Breakfast Bites: Rates may matter more than narrative

Central bank decisions on watch - BoJ, BoE and ECB; The Santa Rally and Seasonality; The Yield Curve; Our take on the small cap trade and fresh tactical ideas (behind the paywall)

Rise and shine everyone

Happy Monday! While the biggest week for the US was last week, we have major macro events for the rest of the world this week. The ECB, the Bank of England and the Bank of Japan all deliver their rate decision on Thursday / Friday, with the BoJ probably the most watched event.

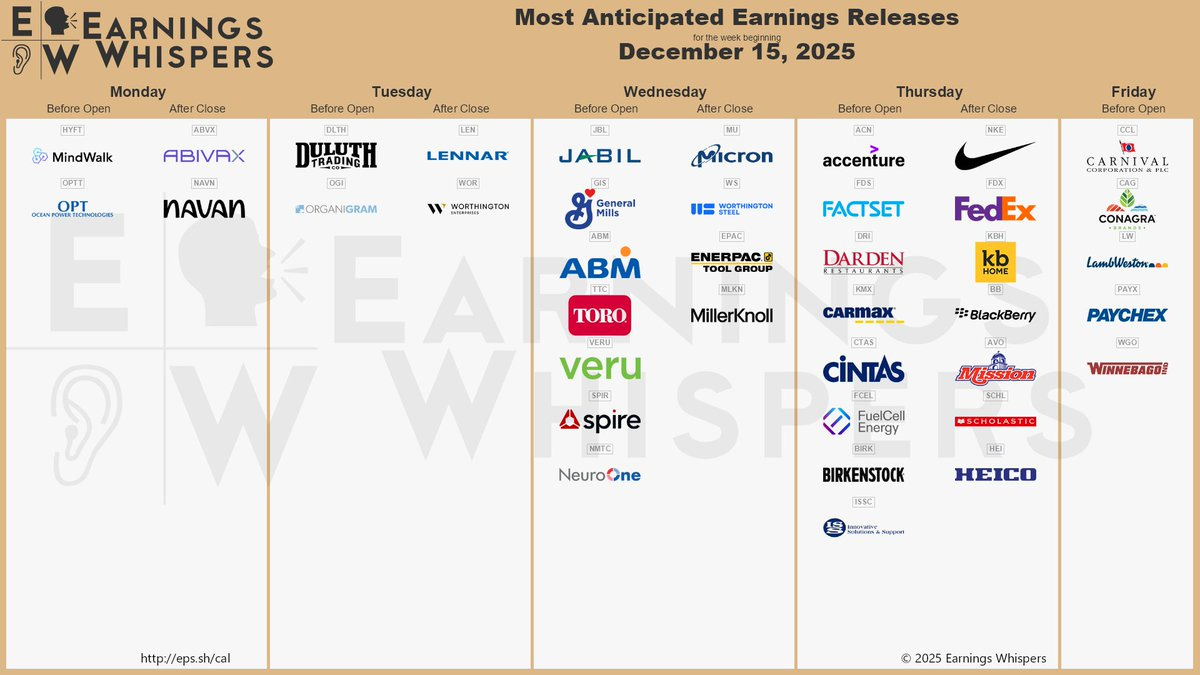

In the US, we expect the Employment Report and CPI numbers. We also get earnings from FedEx, Nike, and Micron.

In today’s edition, we also look at where bond yields are going and what we see for the small cap trade.

Morning Macro Briefing

Just a few macro developments to note today, before diving into the week’s preview. The main events start from tomorrow.

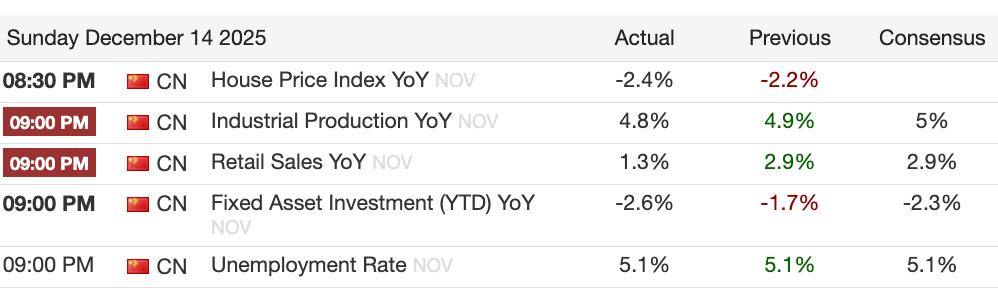

China saw a number of data releases, and most were not up to the mark.

