Breakfast Bites - Nasdaq hits All-time High

Momentum remains strong; Yields Lower despite Hawkish Chair Powell

Rise and shine everyone

US Equity Markets seem unstoppable. The Nasdaq-100 hit an all time high yesterday, and the S&P 500 is closing in on it’s previous high too, despite a hawkish Jerome Powell yesterday saying there’s no rush to cut rates.

The de-escalation in the Middle East is cause to celebrate but we also got softer macro data - the Case-Shiller Home Price Index saw a nice drop to 3.4% YoY from the previous 4.1%. Some of this may be driven by the immigration policies, and decreasing pressure on the demand for housing.

On the negative side, Conference Board Consumer Confidence data took a bit of a hit, dropping “5.4 points in June, falling to 93.0 (1985=100) from 98.4 in May”. Most of this was driven by the Present Situation Index, with Tariffs and Inflation still being some of the key issues on people’s minds.

Nevertheless, bond yields continued to move lower, and the positive market momentum continued. JP Morgan highlights that some of the move was driven by short squeezing and cyclicals.

After the close, FedEx stock fell around 5% after reporting fiscal Q4 results that met cost-cutting goals but failed to reassure investors on the demand outlook. While EPS came in at $6.07 adjusted, revenue growth remained sluggish at $22.2 billion, and the company withheld full-year guidance, citing ongoing trade policy uncertainty, particularly around China. CEO Raj Subramaniam noted that “the global demand environment remains volatile,” and while markets were previously lenient with companies skipping guidance amid uncertainty, that patience appears to be wearing thin.

Chair Powell’s Testimony - Day 1

Chair Powell’s testimony before the House Financial Services Committee reinforced the message he delivered following the most recent FOMC meeting: the Fed remains in wait-and-see mode. He emphasized that the FOMC is “well positioned to wait” before making any policy adjustments, citing the strength of both the economy and labor market.

Powell avoided aligning with recent dovish comments from Governors Bowman and Waller, who floated the idea of rate cuts as early as July. When pressed on the timing of potential cuts, Powell declined to point to a specific meeting, instead explaining that the Committee would need to see either a significant weakening in the labor market or lower-than-expected inflation to act sooner. He acknowledged that the FOMC would still get around to cutting rates if inflation moved higher and the labor market stayed firm, but that it would be a later move.

On tariffs, Powell struck a cautious tone, saying it remains unclear how much of the new tariffs will pass through to consumer prices and whether the effects will be transitory or more persistent. He noted that while some inflation impact is expected, the Fed will need to monitor the data before drawing conclusions.

Chair Powell also briefly touched on the Fed’s framework review, saying the necessary meetings have occurred and that final changes are expected later this summer. Reflecting on the 2021–2022 inflation cycle, Powell admitted he would have raised rates slightly earlier but didn’t believe it would have significantly changed the outcome, though he did concede that the FOMC “would have looked a lot smarter” had it done so.

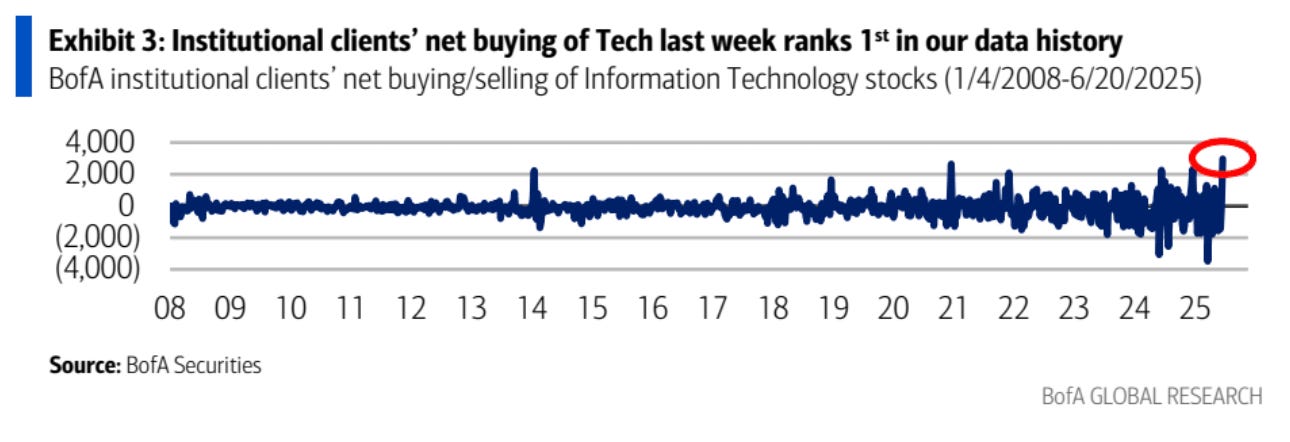

Chart of the Day - Tech rules again

“Buying was concentrated in Tech for the second consecutive week, with last week’s inflows marking the largest since June 2024. Institutional clients’ buying of Tech ranked first in the data’s history and landed in the 98th percentile when adjusted for market cap. We turned more constructive on the sector earlier this month, and recent flows further support that positioning.” - BoFA

Calendars

(news taken from Reuters, FT, Bloomberg; Calendar from Trading Economics)