Breakfast Bites: NVDA Night, Yield Fight

What do we want to see from Nvidia today? Reads from crude draws, War Power Resolution & HD. + One new ETF to buy

Rise and shine everyone

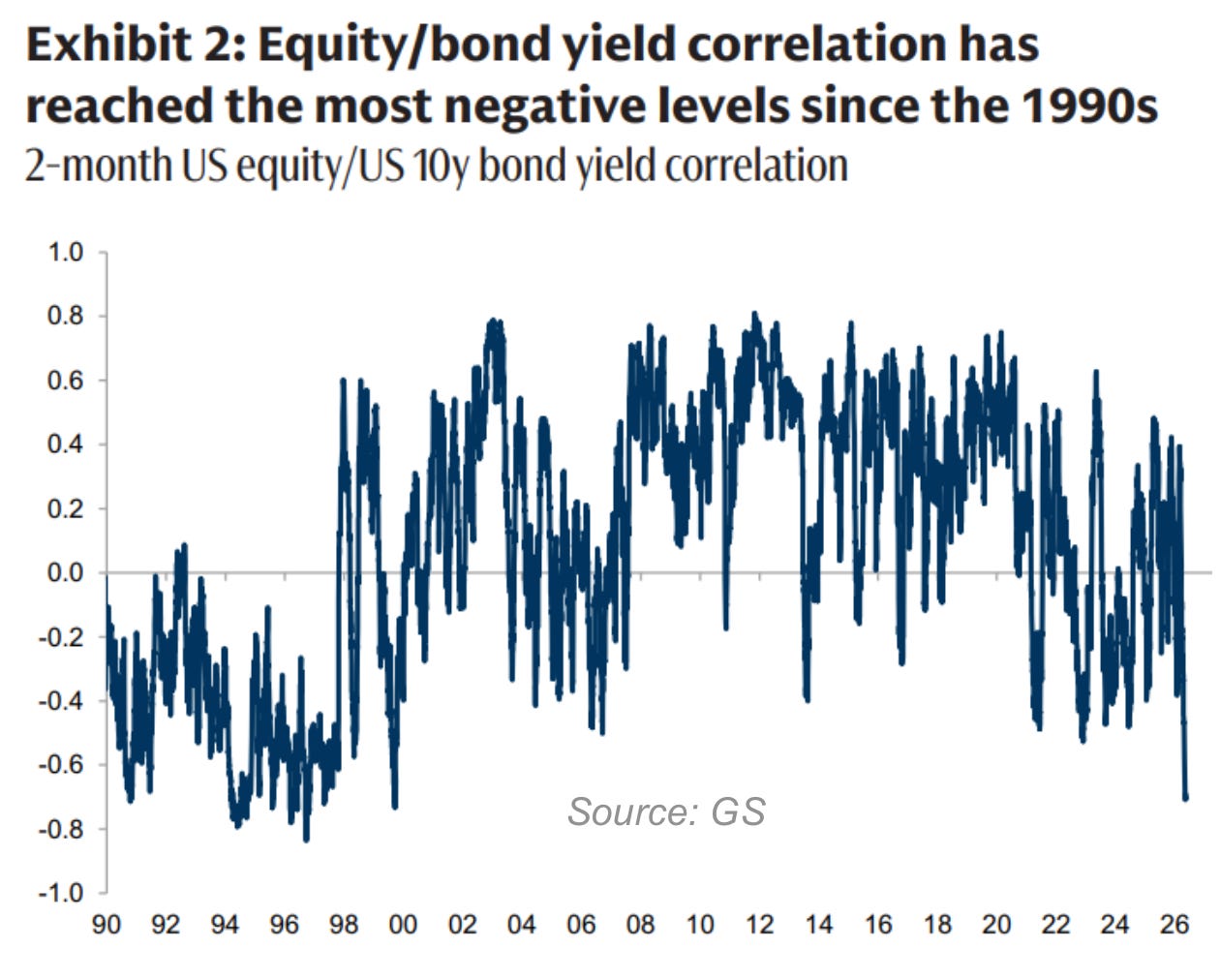

Markets are looking a little more positive this morning, after broad US indices closed lower yesterday for a third day. Yields are pulling back but the Vix still remains elevated just above 20, so still reason to proceed with caution. Also, the 2-month equity/bond yield correlation has now reached its most negative reading since the 1990s. This correlation breakdown is a structural warning that traditional portfolio hedges may not work the way models assume.

