largest drone attack of the war overnight, with Russia claiming to have intercepted 660 drones, hitting the Azov chemical plant in Tula and sparking a fire near the Novomoskovsk power station. Russia is simultaneously dealing with a domestic fuel crisis affecting roughly one in four gas stations, with a diesel export ban now reportedly under consideration.

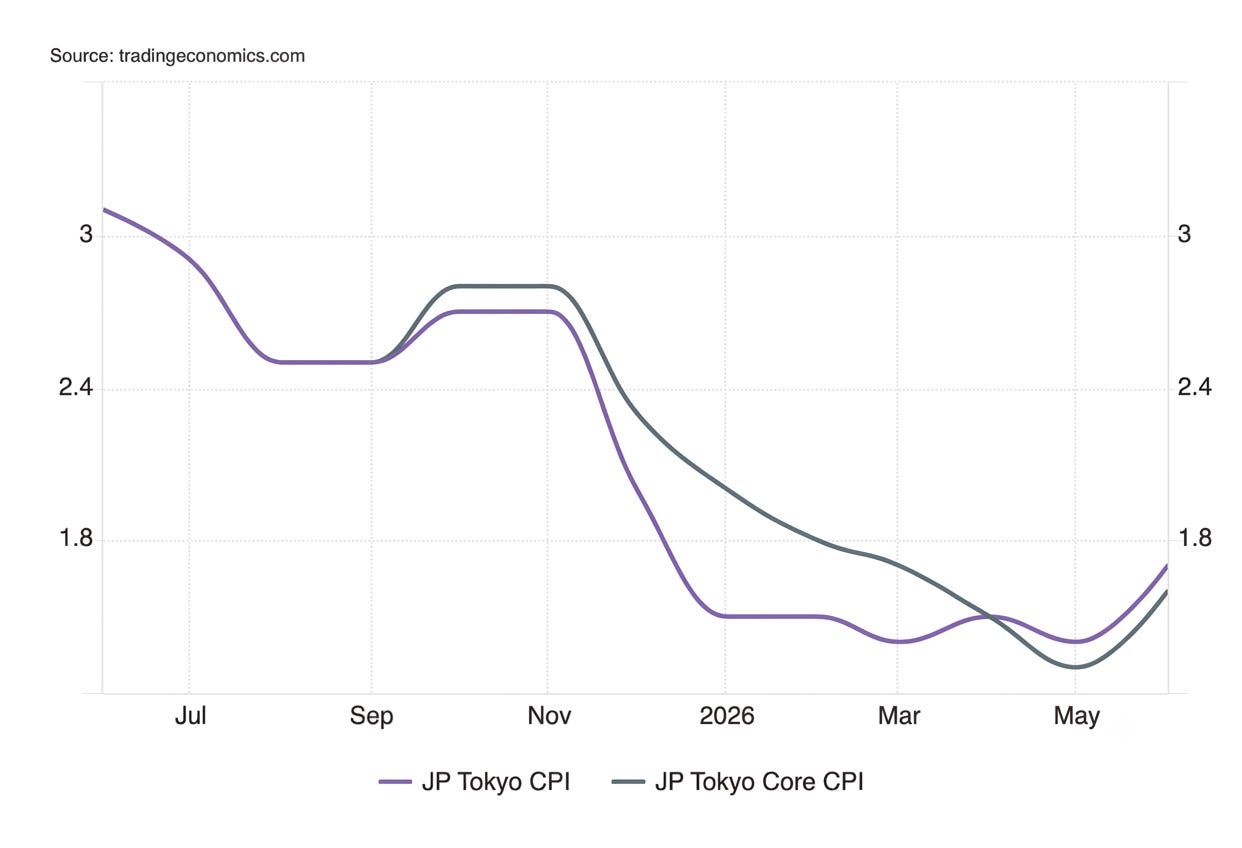

Tokyo’s core-core CPI (excluding fresh food and energy, the series the BOJ watches most closely) rose to 1.9% in May, nearly at target. Headline and core came in at 1.7% and 1.6% respectively, still below target for the fifth consecutive month. The rate hike path is growing more complicated, and not because of the data.

PM Takaichi’s government is moving toward mandating annual bond issuance tied to a new multiyear budget framework, paired with a ¥370T ($2.3T) 14-year investment roadmap covering AI, chips, and energy. Finance Minister Katayama has called it the biggest fiscal reform since World War II. Leaked drafts of the economic blueprint reportedly urge the BOJ to align its decisions with the government’s growth priorities, which is not central bank independence.

