Breakfast Bites: Powell’s Final Presser

Fed holds, four hyperscalers tonight, and Trump readies an extended blockade

Rise and shine everyone

Today is the heaviest day of the quarter, with three event clusters stacked on top of each other. Powell delivers his final FOMC press conference as Chair at 2:30pm ET, four hyperscalers report after the bell, carrying roughly 21% of S&P market cap, and WSJ reports Trump has told aides to prepare for an extended Strait of Hormuz blockade.

Morning Macro Briefing

The war is moving the wrong way again this morning. Trump rejected Iran’s latest proposal because it would have reopened Hormuz while parking the nuclear question for later, and WSJ reports he has now told aides to prepare for an extended blockade. Equities are reading the headline as “escalate to de-escalate,” but oil is taking it at face value with Brent near $113, and the only real positive on the supply side is a single Japan-linked supertanker through the Strait carrying 2 million barrels of Saudi crude.

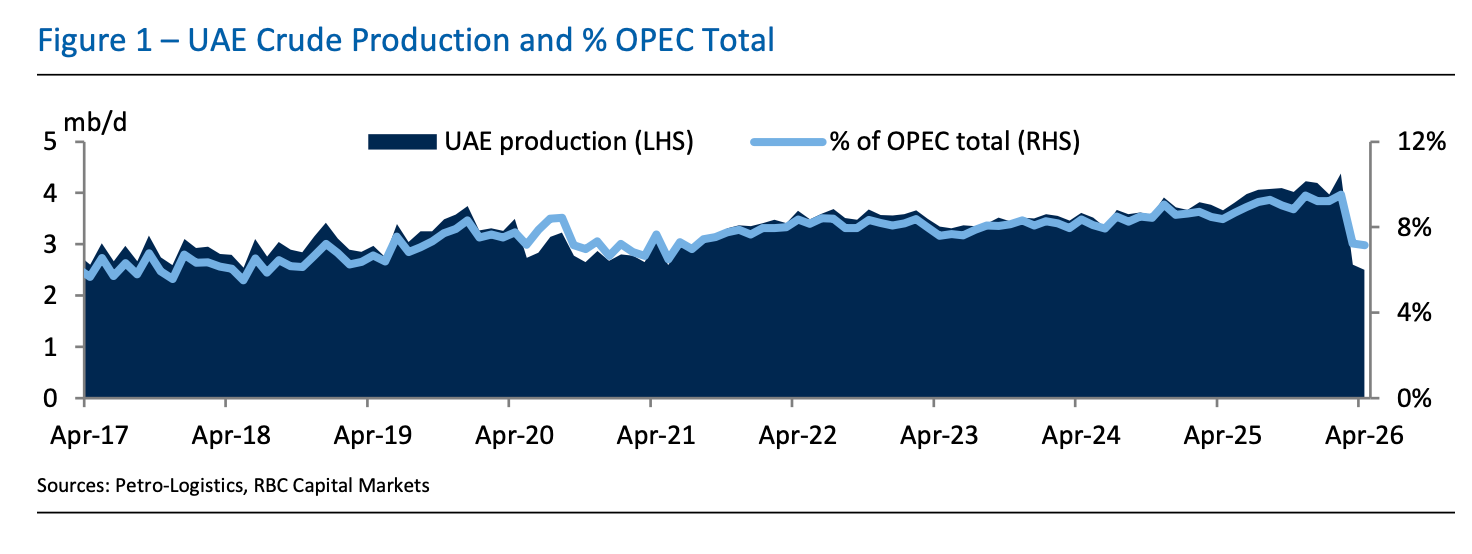

The UAE confirmed yesterday it will exit OPEC and OPEC+ on May 1, ending nearly six decades of membership and marking the largest structural change to the cartel since Qatar left in 2019. Current capacity sits at 4.85 million bpd with a 5 million bpd target for 2027, though Energy Minister Al Mazrouei said output could go to 6 million if the market demands it. Near-term price impact is muted with Hormuz still throttled, but the longer-term read is a meaningfully weaker OPEC once the Strait reopens.

