Rise and shine everyone.

Equity Markets are looking a little more stable this morning after yesterday’s shaky price action.

Data Center Concerns

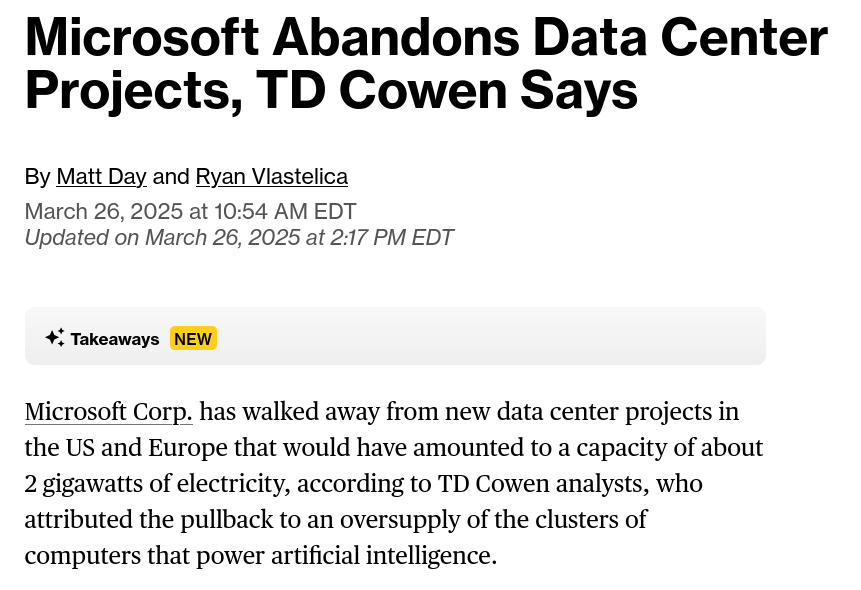

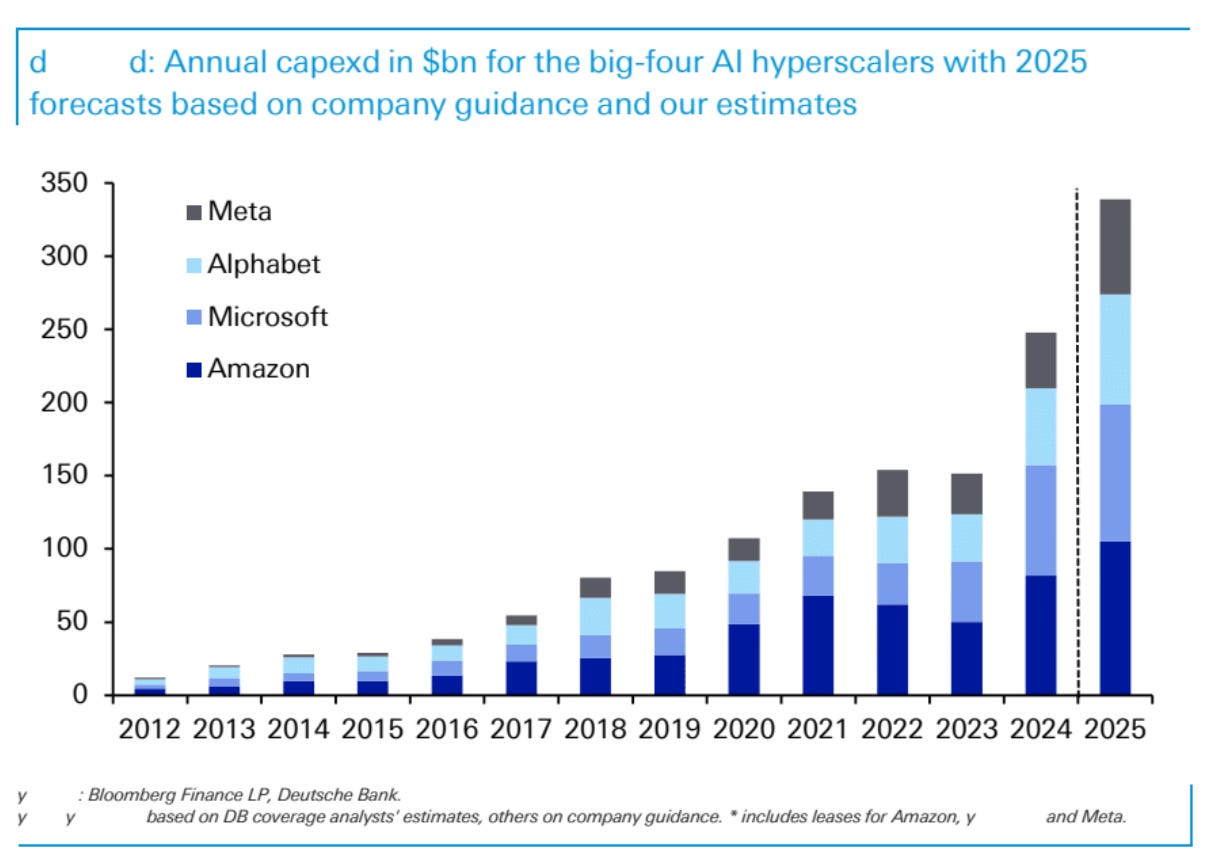

Firstly, Microsoft announced a cancellation of data center projects, and this comes of the heels of Alibaba’s warnings that there was already too much capex being spent on AI. This is definitely going to call into question all the large capital commitments by the various Mag 7 companies, and the sizable revenue projections from the likes of Nvidia.

We’re already hearing a shift in nomenclature from the “Magnificent 7” to the “Lagnificient 7” (BofA) and the “Maleficient 7” (GS).

Yesterday, we also saw the power stocks get hit because of this. In the last few months, electric power-related and, even to a certain extent, energy companies have been hanging their hat on the “AI data center expansion” story, and that got trampled on as well. There could be an opportunity here because for a few of these companies, the data center story may have been played up, but they also have other strong underlying demand forces. Something to keep an eye on.

Auto Tariffs

Then, there was the announcement of 25% tariffs on imported autos into the US. This has obviously impacted global markets - auto manufacturers in Europe, South Korea, and Japan are down. The President also threatened further tariffs on the EU and Canada if they work against the US.

• Nissan: -3%

• Honda: -3%

• Toyota: -3%

