Breakfast Bites: Payrolls Into the Flush

Ceasefire cracks, a momentum unwind leaves AI exposed, and the April jobs number drops at 8:30.

Rise and shine everyone

The US-Iran ceasefire is apparently still in place but attacks continue. Israel struck Lebanon and Iran struck the UAE. Overnight, US Central Command confirmed it had struck Iranian military facilities after what it described as an unprovoked attack on three American destroyers in the Strait of Hormuz involving missiles, drones, and small boats. Iran said it had retaliated for a US strike on an Iranian oil tanker attempting to cross the American blockade. Trump called the Iranian actions a “trifle,” insisted the ceasefire was holding, and told Tehran it “better sign their agreement fast” — or Iran would become, in his words, “one big glow.”

US equity futures are up 0.4-0.5% and pointing toward record levels, while Asia sold off broadly and Europe opened lower by around 0.9%. The absence of any safe-haven bid in Treasuries tells you that this is not risk off. Brent is back above $101. An unverified Al Arabiya post circulating overnight suggested an imminent Strait breakthrough, crude dropped a few dollars on it and Bitcoin briefly retook $82k, but the rumor came to nothing once the Pentagon confirmed the strikes. The same account posted nearly identical language on Thursday. Signal quality here is very low, and yet the market keeps pricing a deal as base case.