Our most recent pick LIT (Lithium ETF) crossed below $81 yesterday - that was where we were looking to buy. On that note, I’m also adding another new ETF to buy, to our tactical list. I wouldn’t wait for price to come in on this one, I’d just start a position.

Three things we’re watching today:

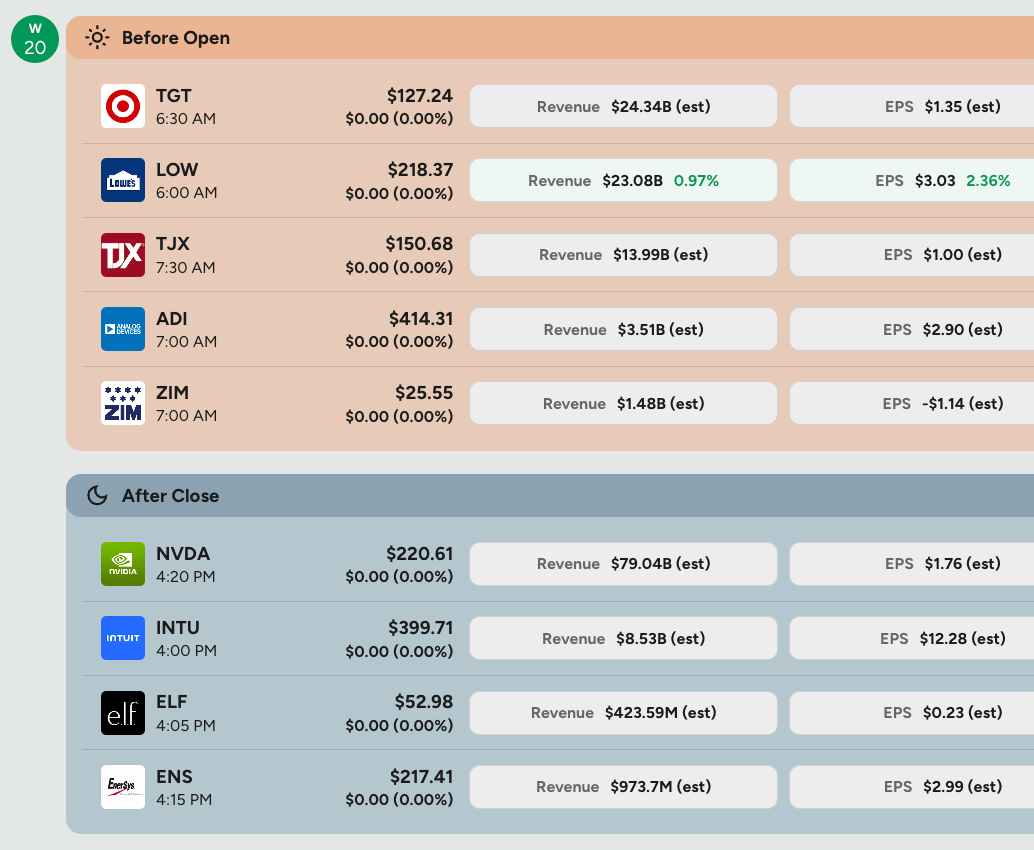

NVDA reporting after the close (preview under Market Prep section); TGT and LOW for a read on whether the consumer is holding up at the intersection of higher gas and higher rates

Discussion and progress of the War Powers Resolution and the Middle East War

FOMC minutes at 2pm ET: The Warsh Fed wants less forward guidance, closer Treasury coordination, and today’s minutes could validate the hawkish lean — three dissents at the last meeting, and any “no cuts this year” reinforcement simply adds to bond pressure.

Morning Macro Briefing

The Senate recently advanced a bipartisan resolution to limit President Trump’s war powers regarding Iran, leveraging a fragile ceasefire to challenge the current administration’s military strategy. Next, the measure must pass a full Senate floor vote before moving to the Republican-controlled House, though any final passage faces an inevitable presidential veto that Congress currently lacks the supermajority to override. If the resolution somehow becomes law, it would legally mandate the withdrawal of US forces from hostilities, though the executive branch is already attempting to exploit legal loopholes by arguing the ceasefire paused the statutory timeline.

