Breakfast Bites: Strong Data, Dangerous Backdrop

Q1 GDP holds at 2% on AI investment, PCE hits a three-year high, and the blockade shows no sign of breaking

Rise and shine everyone.

It is May 1st, May Day, and most of Europe is closed for the holiday while the rest of the world watches a Strait that will not reopen on its own. Trump called the blockade “incredible” on Thursday, told reporters Iran’s economy is crashing, and promised gas prices would drop “like a rock” once the war ends. Iran’s new supreme leader vowed to keep control of Hormuz and refused to yield on nuclear or missile technologies.

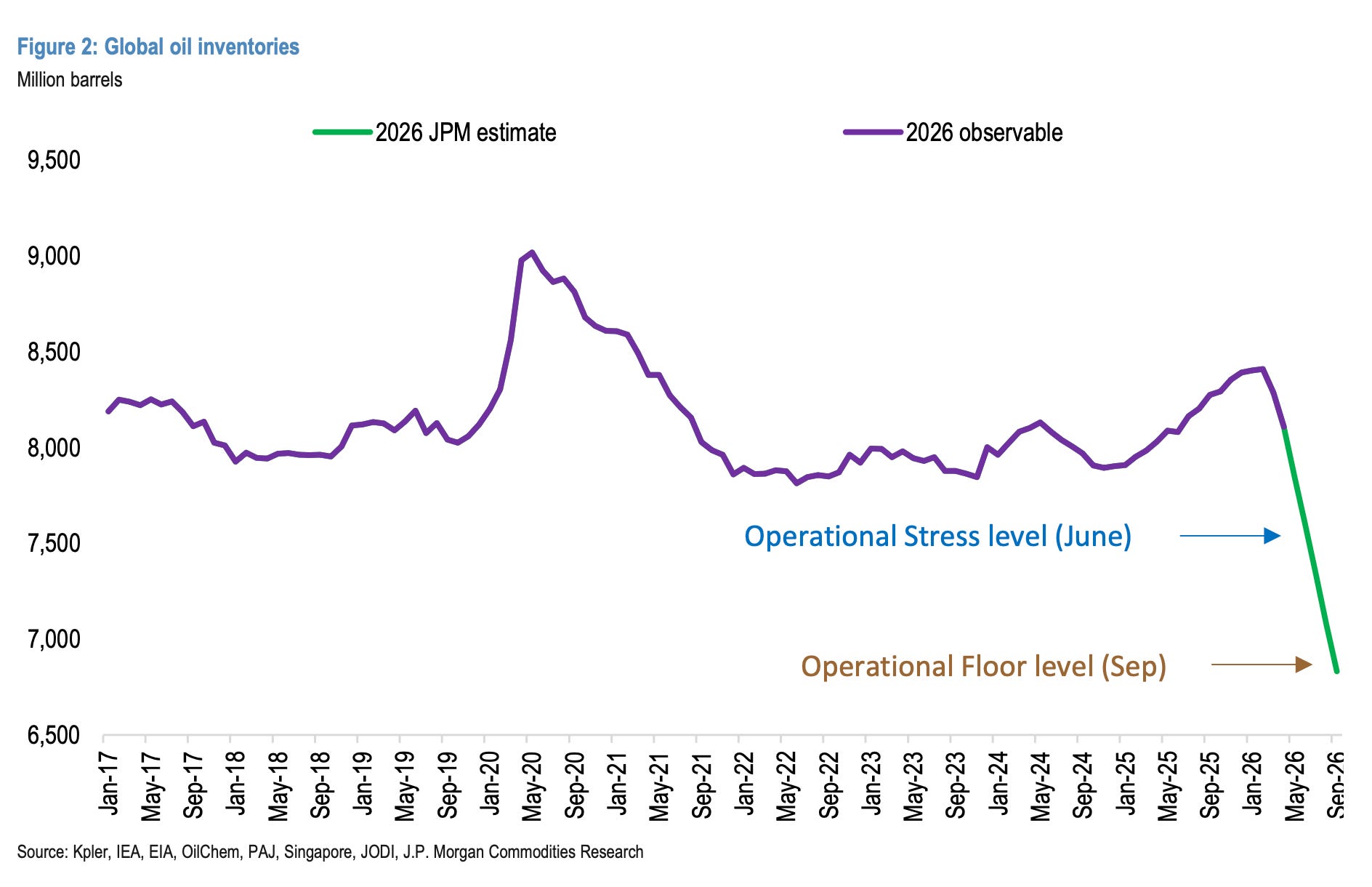

JPM’s commodities team published the most important analytical piece of the week: of 8.4 billion barrels in global storage, only 0.8 billion are realistically drawable without pushing the system into operational stress. OECD commercial inventories are on track to hit that threshold by June. JPM calls it the illusion of plenty, and it is exactly the right phrase.

