Breakfast Bites: Ships Move, Hawks Stir

Oil flows through Hormuz, FOMC minutes turn hawkish, and SpaceX files for the biggest IPO in history.

Rise and shine everyone

I think the SpaceX IPO filing dulled some of Nvidia’s shine. But at least we didn’t see the market crash and burn on bad earnings. As expected, NVDA delivered a double beat, but the guide fell a bit short of Street whisper numbers.

The first take on the SpaceX IPO is not great either - the company is losing -$4.8B while seeking a $2T valuation. I haven’t had a chance to read the whole S-1, so keeping an open mind as to what I find.

Oh, and OpenAI also announced filing their IPO as soon as September, eyeing a $1T valuation.

The good news is that oil is moving through the Strait of Hormuz, WTI has broken back below $100, and markets ran hard on it yesterday. Trump confirmed the US is in the final stages of talks with Iran, Brent fell nearly 6%, and the reopening trade took airlines, homebuilders, and retailers all higher by more than one standard deviation.

JPM’s energy desk also flagged an unusual options position: a buyer stands to collect $129 million if July Brent futures fall roughly 19% by May 26th expiration.

But the FOMC published minutes showing a committee that is quietly but meaningfully shifting its posture on inflation. The two stories pull in opposite directions, and this morning we have the data to determine the path - PMIs and earnings from WMT.

Today we’re watching:

US flash PMIs at 9:45 am ET, the most important data print of the week

Walmart and Ross earnings before the open, the cleanest consumer reads left this season

European flash PMIs from 3:15 am ET, which will set the early tone for rates

And finally, the ETF we added yesterday saw a nice rally.

Morning Macro Briefing

Yesterday’s FOMC minutes were the most hawkish read from this committee in several meetings. A majority of participants said policy firming would likely become appropriate if inflation continued to run persistently above 2%. That is a significant shift. Prior minutes framed hikes as a tail risk; now they are the stated response function to a persistent miss.

The shift on cuts is equally pointed. Where prior minutes had “many” participants focused on eventual easing, now “several” want cuts only after clear signs disinflation is firmly back on track. Last time, the concern was an absence of further deceleration; this time, participants flagged outright acceleration, with core moving further above 2%. New additions included several members noting AI investment could raise input costs near-term, and recognition that commodity prices may stay elevated even after the conflict resolves. Warsh takes the chair at exactly the moment the committee’s patience is running out.

Korea’s April PPI hit 6.9% year-on-year against 4.1% prior, the fastest pace in 28 years, and semiconductor exports for the first 20 days of May reached a record $52.7 billion, up 202% year-on-year.

Australia’s April jobs report was poor enough to move rates. The unemployment rate jumped, sending three-year yields down 13bps. NAB shifted its RBA cut call out to August. Australian duration is worth watching on the short side if the data stabilises from here.

Indonesia’s central bank hiked 50bps overnight, 25bps more than expected, citing the need to stabilise the rupiah amid global volatility. The Jakarta bourse fell 2%. Indonesia joins a growing list of EM central banks effectively importing tighter policy from the Middle East shock, forced to defend currencies even as the domestic cycle does not demand it.

Taiwan’s export orders extended their run in April, up 48%, again beating expectations. The more sensitive item is the Pentagon reportedly expressing doubts over the approved $14 billion arms deal with Taiwan, with Taipei’s response conspicuously vague. Any signal that the US is softening security commitments to Taiwan carries implications well beyond the defence budget.