Home prices continue to fall. We’ve been discussing problems cropping up again in the China property market - there have been defaults and payment delays. And this data proves further that there is a lack of demand.

Speaking of demand, Retail Sales has also been on a decelerating path, with November “marking the slowest yearly rise since December 2022 despite ongoing consumer subsidy programs from Beijing”.

Fixed Investment is falling, and while there is a strategy to curb overcapacity, the major declines came from property investment and infrastructure.

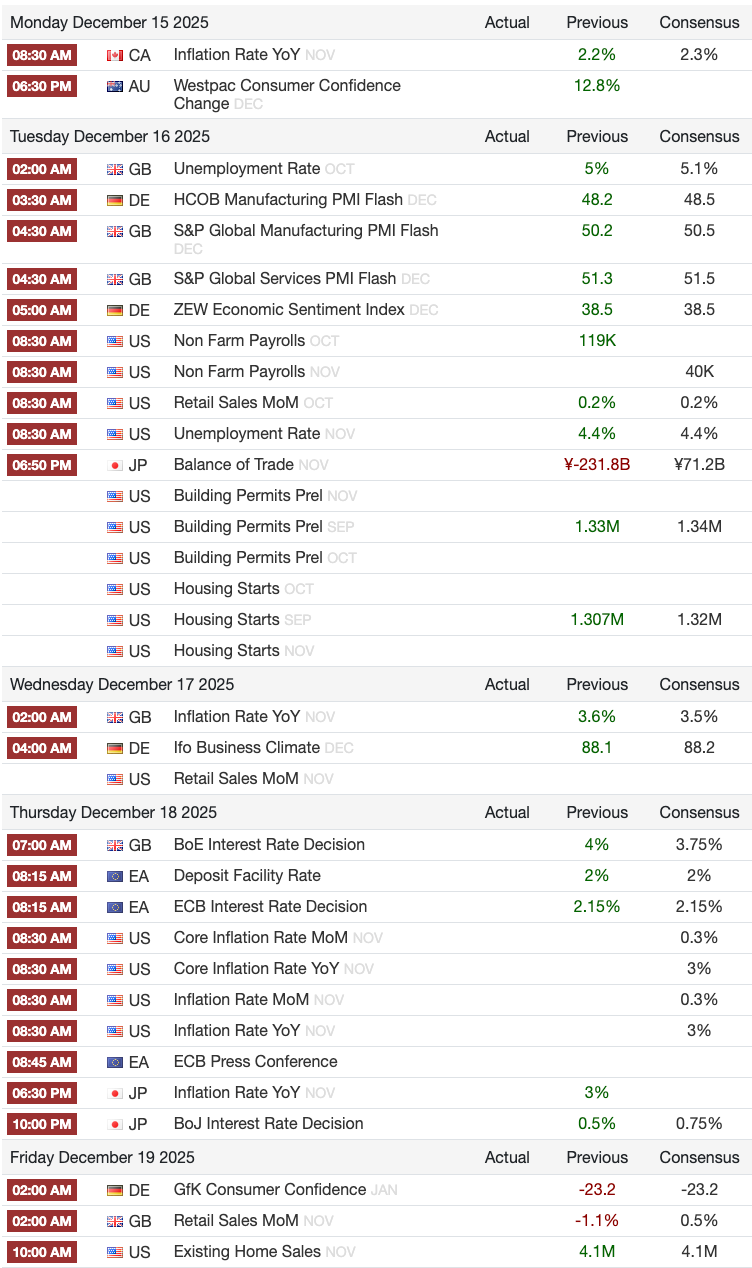

This Week’s Outlook

Key Events This Week

Central Banks

BoJ (Early Friday in Asia; Thu 7:50pm ET);

