Breakfast Bites: Ships Down, Talks Stalled

Ceasefire extended but two vessels attacked in the Strait, Vance’s trip shelved, and markets waiting for clarity that is not coming; Copper may move higher; New Energy Capex Cycle

Rise and shine everyone.

The ceasefire did not expire cleanly. Trump extended it at Pakistan’s request, citing deep fractures within Tehran’s leadership, while keeping the naval blockade firmly in place. The Vance trip to Islamabad was first paused, then delayed indefinitely, with Iranian officials confirming they would not attend the talks.

Two cargo vessels were attacked in the Strait of Hormuz in the early hours of Wednesday, the Epaminondas and the MSC Francesca, both now stopped in the water. Markets are in a holding pattern, with the Stoxx Europe 600 up 0.3%, US futures pointing to a 0.6% gain, and Brent crude hovering near $98. As MUFG’s Derek Halpenny put it, financial markets remain in limbo, awaiting news on whether negotiations progress or another wave of strikes lies ahead.

Morning Macro Briefing

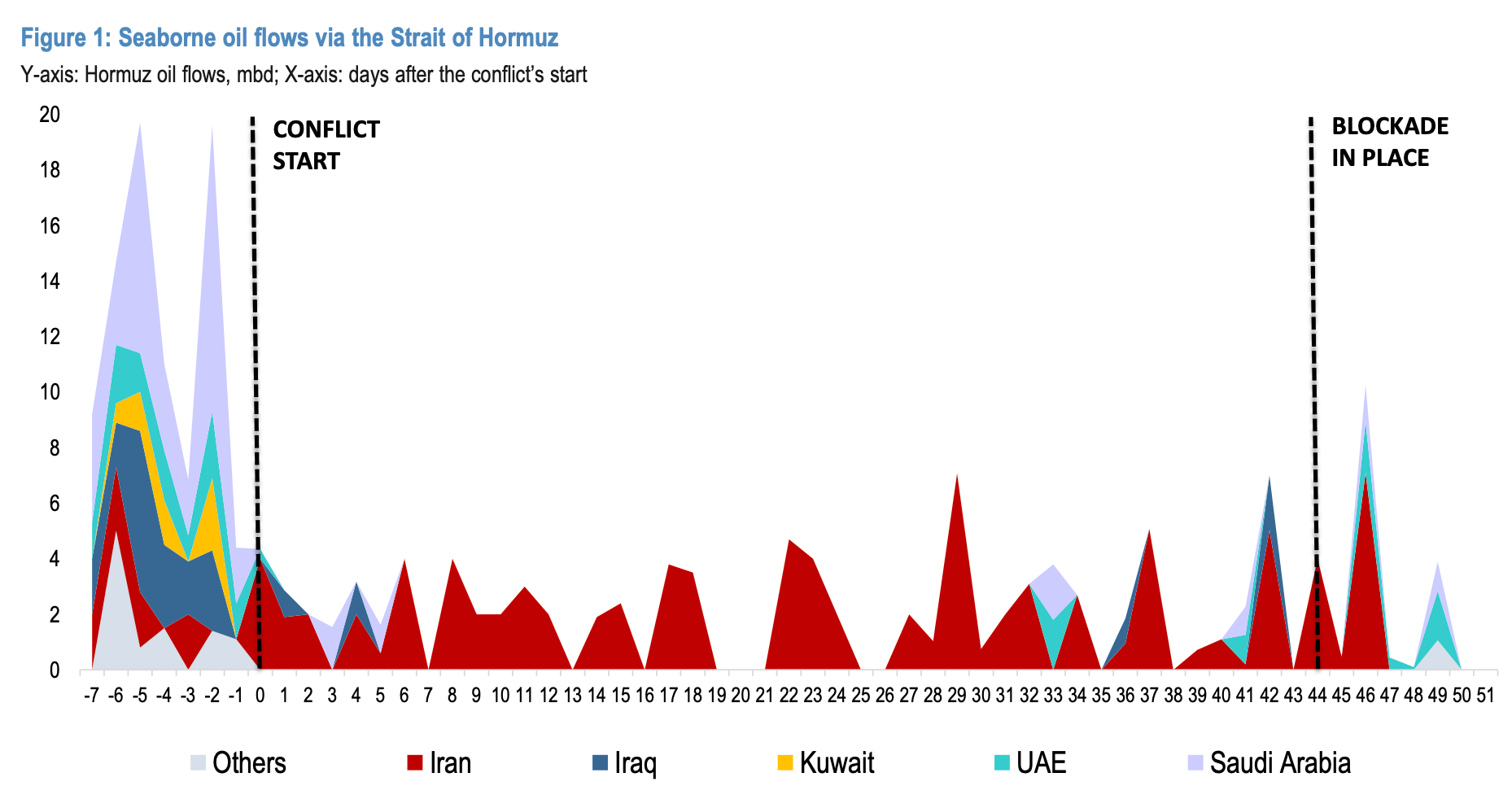

JPMorgan’s commodities team provides a useful clock for thinking about how long Tehran can sustain the current standoff. Iran’s onshore storage is running at roughly 54% capacity, leaving working room equivalent to approximately 22 days of exports, extendable to around 26 days if four Iran-linked VLCCs inside the Strait were loaded. The blockade is compressing flows rather than stopping them, with less than half of Iran’s March export pace currently estimated to be reaching global markets.

One asymmetric risk worth flagging this morning is the Houthi angle. Iranian state media reported over the weekend that Houthi forces in Yemen have been placed on high alert, bringing the Bab el-Mandeb back into focus as a potential venue for horizontal escalation. A second chokepoint under pressure would change the energy supply calculus materially.

