Breakfast Bites: Post-Fed Calm, Rotation in Markets

Fed news digested, markets are seeing a rotation; Adding new names to Tactical Watchlist on this rotation

Rise and shine everyone

Happy Friday! My apologies that I missed putting out the Breakfast Bites yesterday because I had to attend to personal matters. But let’s get back to it.

Morning Macro Briefing

Clearly, the market has digested the Fed’s news, and the narrative circulating is that the Fed wasn’t as hawkish as expected. Despite projecting only one cut for next year, the market seems to be more encouraged about the T-Bill purchases. The Fed has decided to purchase $40B in T-Bills per month to maintain ample reserves. This is not unusual, and T-Bills are preferred because they don’t have a big impact on the yield curve, or at least they shouldn’t.

Now, while the Fed is not signaling this as a stimulus policy measure, we know that liquidity has been running low, and that needs to be managed. Introducing liquidity into the market is bound to have some what of a stimulative effect.

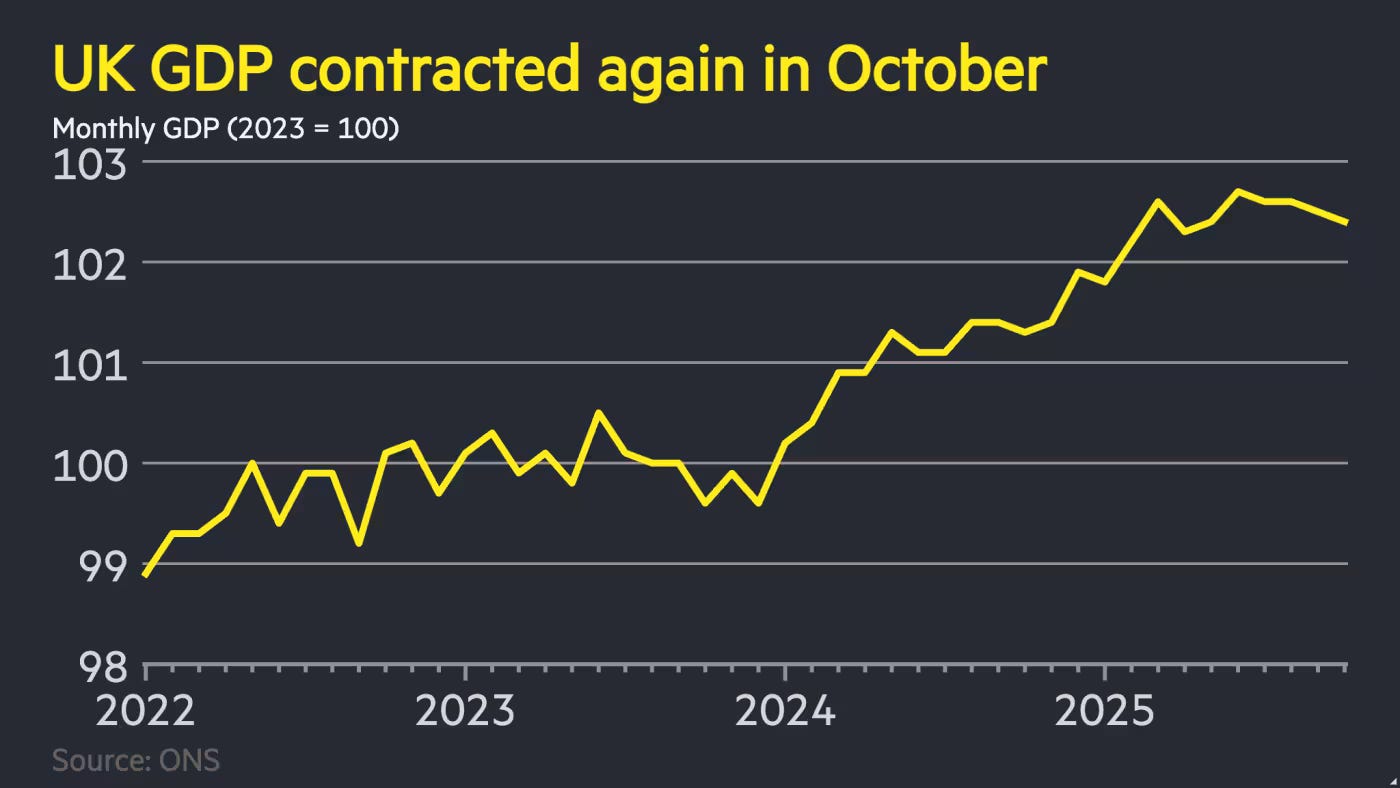

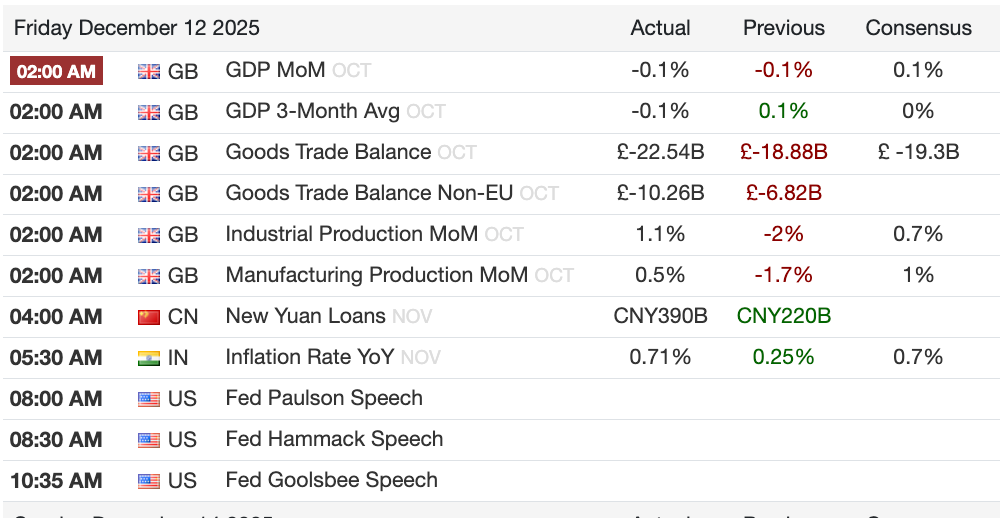

In international markets, the UK saw disappointing GDP growth numbers. The UK economy unexpectedly contracted 0.1% in October, showing us how months of Budget leaks and uncertainty led many businesses to pause and wait for clarity.

Activity slowed across most parts of the economy, and growth has now gone nowhere since May, leaving momentum weak as we head toward year-end. This backdrop strengthens the case for a Bank of England rate cut next week, something we flagged earlier in our UK analysis, and markets are already largely priced for it.

Turning to China, the CEWC (Central Economic Work Conference) was held and the news overnight is that there is a clear bias toward further fiscal expansion. Authorities reiterated they will maintain necessary fiscal deficits and keep RRR and interest-rate cuts in play, acknowledging that the economy still faces meaningful challenges.

This came in the face of Credit Data from China:

New yuan loans: CNY 390 billion in November, up from CNY 220 billion in October but below CNY 580 billion a year ago and CNY 500 billion expected.

Total social financing: CNY 2,490 billion, up from CNY 810 billion in October and slightly above last year.

Loan growth: 6.4%, a fresh low, down from 6.5% previously and 7.7% a year ago.

Finally, China also announced the rollout of a broad licensing system for steel exports from Jan. 1, requiring permits for around 300 products amid record shipment volumes and rising trade tensions. The move is likely aimed at curbing tax-related practices and managing sentiment, with limited impact on export volumes over the medium term as overcapacity and weak domestic demand continue to push steel into global markets.