ECB (Thu 8:15am ET);

BoE (Thu 7am ET)

US Macro

Tue: NFP (Oct & Nov) + Unemployment Rate (Nov); PMI

Thu: CPI

Fri: PCE

Earnings - Wed - Micron; Thu - FedEx, Nike- All After Market

Central Bank Expectations

Bank of Japan - Hike by 25bps expected

Hike from 0.50% to 0.75% expected. The Real Interest Rate still remains negative, with inflation hovering around 3%. Given that Japan has been contending with very low levels of inflation prior to 2022, the current inflation levels are significant and healthy to a certain extent.

We say to a certain extent because the BoJ has been looking for wage hikes, and inflation to take hold more at the core level. We’ve seen some improvements in that area, but not enough. Headline inflation, with lower wage growth, is putting pressure on people. Now the new PM wants to introduce fiscal measures to offset this pain, and that could introduce more headline inflation. The BoJ, therefore, is likely looking at this hike to offset some of that.

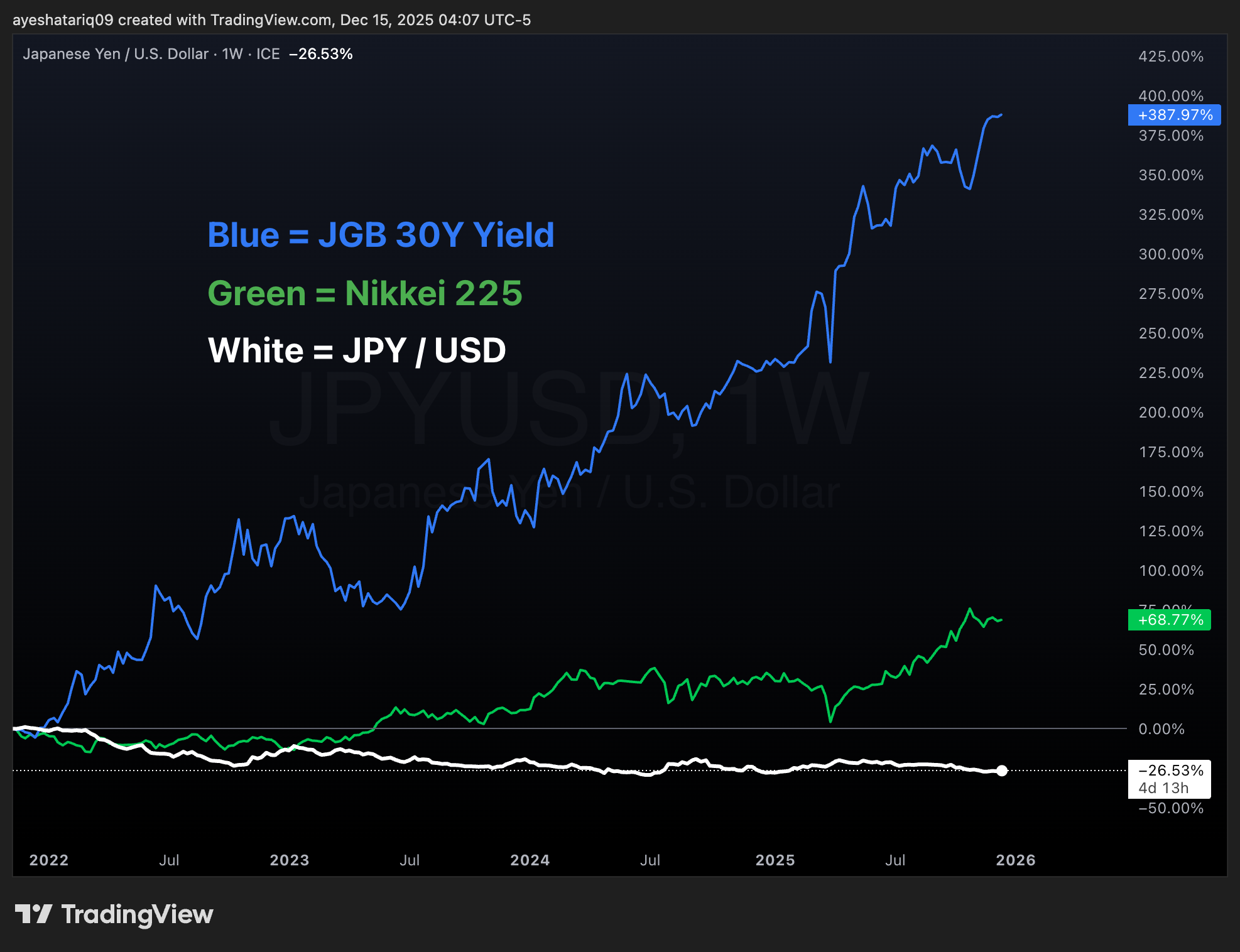

What’s the impact, though? The prospect of a hike has already pushed up long-end yields, and we’re seeing some demand and funds flow into that as well. This puts a dampener on equity markets and on the JPY. However, given the circumstances, both the Nikkei and, to some extent, the JPY have held up relatively well.

Bank of England - Cut by 25bps expected

Cut from 4% to 3.75%. In our previous article, we argued that the BoE would likely have to cut rates to offset weaker growth driven by fiscal consolidation, and the OBR’s lower growth forecast largely confirms that view, keeping a December cut firmly on the table.

We also continue to see the terminal rate slipping from 3.5% to 3.25%, though some analysts, including GS, are now discussing a lower 3% endpoint. While lower rates are supportive for equities, they are less constructive for the GBP. However, the latest budget did push up the borrowing requirements over the next year. Remember, more borrowing needs = more bond issuance = more supply = lower prices = higher yields.

ECB - Hold expected

Hold at 2%. The ECB looks set to leave rates unchanged, but the more important shift is in how policy is being framed. Recent data have been firmer than expected, with growth showing more resilience and inflation momentum proving stickier in the near term, even if it remains below target further out. That combination makes it harder to justify an easing bias, and the policy stance is increasingly being described as one that is already in a “good place.”

At the same time, markets have quietly moved from debating cuts to entertaining the possibility that the next move could eventually be a hike, even if that scenario sits far in the future and is still priced modestly. Policymakers are unlikely to endorse that idea outright, but they also cannot fully rule it out given recent upside surprises in growth.

Others:

Norges Bank: Hold at 4%

Riksbank: Hold at 1.75%

Volatility Pockets

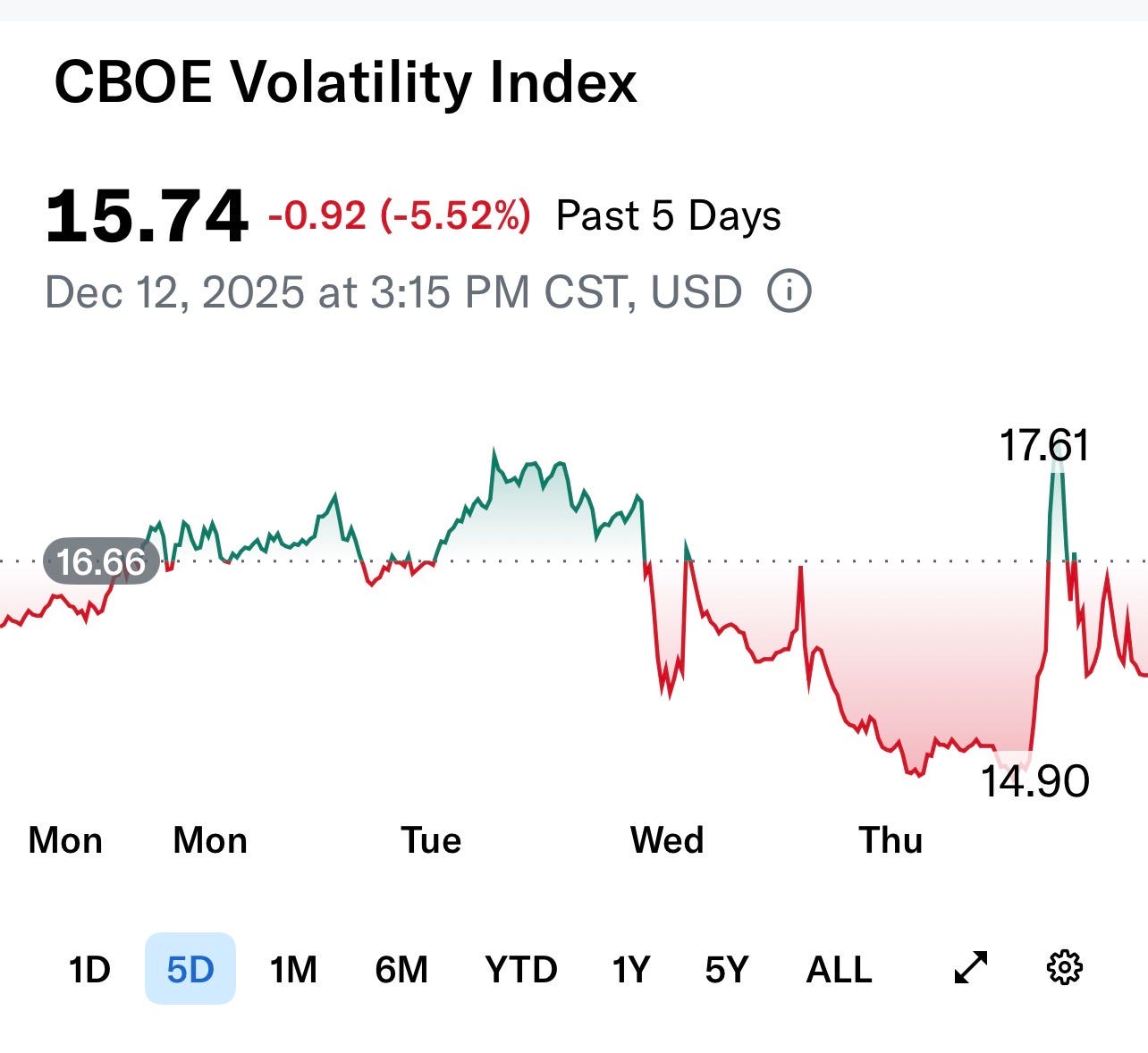

As expected, we saw volatility compress last Wednesday, after the Fed. However, we did see a spike later during the week because of the concerns surrounding Oracle, Broadcom, and the AI narrative. The market is not pleased with companies going from capex-lite to capex-heavy, and we saw Oracle walk back some of its plans after its earnings report. Still, the Vix remains below 20, and that keeps the optimism alive.