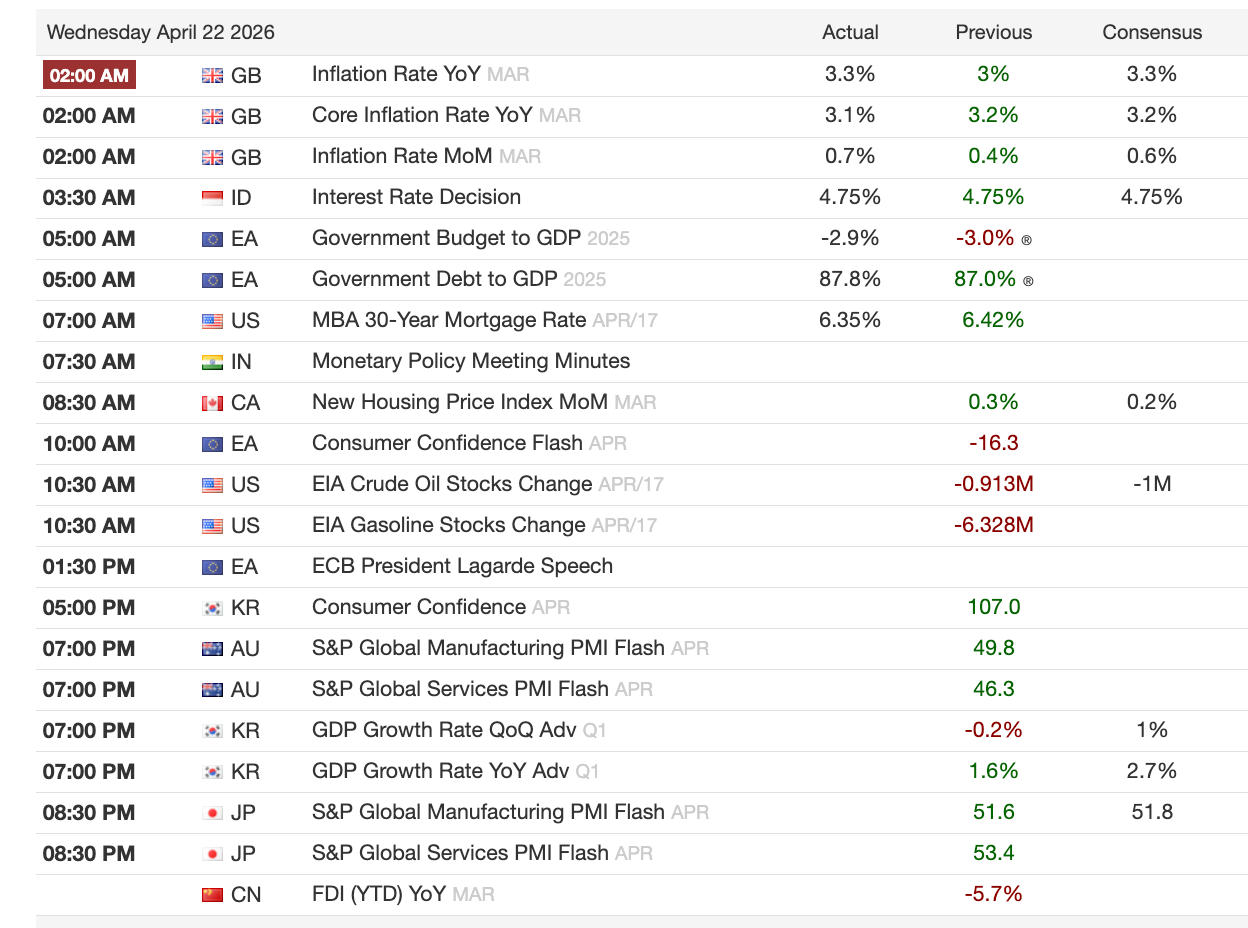

On the data side, March retail sales were a strong print. Core retail sales rose 0.7% month-on-month, well above expectations, with February revised upward, pushing Goldman’s Q1 GDP tracking to 3.3% annualized. The more pressing question is what April looks like once energy costs had more time to compound into spending behavior.

Ten-year US Treasury yields moved higher on Tuesday, settling near 4.3%, reflecting both geopolitical risk premium and attention to the Warsh nomination hearing. Warsh committed to Fed independence while framing inflation as a policy choice, and Democrats raised financial disclosure concerns. Senator Thom Tillis of North Carolina remains a potential obstacle, conditioning his support on the administration ending its investigation into Jerome Powell.

The macro impact of the Middle East war is beginning to show:

UK CPI rose to 3.3% in March, its highest in three months, driven primarily by war-related fuel price surges, with broader acceleration across housing, food, and services inflation.

South Korea’s March PPI jumped sharply, rising more than two percentage points to above 4%, reflecting the Middle East supply crunch feeding through the supply chain.

New Zealand’s market pricing for a May RBNZ rate hike has moved to around 50% following a second consecutive quarter of above-target CPI.

A sulphuric acid shortage, driven by Middle East supply disruption and compounded by China’s export restrictions, is creating a genuine operational problem for copper miners, with traders at the FT Commodities Summit describing customers panicked about securing supply.

Mercuria’s Kostas Bintas is explicitly flagging downside risk for copper if the conflict extends into a recession scenario, noting that a prolonged crisis is not yet in the price.

We had a long bias in Copper for this exact reason.

Singapore’s Foreign Minister Vivian Balakrishnan made clear that Singapore will not participate in any effort to restrict, interdict, or impose costs on traffic through the Straits of Malacca and Singapore. The message has been delivered to both Beijing and Washington, with Singapore, Malaysia, and Indonesia aligned on this position as trade-dependent economies with a direct strategic interest in keeping their waters open. This is an interesting issue, and Iran pushing for tolls for the Strait of Hormuz sets a precedent for this situation. Keep an eye on this.

