Breakfast Bites: Reflation

Beijing summit puts Taiwan front and center, PPI confirms the reflation story, and Retail Sales this morning tells us if the consumer is still standing.

Rise and shine everyone

The market is showing us clear signs of reflation. Yesterday’s PPI coming in at the highest since 2022 added to the story that CPI told us the day before. This shouldn’t really come as a surprise. We know that commodity prices are going up, and that’s being reflected in the numbers.

We added an exposure to copper on Mar 04, 2026. We were early, and it was a bumpy ride, but since then, copper prices have inflated by over 10% to reach an all-time high.

Yes, we’re seeing a 1% pullback today, and that is to be expected when we encounter parabolic moves. Nevertheless, this is the new reality for us now. Commodities will continue to push higher.

Morning Macro Briefing

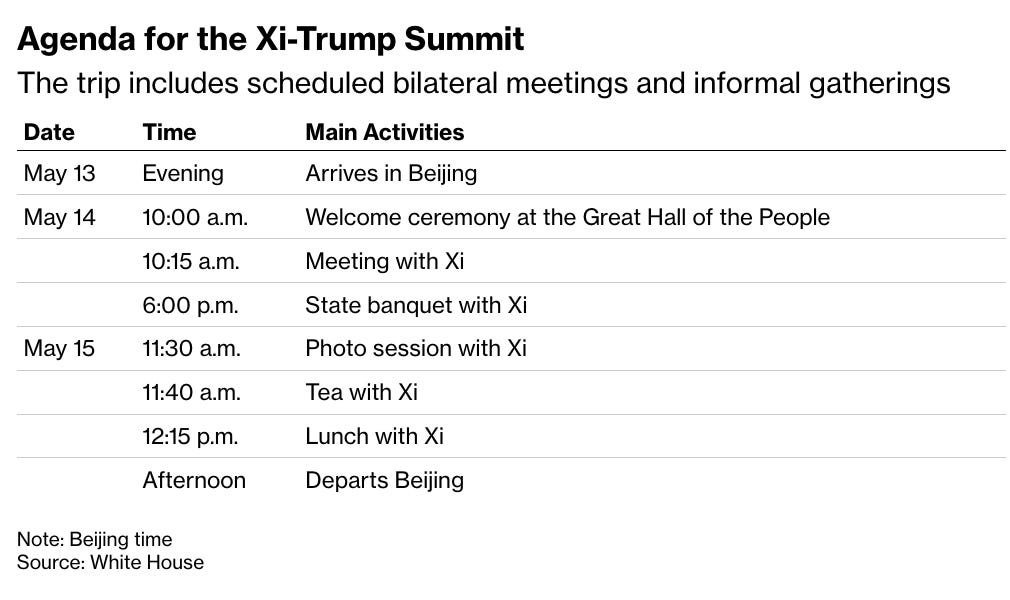

“Xi warns Trump on Taiwan” is what’s making the headlines today. The two presidents met for nearly two and a half hours today, the first visit by a sitting US president to China in nine years.

The substance, so far, has been thinner than the atmosphere. The most developed framework being discussed is a potential $30 billion in tariff reductions on goods neither side deems a national security risk. For context, China ran a trade surplus of roughly $85 billion in April alone. Goldman explicitly rules out a “grand bargain,” given the strategic gaps that remain.

For markets, the read-through is not panic but it is a ceiling. China-exposed equities and the yuan have both run hard into this week on summit optimism, and the risk now is that Trump departs Beijing Friday without the concrete concessions on tariffs and export controls that would justify those moves.

We also don’t think that there will be any concrete discussion or resolution about the Middle East war. Yes, China is in somewhat of a bind with the price of energy going up, but it’s not a reason for them to get directly involved.

The Taiwan warning is what deserves the closest attention from us. The informal concessions Trump may make, without any formal announcement, are the real concern for those with Taiwan and regional semiconductor exposure. Any quiet shift in the US position on arms sales would have direct implications for TSMC, the TWSE broadly, and Kospi names. Watch what comes out of Friday’s working lunch, and watch what is not in the official readout.

