Breakfast Bites: Rotations to Watch

Rotations to watch in the market; State of the Union Speech today; Anthropic's keynote at 9:30 am; HD reports

Rise and shine everyone

As the dust settles on the tariff situation, markets are stabilizing to a large extent. Yesterday saw the highest level of selling since Liberation Day, and not just in the US but across the globe.

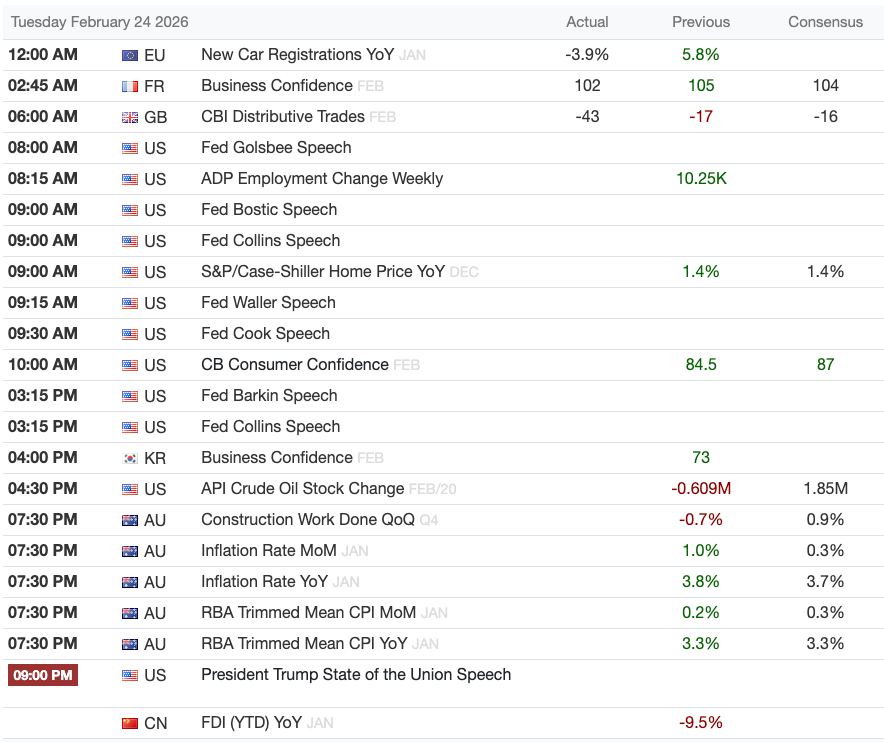

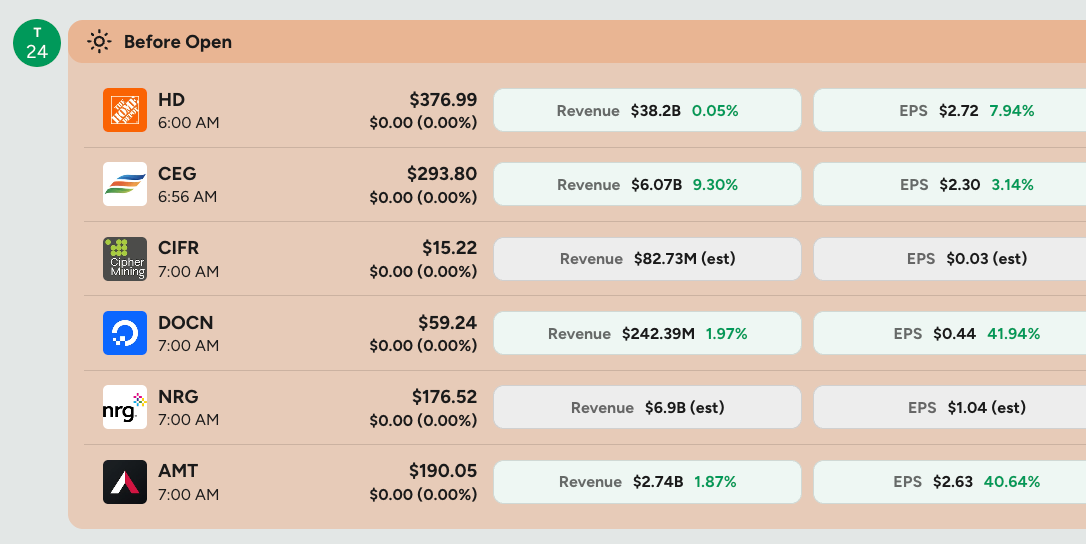

Today’s focus will be on the State of the Union address from President Trump, and of course earnings from Home Depot before market open.