• Mitsubishi: -4%

• Subaru: -6%

• Hyundai (Korea): -4%

• Kia (Korea): -4%

• Tata Motors (India): -5.5%

• Porsche: -5.4%

• Mercedes-Benz: -4.8%

• BMW: -3.7%

• Volkswagen (VW): -2.9%

Japanese automakers with large cash reserves have already announced plans to shift production to the US from Canada and Mexico. While this will squeeze margins, it will increase prices in the US. The same is true of US automakers because they have been importing parts from Canada and Mexico as well. This is why we’re seeing a decline in stock prices for US automakers as well.

The political reaction was also interesting.

Canada’s newly appointed PM Carney condemned the tariffs as a "direct attack" on Canadian workers, acknowledging the harm while threatening retaliatory measures.

Brazil’s President Lula echoed similar sentiments, warning of counter-tariffs.

In Europe, EU Commission President Von der Leyen stated the bloc would assess the tariffs before deciding on a response. There’s discussion of counter tariffs of ~20%

Japan’s PM Ishiba took a more restrained approach, appealing for an exemption and emphasizing Japan’s role as a significant investor in the US.

Meanwhile, Trump suggested a potential "little reduction" in tariffs if China agrees to a TikTok deal in the US. This development coincided with a meeting between US Trade Envoy Greer and Chinese officials on trade and economic ties, though a former PBOC official warned that China should prepare for a possible trade war.

Not exactly the best Thursday morning so far!