ECB 1-year inflation expectations jumped to 4.0% against 2.8% consensus, and OIS briefly priced an additional 11bps of ECB hikes by year-end before fading. Aramco told some buyers it cannot finish repairs at the Juaymah LPG facility hit in late February, which means no May deliveries even if Hormuz opens. Germany’s net borrowing estimate ticked up over 8% for 2027, which keeps the fiscal dominance theme firmly in place.

Chart of the Day

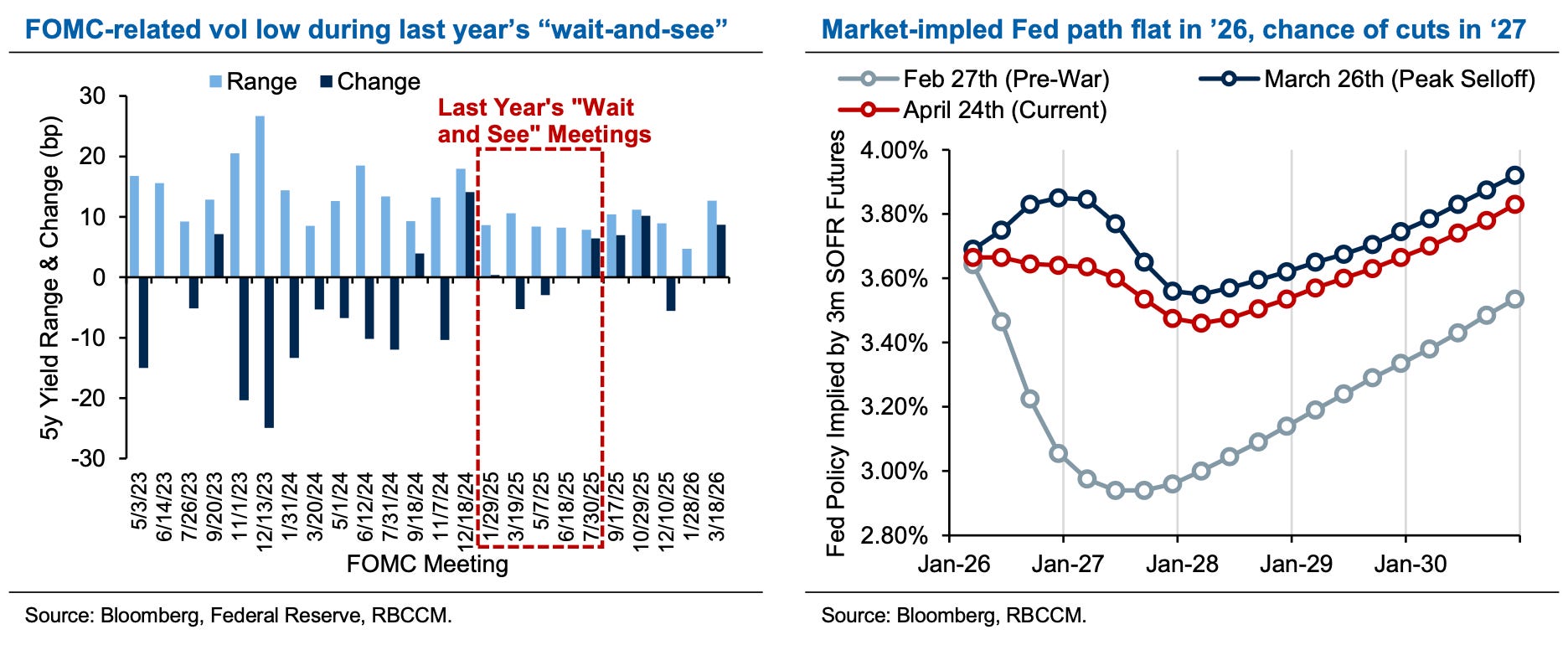

FOMC-related volatility was low during last year’s wait-and-see. Currently, the market implied Fed path is flat in 2026, i.e., no cuts, but 2027 shows cuts possibly resuming.