Morning Macro Briefing

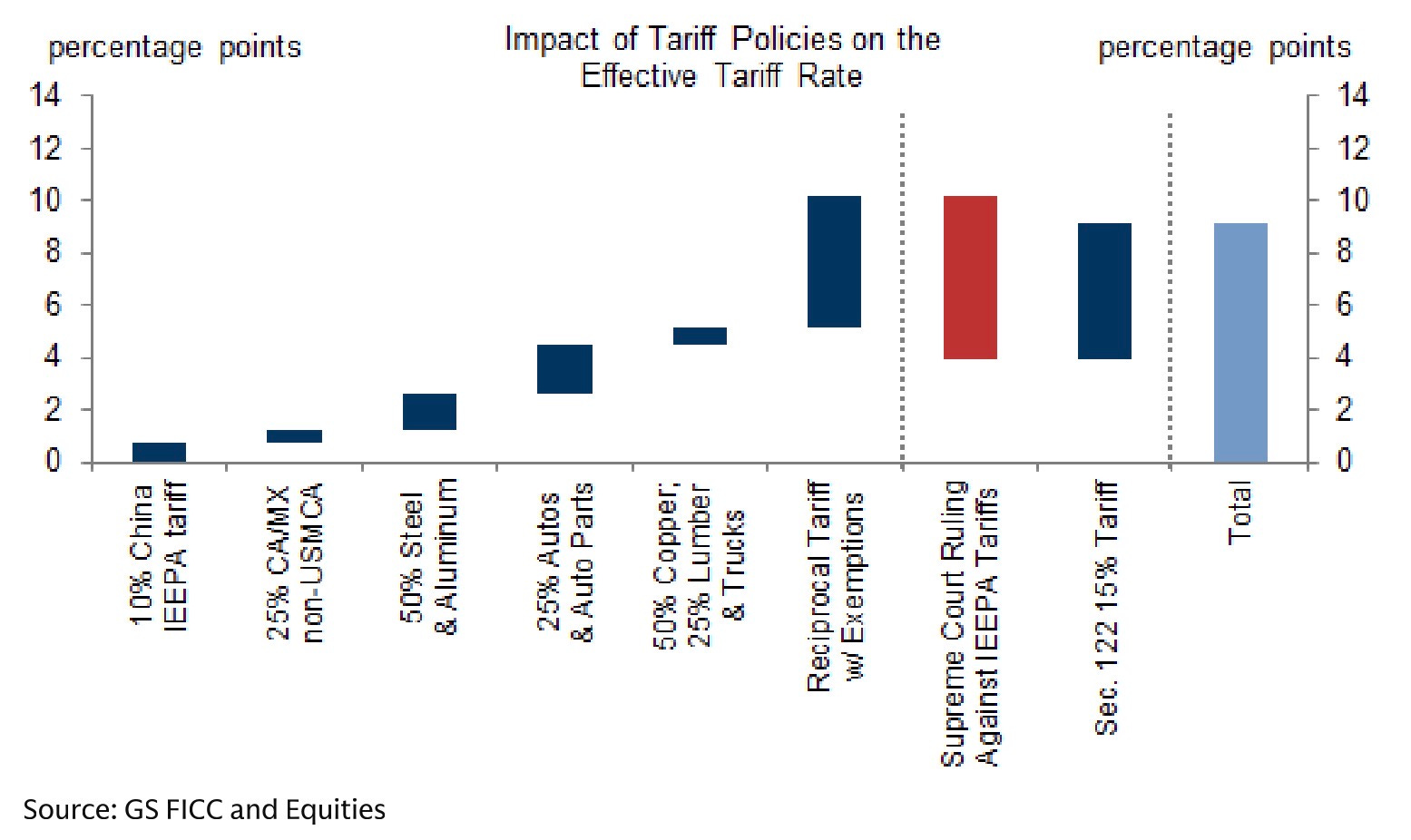

Increasingly, reports are circulating that the net impact of tariffs will not be as significant as initially expected. In fact, GS reports that the effective tariff drops from 10pp to 9pp.