Chart of the Day

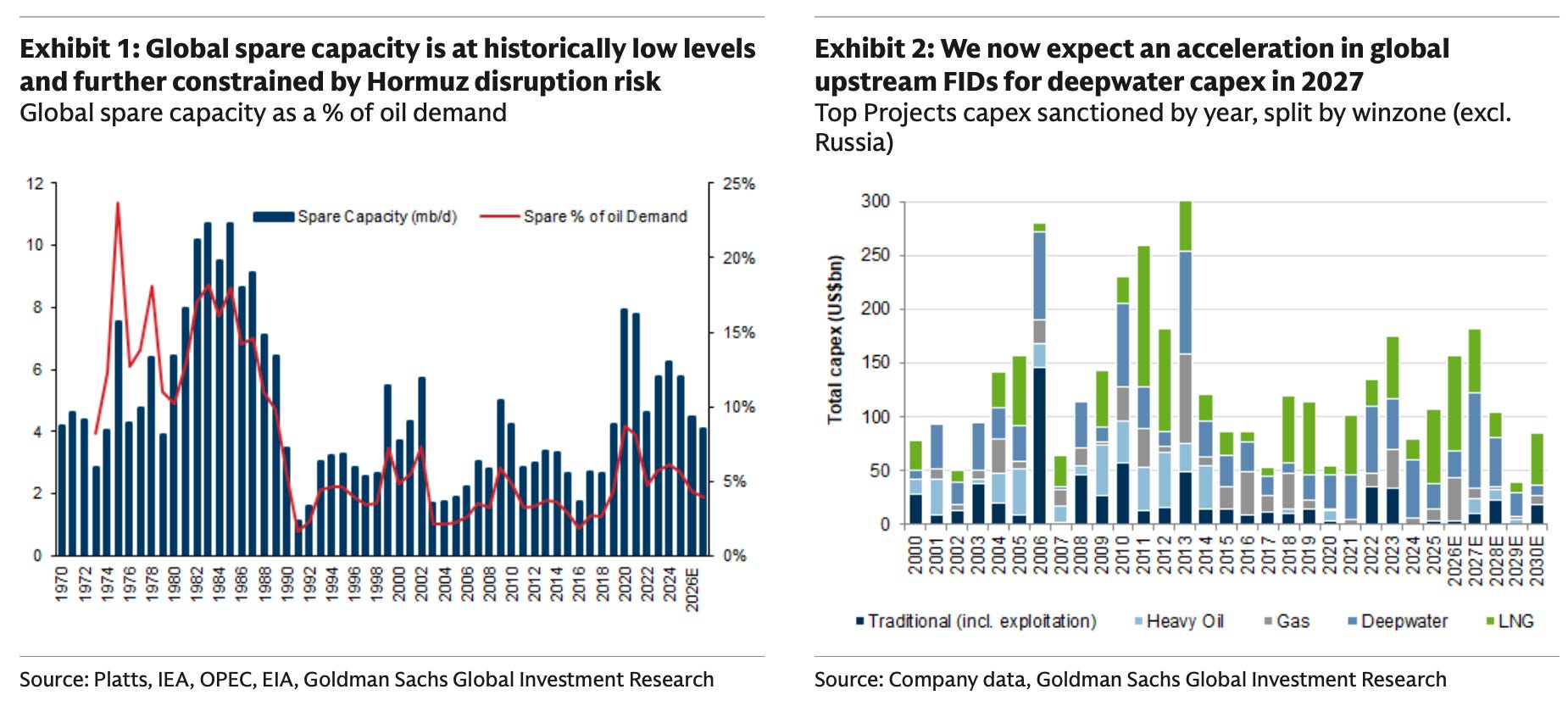

Goldman’s global energy team argues that the Iran War’s disruption to oil supply is triggering a major capex upcycle comparable to the early 2000s. Global spare capacity is already at historically low levels, and the team projects an acceleration in upstream deepwater investment decisions beginning in 2027.

