Breakfast Bites: MOMO Watch

Watching Yields, Oil and Food prices. Momentum pullback is all everyone's talking about in terms of market dynamics.

Rise and shine everyone

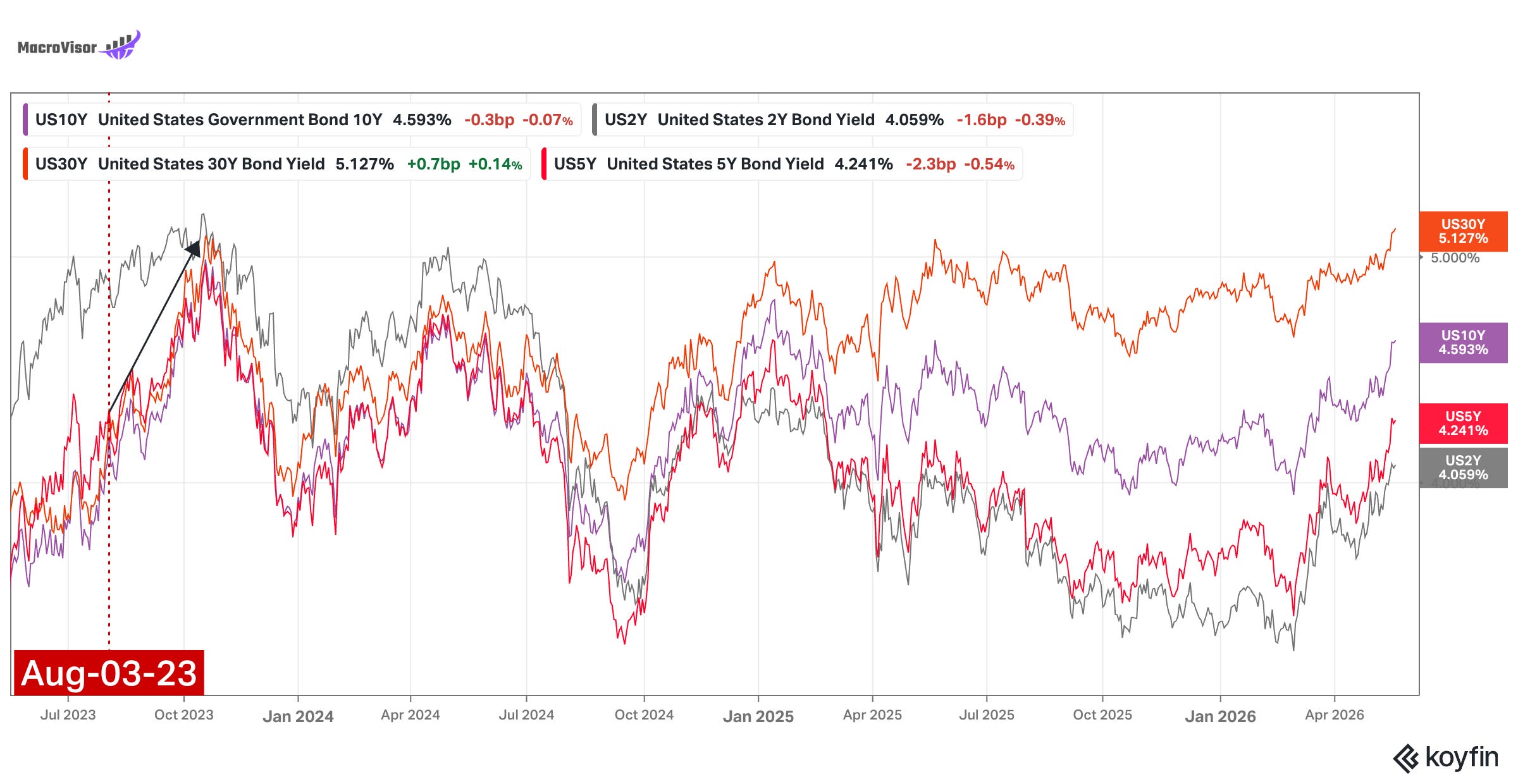

The violence in yields has calmed down, but rates are still moving higher. No surprise that markets are therefore, still moving lower.

Three things we’re watching:

War Headlines and Yields - Oil is inching higher again today, as are yields. Oil took a bit of breather after President Trump put a pause on the threat of attacks. Let’s see what today brings.

