Breakfast Bites - Reciprocal to Retaliatory

Tariffs are getting complicated - more letters released; FOMC didn't bring big surprises; NVDA hits $4T market cap

Rise and shine everyone.

During the US session, equities extended their impressive rally, defying the skepticism that has persisted among many analysts and institutional investors. The NASDAQ led the charge to a new all-time high, driven in large part by continued strength in the tech sector. Nvidia briefly touched a staggering $4 trillion market cap!

Bond yields declined across the board, reflecting a bid for duration amid shifting macro expectations. US Treasuries found support following a well-received 10-year auction, which drew solid demand and reinforced investor confidence in the stability of US debt markets. The drop in yields also helped ease some pressure on equity valuations, particularly for high-growth tech stocks that are sensitive to interest rate moves.

The FOMC meeting minutes gave us a mixed picture, with some saying they want to cut in July and some saying they ought to wait to see the impact of tariffs on inflation. This is now a big debate - do the tariffs cause inflation or do people just stop buying and we see deflation? I doubt that it will be the latter just yet. And something tells me that with this new round of tariff letters, we’re not likely to see a cut in July.

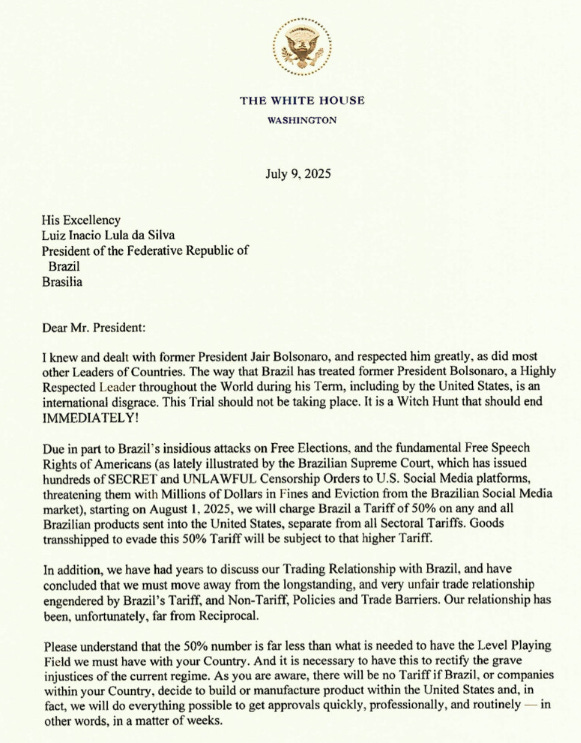

Speaking of tariffs, we’ve now moved from reciprocal to retaliatory. John Authers from Bloomberg points out this morning that tariffs are no longer about trade but rather about politics. He states Brazil as one example, and here’s the letter sent to them.

On the flip side, I’m in Bangladesh right now - one of the major exporters of daily wear clothing to the US. What I’m hearing is that one of the conditions for the 35% tariff is that Bangladesh needs to reduce its imports from China. There needs to be a value addition of 40% before an item can be shipped to the US. So while we have proposed reciprocal purchases from the US with likes of ordering Boeing jets, seemingly that’s not enough. There’s a bigger agenda here, which involves reducing world trade with China.

And of course, there’s the tariff on copper. President Trump reiterated the 50% tariff on copper starting Aug 1. The question is not whether mining can be moved or how long it takes, but that right now, about 45% of the copper used in the US is imported. Assuming that some of this can be moved to local sources immediately, it still means there could be sizable cost increases for infrastructure and construction. Couple this with increasing wages as immigrants have to leave these construction jobs, and we’re looking at a definite slowdown in activity and/or increasing prices.

I say all this to illustrate just how complicated everything is becoming. Most analysts are banking on this being a strategy that will later be reversed. But for now, it’s causing not just a rift among countries but also further turmoil in global and US markets.