Themes to Watch

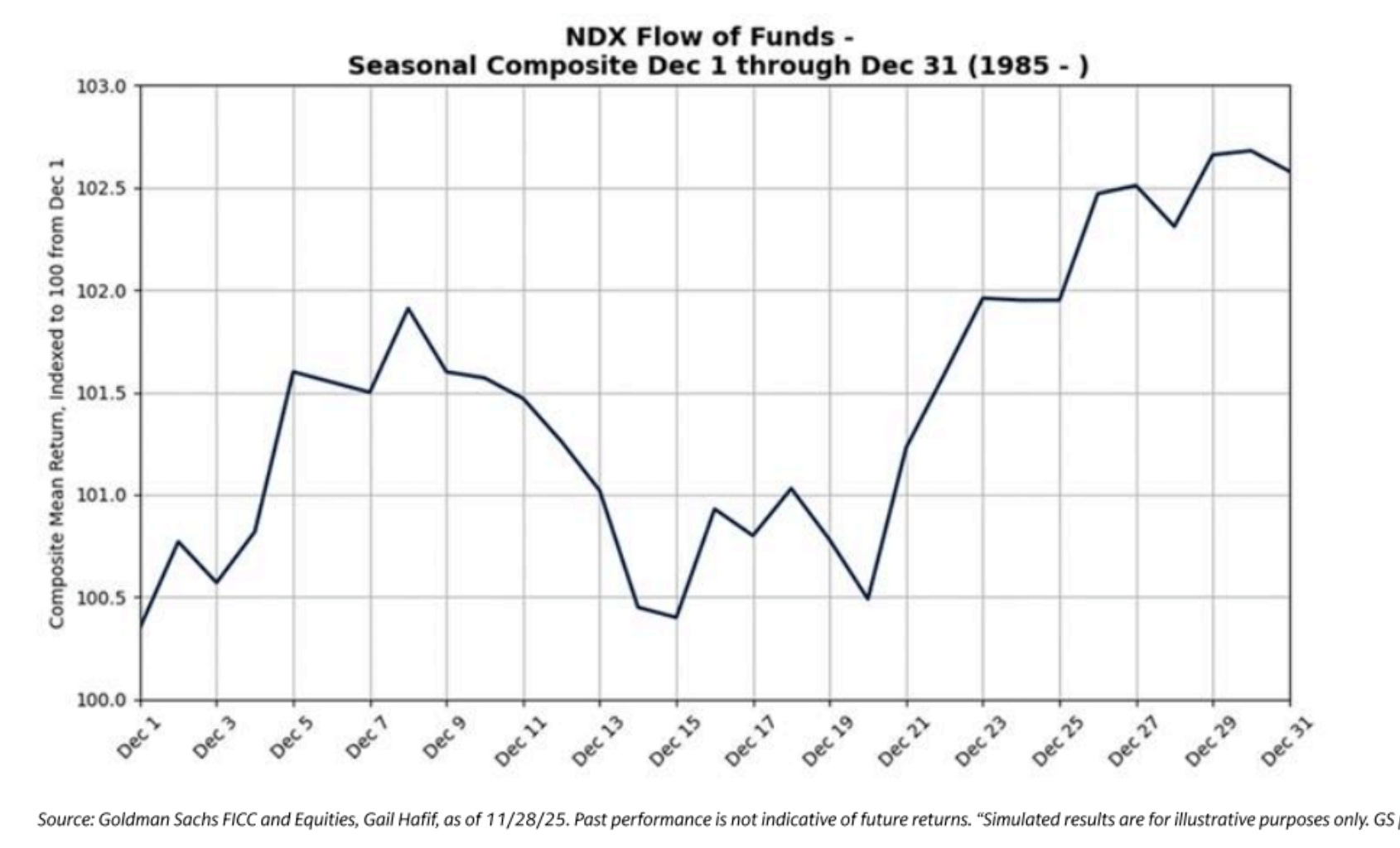

The Santa Rally

As we head into the second half of the year, let’s do a quick sanity check on seasonality and the expected Santa Rally.

Clearly, we’re still in the low period of the month, if we are to go by this chart. If the pattern holds, we’re likely to see the start of the rally around the 21st of December. Now, we do have other issues weighing on the market - the shakiness of the AI narrative, the spike in the yield curve. Nevertheless, the flows could overtake narratives, and we get a rally, but a slightly dampened one because of the negativity.