Fed Preview

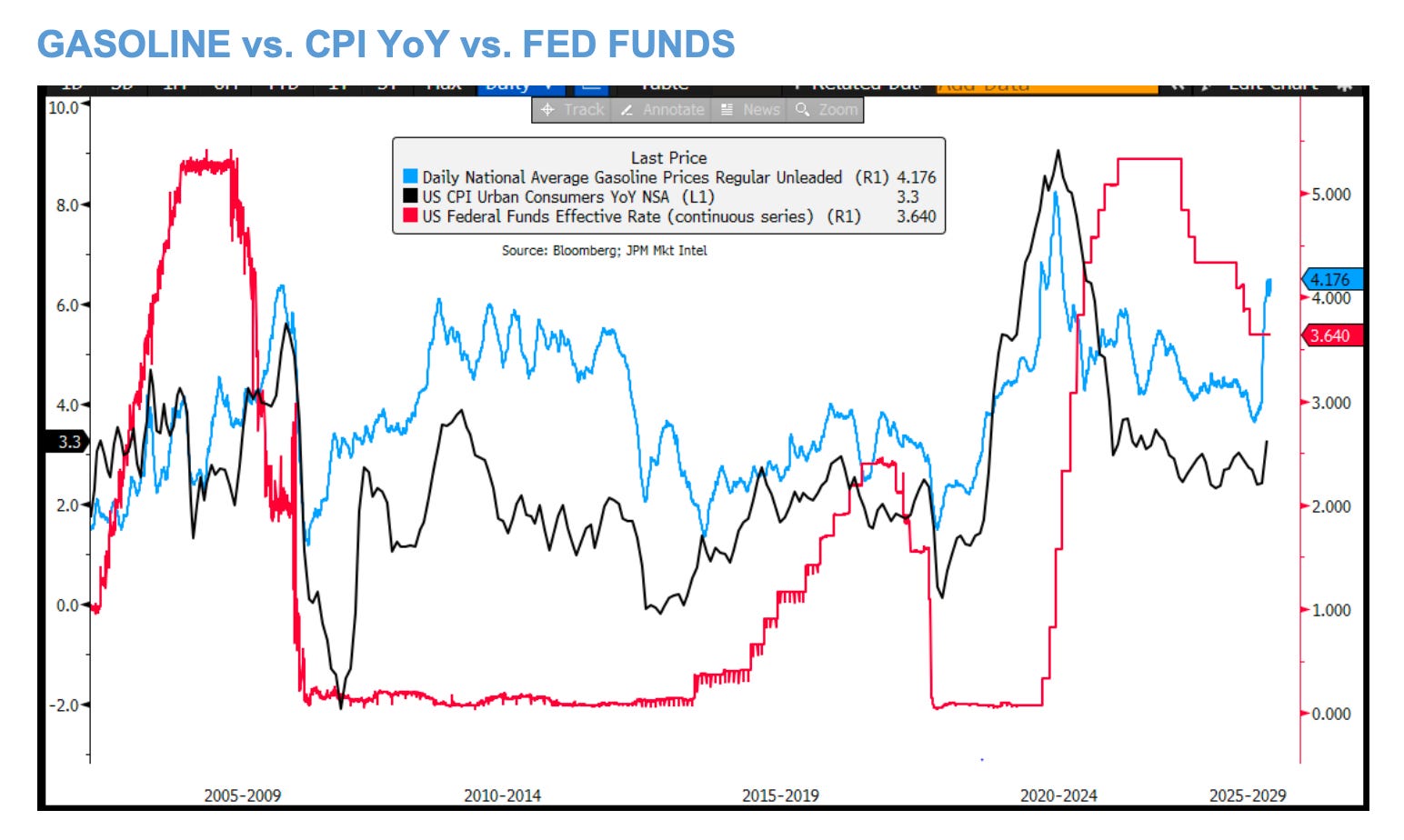

The decision itself is locked. We don’t expect the Fed to hold today, with a mention of Middle East uncertainty in the statement. GDP for the last two quarters has averaged roughly 1.5% GDP growth, and we may see softer language around growth. Inflation will continue to be the focus, and there is precedent for this. Gasoline prices have, historically, pulled up inflation.