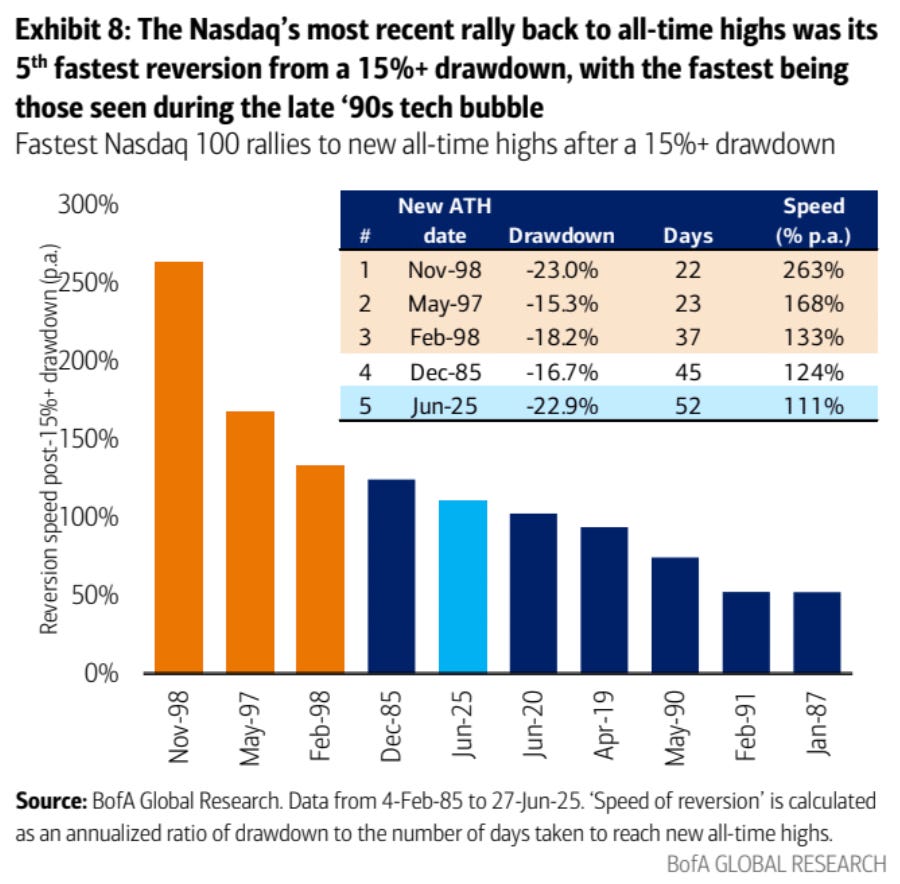

Chart of the Day

This chart is from a few days ago but, it’s still a good one. The recent rally in the Nasdaq is the 5th fastest reversion in history!

What We’re Watching Today

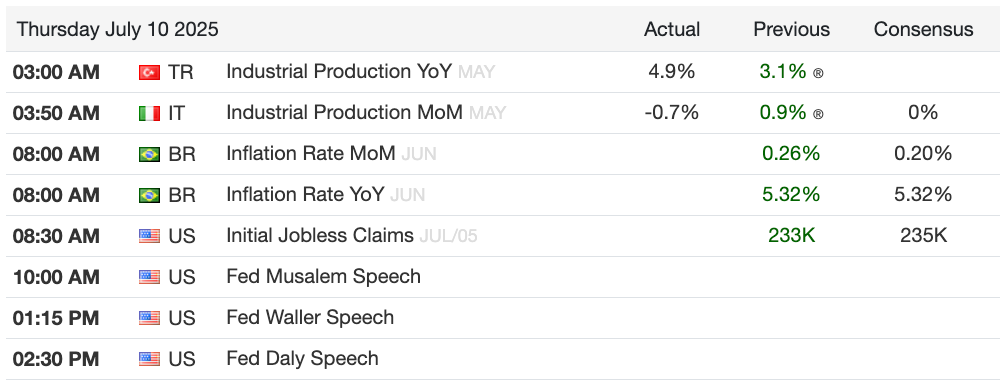

8:30 am ET - US Jobless Claims - Initial and Continuing

(The jobs market is cooling. Last week, we saw continuing claims continue to spike, meaning hiring is slowing down. Let’s see what this week brings.)

Calendars

(news taken from Reuters, FT, Bloomberg; Calendar from Trading Economics)