Now on to macro data.

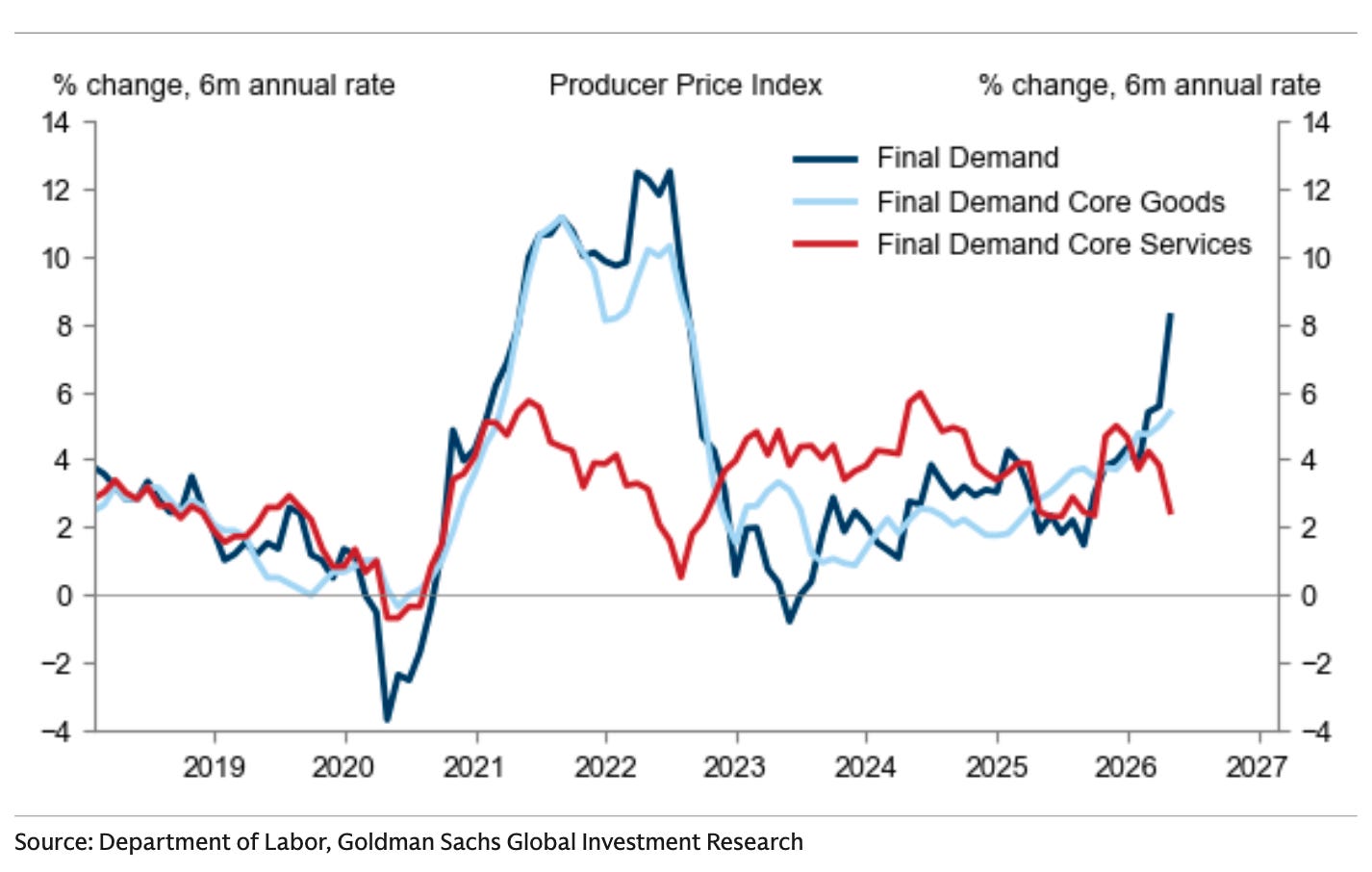

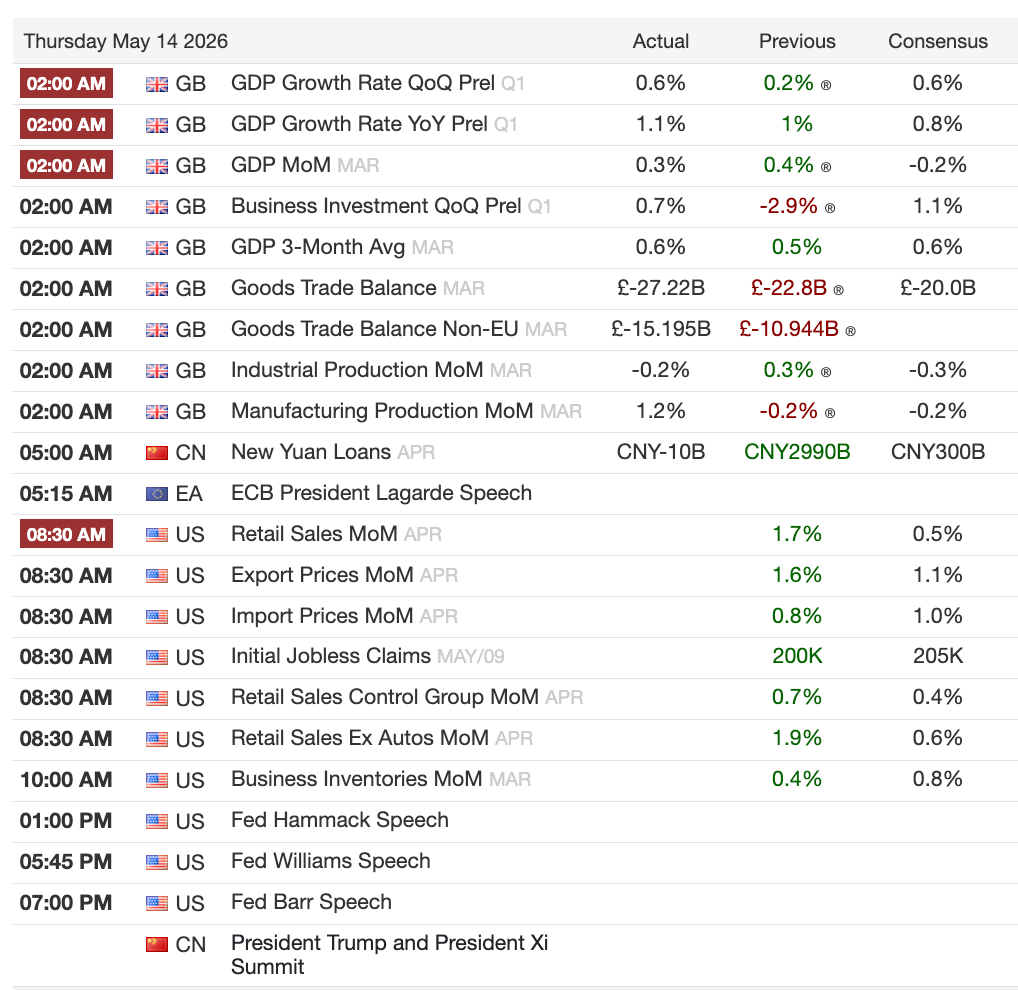

As we discussed, reflation is on the cards. PPI for April came in at +1.4% MoM and +6.0% YoY, well above the median forecast of +0.5%. Energy prices rose 7.8% on the back of elevated oil from the Iran conflict, but the story underneath was not just energy. Transportation and warehousing services surged 5% as fuel costs fed into the core, and retailer margins expanded 2.7%, a sign businesses are still successfully passing costs downstream.

The implications for the Fed are now material. We’d talked about one cut this year, in Q3, and Goldman is now echoing that view after pushing out its final two expected cuts to December 2026 and March 2027. The only scenario that changes this calculus is political. With midterms in November, a newly confirmed Fed Chair Warsh may feel pressure to deliver a cut ahead of the vote.

