Breakfast Bites: Relief Trade, Not All Clear

Oil is off its highs, futures are green, and almost nothing is resolved.

Rise and shine everyone

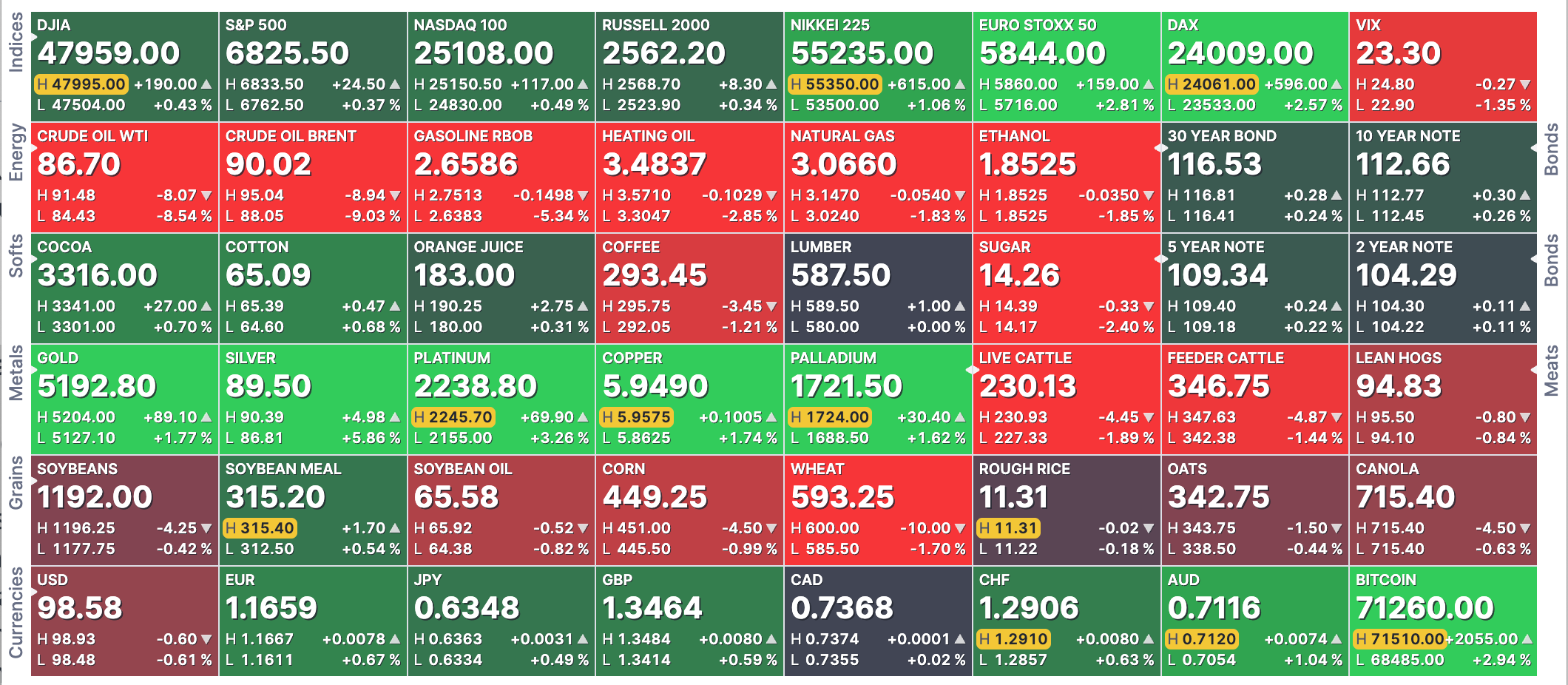

What a recovery in equity prices yesterday! What started out to be a horrific day, saw broad US equity indices end in the green. Again, it was any real substantial actions that led to this but rather headline news.