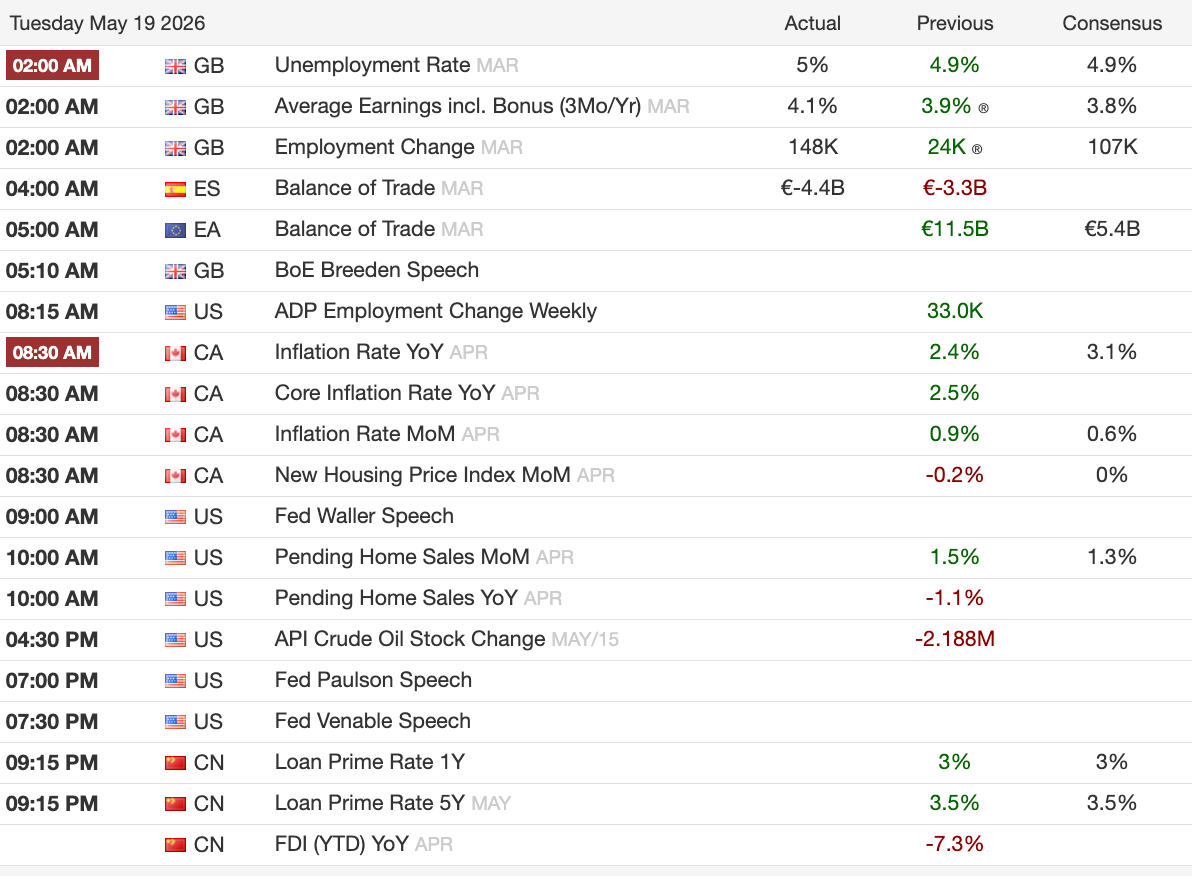

API crude stocks change released at 4:30 pm ET - there was a huge draw of over -8m barrels towards the beginning of the month. With summer demand season, this doesn’t bode well for oil prices and inflation.

Food prices - we’re seeing food related commodities start to surge, specifically grains. There’s no doubt this could lead to more headline inflation, and hurt consumers. Watch $DBA - the agriculture ETF.

Morning Macro Briefing

News that has been developing over the past few days is the employee strike at Samsung. The labor dispute has rattled shareholders, with the KOSPI shedding more than 4% as the market priced in the risk of prolonged disruption at one of the country’s most systemically critical companies. The Bank of Korea has now weighed in, warning that a general strike could knock up to 0.5% off GDP. Samsung is not just a stock; it is the Korean economy, and when it is in labor uncertainty, the whole market trades like it.

JGB markets took a partial breather overnight, though yields at the long end still crept up 5-6bps into the close ahead of tomorrow’s 20-year auction. Japan’s Q1 GDP came in at an annualised 2.1%, with nominal growth running well above real as inflation does the heavy lifting, and consumption beating expectations. The resilient growth print, combined with PM Takaichi’s confirmation that an extra budget is on the cards, keeps the BOJ firmly on track for a rate hike in June or July.

For global investors, a BOJ hike matters beyond Japan’s borders. Yen strength, pressure on export sector margins, and the ongoing unwind of yen-funded carry trades all feed directly into global capital allocation decisions.