Most Asian countries are set to benefit, as the tariff rates there have been negotiated at much higher levels. However, it remains to be seen whether the US administration can enforce the previously signed deals. All signs point to a renegotiation of these deals, but again, the situation remains uncertain.

Yesterday, GS also raised its oil prices targets for the year - Brent at $60 by the fourth quarter. Now, while most think this is related to Iran, they’re saying it is not. They don’t see disruption in supplies from Iran tensions, and rather suggest a lower level of OECD stocks leading to higher prices.

Europe is still grappling with a 15% tariff on exports after delaying a US trade pact, while tensions in Ukraine and energy disruptions in Slovakia add further pressure. Meanwhile, the Yen has weakened following dovish signals from Japan, even as oil and copper prices see modest gains.

JPMorgan recently shared a balanced outlook that pairs record income projections with long-term caution. CEO Jamie Dimon raised 2026 net interest income targets to $104.5 billion but warned of structural risks like inflation and AI disruption. He also signaled a potential succession timeline, suggesting he may transition to a chairman role in a few years. JPM sold off -4.22% yesterday.

FedEx is pursuing a significant legal challenge to recover duties paid under emergency tariffs recently ruled unlawful by the Supreme Court. This lawsuit could potentially offset over $1 billion in projected trade headwinds if the court mandates a full refund. While the timing of these payments remains unclear, the case sets a massive precedent for importers across the US. [WATCH FDX]

Calendars

Market Prep

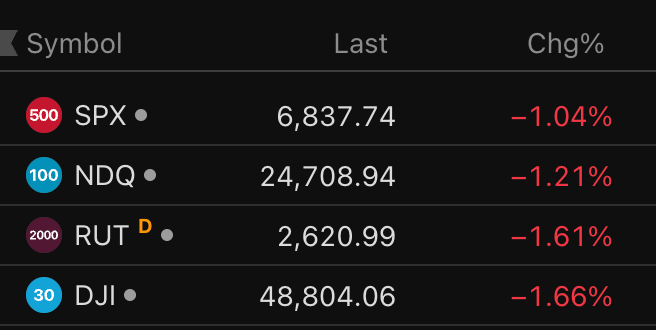

Yesterday saw the strongest level of selling since Liberation Day. I was wrong about the panic selling, but mostly right about the Russell2000 taking a relatively bigger hit.

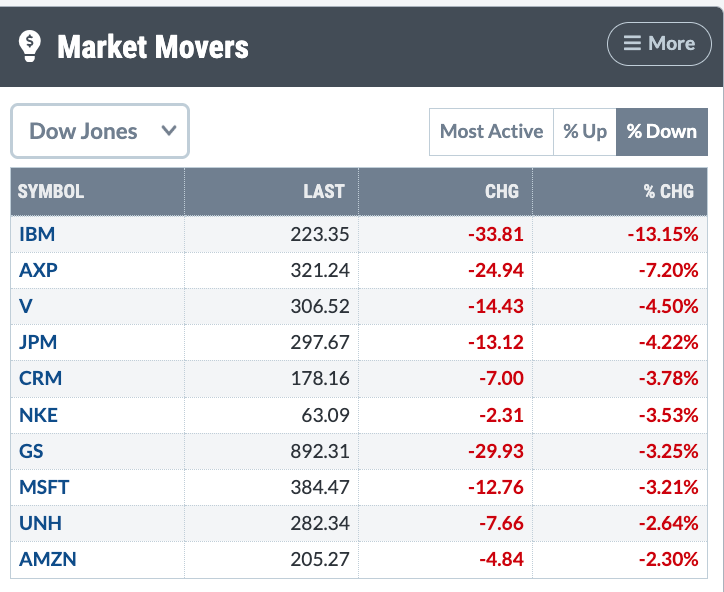

The DOW, however, closed lower than the Russell, but that was because of stock-specific sell-offs. Here’s what sold off in the DOW yesterday:

So what’s going on with markets right now? Well, for one, we talked about a lower probability of a Fed cut and a slim probability of putting hikes back on the table. That’s the overarching macro situation. This scenario should give the USD some strength, relative to where it stands right now.

Tariffs coming in slightly lower also bodes well for the economy and inflation. So while we are seeing a more hawkish narrative from the Fed, this may soften in time. So we’re looking at a scenario of a stronger USD in the next few months, followed by dollar weakness. But this is enough to consider a hit to Profit Margins, since the weaker dollar has been the biggest tailwind for corporate profits.