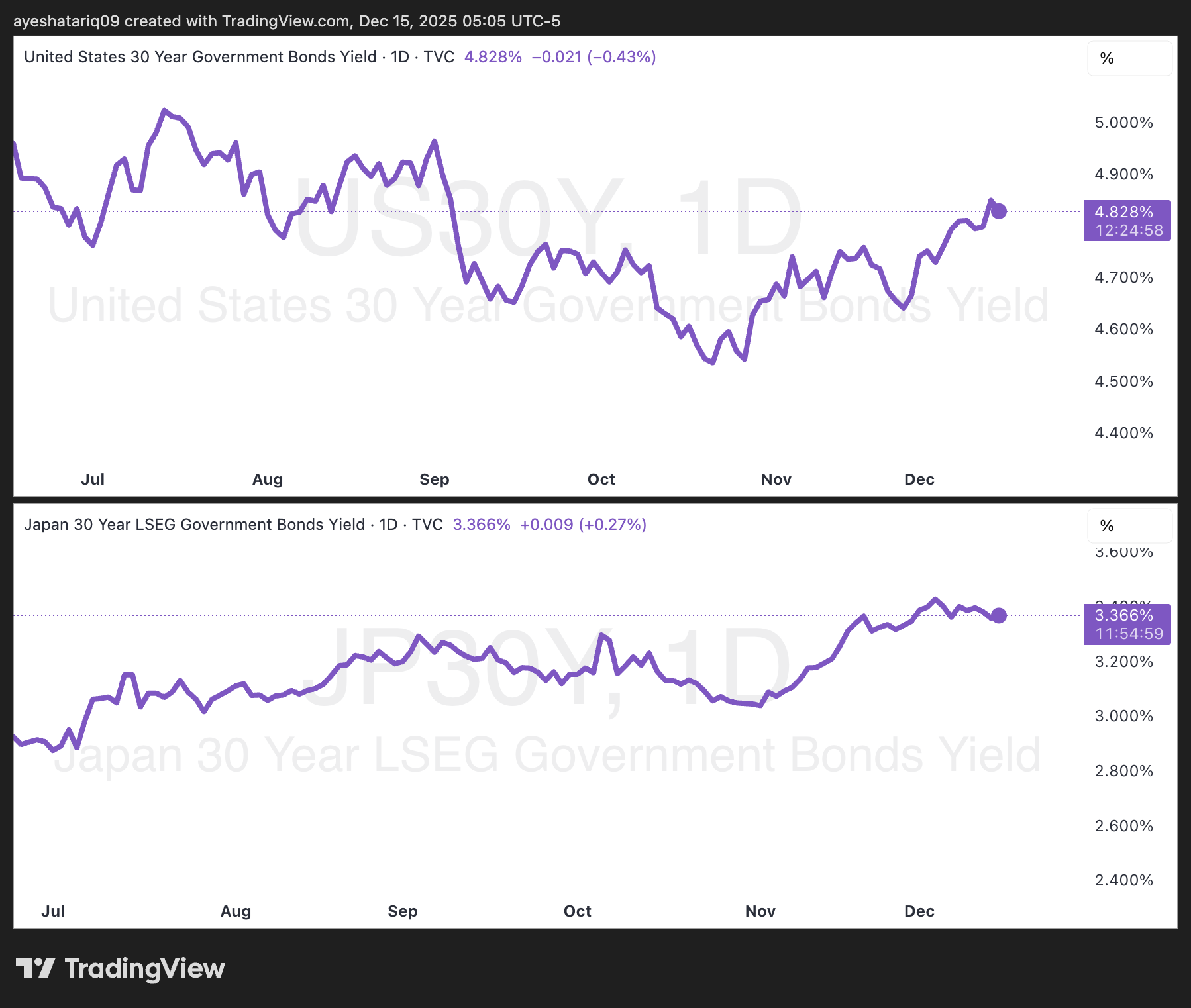

The Yield Curve

The US 10Y-2Y Yield Curve continues to spike, post the Fed’s less-than-hawkish meeting. I also think the balance sheet expansion is weighing on the front-end. As the Fed buys more T-Bills, it pushes yields lower, and on a relative basis, we’re seeing the curve steepen.

Then we have President Trump talking about one of the two Kevins - Hassett or Warsh - being the next Fed Chair, with the disclaimer that they will have to consult with the President on rates. Hassett is the more dovish choice, but I’m not sure either of them can resist Presidential pressure as Powell has. This could mean we get cuts sooner- and more-than-expected next year. Again, putting pressure on the 2Y.

Finally, on the long end, we have the US factors, but we also have Japan. The long-end for both countries tends to move in tandem, even if not perfectly aligned. So with the BoJ hiking, we could see another spike in the long-end in Japan, pushing up rates in the US as well.