While this political showdown heavily pressures the White House to find a diplomatic exit rather than escalating the war, investors must brace for localized market volatility. Key indicators to watch include sudden spikes in global crude oil prices due to Middle East supply disruption risks and defensive rotations into safe-haven assets if the fragile ceasefire collapses. Ultimately, tracking whether the House mirrors the Senate’s bipartisan cracks will dictate if defense spending timelines are abruptly shortened, directly impacting market sectors tied to the conflict.

The Senate advancing a bipartisan war-powers challenge matters because it introduces a political overhang on the Iran conflict timeline, with direct implications for oil supply risk and energy price volatility.

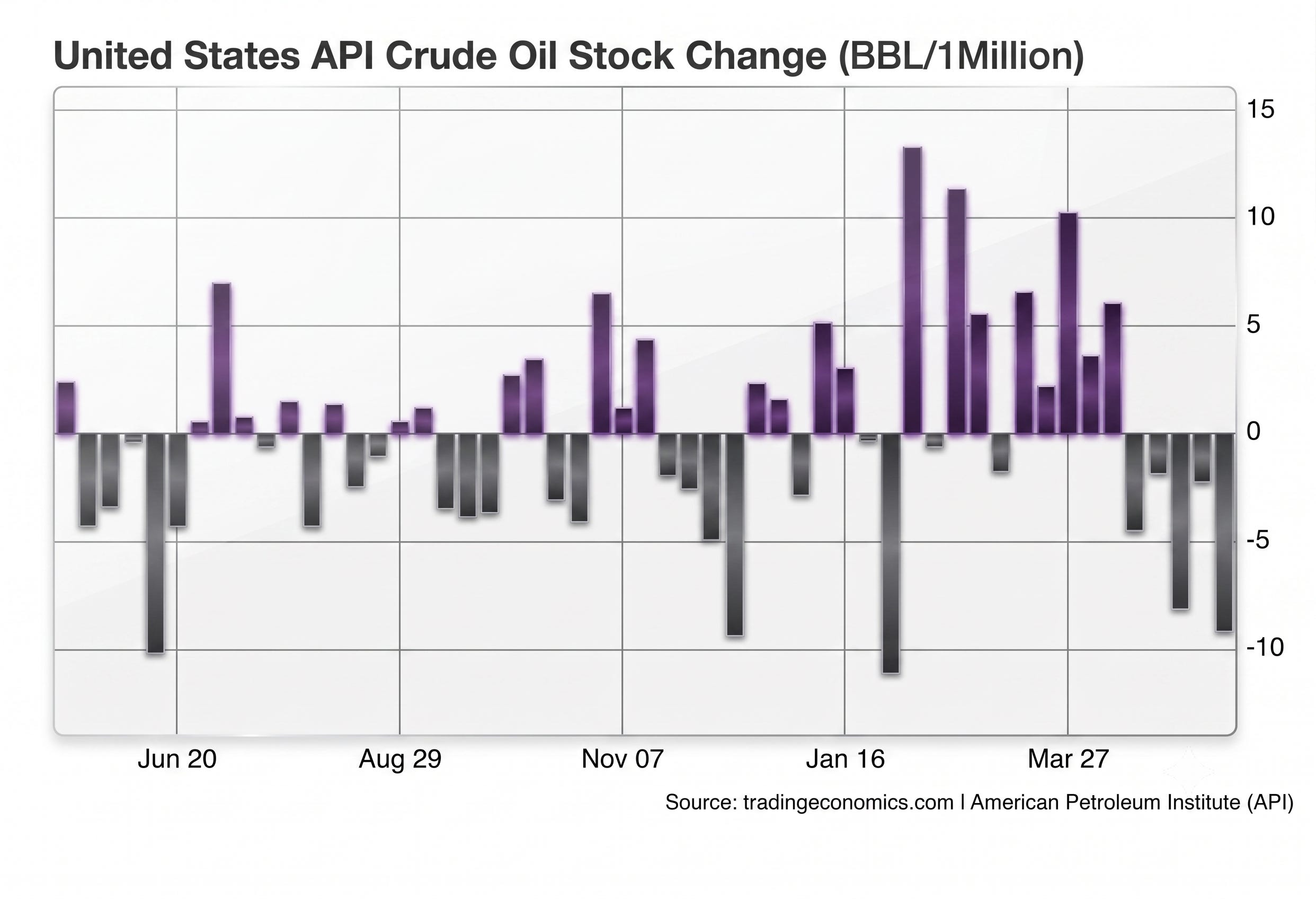