The bottom line: We will continue to see some volatility, and the story of stocks going straight up has been shaken for now. Watch the US Dollar.

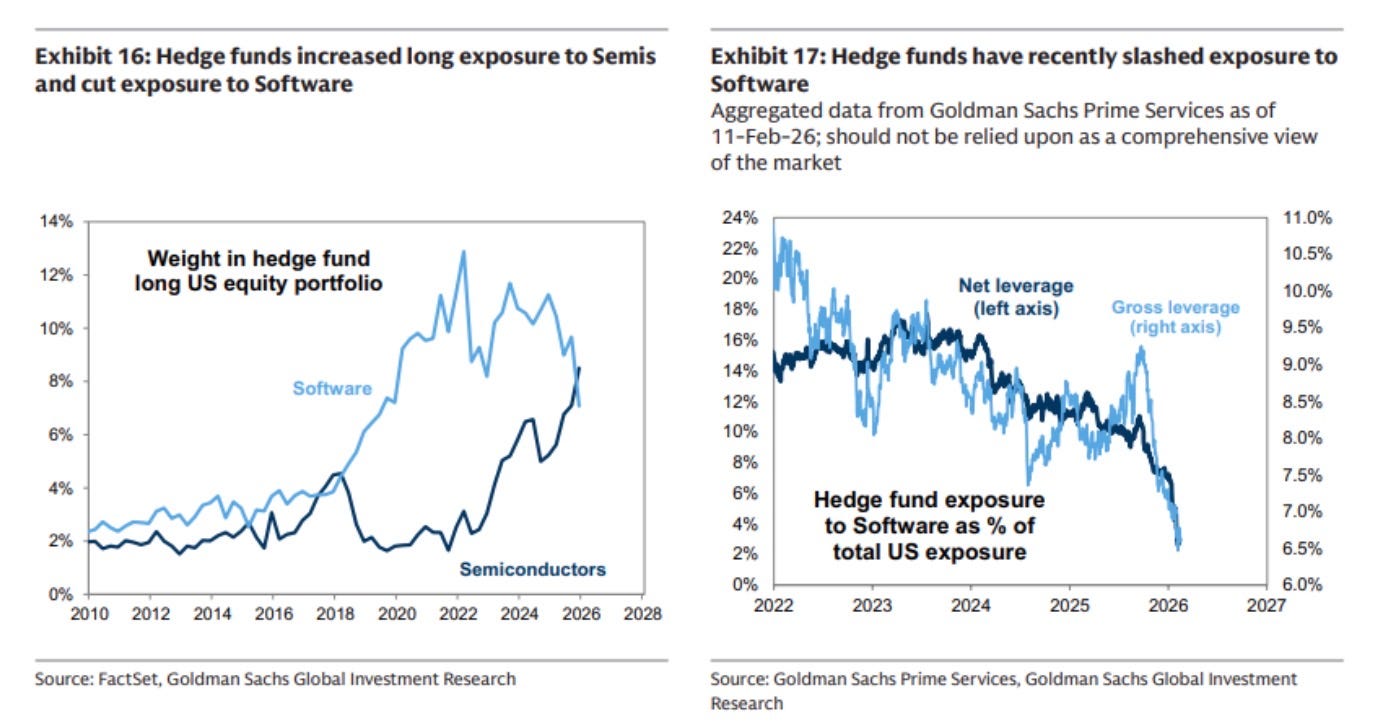

But on a more granular level, we are seeing a shift in positioning - something that started at least two to three weeks ago and has since intensified. While the Mag 7 still remains favored among most investors, we are seeing a distinct rotation in other areas.

Firstly, we have the AI rotation - out of Software and into Semis. This tells us that there is still high conviction in the AI story.