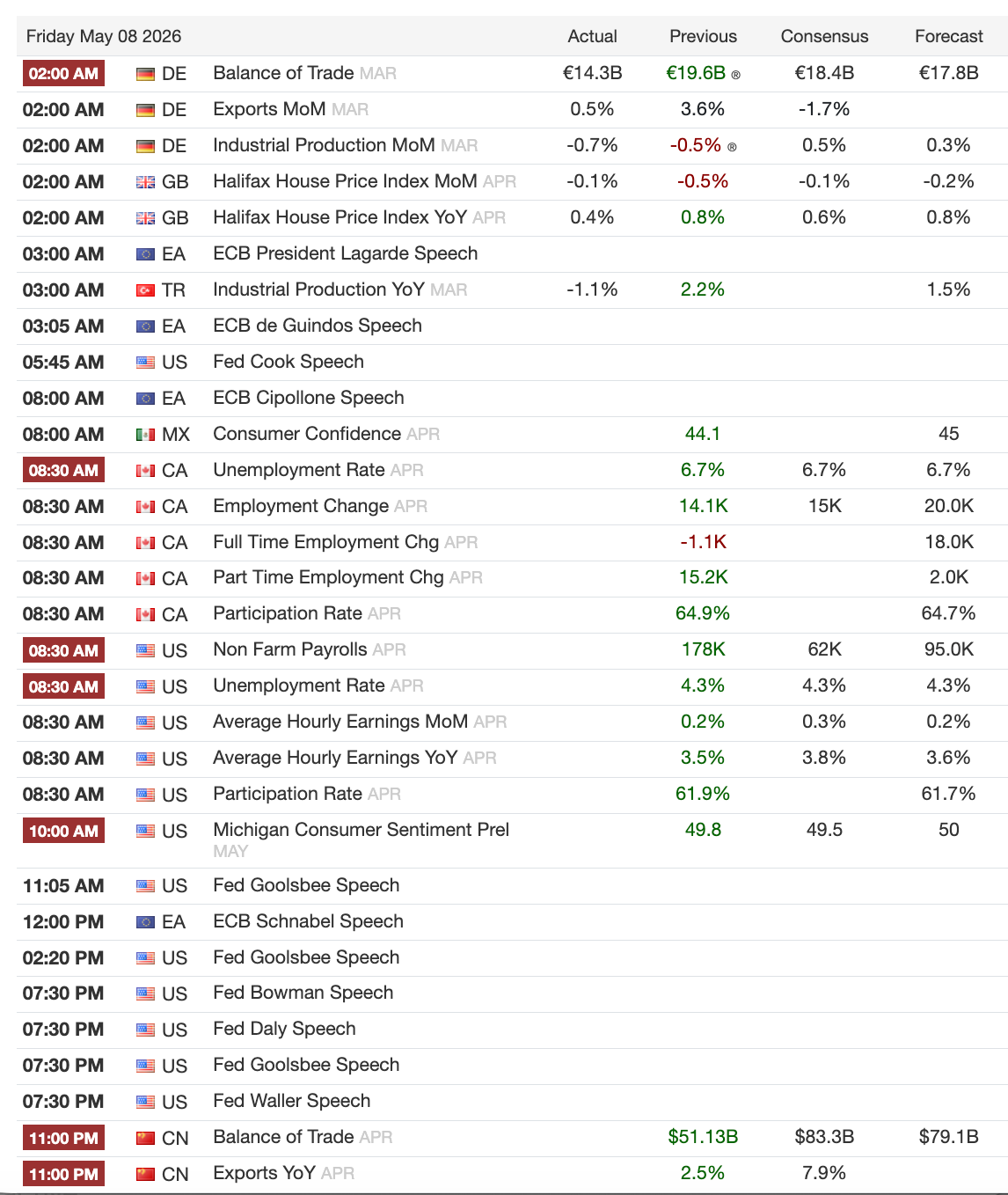

Today is Jobs Friday in the US. The data drops at 8:30 ET into a tape that spent Thursday digesting a violent momentum unwind, with the SPX at record levels, positioning maxed, and Iran headlines resetting sentiment every few hours.

Morning Macro Briefing

UK local elections have delivered a result that will rattle gilts through the session. Reform has taken north of 390 council seats, Labour and Conservatives each sit around 250, Liberal Democrats near 220. Reports are already circulating that Ed Miliband has urged PM Starmer to set out a resignation timeline, and Labour MPs are openly calling for his departure. ING has cautioned that sterling carries no political risk premium and is therefore vulnerable, particularly against the euro. The 30-year gilt yield hit a 28-year high of 5.79% this week. This usually leads to high volatility in the stock market as capital migrates out of equities and into fixed income.

President Trump confirmed a July 4th deadline for the EU to meet the terms of the trade agreement before he raises tariffs, having threatened last week to lift the auto tariff from 15% to 25%. Von der Leyen described a “good call” and said progress was being made. Separately, the Court of International Trade ruled Trump’s Section 122 “plan B” tariff authority illegal. The immediate market read is legally negative but operationally muted: the injunction is plaintiff-specific, duties likely continue collecting during appeal, and the tariffs expire July 24 anyway. The more important signal is strategic: courts are closing off the White House’s improvised tariff authorities faster than they are needed.

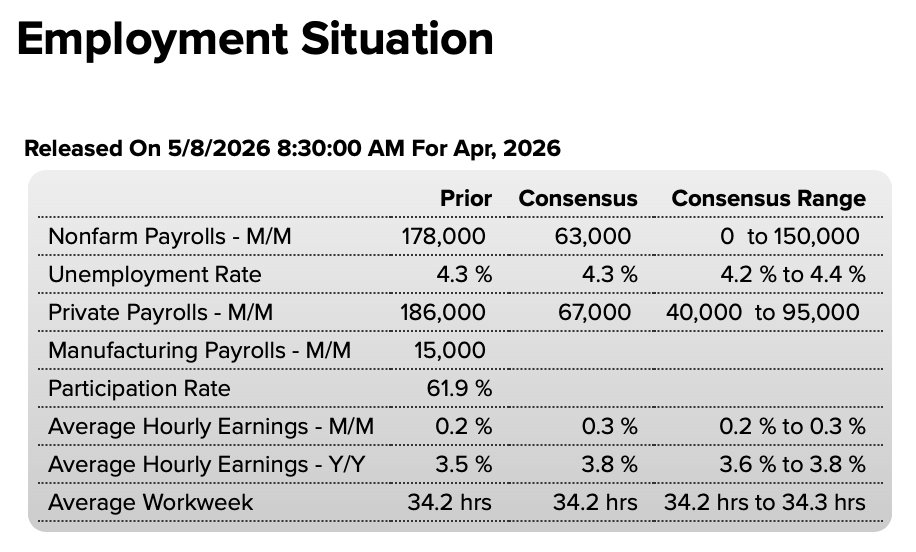

US Employment Report Preview

The April payrolls report drops at 8:30 ET and the street is braced for a soft number.