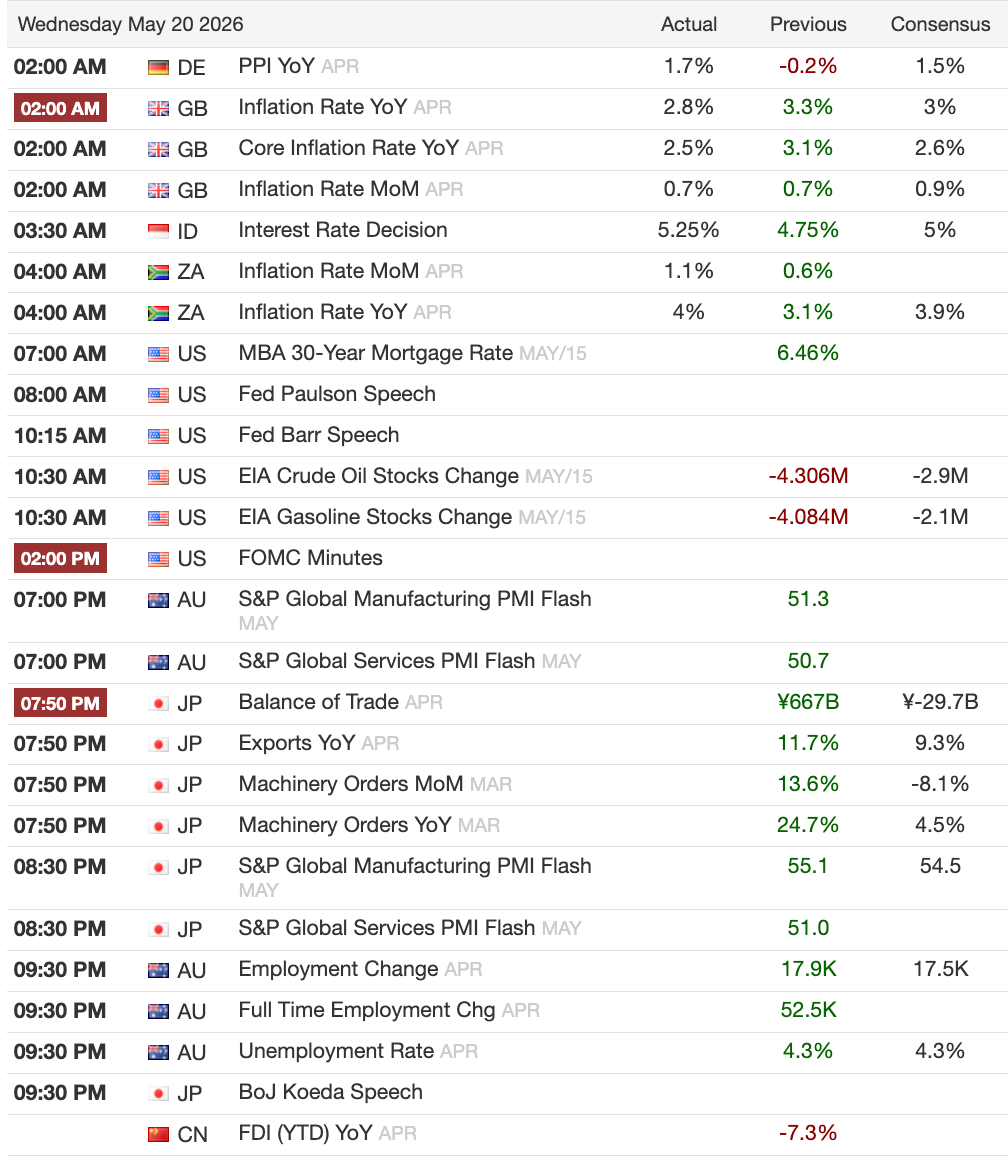

Yesterday’s crude draw came in at -9.1m barrels vs. an expected -3.2m. Because the government is aggressively drawing down the Strategic Petroleum Reserve to keep a lid on domestic fuel prices near $110 per barrel, public safety cushions have fallen to their lowest levels since mid-2024. This is a reminder that the government’s ability to suppress energy prices through reserve releases is shrinking.

For equity markets, these shrinking buffers present a structurally bullish backdrop for energy stocks while placing broader corporate profit margins under severe pressure due to elevated input and transport costs. If the fragile regional ceasefire collapses, we should prepare for a swift defensive rotation into traditional safe-haven assets and a sharp drag on consumer-discretionary sectors.