(It feels so weird to say Fed Chair Warsh!)

In Japan, the 10-year JGB yield hit 2.6% overnight, a level not seen since 1997, and the 30-year is also at an all-time high. BOJ board member Masu added hawkish commentary this morning, saying rates need to rise “at the earliest stage possible.” The JGB move feeds directly into global duration pricing and is a risk for anyone long bonds anywhere.

The US April Retail Sales print is out at 8:30am ET. Watch the control group measure specifically. A weak control group alongside a hot PPI is the combination that sharpens the stagflation narrative and gives the rates market something more to run with.

Chart of the Day

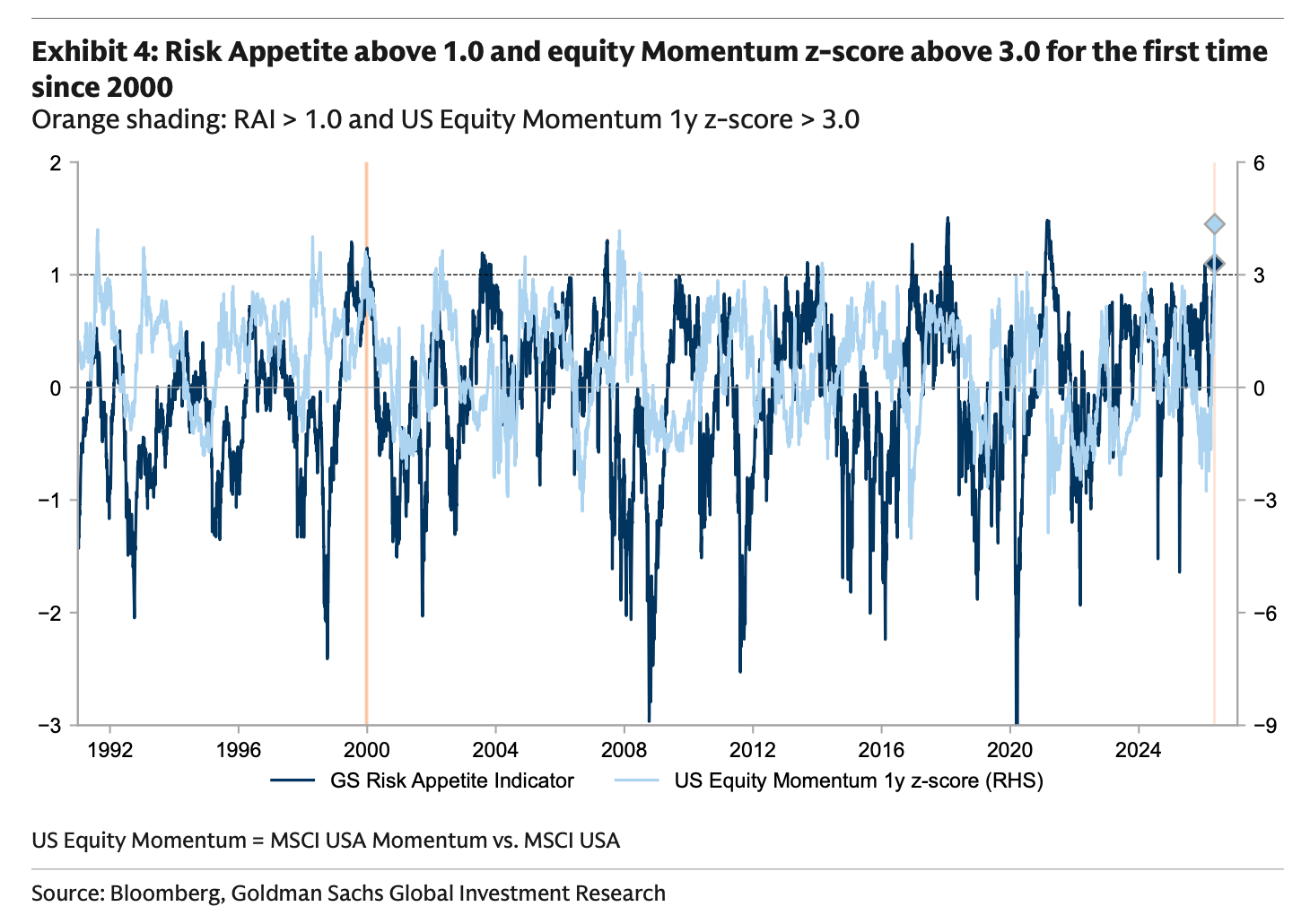

Goldman’s Risk Appetite Indicator rose above 1.1 this week, a level reached only 2% of the time since 1950. What makes the setup unusual is that US Equity Momentum has simultaneously hit a 1-year rolling z-score above 3.0, the first time both have been this elevated simultaneously since 2000. History across comparable episodes shows modest positive forward returns for the broad market on average, but wide and symmetric tails for Momentum, and when Momentum unwound in those episodes, it tended to start quickly from these entry levels.

Calendars

Market Prep

US equity futures are pointing modestly higher this morning, up 0.1% to 0.3% through the Asia session. The SPX and NDX both reversed post-PPI losses on Wednesday to close higher, with China ADRs, Semis, Mag 7, and Cyclicals doing the heavy lifting. That said, only 64% of S&P 500 members actually finished higher. The index-level strength is masking a narrower tape than the headline suggests.

The positioning backdrop is stretched. Call option positioning has turned sharply bullish since March, with call/put volumes, call skew, and spot/vol correlation all elevated across equity markets.

Goldman recommends put spread collars funded by selling OTM calls as the preferred structure given the high call skew. Goldman’s desk estimates show retail trading volumes up 28% since mid-April, and margin debt has hit a record $1.3 trillion, or 52% of gross customer balances. Retail is levered and long, which amplifies moves in both directions.