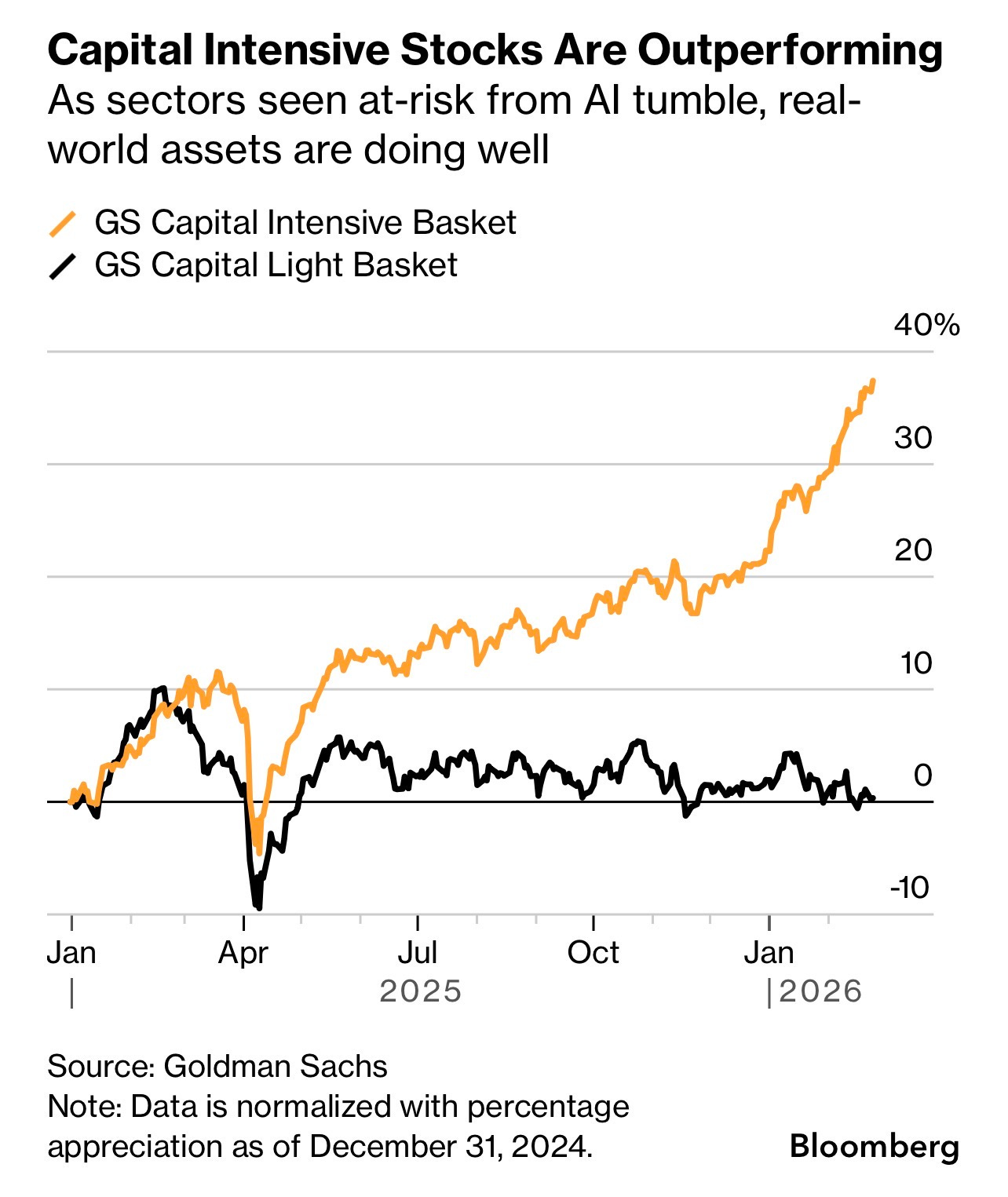

Secondly, we’re seeing rotation into old economy cyclicals. GS puts it nicely, calling this the “HALO effect” - Heavy Assets and Low Obsolescence. So more and more, investors are moving into companies that can withstand a certain level of AI displacement.