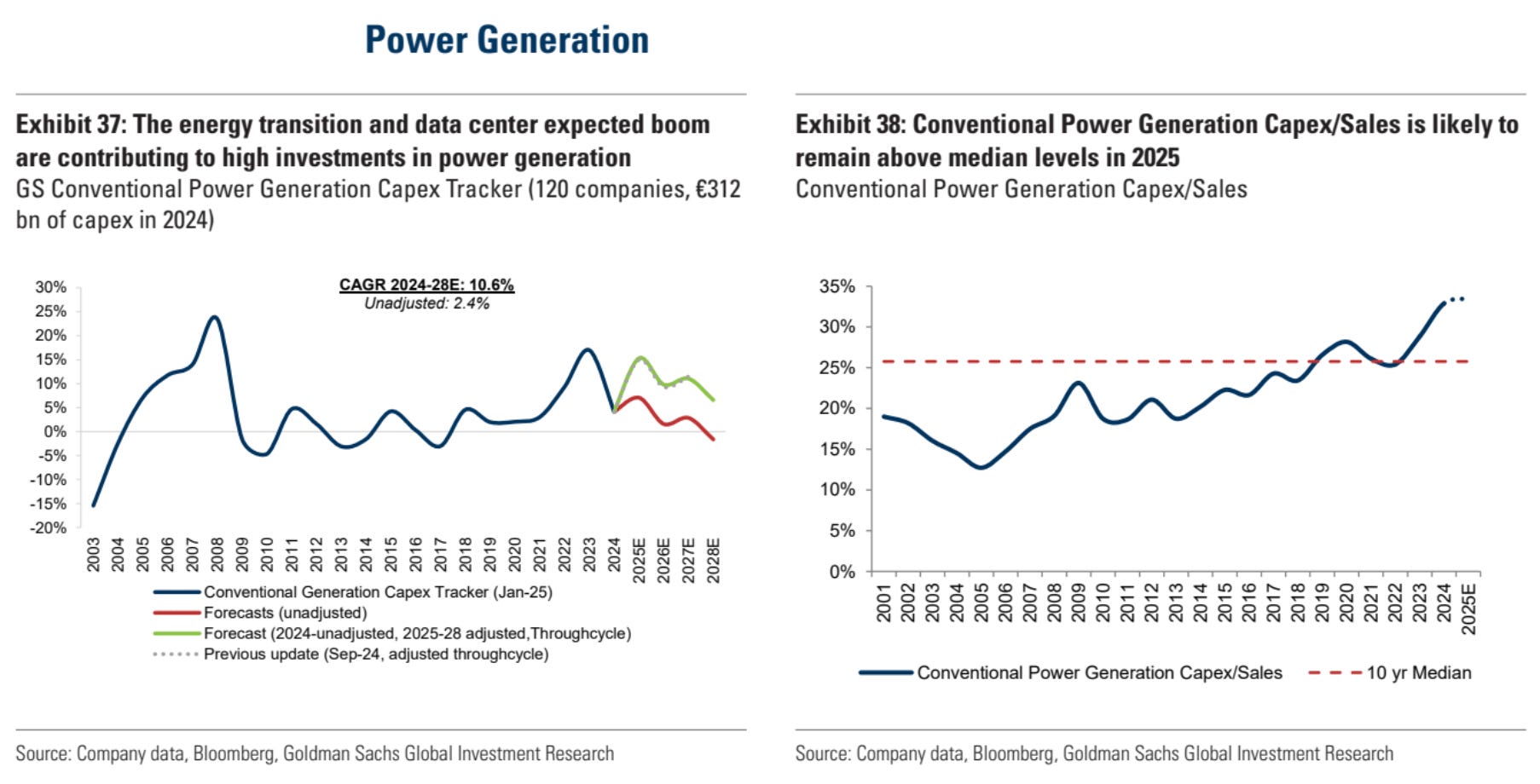

Chart of the Day - Power Under Pressure

This chart is from a GS publication on Jan 7, 2025, talking about the capex increase in the power sector. It goes back to what we said in the beginning, all these companies were starting to allocate capex for data centers, and this was supported by the new administration. What will happen to this allocation if there is a pullback in data center build?