The case for upside comes mainly from the higher-frequency data. Claims were benign through the survey week, with initial claims averaging 211k in the April payroll month, unchanged from March. BofA estimates the weekly ADP data will imply April private sector growth of 120-160k versus 60k in March. The case for a softer print is narrower with a net 5k decline in government payrolls, an ongoing federal hiring freeze, and some drag from Iran war uncertainty in leisure, hospitality, and transport. Weather is expected to be a neutral factor this month.

These trends support consumer spending without triggering immediate concerns about wage inflation. The jobless rate should hold at 4.3% or perhaps round down slightly. The Fed has likely shifted its strategy as rate cuts are no longer the immediate priority. A very strong report could actually be problematic by ending hopes for lower rates while oil prices rise.

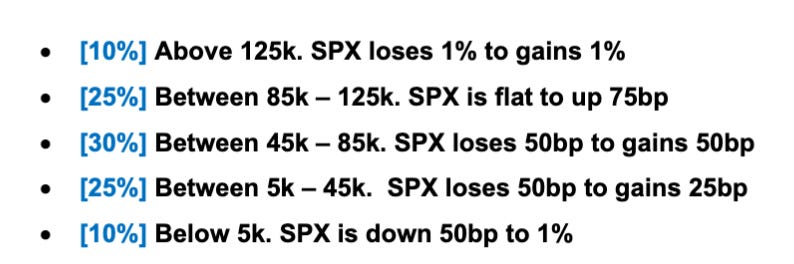

JPM’s scenario analysis is below:

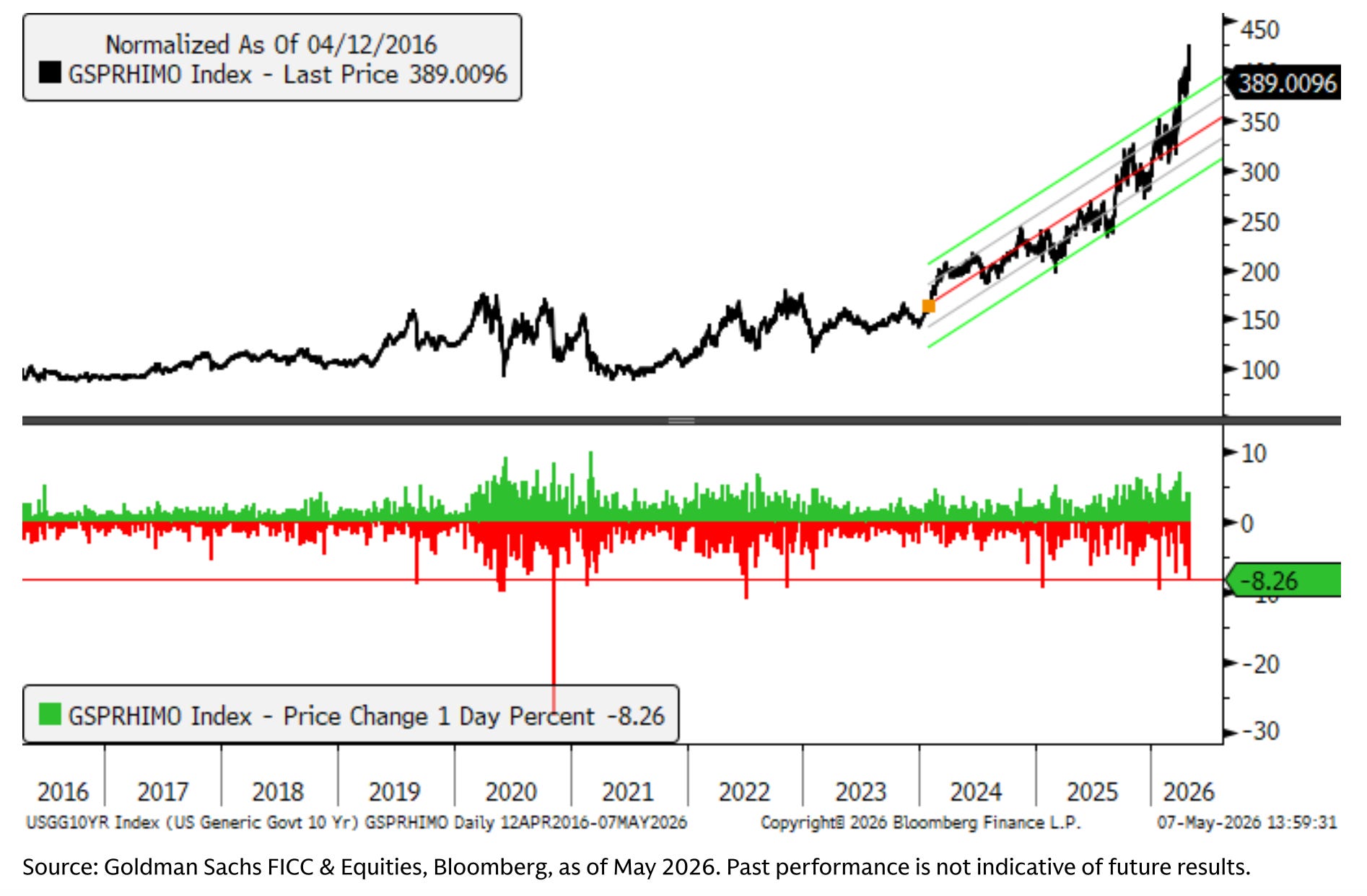

Chart of the Day

This is Goldman’s High Beta Momentum pair (GSPRHIMO) showing Thursday’s -8.26% drawdown against the full historical series. Five of the ten largest single-day moves in this pair over the last five years have now occurred in 2026. The historical retracement table tells you the base rate: these dislocations have reversed within one week in 58% of prior instances, with a median 1-week forward return of 1.64%.

Calendars

Market Prep

Markets closed in the red yesterday, with high beta momentum leading the way done. According to GS, the unwind was driven simultaneously by both the long and short leg. Software names squeezed hard on better-than-feared earnings: DDOG +31%, FTNT +20%, DASH +2%. At the same time, AI themes and semis exhausted after a well-publicized 50%-plus move since early April. ARM fell 10% on sluggish smartphone royalty results. COHR dropped 8% on softer-than-expected gross margins. Memory names pulled back after the overnight session. Goldman’s prime brokerage data had already flagged that momentum exposure had reached the 99th percentile over one year and the 100th percentile over five years. This was not a flush from light positioning.

US equity futures are holding up remarkably well given the overnight geopolitical deterioration, and the divergence from Asia is deliberate. The market is pricing the Iran process as “alive but bumpy,” not “re-escalating structurally,” and the absence of any flight to duration supports that reading.

Thursday’s Momentum unwind was an important event. Historically these dislocations retrace within a week at a 58% hit rate, but the setup is different from prior episodes in one critical respect. The correlation between the momentum factor and the AI complex is near all-time highs. This is not a clean factor flush with a rotation destination sitting in wait. It is a crowded book exhausting simultaneously in the highest-momentum names, driven by both legs: software squeezed on earnings while AI and semis ran out of catalyst.

Five of the ten largest single-day Momentum moves in five years have now occurred in 2026. The factor’s one-month volatility is in the 96th percentile. Momentum exposure on prime brokerage sits at the 100th percentile over five years. Nomura’s McElligott is calling this a “crash-up” and predicting a “crash-down” later, driven by the weight of accumulated delta from levered ETF rebalancing, options flows, and vol-targeting strategies all feeding the same direction. BofA is comparing the tape to the dotcom nineties.

My Take

The market is telling you the Iran ceasefire is going to resolve. I am not so sure. What I see is a recurring pattern of brief exchanges followed by Trump insisting the truce is holding while simultaneously threatening to make Iran “one big glow.” An unverified social media post moved crude by several dollars twice in 48 hours. These are not the mechanics of a negotiation approaching conclusion. Tehran’s red lines on the nuclear program and Strait access have not moved, and the US demand for advance commitments on both is not a minor ask.

Three things to watch today: the headline NFP print and specifically whether unemployment rounds to 4.2% or stays at 4.3%, whether a strong number generates a rates reaction that presses on the equity multiple, and whether the momentum complex stabilizes or the unwind from Thursday extends into any negative data surprise.

Goldman notes that with earnings season largely through, optimism may be starting to capitulate, leaving valuations stretched and factor volatility elevated with no imminent re-rating event to lean on.