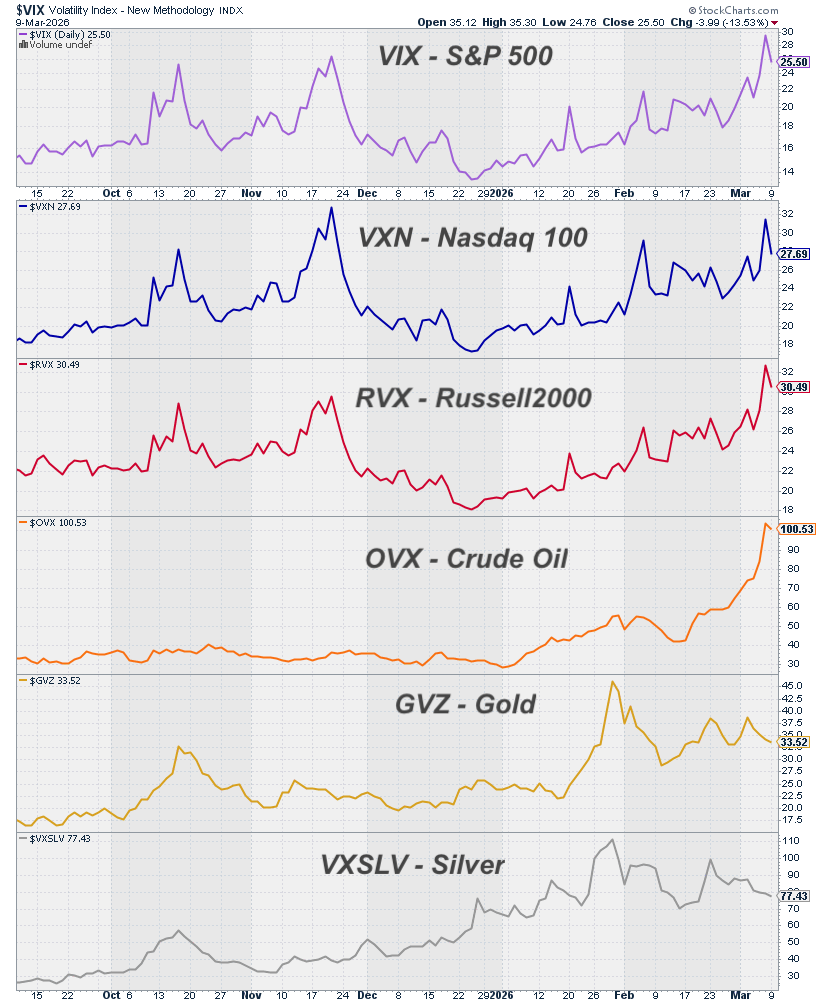

Volatility still remains significantly high in crude, and in equities for that matter. Where we see it has retreated is in the precious metals. Please remember, higher volatility increases the trading ranges, and can lead to sharper moves.