Beneath the war, two things happened overnight that the market will be digesting. Apple beat after the bell with strong iPhone and China sales and announced a buyback, and a bipartisan US delegation led by Trump ally Senator Steve Daines landed in Beijing to begin laying groundwork for a mid-May Trump-Xi summit. The AI capex machine kept printing, oil held in triple digits, and the yen bounced after Japan’s first intervention since 2024.

Morning Macro Briefing

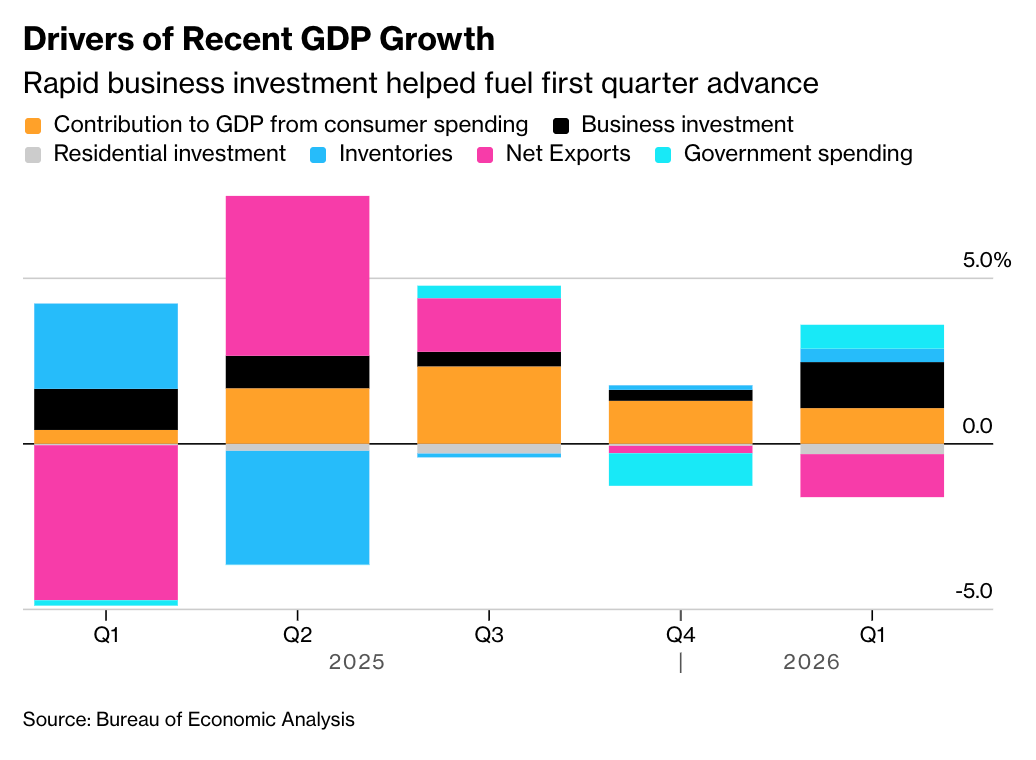

US Q1 GDP came in at 2.0% annualized, missing the 2.3% consensus. Business investment in equipment and structures surged 10.4%, the fastest in nearly three years, almost entirely AI-driven, while consumer spending beat at 1.6% against 1.4% expected. Net exports subtracted 1.3 percentage points from the headline, largely from a surge in computer equipment imports, and the cleaner final sales to private domestic purchasers metric grew 2.5%.