Calendars

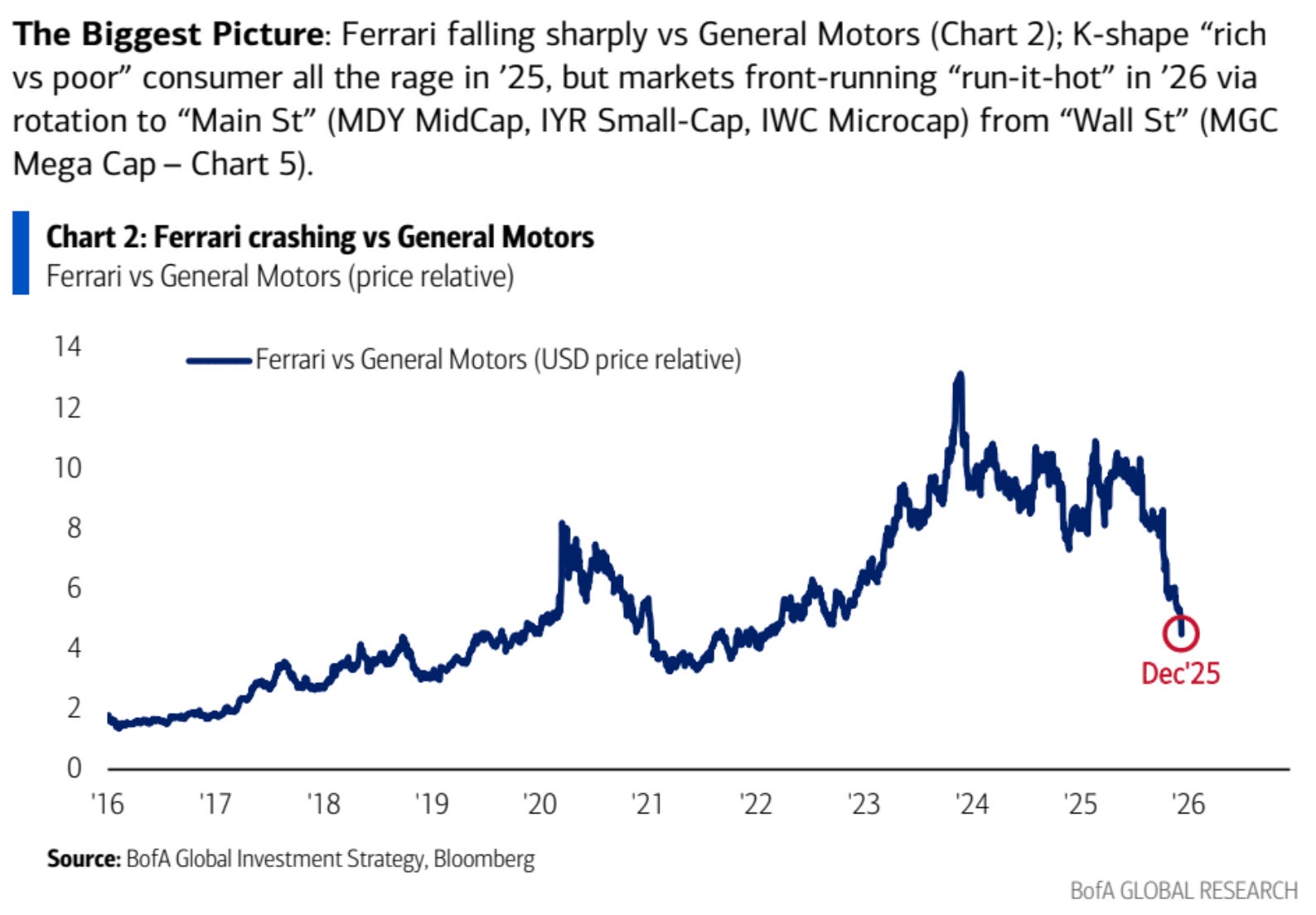

Chart of the Day - Run it Hot 2026 - BofA

This is an interesting chart from BofA comparing Ferrari to GM. Most of us know about the drastic rise of Ferrari’s stock over the past couple of years. That trend seems to be reversing, and BofA posits that this is a rotation from Wall St. to Main St. as easier conditions prevail.

Continue reading for our take on the small cap trade, market levels for the week, and the daily tactical watchlist, with new ideas added on Friday and today.