ECB consumer inflation expectations cooled at the one-year horizon to 3.5% from an estimated 3.9%, while the three-year ticked slightly higher to 2.9%. Traders are no longer fully pricing in another ECB rate hike. The Bank of England looks set to sit on the sidelines.

Beijing is advancing new legal tools allowing state prosecutors to file civil suits against foreign organizations and individuals deemed to harm China’s interests. The proposed “procuratorial public-interest litigation” law is at its second reading and could pass by year-end. This adds another layer of operational risk for foreign businesses in China, on top of the antiforeign sanctions law from 2021 and subsequent countermeasures regulations.

Trivium China describes it as another tool in Beijing’s growing counter-sanctions legal kit. The American Chamber of Commerce in China, representing more than 800 mainly US companies, says it will be watching implementation closely.

OpenAI and Broadcom unveiled a custom AI inference processor called “Jalapeño” this week, incorporating Broadcom silicon and Celestica rack technology. The message is straightforward: when chip suppliers are taking 75%+ design margins, customers find other paths. Every major hyperscaler and both large model makers are moving toward custom silicon.

AWS is also raising hourly rates on high-end GPU capacity blocks by approximately 20% from July 1st. The power and capacity constraints are feeding through to pricing.

Watch the spenders, not the beneficiaries. Google, Microsoft, and Amazon all traded heavy even on a day when the broader AI supply chain was rallying, and that is where the real signal in this trade sits.