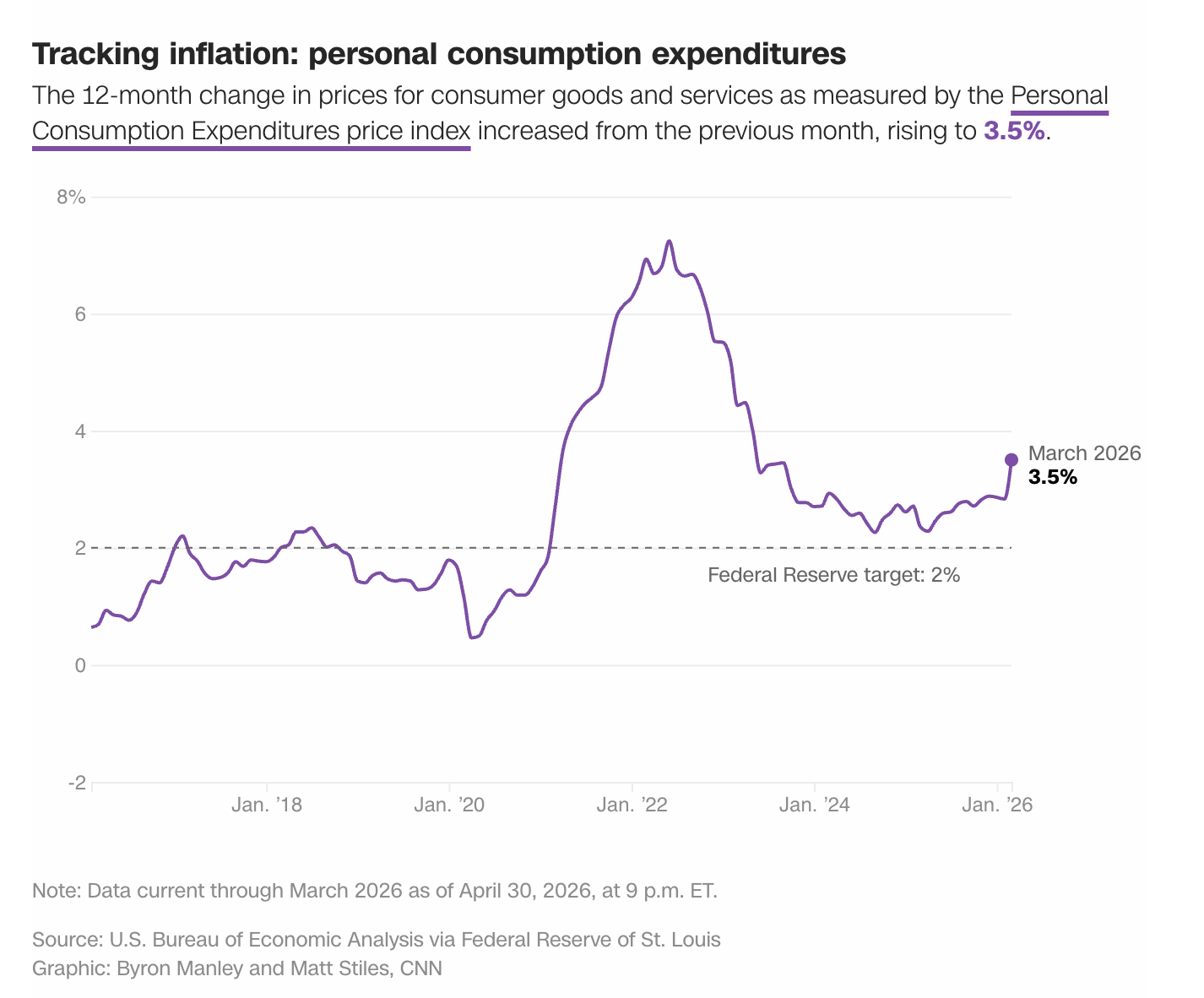

March PCE rose 0.7% month-on-month, pushing the annual rate to 3.5% from 2.8% in February, the highest since May 2023. Core PCE came in at 0.3% month-on-month and 3.2% year-on-year, up from 3.0% and the highest in more than two years. US average gasoline hit a four-year high of $4.30 per gallon on Thursday per AAA.

Real disposable income fell 0.1% in March, the second consecutive monthly decline, and the personal saving rate dropped to 3.6%, a four-year low. The economy entered the war in solid shape, AI investment is carrying the growth story, but this is exactly why the Fed cannot cut.

Powell’s tenure as Fed chair ends May 15, and his seat on the Board of Governors runs to 2028. He said Wednesday he intends to serve as governor for a period to be determined. Trump on Thursday said he doesn’t care, calling Powell “a negative force” and suggesting nobody would want to hire him.

The ECB held its deposit rate at 2.0% Thursday, but the press conference was anything but quiet. Lagarde acknowledged the Governing Council had discussed a rate hike “at length and in depth” before unanimously rejecting it. Subsequent sources reinforced expectations that a June rate increase remains likely, with some analysts arguing one or two precautionary hikes could help anchor inflation expectations.

Eurozone Q1 GDP came in at 0.1% quarter-on-quarter, missing the 0.2% consensus. Strip out the volatile Irish GDP component and growth was 0.24%. April inflation rose from 2.6% to 3.0% year-on-year, though the monthly pace slowed to 1.0% from 1.3% in March.

The probability of a June hike rising materially if Hormuz remains shut through May. April PMI data suggest firms are increasingly passing higher input costs to customers, which is the second-round effect the ECB is most focused on. Goldman now formally expects two 25bp ECB hikes this year, in June and September, taking the deposit rate to a peak of 2.5%.