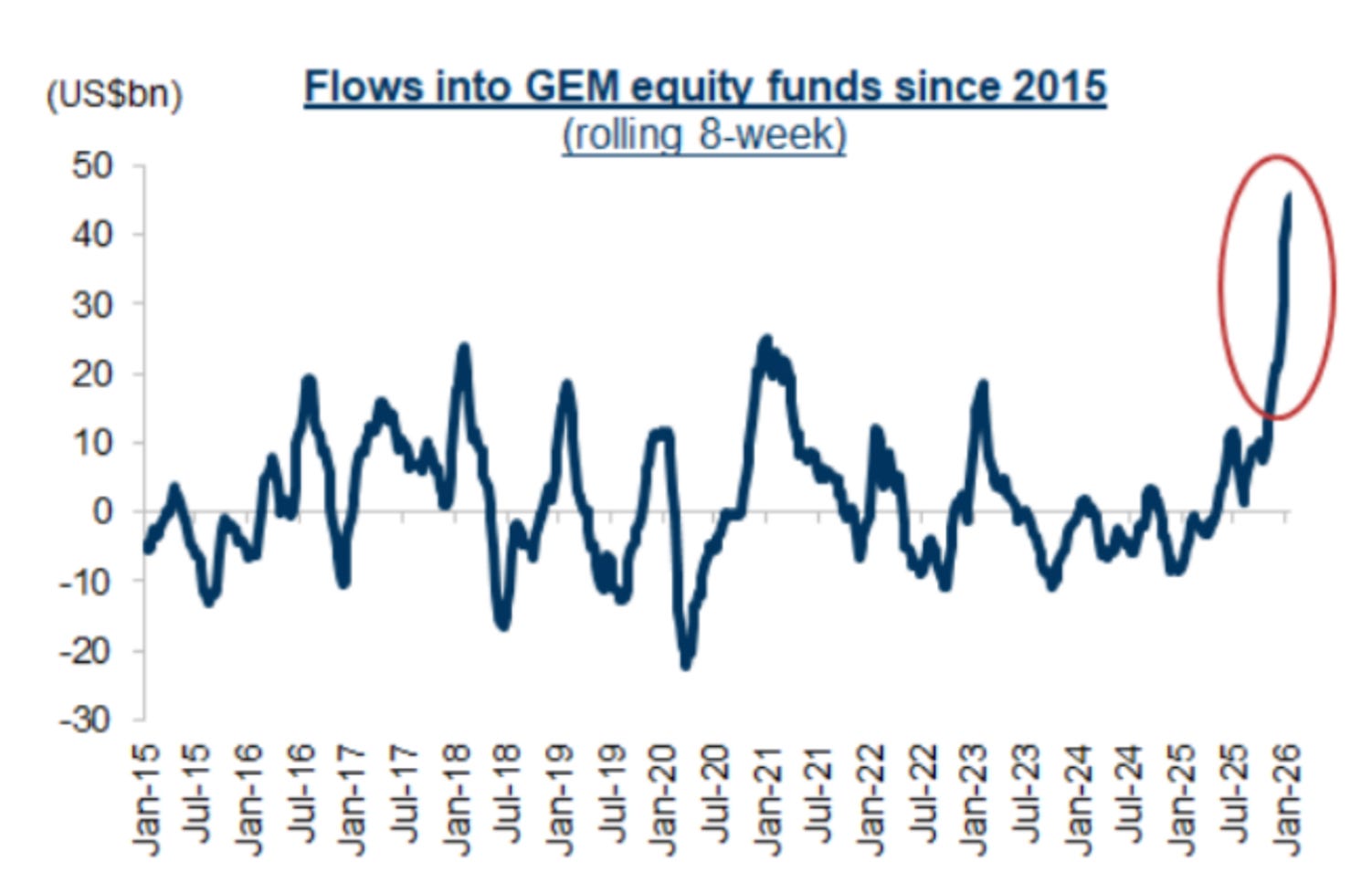

Finally, investors are looking at international markets, particularly EM. This doesn’t necessarily signal the end of US exceptionalism but rather investors getting nervous about the macro (US tariffs, New Fed Chair) and micro (AI story), and seeking diversification elsewhere. GS notes that Global EM Equity Funds have now recorded 18 consecutive weeks of inflows - the fastest annual pace of buying in two decades!

My Take

Today’s big event is the State of the Union Address by President Trump. I suspect there will be a discussion on global trade and the current geopolitical situation, including Iran.

We will likely see a bit of a bounce today, as more reports roll in about the tariffs actually being lower than before, and likely providing some boost to economic growth.

I’ve outlined three distinct rotation patterns that we’re seeing in the US markets - these are issues to keep an eye on. I also think it is becoming increasingly important to track the US dollar, as we’re likely to see some moves from here, and the strength of the USD is important for corporate profits.

Watch Anthropic’s “The Briefing: Enterprise Agents” keynote at 9:30 am ET.

Tactical Watchlist

No changes to the watchlist.

Yesterday was a tough day, but so far, the portfolio is still holding up.