The real event is the press conference. With Tillis clearing Warsh’s confirmation, today is almost certainly Powell’s last appearance behind the FOMC podium as Chair, and the open question is whether he stays on as Governor through 2028. Sticking around would break a precedent dating to 1948, and Tillis has already said he sees a “rational basis” for Powell to stay as long as the Fed renovation investigation remains active.

Powell took the chair in February 2018 and has been tested in ways no Fed leader has faced since Volcker, taking rates to zero in a weekend in March 2020, standing up emergency facilities through Covid, then walking back transitory and hiking 525bps into the fastest tightening cycle in 40 years, all while fighting the fiscal impulse. He absorbed sustained public pressure from a sitting president that no Chair before him has had to take on in modern memory, and he kept the institution’s independence intact through every round of it. Whatever you think of the individual calls along the way, the man showed up, and tonight is the last one. I, for one, will miss him!

This is, by far, the most historic speech delivered by Chair Jerome Powell - the 8-minute speech at Jackson Hole that rocked the market!

Market Prep

Futures are flat into the open with NDX leading on the post-market earnings setups. Cyclicals are leading defensives in pre-market with Energy, Industrials, and Materials at the front, and semis are catching a bid back after yesterday’s selloff.

Market structure is the variable that actually matters today. Nomura’s McElligott has QQQ $delta at the 99.8th percentile across strikes through the next six months and Mag7 3M call skew at the 92nd percentile, which together mean a real chunk of this rally is upside option chase rather than clean delta-one buying.

JPM is Tactically Bullish into the prints with Big Tech framed as the catalyst, but they flag the same concentration risk in beta and momentum and recommend hedges. Their Monetization Menu emphasizes Tech, Semis, South Korea, and Financials as buy-the-dip on Middle East insulation, while reducing exposure to airlines and homebuilders. Inflation is the named risk to the bull case, and the next clean test is the May 12 CPI print.

Tonight’s hyperscaler quad will be a test of AI monetization - show me the money! JPM positioning ranks the names from most to least crowded as AMZN, META, GOOG, AAPL, MSFT. The buyside estimates: AMZN AWS +29% to +30% versus +25% consensus, META Q1 revenue $57 billion plus, GOOGL Search +18% with Cloud high-50s to 60%, MSFT Azure +37% to +38% versus +35% consensus.

The OpenAI piece, however, is a cautionary tale for all of these companies. WSJ reported Monday that OpenAI missed FY25 internal targets on ChatGPT revenue and the 1 billion weekly user mark, with CFO Friar reportedly pushing back on the 2026 IPO timeline because revenue may not scale fast enough to cover compute commitments. The amended MSFT-OpenAI deal announced the same day makes the IP license non-exclusive through 2032 and lets OpenAI serve products on any cloud, which the JPM TMT desk reads as cleanly bullish AMZN and GOOGL on workload portability.

My Take

We say farewell to Chair Powell today, and whatever he says in the press conference will be parsed as much for what it signals to Warsh as what it tells markets. If he hints at staying on as Governor, the rates market will read that as a partial check on the next administration of the Fed. I’ve included a brief preview above, with the famous Jackson Hole speech from 2022.

The bigger near-term risk is not the Fed itself, it is four hyperscalers meeting positioning extremes with dealer gamma stacked on top. A clean print plus capex tied to committed AI demand runs us higher and pulls CTAs back in.

Oil is the macro pin, and the asymmetry is to the upside. Aramco can’t repair Juaymah, the UAE is structurally bearish for 2027 but supportive now, and Trump is openly preparing for an extended blockade.

I have included a new name in our Tactical Watchlist below (behind the paywall) - personally, I’ve liked this company for a while, and I’d like to buy this dip.