The Bank of England voted 8-1 to hold Bank Rate at 3.75%, with Pill dissenting in favour of a 25bp hike. Bailey described the decision as an “active hold,” with the MPR presenting three scenarios depending on the energy price path and the extent of second-round effects. The bar for further hikes may be higher than the ECB’s, given labor market weakness and soft demand.

Japan’s Ministry of Finance intervened in the yen market Thursday for the first time since 2024, later confirming the action to Nikkei. The sequence was deliberate: Finance Minister Katayama delivered the first warning volley, and top FX diplomat Mimura followed just 40 minutes later with a repeat. USD/JPY promptly gained five big figures to 155 from above 160.

The yen was trading around 157 Friday morning in Tokyo. Mimura declined to comment on whether further action was coming but warned that “we are just at the beginning of a long holiday period” — Japan observes Golden Week from May 4-6, and in 2024 the MoF intervened multiple times during the same break. Analysts note the impact may be limited without a narrowing of the rate differential, which requires either Fed cuts or BOJ hikes, and neither is imminent.

The BOJ confirmed it will maintain bond purchases at the same amounts in May as in April. Tokyo April CPI was surprisingly soft: Core came in at the slowest pace in four years, and Core-Core, which strips both food and energy, fell below 2% for the first time since February 2025. The US press attributed the softness to fuel subsidies offsetting higher raw material costs, which masks rather than resolves the underlying energy passthrough.

Chart of the Day

JP Morgan’s “The Illusion of Plenty” report warns that global oil markets are nearing a breaking point. While total inventories sit at 8.4 billion barrels, the accessible buffer is only 0.8 billion.

Key Takeaways

The Deadline: At the current OECD draw rate of 2.2 million b/d, the system hits operational stress by June 2026.

The Floor: Current trajectories suggest inventories will hit the “September line”—the level at which the global supply chain effectively ceases to function.