Calendars

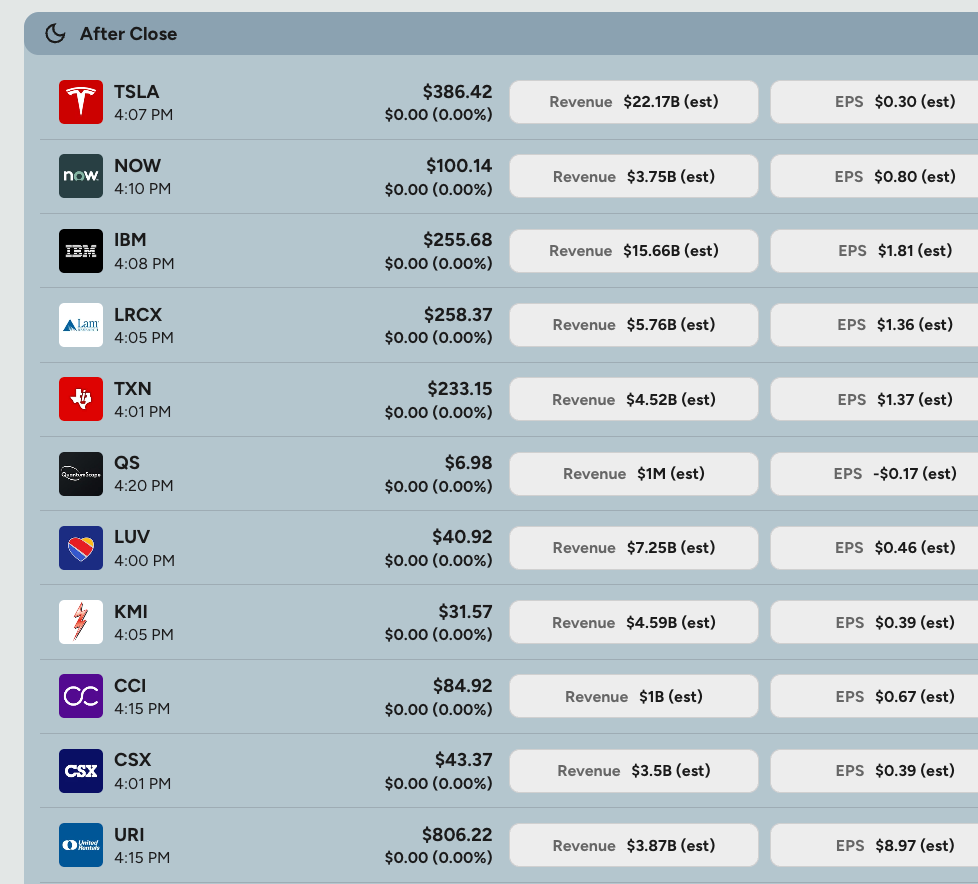

Earnings Updates

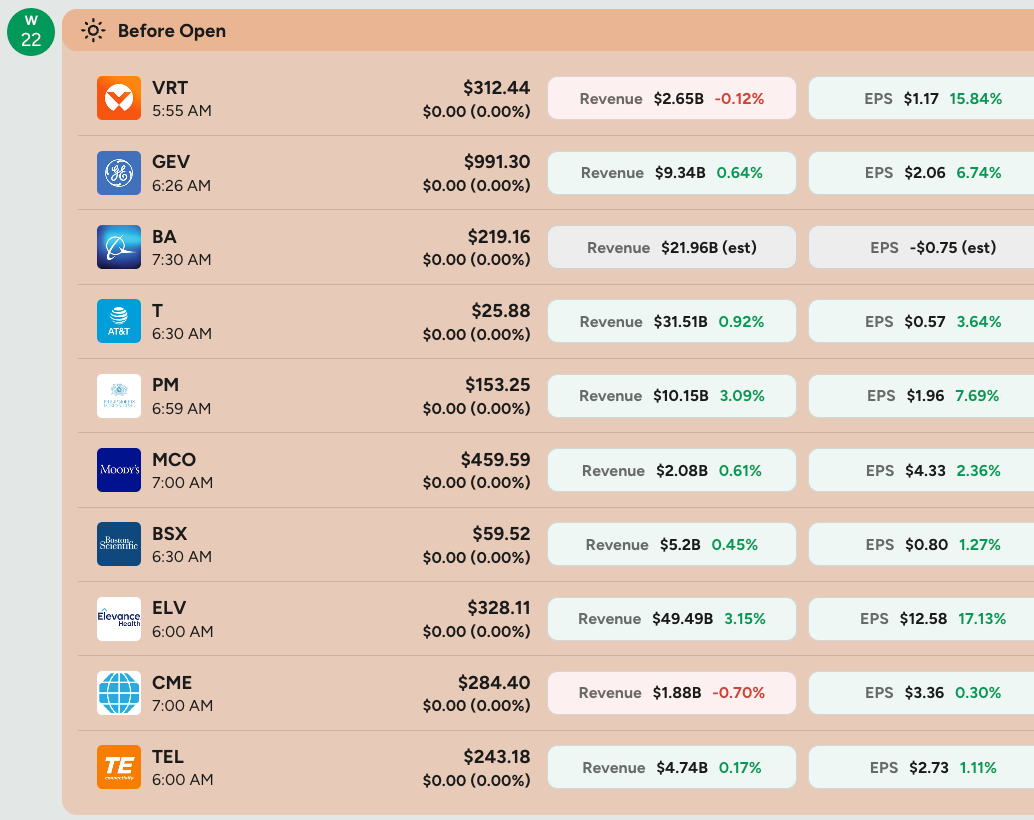

UnitedHealth Group (UNH) surged nearly 8% after beating first-quarter expectations and raising its full-year guidance, with investors encouraged by strong premium growth and the company’s ability to manage medical cost ratios through a complex regulatory environment.

RTX delivered double-digit organic sales growth and a 21% rise in adjusted EPS, prompting the defense contractor to raise its 2026 outlook on both sales and earnings, though investors weighed a record $271 billion backlog against ongoing supply chain constraints.

Danaher reported nearly 10% adjusted EPS growth fueled by strong performance in bioprocessing and life sciences, and announced its intention to acquire Masimo Corporation to expand its patient monitoring capabilities.

Capital One posted net income of $2.2 billion for the quarter with solid credit performance and a 23% reduction in marketing expenses, while investors focused on the Discover integration, which generated over $400 million in related costs during the period.

GE Aerospace beat first-quarter estimates but fell more than 5% as management flagged rising fuel costs and their effect on global flight volumes, with geopolitical uncertainty overshadowing an otherwise solid earnings print.

Market Prep

US equity futures are pointing to a gain of around 0.6% at the open. Asia was a split picture overnight: risk assets, including gold, silver, and bitcoin, moved higher while equities were broadly flat to down 1%, with the Nikkei touching a fresh record high above 59,700 before fading. Brent crude is hovering near $98, though the two shipping incidents in the Strait this morning could test the oil market in either direction.