On rates, the 10-year at 4.47% is not yet at the level where equity investors broadly reprice risk. JPM puts that threshold at 4.60-4.65%, and the pace of any move matters as much as the level. Watch the bond market’s reaction to Retail Sales this morning first.

Cisco surged more than 19% after Wednesday’s close after raising its forward outlook, a print that cut through the inflation noise and reminded the market that underlying tech demand remains strong. What makes the move more than just a one-day earnings pop is the context: Cisco has now fully recouped the losses it suffered in the dotcom collapse, a 25-year round trip that says something about both the staying power of enterprise networking infrastructure and just how long markets can take to forgive a bubble. For investors, it is a useful signal that the AI-driven upgrade cycle is feeding through into real enterprise spending, not just hyperscaler capex.

Three things anchor today’s session: the Retail Sales control group at 8:30am as the test of whether the consumer is beginning to crack; any fresh headline out of Beijing as Trump attends Thursday evening’s state banquet alongside Jensen Huang and Elon Musk, with Xi’s Taiwan posture the shadow over all of it; and AMAT after the close as the live read on whether AI capex is translating into real semiconductor equipment order flow.

My Take

The Xi-Trump summit has delivered a warm atmosphere and Xi’s sharpest-ever Taiwan warning. What it has not delivered, so far, is a deal that justifies the China-exposed positioning that went into this week. I would be trimming into any Friday rally that treats the summit as an unambiguous win.

The inflation picture is now unmistakably uncomfortable. PPI at a four-year high following a hot CPI means core PCE for April is tracking at 3.3% YoY, Goldman has pushed its next cut out to December, and the Fed is one bad print away from a hike conversation becoming serious.

The Risk Appetite and Momentum setup is the most extended since 2000. The macro backdrop is still holding, but the asymmetry from here is clearly worse than it was three months ago. I want to own protection, not press longs.

Retail Sales this morning will be one to watch. A weak print into a hot PPI sharpens the stagflation narrative and gives the rates market a reason to push yields toward that 4.60-4.65% zone that JPM has flagged as the equity pain threshold.

Our watchlist and specific positioning below the paywall.