Morning Macro Briefing

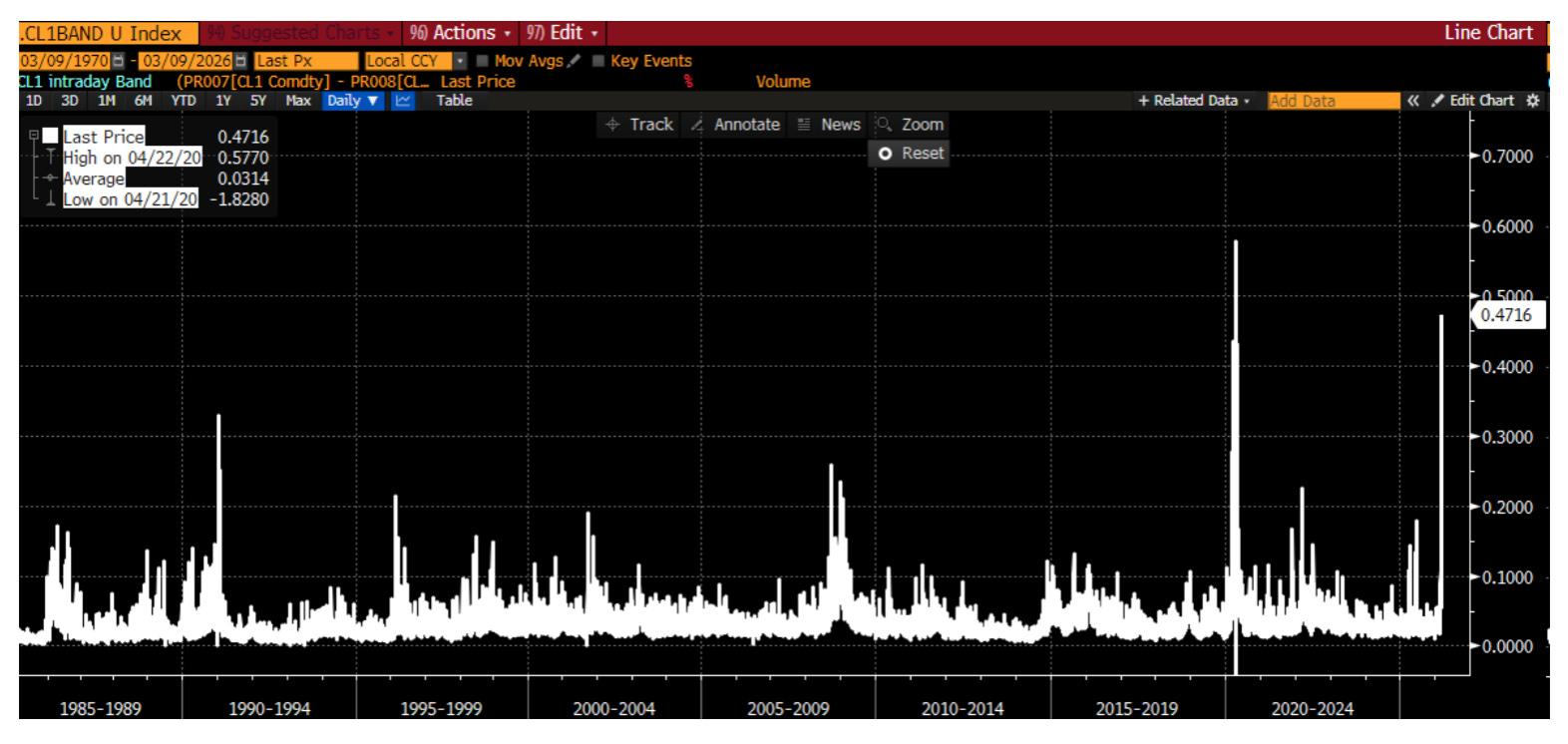

Oil prices staged a dramatic intraday reversal yesterday, plunging from near $120 to around $80/bbl on the back of SPR headlines and Trump’s comments on the war’s progress.

The move marked the second largest trading range outside Covid, but the relief may be short-lived. Trump followed up during the Asia session warning that Iran will be “hit harder” if it withholds oil supply, while the IRGC responded that Tehran will not allow “one liter” of regional oil to flow if US and Israeli attacks continue. This back-and-forth keeps the situation fragile.