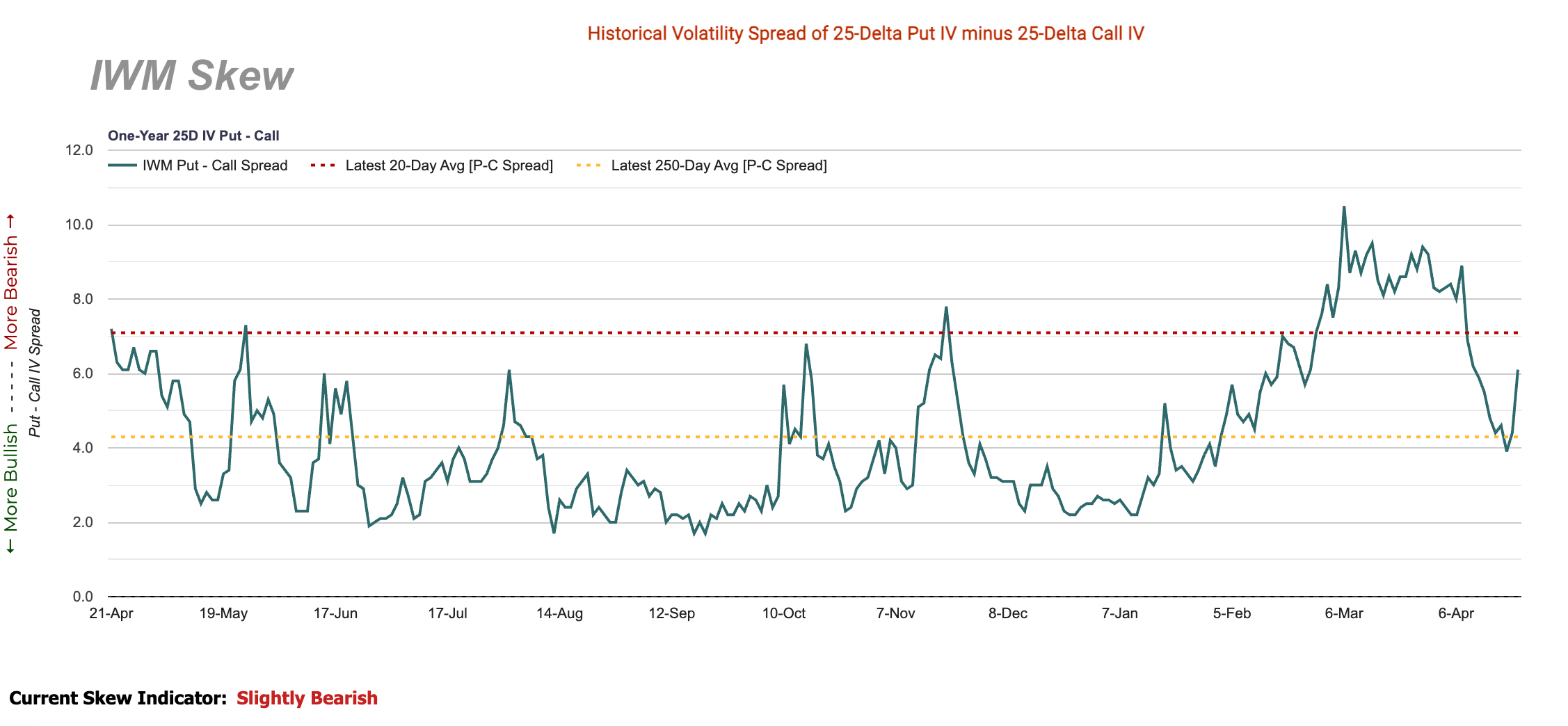

IWM skew is rising again, a signal that bearish sentiment in small-caps is building beneath the surface of the broader equity recovery. Small-cap skew has historically been a reliable early indicator of deteriorating risk appetite, and the move comes at a moment when the broader cross-asset complex is not fully aligned with equity pricing. This warrants attention, given where we are in the geopolitical timeline.

Goldman Sachs’ cross-asset strategy team frames the market picture clearly: equity markets have moved quickly to price out growth risks, but rates and energy tails have not followed, with Brent and European gas prices still roughly 30% above pre-war levels. Rate volatility has declined more slowly than in prior cycles because sticky baseline inflation expectations provide a floor that did not exist in 2022. Goldman’s three-month tactical positioning remains defensive, overweight cash, neutral equities, bonds, and commodities, and underweight credit, with near-dated puts on European and US equities flagged as attractive given the reset in skew pricing since early April.

Tesla kicks off the Mag-7 earnings season tonight after the US close, with investors watching Q1 figures and updates on Robotaxi, Optimus, and AI capacity progress. Separately, international concern is growing around the cybersecurity implications of Anthropic’s new Mythos AI model, with Japan’s Finance Ministry meeting major banks this week and both the RBA and RBNZ said to be monitoring developments.