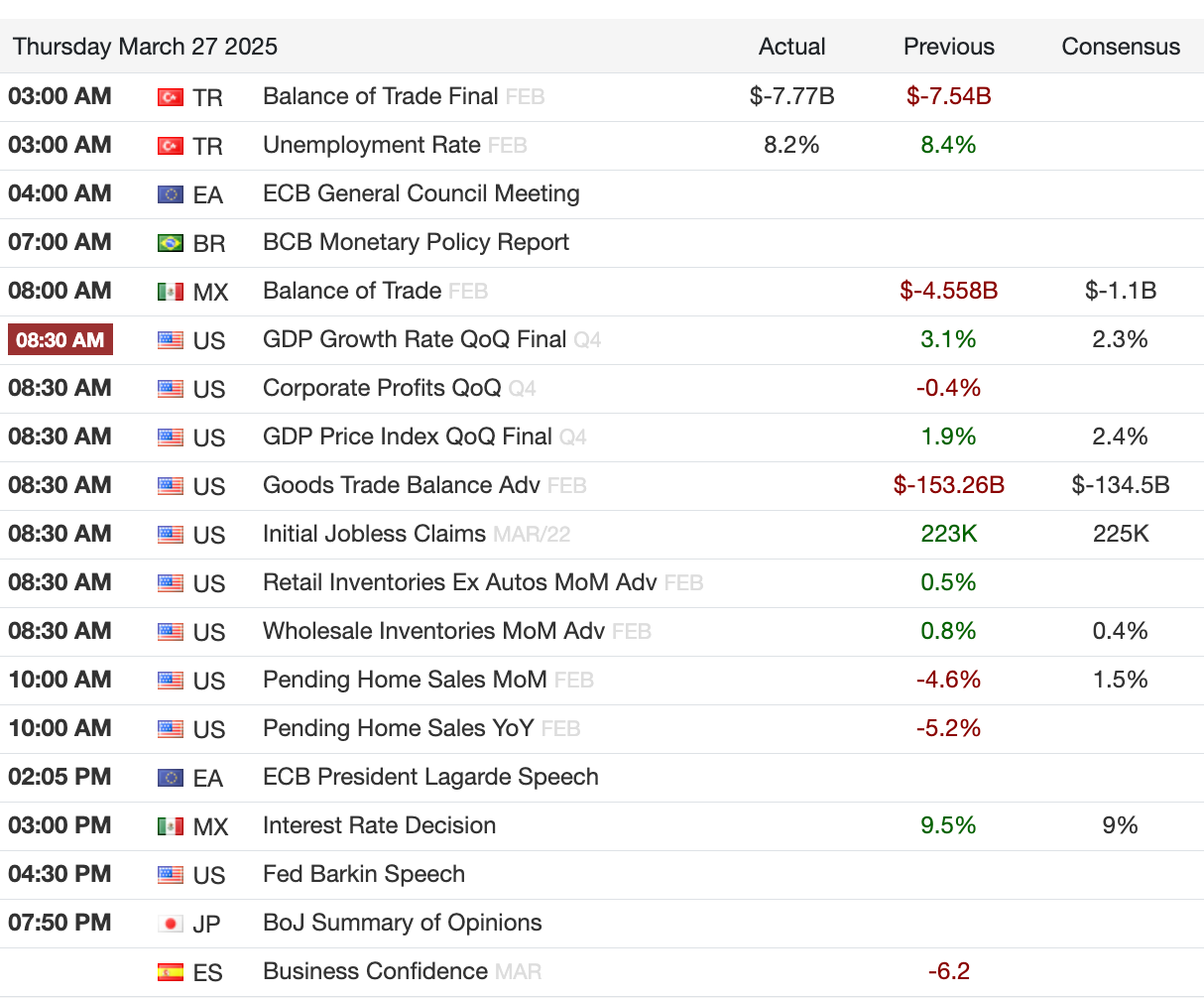

What We’re Watching Today

8:30 am ET - Final US GDP Growth numbers for Q4

After the Close - Lululemon earnings

Calendars

(news taken from Reuters, FT, Bloomberg; Calendar from Trading Economics)