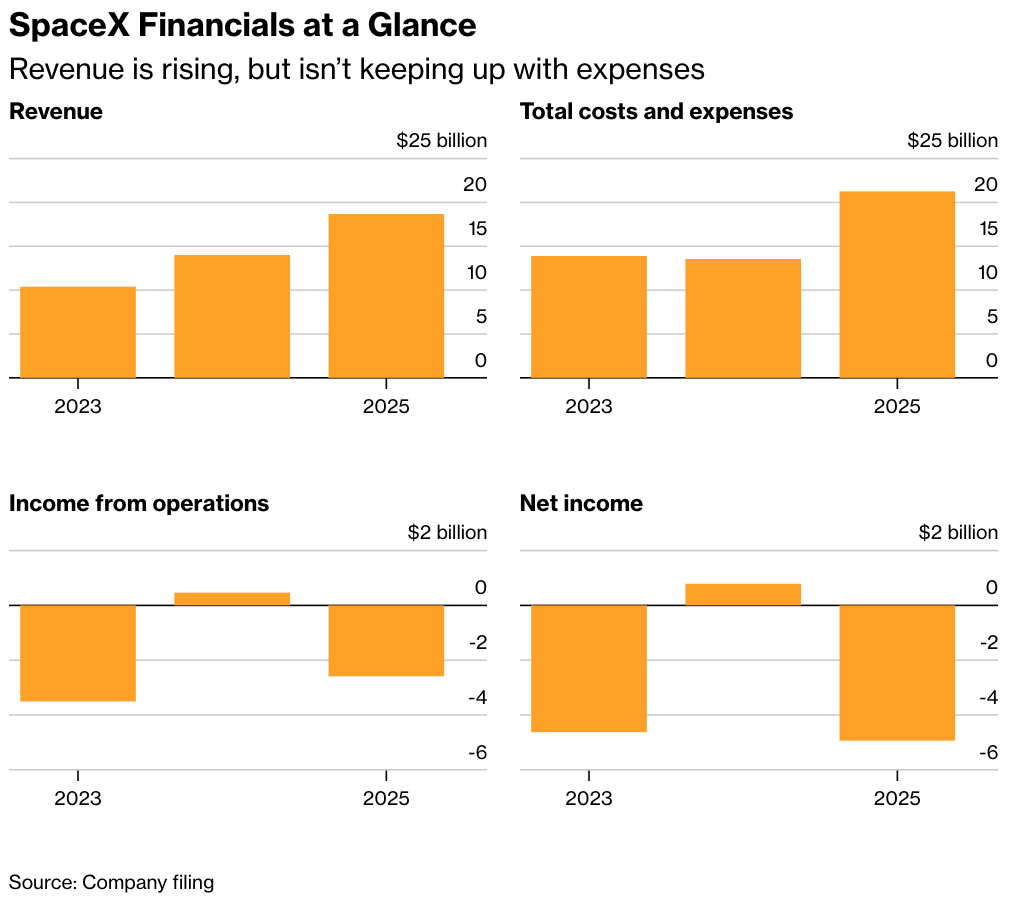

Chart of the Day

SpaceX filed its IPO prospectus targeting a $2 trillion valuation, which would be the largest public market debut in history.

The headline numbers: $18.7 billion in 2025 revenue, growing roughly a third annually, Starlink generating $3.26 billion in Q1 alone, with 10.3 million subscribers across 164 countries. Against that: a $4.94 billion net loss, capex nearly doubled to $20.7 billion, and $29 billion in debt, largely from the xAI acquisition. The filing frames the total addressable market at $28.5 trillion, the vast majority from AI rather than space. Musk controls 85.1% of voting power.

Market Prep

US equities closed well yesterday. SPX +1.1%, NDX +1.7%, RTY +2.6%. WTI settled at $98.26, down nearly 6% on the session. The 10-year closed at 4.586%, gold at $4,544, VIX at 17.44.

Nvidia posted Q1 revenue of $82 billion, up 85% year-on-year, with data centre at $75 billion and networking nearly tripling. Free cash flow hit a record $49 billion, the dividend was raised to $0.25 per share, and $80 billion in new buybacks were authorised. The stock was down about 1.3% after hours, which tells you more about positioning than the print: up 35% from its March low, there was simply not much left for a beat to unlock.

Jensen guided Q2 at $91 billion and endorsed the capex supercycle: “Compute is revenues. Compute is profit.” The most significant new disclosure was Anthropic added as a strategic compute partner, taking Nvidia’s share of frontier AI inference from near zero to substantial almost overnight. The one overhang is China: no data centre compute revenue is included in the Q2 guide, with H200 export licences still unresolved.

Asian equities recovered sharply overnight, catching up to yesterday’s Hormuz relief. The Kospi surged 8%, with Hynix up 11% and Samsung up 7%, after Samsung and its union signed a tentative pay deal calling off today’s planned strike. A shareholder group has since said it will seek an injunction if the deal is approved, so this is not closed.

Goldman’s prime book shows HFs were net buyers on the session, concentrated in Consumer Discretionary, Industrials, and Materials, but selling Tech and Energy. LOs were net sellers across Healthcare, Staples, and Tech. Top of book liquidity is down 38% versus the 20-day average, meaning moves can amplify quickly.

The short base in macro products is enormous, and if this morning’s PMIs come in firm or Hormuz progress accelerates, a CTA-driven squeeze in index shorts is the path of least resistance higher. JPM’s energy desk also flagged an unusual options position: a buyer stands to collect $129 million if July Brent futures fall roughly 19% by May 26th expiration. Traders are on high alert for unusual flows.