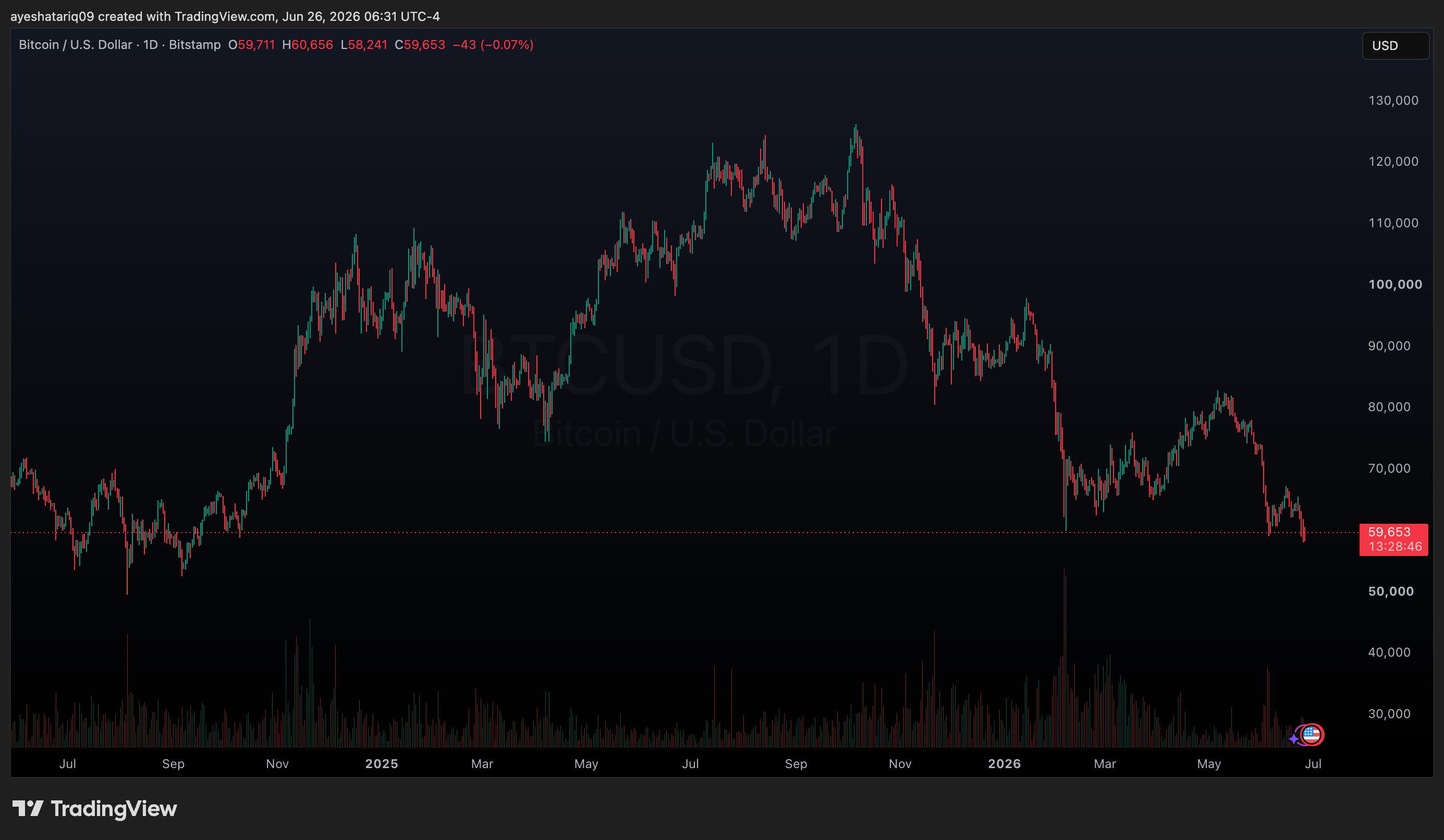

Chart of the Day

Bitcoin is really taking a beating. We’re down to 2024 levels.

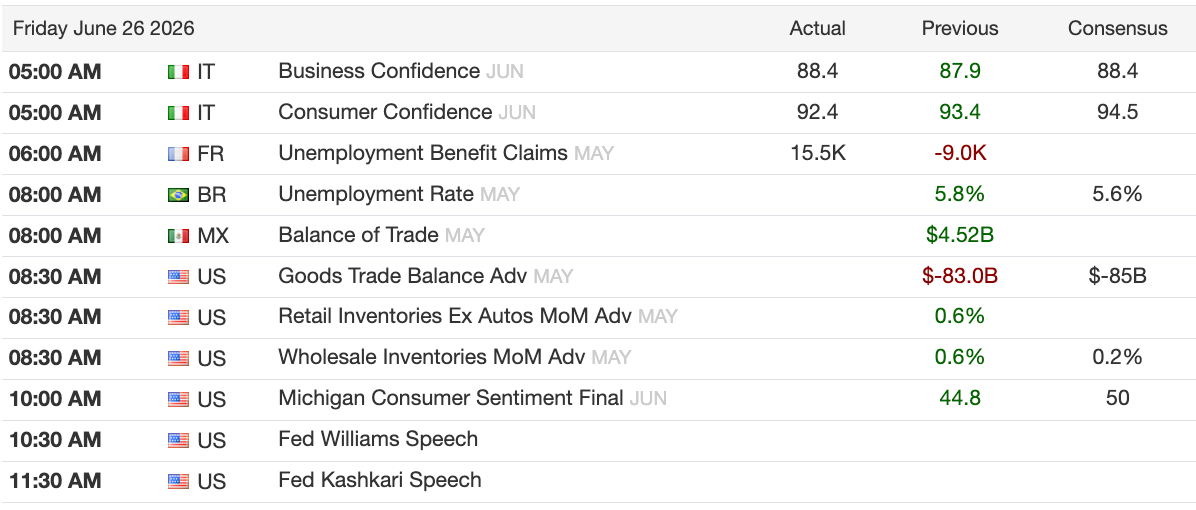

Calendars

Friday closes out a turbulent week. Core PCE and the GDP final revision are already in, so the data slate is light today. Watch for weekend geopolitical developments around the Strait of Hormuz, and watch any Fed commentary following the inflation print.

No earnings of note.

Market Prep

Thursday’s session ended with the S&P 500 near flat at 7,357, Nasdaq 100 up 75bps to 29,440, Russell 2000 up 62bps to 3,005, and the Dow adding 14bps to 51,920. VIX sits at 18.92. Gold closed at $4,027 and WTI at $72.08.

Those numbers mask a chaotic session. Micron’s blowout print sent Nasdaq futures up 2% overnight before the cash open erased the entire move in under 30 minutes. US equity futures then made fresh weekly lows during Asian trading, with the Kospi down as much as 8% and the Nikkei off 4.5%.

OpenAI is reportedly considering pushing its IPO to 2027. Bankers cited the tech stock volatility and waning retail appetite following SpaceX’s post-IPO drop, from above $225 to around $153, as the driver. Sam Altman is not willing to accept a lower valuation for an earlier listing, and SoftBank, which holds roughly $65bn in OpenAI, fell 13% on the news.