The Catalyst: With the final Hormuz cargo having arrived on April 20, the exhaustion of floating stocks shifts the entire supply burden to onshore commercial inventories.

The inventory math is what makes this conflict structurally different from every energy shock of the past decade. JPM’s team breaks global inventories into layers, with each layer progressively harder to access and more expensive to draw. Floating commercial stock has already drawn 140 million barrels over two months; with the last Hormuz cargo in, that draw rate now moderates.

OECD commercial onshore inventories started drawing at 2.2 million barrels per day in April after a much smaller 0.45 million barrel per day draw in March. Strategic Petroleum Reserve releases are running at 2.5 million barrels per day across the US, Japan, and South Korea. Observed global demand has already fallen 2.8 million barrels per day in March and 4.3 million barrels per day in April.

Demand destruction needs to scale to 5.5 million barrels per day in May to prevent the system from hitting June stress thresholds. That is not voluntary conservation; it is price rationing, where costs are high enough to force reduced consumption across transportation, aviation, and industry. The feedback loop between falling inventories and higher prices is not yet fully reflected in the market.

Goldman pushed its assumed normalization date for Persian Gulf exports from mid-May to end-June and expects production to recover more slowly than previously modeled. European jet fuel inventories are forecast to hit the IEA’s critical 23-day shortage threshold by end-May and breach it in June. Goldman’s equity analysts note chemical prices have risen twice as fast and twice as much as during the 2022 European energy crisis.

Market Prep

US equity futures are flat to marginally positive, trading in a narrow range. Most of Europe is closed for May Day, with Germany, France, Italy, and Spain all off, leaving the UK, Denmark, and the US as the primary active markets. FTSE 100 is down 0.8%, KOSPI fell 1.4%, and Asian markets closed mixed.Brent is up to around $111/bbl and WTI is up to $105/bbl.