USDKRW moved sharply from 1450 to above 1500 last week on KOSPI profit-taking and index rebalancing flows, with the key event now the NPS decision deferred to May 28, where, without target revisions, Infomax estimates roughly 150tr KRW (~$100bn) in mechanical domestic equity selling given current overexposure. This is a significant EM risk event, and the smart money is betting on political intervention to cap the damage before the June 3 election.

Home Depot reported a resilient yet highly cautious US consumer navigating a housing market heavily constrained by high mortgage rates and low turnover. Homeowners are largely choosing to renovate existing spaces through professional contractors or smaller DIY projects rather than taking on major, finance-heavy remodels. Despite transactions dipping 1.3%, the company reaffirmed its fiscal 2026 sales growth guidance of 2.5% to 4.5% based on steady underlying demand.

HD’s cautious consumer and reaffirmed guidance sets the baseline read on housing-adjacent spending, with direct read-across to LOW reporting this morning — a cleaner beat there would confirm the sector is holding.

FOMC minutes drop at 2pm ET. Three Fed presidents dissented at the last meeting, arguing the statement carried a downward bias and should be more neutral. Rob Kaplan, Vice Chairman of Goldman Sachs, expects Warsh to neutralize that language at the June meeting and notes Warsh is also likely to reduce reliance on forward guidance and work more closely with Treasury on the balance sheet over time. The minutes will be read closely for any further sign of a shifting policy bias.

Chart of the Day

The 2-month correlation between US equities and the 10Y yield has reached its most negative reading since the 1990s. Most risk models built over the past two decades assume bonds and equities diverge under stress, providing natural portfolio diversification. That assumption broke down in 2022 and it is breaking down again now. When both assets sell off together, the hedging calculus changes, forced de-risking accelerates, and the volatility mechanics become self-reinforcing. This is the structural backdrop against which today’s positioning dynamics must be read.

Calendars

NVDA Earnings - Brief Preview

What do we want from NVDA earnings today? Validation. The company is central to the AI spending and what we want to know is whether the hyperscalers are justified in the capex projections.

The stock has pulled back 6.4% from its May 14 high after a 40% rally from the April lows, and the momentum unwind of the past three sessions has been most acute in the AI and semi complex. JPM’s buyside survey puts F1Q27 revenue expectations at $80.97bn versus the Street consensus of $78.6bn, against the company’s own guide of $78bn. On EPS, the buyside survey mean is $1.84 vs the Street at $1.76. For F2Q27, the Street is looking for $86.4bn in revenue.

A clean beat and strong Q2 guidance would validate the AI capex thesis at the moment it most needs it. A miss, or conservative guidance, would hand the momentum unwind fresh fuel in an already structurally fragile positioning environment.

Semis had been quietly recovering in the final hour of yesterday’s session as large buy orders came in post-Europe close, which suggests some positioning ahead of the print.

The options setup around the print matters as much as the numbers. Upside call skew in MegaCap Tech and semis is at extreme percentile readings. Nomura has flagged that convexity hedges have been building in SMH and DRAM via wingy puts, alongside shorter-dated QQQ and SPX hedges. A big enough upside surprise could squeeze shorts and arrest the momentum decay. A disappointment into this setup, however, would not be orderly.

Market Prep

Yesterday’s session closed with SPX -0.7%, NDX -0.6%, and the Russell -1.0%, with 63% of SPX names finishing lower.

The move was broadest in Cyclicals, with Materials, Consumer Discretionary, Financials, Industrials, and Comm Services all down over 1%.

Yesterday’s session was rough under the surface. The stocks that had rallied the hardest this year, AI and tech momentum names, sold off sharply, with some down as much as 7-22% from recent highs, even as the broad index only fell modestly.

The market is sitting on a fragile structure. Almost all the gains this year have been concentrated in a handful of big tech names, and the options positioning means that if stocks drop 2% in a single day, automated selling kicks in and amplifies the move lower.

Trading conditions are thin and one-sided. There are far more sellers than buyers right now, and the big institutional players are not stepping in aggressively — they are cautiously trimming risk and adding hedges rather than buying the dip.

The combination of a momentum factor already down 12.8% in three sessions, dealers short gamma, thin liquidity, and risk-parity still selling sends a signal that the next -2% day in the SPX may not be a buying opportunity until the options machinery finishes clearing.

Our Tactical Watchlist is below the paywall, with our latest pick.