Breakfast Bites: Potential Impacts of Tariff Ruling

A detailed look at the tariff situation; Busy week ahead with State of the Union Address, NVDA, HD and Software earnings

Rise and shine everyone

The only thing anyone cares about this morning is US Tariffs. After the Supreme Court ruled against the Trump Tariffs on Friday, markets have been hit by uncertainty about what’s next. For the moment, the administration has levied the 15% tariff (under Section 122), which can continue for 150 days, until they decide what steps to take next.

The US has also asked trading partners to stick to the agreements that have already been signed, even though they were technically signed under the IEEPA construct. But countries have their own ideas.

The major events for the week will be President Trump’s State of the Union Address on Tuesday, Home Depot Earnings on Tuesday, and Nvidia, Salesforce, Snowflake reporting on Wednesday.

Morning Macro Briefing

Back in January, when we expected the ruling to come out, we discussed a few of the other options that the administration may have for continuing their tariff policies. Here’s a quick recap:

Section 122 of the Trade Act of 1974: 15% tariff that can continue for 150 days and then will require Congressional approval. This requires no formal investigation or process.

Section 301 of the Trade Act of 1974: This is in response to unfair trade practices. It requires investigations, so tariffs can only be levied after a few months. However, there is no limit on the level of tariffs or the duration. China is already under investigation for not abiding by the agreements set forth during the President’s first term. This could very well be used against China again.

Section 232 of the Trade Expansion Act of 1962: This allows for tariffs based on “National Security” concerns. Already used for tariffs on steel, aluminum, autos, copper, and furniture.

Section 338 of the Trade Act of 1930: A 50% tariff on imports from countries that discriminate against the US. This limits the amount of tariffs but does not require investigation.

We don’t know what the tariffs will be, and we have no definitive course of action at the moment. All we know is that there will be retaliation against this ruling from the administration.

So what are the potential impacts now of the tariff ruling?

I’m just going to run through these as I think the situation is still fluid, and there’s still much to be confirmed.

China gains some bargaining power. President Trump will be visiting China soon, and it’s likely that this ruling could be used to gain an upper hand in negotiations, particularly with regard to China purchasing soybeans and allowing the export of rare earths.

However, the US has other options that it can use, so we could also potentially see some hoarding of Chinese goods before a final decision is made.

Chinese ETFs are trading higher in the pre-market. Markets in Mainland China will open tomorrow, and then the impact will be clearer.

Other countries may take a wait-and-see approach. Many of the bilateral deals were signed under the IEEPA, and if every country received the same universal tariffs, it stands to reason that there is no competitive advantage or disadvantage. Everyone is equally penalized. So countries may choose to accept the universal 15%.

This means countries may not go ahead with their deals of purchasing Boeing aircrafts, LNG, and soybeans from the US. (WATCH BA TODAY).

Countries where the negotiated tariff is lower than 15% will create trouble, e.g, Europe. Europe is refusing to make further concessions, choosing instead to monitor how the US pivots its tariff policy. Although the overarching rate is set at 15%, the EU wants to maintain the previously agreed exemptions.

US companies may not get a refund. There are two issues here. First, under some of the regulations, companies need to file for a potential refund ahead of the ruling. Second, many of the companies that have actually absorbed the tariffs are not direct importers and therefore, they are not entitled to a refund from the US government. The fact of the matter is that any of the tariff burden that’s been passed on by the actual importer, whether to distributors or the end consumer, has already done its job. The $175B in tariff revenues that’s up for debate may not actually be!

Friday also brought us a number of macro releases. US GDP growth came in lower than expected at +1.4% in 4Q2025 vs the consensus of +3% (+4.4% previous).

Now, this would ordinarily raise some eyebrows, but some of the decline was on account of the reduced government spending because of the partial government shutdown. This should adjust in 1Q2026.

Consumer and business spending continues to remain robust, and we saw some of that in the inflation numbers. PCE and core PCE came in marginally hotter than expected, by 0.1% across the board for the YoY numbers.

Add this to the trade and tariff uncertainty, and Fed rate cuts are likely to be off the table for a while. Fed speakers are also talking about putting hikes back on the table if inflation continues to move higher.