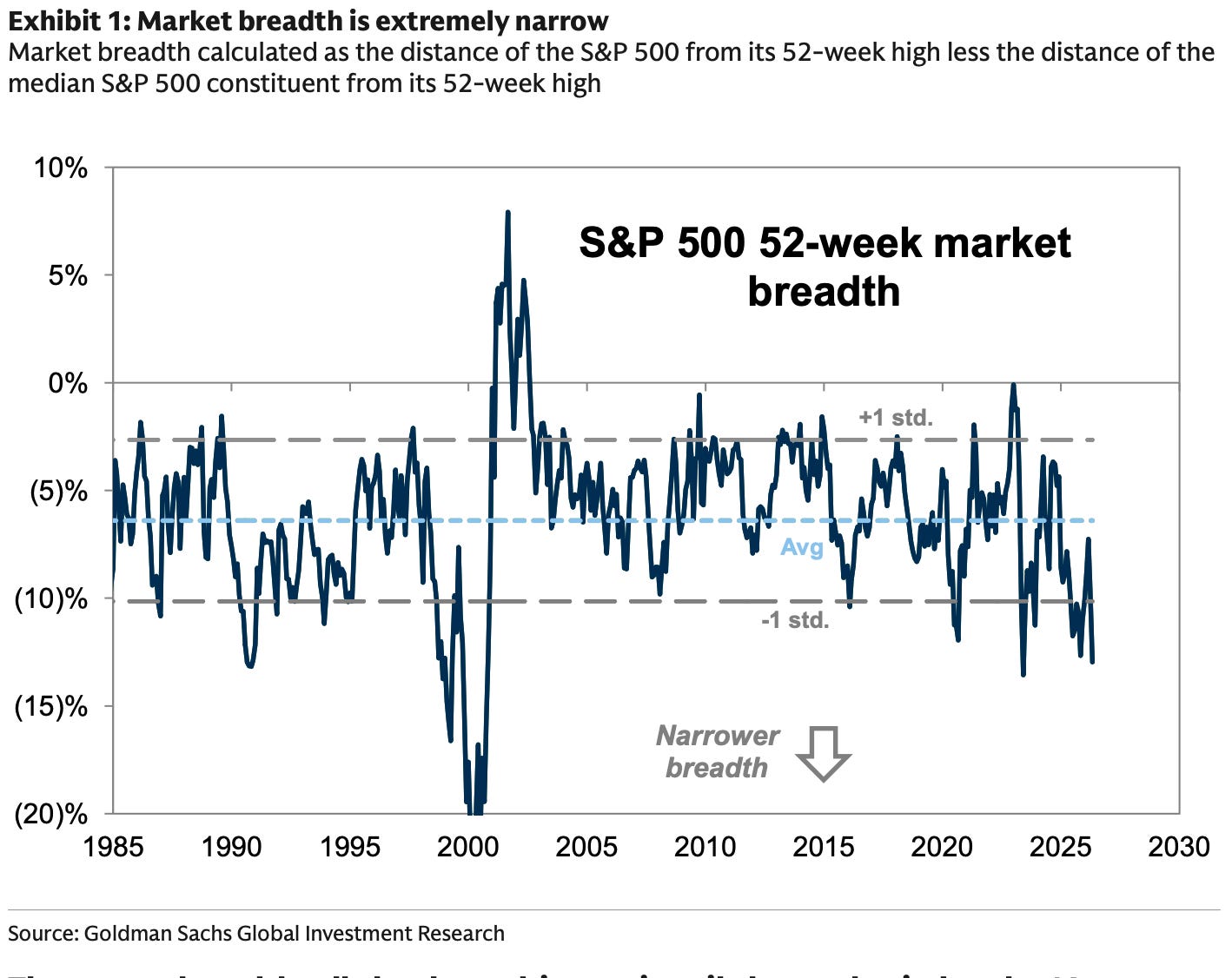

Goldman’s desk estimates approximately $27 billion in US equity selling from end-of-month pension rebalancing, ranking in the 86th percentile by absolute dollar value over the past three years. Combined with thin holiday-related European liquidity, that flow is the dominant technical factor today. The record high in the S&P 500 is a headline, but the median constituent sits 13% below its own 52-week high and Goldman’s preferred breadth measure is at its narrowest since the Dot-Com Bubble.

The Momentum factor has surged 25% YTD but the drawdown risk is structurally elevated. Goldman PB data shows hedge fund net tilt to Momentum near multi-year highs and gross leverage at the upper end of the 5-year range for both the overall universe and fundamental equity long/short funds. Sharp narrowing of breadth has historically preceded larger-than-average S&P 500 drawdowns in the subsequent 6-12 months.