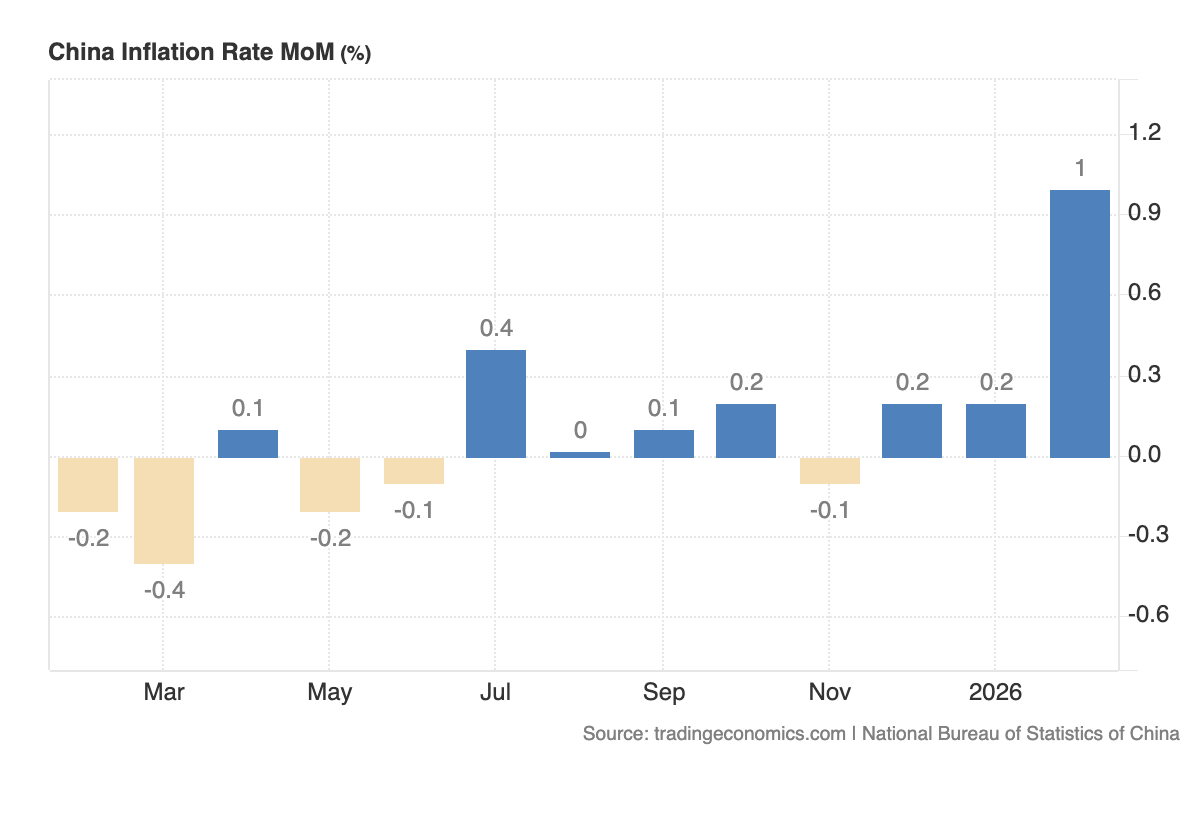

In all the Hormuz noise, China’s weekend data barely got a mention. CPI rose 1% month-on-month in February, the highest since February 2024. PPI came in at -0.9% year-on-year, a notable improvement from -1.4% in January and better than the -1.1% consensus.

The PPI details matter here. Deflation is easing across production materials and intermediate goods, and processed goods prices actually turned positive at 0.3%. Premier Li flagged an “appropriate rebound” in prices as a key monetary policy goal. China may be shifting from exporting deflation to exporting inflation, and that changes a lot of things.

Asian central banks were already dealing with soft core inflation reflecting domestic slack. Add imported price pressures from China on top of an energy shock, and the calculus gets uncomfortable fast. Holding or easing just became a harder call.

China’s trade numbers were a blowout. January-February exports surged 21.8% year-on-year, with February-only growth estimated near 40%, and the trade surplus hit $213.6 billion against a $196.6 billion consensus. ASEAN and EU exports were both up around 20%, while US-bound exports fell nearly 17% in the combined period, though implied February-only US exports rose 9.7%.

Two things inflate that headline. China merges January-February data to smooth Lunar New Year distortions, and this year the holiday fell later than in 2025. There’s also a strong frontloading argument, with exporters likely rushing shipments after the Supreme Court struck down the Trump administration’s IEEPA tariffs. The underlying trend is softer than it looks. Worth keeping in mind as Trump heads to Beijing at end of March for talks with Xi.