So things at the Fed are not going according to plan. We already expect long-end US Treasury yields to rise. Chances are, we now see the entire yield curve shift upwards.

None of this bodes well for the US markets and the US consumer.

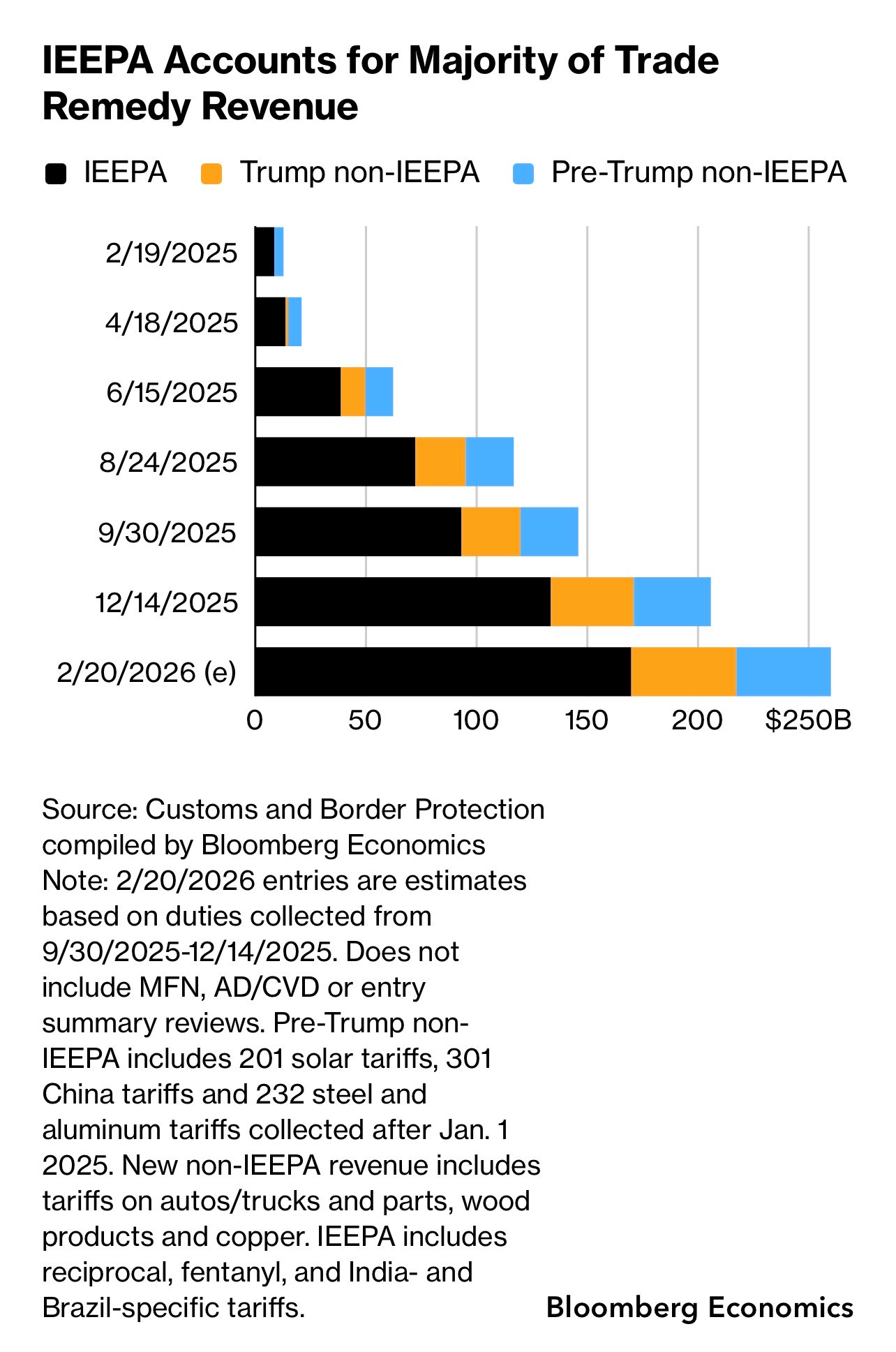

Chart of the Day

While we don’t know what happens with the refunds, here’s an interesting chart. The IEEPA tariffs account for the majority of trade remedy revenue…. so the impact is not minimal. IEEPA codes will be closed out tomorrow.