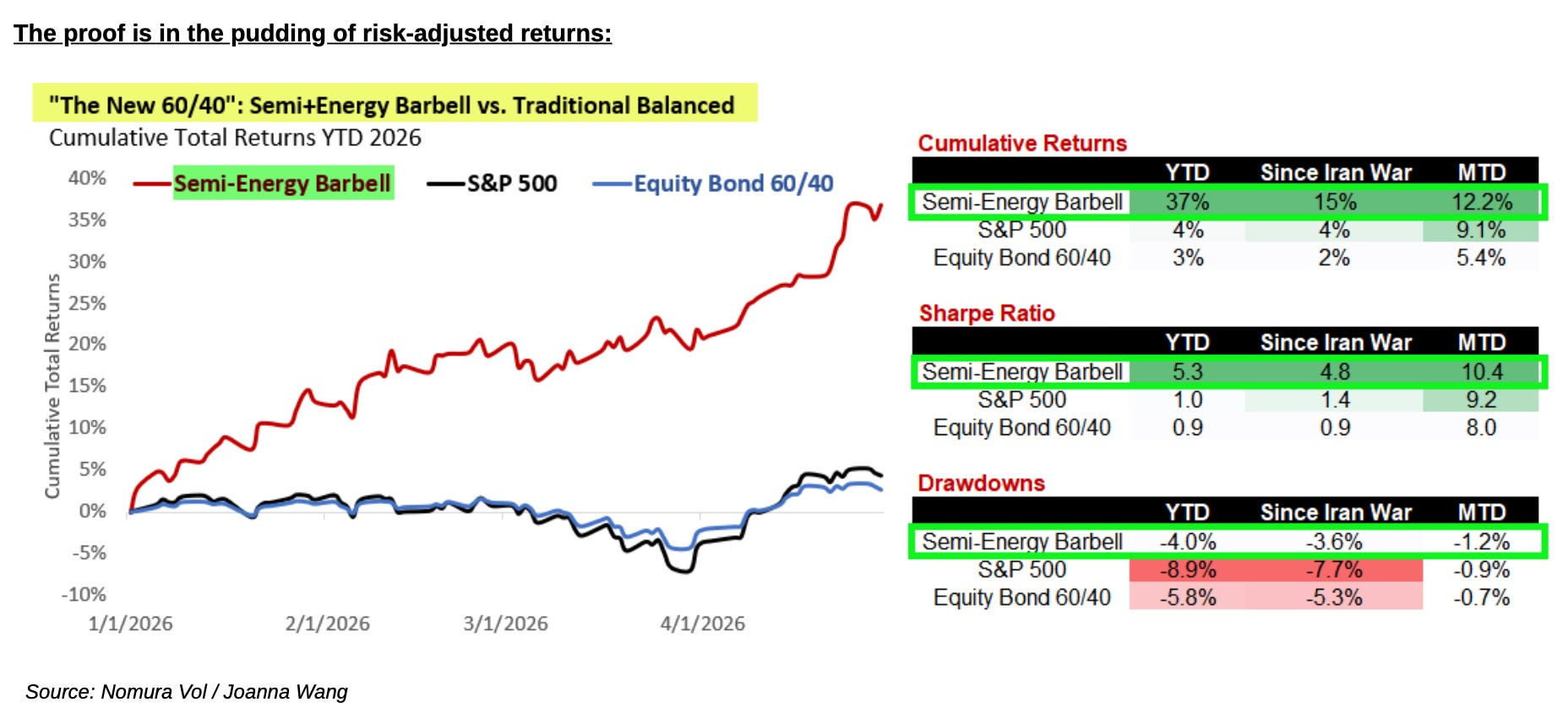

Nomura’s Charlie McElligott frames the positioning problem clearly: the market has been acting like it is short the “New 60/40,” the 50/50 semis-energy barbell. The same funds underweight Mag7 are also underweight energy, and both Energy and Tech are the top EPS revision sectors YTD at 40% and 22% respectively. McElligott hedges the barbell with the VIX call wing and SPX put wing.

On earnings, Apple beat on revenue and EPS after the bell, announced a buyback, and posted strong iPhone and China sales numbers, with the stock up 1.9% in after-hours. Caterpillar reported a massive beat with shares up 10%, and Tokyo Electron rose 7% on earnings and a positive outlook. Mastercard beat on revenue at $8.4 billion versus $8.25 billion consensus, with adjusted EPS of $4.60 versus $4.40, but traded lower on cross-border disappointment and flat guidance. Anthropic is reportedly pushing investors to submit allocations within 48 hours for a new funding round expected to close in roughly two weeks, which could significantly boost its valuation relative to OpenAI’s reported $852 billion post-money raise.

My Take

The war is the dominant variable and the JPM inventory piece is a good one: June is the operational stress date, and Goldman has already pushed its normalization assumption to end-June with risks skewed further out.

The “New 60/40” from Nomura remains the best structural frame for this regime: semis and energy, whoever controls compute and molecules wins, and the funds that missed both are still chasing.

Momentum volatility will continue until the breadth problem resolves, and Goldman’s PB positioning data suggests the risk is a catch-down in leaders rather than a catch-up from laggards.

On the data front, watch the double PMI print - the US April S&P and ISM Manufacturing figures release within 15 minutes of each other tonight, and any divergence between them will generate noise. The new orders sub-components and the prices paid readings are what matter, given the current inflation picture.