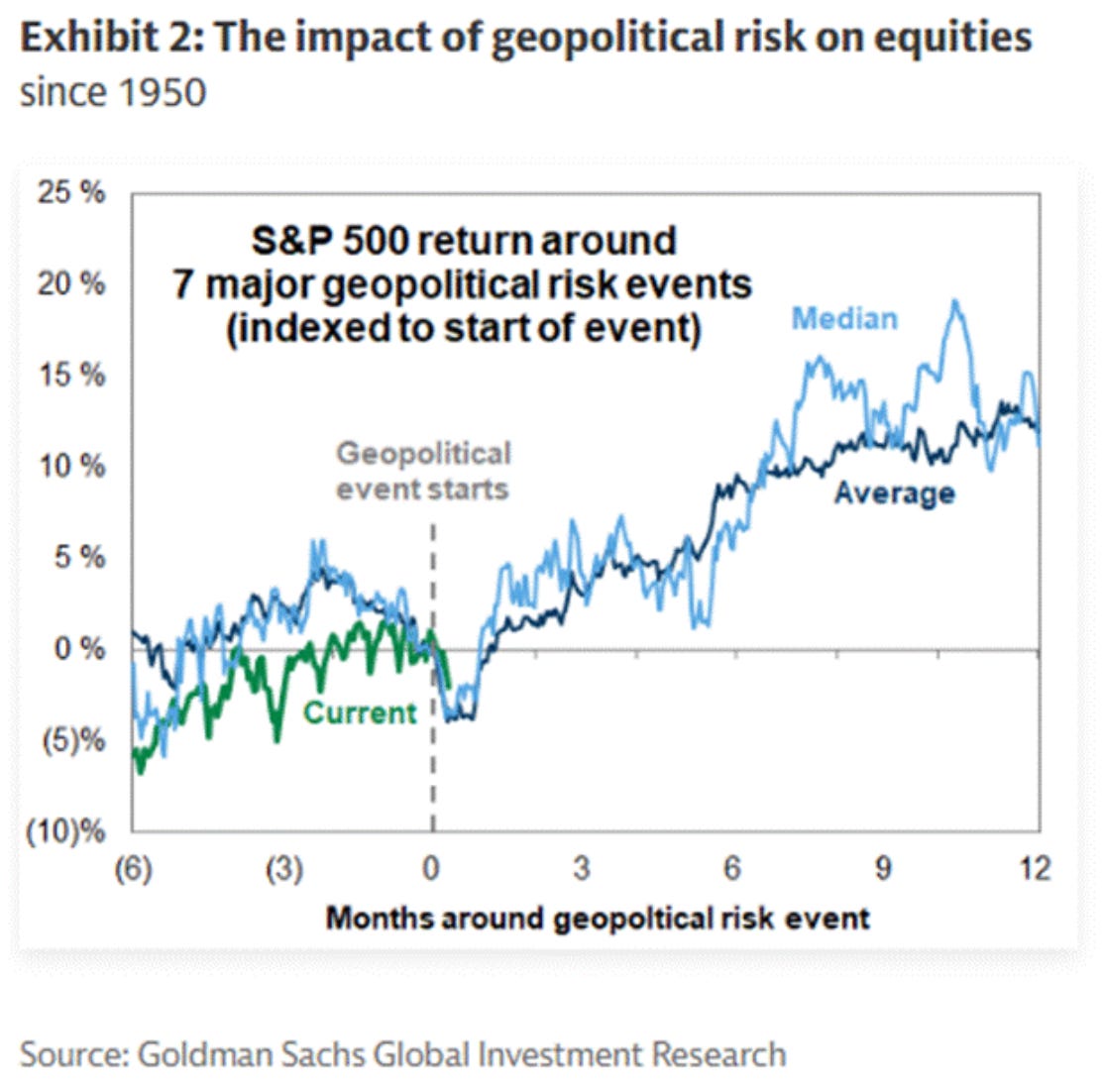

Chart of the Day

“During seven geopolitical risk episodes since 1950, the S&P 500 declined by an average of 4% in the first week but recovered within the subsequent month.” - GS