Calendars

Market Prep

Interesting comments from GS…

“the quantum of selling/shorting/ de-grossing/de-netting is more suggestive of a VIX at 35 vs a VIX at +/- 19.”

Be careful what you wish for…

Now we’ve got trade and tariff uncertainty thrown into the mix once again, and markets will likely de-gross further.

On the plus side, however, investors have already taken down a significant level of risks, and this means the likelihood of “panic selling” will be lower.

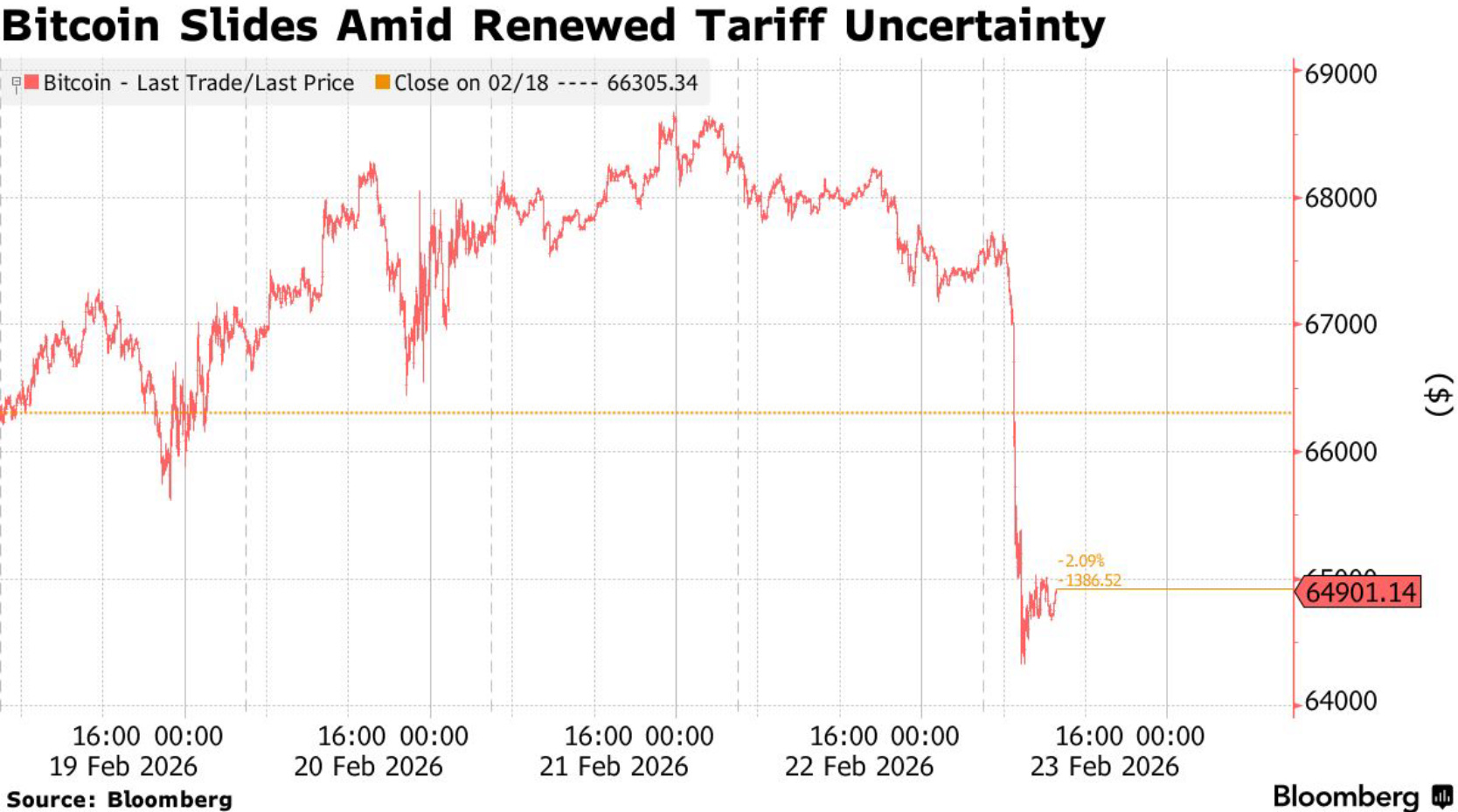

But that’s not the case across the board. Crypto seems to be reflecting extreme risk off, while gold and silver once again become the safe haven.