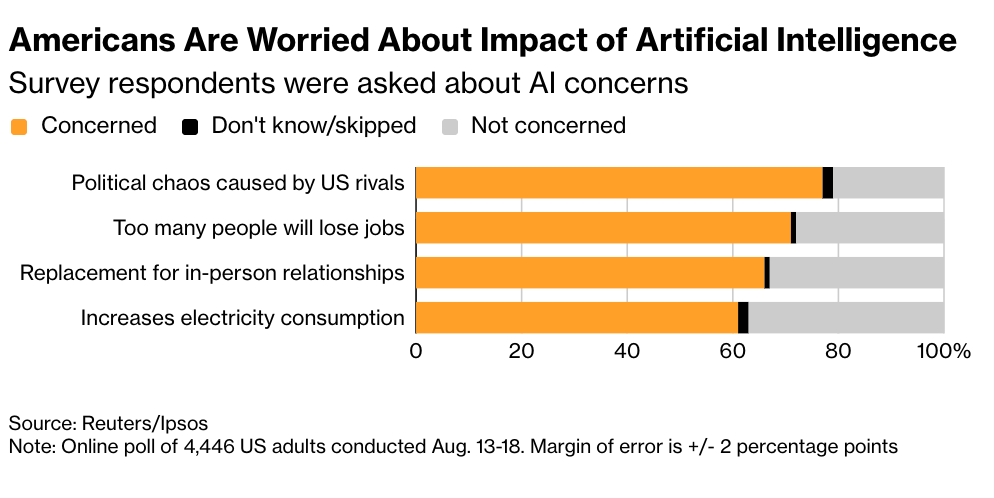

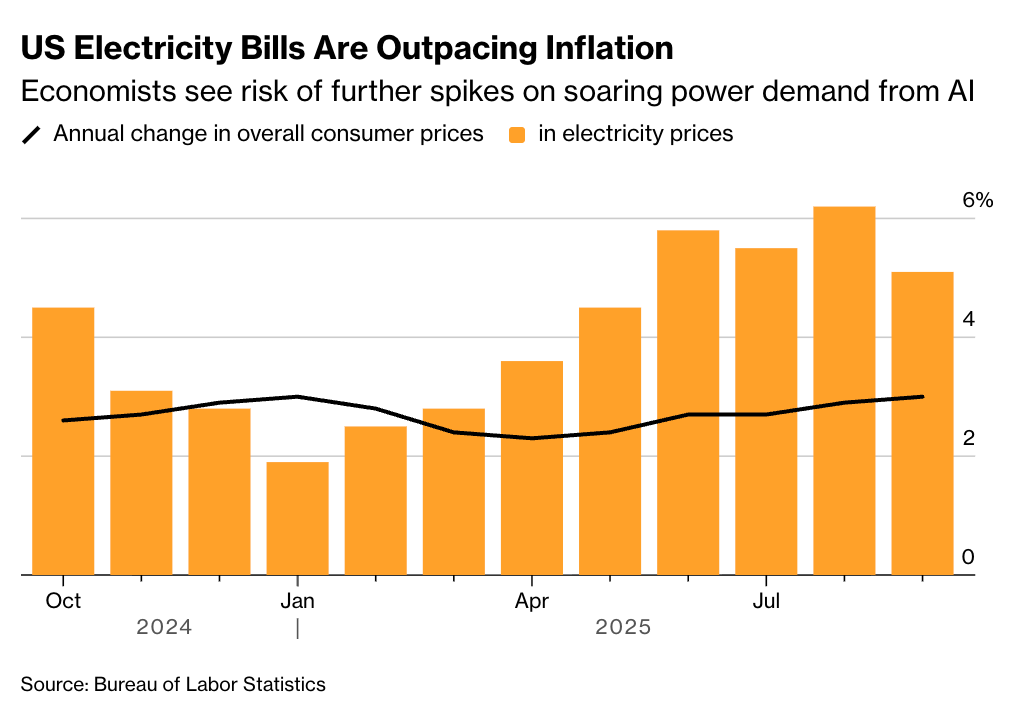

Chart of the Day - People worry about AI

Americans are increasingly worried that AI could raise living costs and threaten job security, with growing concern that productivity gains may not translate into broad-based benefits for workers.

At the same time, surging power demand from data centers is starting to show up in higher electricity bills, turning energy affordability into a political flashpoint as households feel the cost of the AI buildout directly.

Source: Bloomberg

Calendars

Market Prep

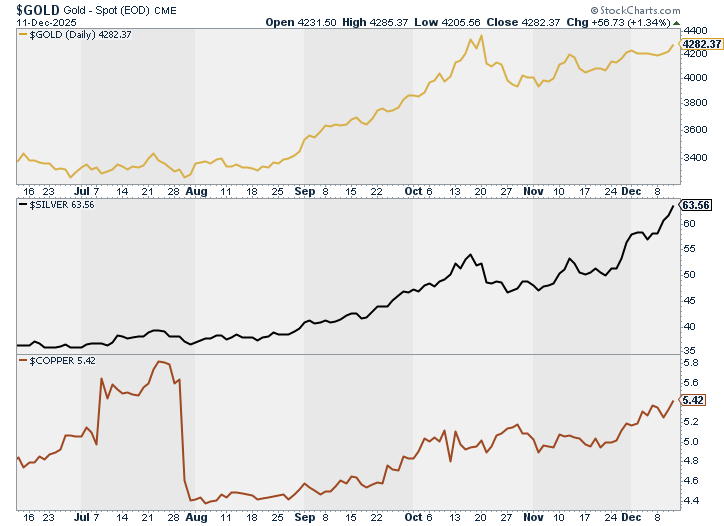

It’s almost as if the market was waiting for the event risk of the Fed to pass to have the all-clear signal to move higher. As discussed under the macro section, it’s likely that the T-Bill purchases are being seen as having a more immediate effect, compared to longer-term thoughts of one cut next year.

Most market participants already think that the President will soon announce his candidate, who will be far more dovish. Alongside higher growth expectations, the market could be discounting the liquidity from the Fed, and possibly an easier-than-projected environment for 2026.

We can see this in yesterday’s commodity prices.