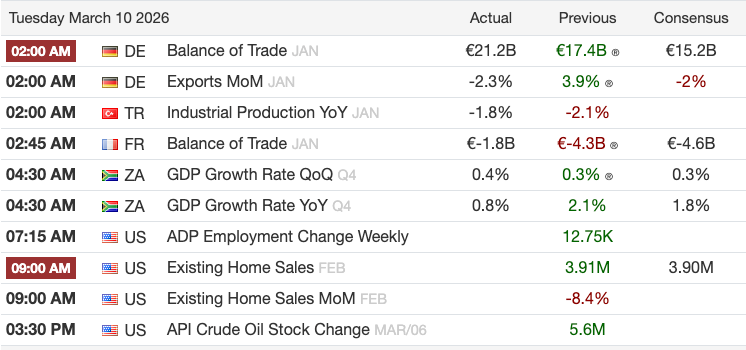

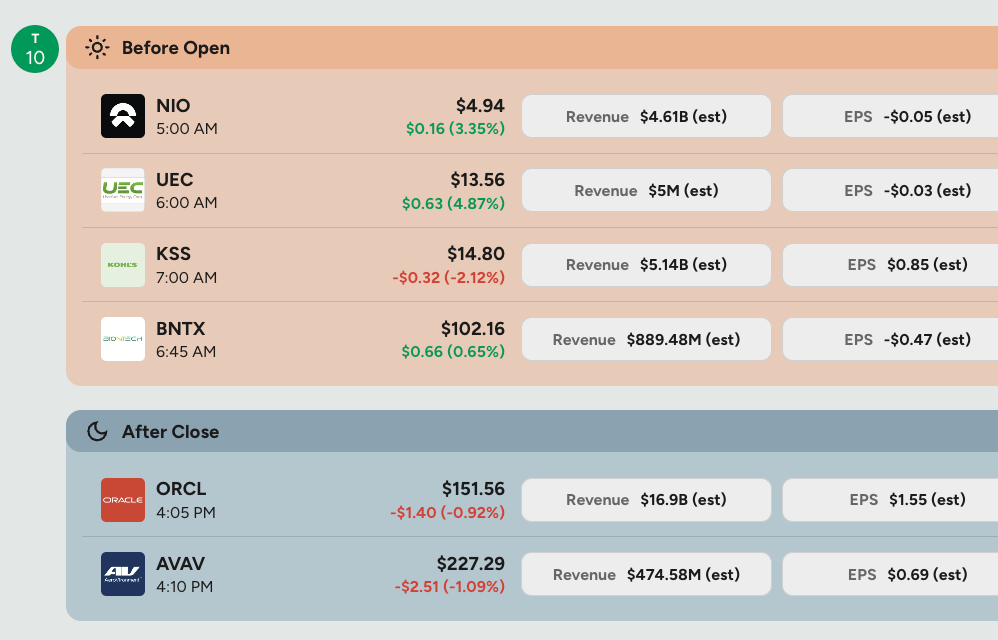

Calendars

Market Prep

The big news yesterday came towards the end of the trading day when President Trump said:

“I think the war is very complete, pretty much. They have no navy, no communications, they’ve got no Air Force.”

According to CBS, he added that the U.S. is “very far” ahead of his initial 4-5 week estimated time frame. This gave people some relief and hope that the war could be nearing an end.

The initial rally was sparked by the SPR talk. The IEA called for a coordinated release, the G7 was “considering” one — then confirmed they would wait. Later, Energy Secretary Wright said, “we’re talking about coordinating releases from the SPR.”

That the conversation is still at the talking stage suggests the war is far from over. Iran has given no indication that it is agreeing to anything, so headline-driven volatility is not going away.

The worse news from yesterday: further shut-ins, with Saudi Arabia now cutting output. As we’ve noted, the longer production stays offline, the harder the restart.