Bitcoin dipped below $65,000 earlier in the day before recovering slightly. My take is that the Russell 2000 also gets hit more than large caps because of higher yields, more tariff burden, and fewer reasons to get a refund.

Coming up also during the week is NVDA earnings, which always brings some volatility to the market. Particularly after all the narratives in the past few weeks, the markets will surely be looking at NVDA as a bellwether for AI.

CTA / Trend Following Flows (from BofA)

US Equity unwinds with negative price action. Nasdaq is likely to be the fastest to fall.

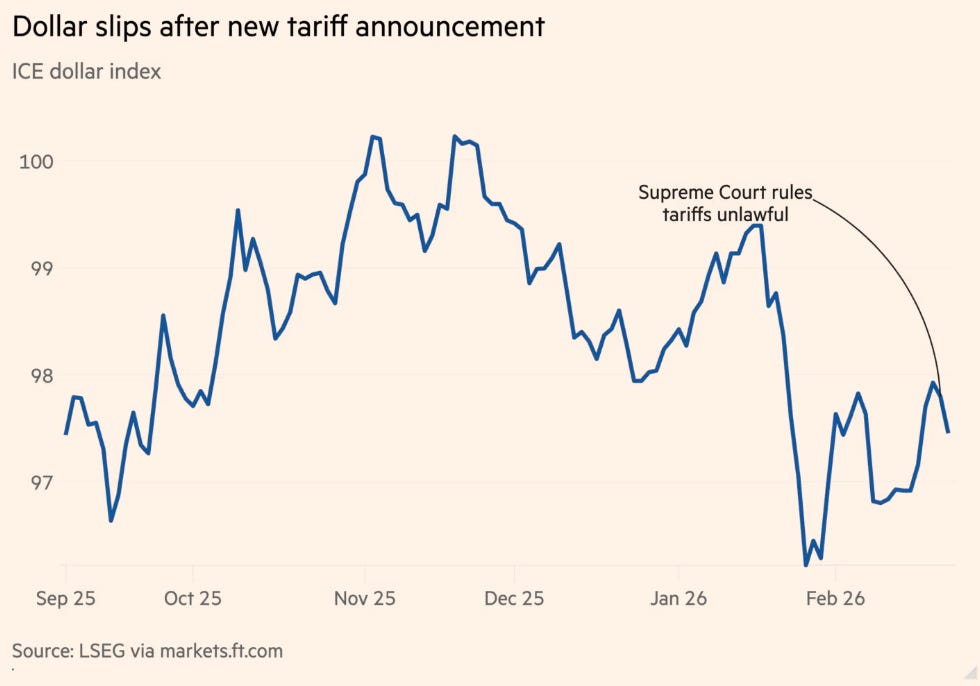

USD short positioning has been extreme so we may get some unwind there (i.e., buying) despite the fall we see this morning

UST Futures prices could increase despite the view of higher yields, reversing this view

Trend followers are still long gold, and were buying soybean complex futures.

My Take

The Supreme Court just threw a massive wrench in the works, leaving the US administration to pivot toward a 15% tariff. We’ve discussed what the potential impacts could be for the market, but this still remains fluid. Between countries not willing to honor their previous commitments, and the mess surrounding those $175B in potential tariff refunds, we’re looking at a total “wait-and-see” standoff for global trade.

Toss in a “hot” PCE print and a shutdown-stunted GDP, and suddenly those Fed rate cuts are off the table.

On the market side, we see a clear risk-off stance, although the likelihood of panic selling is lower given that many investors have already de-grossed over the last few weeks.

Keep an eye on the State of the Union address from President Trump tomorrow, and earnings from Home Depot on Tuesday and Nvidia & software companies on Wednesday.