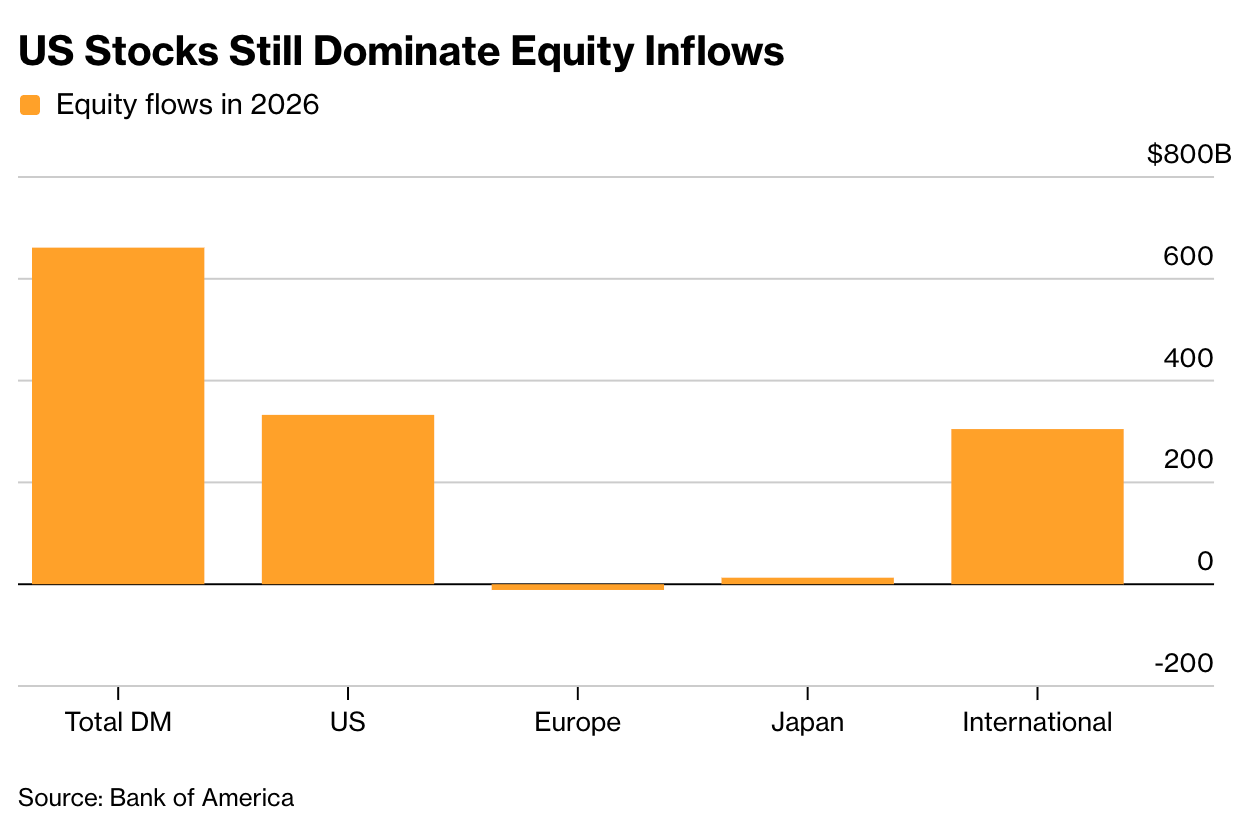

BofA’s EPFR data through June 24 shows US equity funds shed $8.5bn for the week, the first outflow in three months, with tech funds registering a record $9.3bn in withdrawals. That followed an unprecedented $19.2bn inflow to tech the prior week. That reversal in a single week is positioning stress, not noise.

The Kospi hit a record above 9,000 on Monday, triggered two circuit breakers in the same week, and ended sharply lower. Samsung and SK Hynix together make up nearly 60% of the index weighting.

Societe Generale’s Rajat Agarwal notes that leveraged ETFs are capturing as much as 60% of total turnover on large down days, creating a self-reinforcing loop between flows and returns. Retail investors bought more than $5bn in Kospi shares on Friday alone, on margin.

Friday opens with Nasdaq 100 futures down 1.1% and S&P 500 futures off 0.5%. The dollar is broadly firm, supported by Warsh’s price stability commitment. Brent is lower by more than 3%, trading below $73.

Into the weekend, watch whether the broadening rotation holds, how the Strait of Hormuz situation develops, and where the hyperscalers close. Goldman is right that the spenders are the signal. Everything else in the AI trade is downstream of that answer.