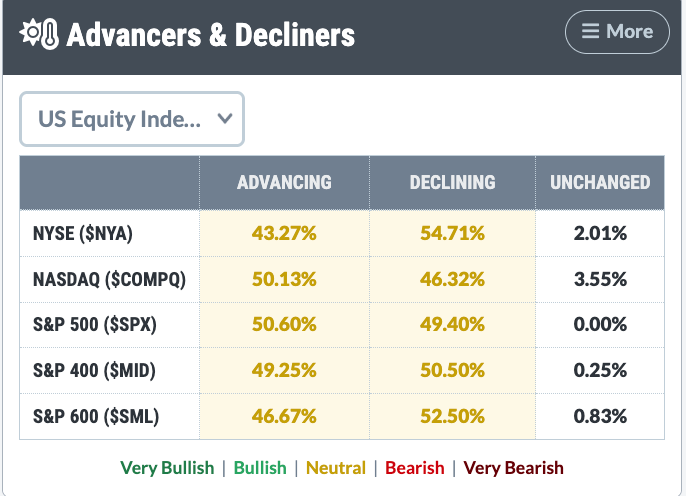

As for the market yesterday, despite the stark recovery, market breadth was tepid. Advancers & Decliners point to a more neutral stance.

Asian markets bounced back overnight, with the Kospi recovering 4.3% after yesterday’s 7% drop and the Nikkei adding 2.3%. All major indices clawed back some ground following the recent volatility. Ahead of the BOJ decision on March 19, the probability of a 25bp hike this month remains negligible at 3.5%, while April sits at 62%. The BOJ also notably rejected over 75% of offers to sell short-dated JGBs, with long-end Japanese yields slipping 3-4bps and the curve flattening.

US futures are choppy but holding in the green despite the VIX staying above 23. Precious metals and Bitcoin are recovering alongside a softer dollar. Soft agricultural commodities are under pressure, with reports of fertilizer shortages adding a new layer of concern for food markets.

On to the highlight of the day - Oracle earnings.

Oracle reports earnings after the bell today, and the bar is simultaneously high and treacherous. The market expects roughly 20% revenue growth and an 82% jump in cloud infrastructure sales, but investors are less focused on the top line than on capital expenditure guidance. Oracle is on track to spend over $50 billion on capex this fiscal year, and negative free cash flow has become a real concern. (the chart below is quite remarkable). We’ve talked about this: Too much spending spooks the market; too little raises questions about its ability to compete. So management in a difficult position either way.

Finally, here’s a summary of what GS says about CTAs and Options:

CTAs (trend-following algo funds): Heavily long the S&P 500 near the top of their historical range, but momentum signals had turned negative, so they were primed to sell. The market absorbed a $3.7B close-of-day sell order and closed just above a key technical level. Had it closed below, CTA selling would have been much more aggressive. We’re in a fragile zone where small moves could trigger large mechanical selling.

Options/Derivatives: Fear came out of the market fast today. Vol and hedging costs got crushed. Their internal panic index hit nearly a perfect 10 over the weekend. Dealers have now flipped to a position where they’ll amplify any move lower, so a selloff could get disorderly quickly. Tomorrow’s expected daily move is priced at 2.13%.

My Take

Yesterday’s recovery was real but fragile. Breadth was tepid, the VIX is still above 23, and dealers are now positioned to amplify any move lower. One bad headline out of the Strait and the unwind gets disorderly fast.

The SPR conversation is still just that - a conversation. Iran hasn’t agreed to anything, Saudi output is being cut further, and the longer production stays offline, the messier the restart. Oil volatility isn’t going away, and neither is the uncertainty premium baked into every risk asset right now.

The China data adds a new wrinkle worth watching. If deflation is genuinely turning in Beijing, Asian central banks face an imported inflation problem on top of an energy shock, at exactly the wrong moment. The Fed gets all the attention, but it’s the BOJ, the RBI, and regional peers who may be walking into the harder policy corner.