For the UK, it’s not just political pressure that’s building. The unemployment rate increased to 5% again from 4.9%. Dec 2025 and Jan 2026 saw the highest rates in 10 years at 5.2%, outside of the pandemic shock. The labor market pain doesn’t seem to have gone away. Average earning growth also inched higher to 4.1% from 3.9% - a worry for the Bank of England (BoE) for core services inflation. All of this is yet more reason for the BoE to lean hawkish, and for gilt yields to move higher, putting pressure on stocks. I suspect GBP will continue to come under pressure.

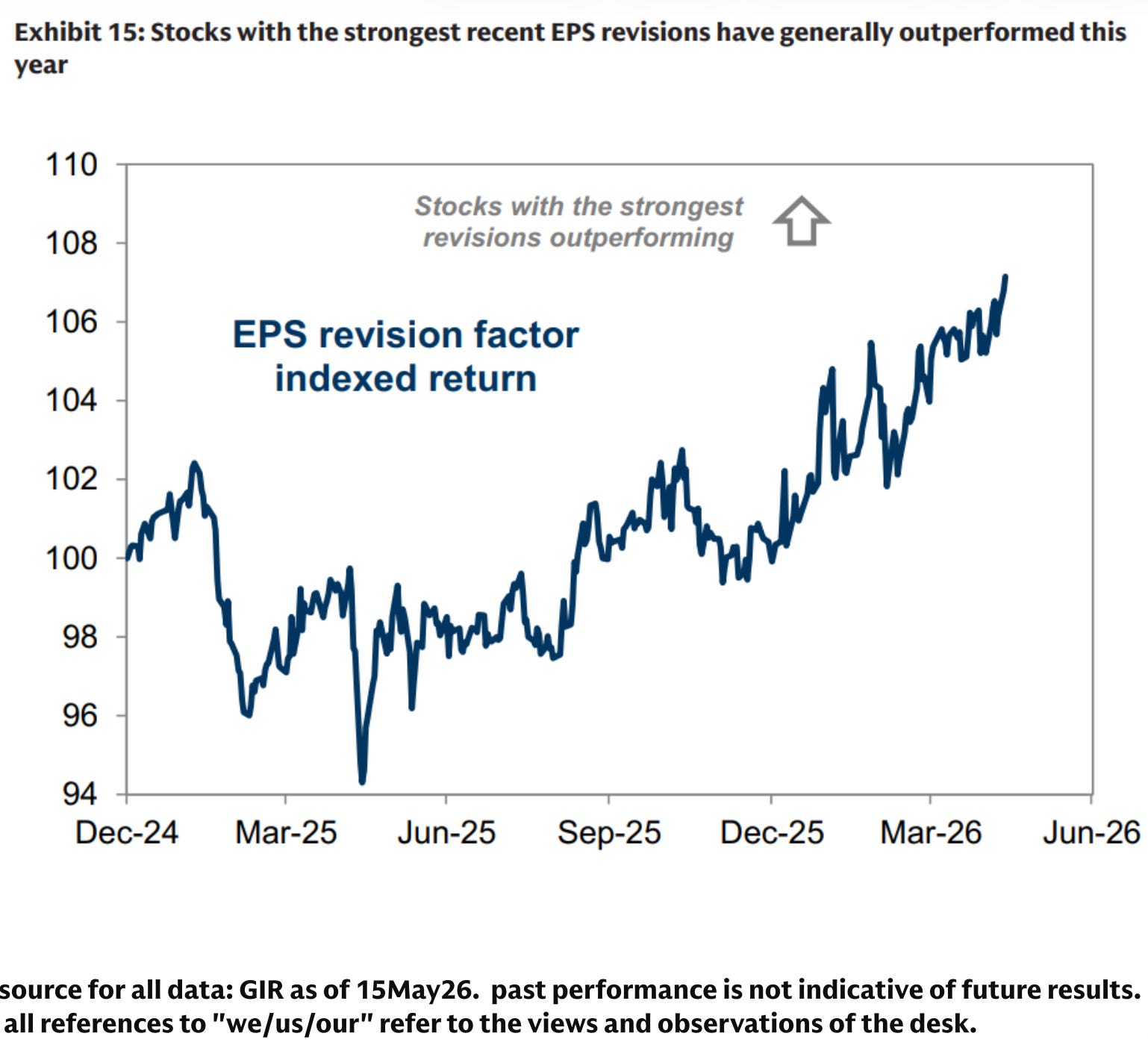

Chart of the Day

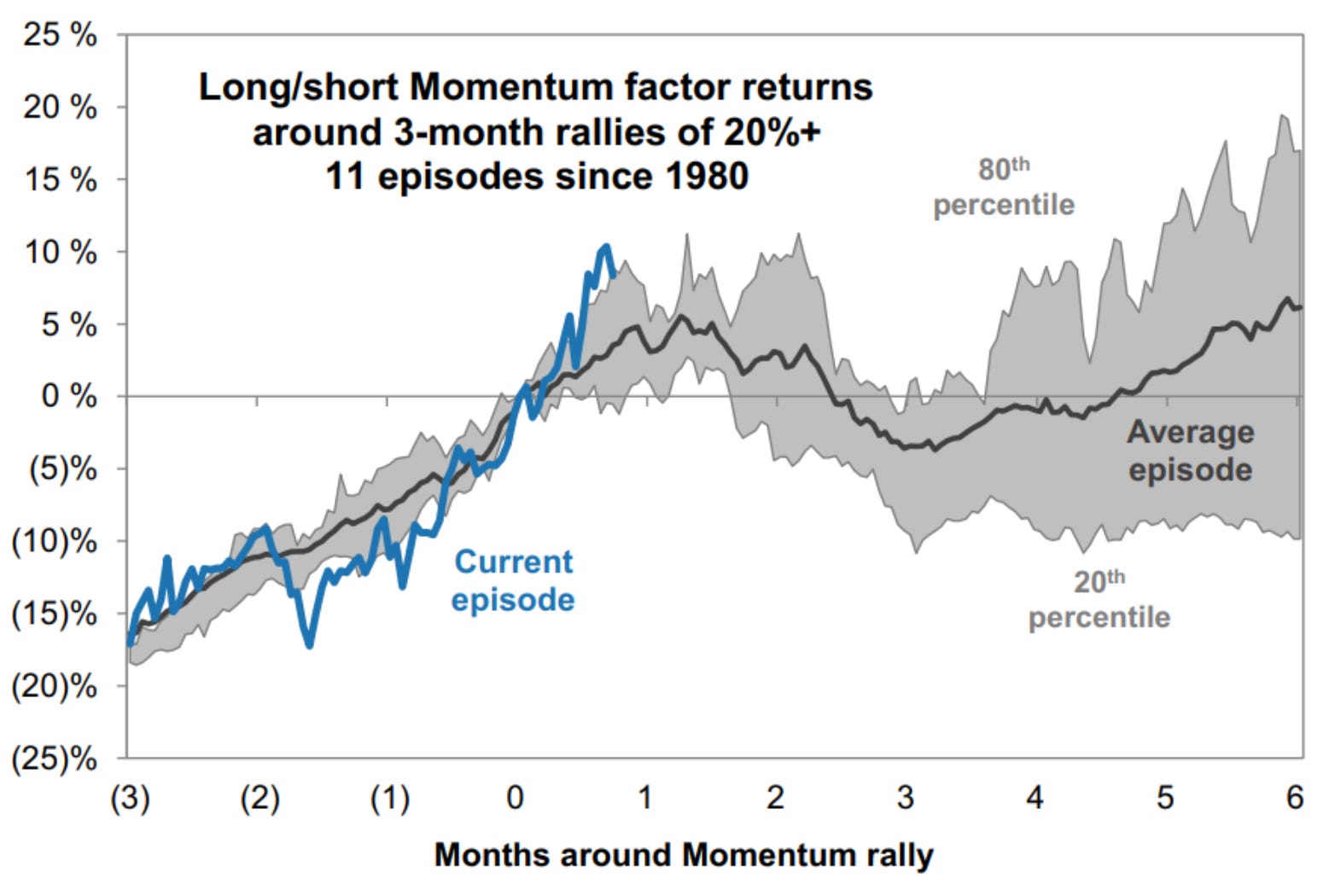

GS has been talking a lot about the momentum rally. Here’s what they say about continuation:

“In the past, similarly sharp 3-month Momentum rallies have usually extended for another month before peaking. Since 1980, there have been 11 other distinct episodes where Momentum rallied by 20% or more in a 3-month period. On average, Momentum went on to deliver an additional gain of 6% during the following month, but the strength of the recent Momentum rally has already exceeded that average. The Momentum factor then typically declined during the following two to three months.”

Last week I had a chart from GS that showed returns often turn lower after a strong momentum rally. However, “unlike in the late 1990s or 2021, however, the recent market rally has been driven primarily by surging near-term earnings estimates. Within the index, increasing expectations for AI capex spending and higher energy prices have driven the majority of the positive revisions.”

(All quotes from GS)

Calendars

Market Prep

Where the market is concerned, we’re all banking on earnings. With earnings breadth increasing, we’re extrapolating that market breadth will also eventually start to increase. This is what could make the difference to equity markets remaining resilient.

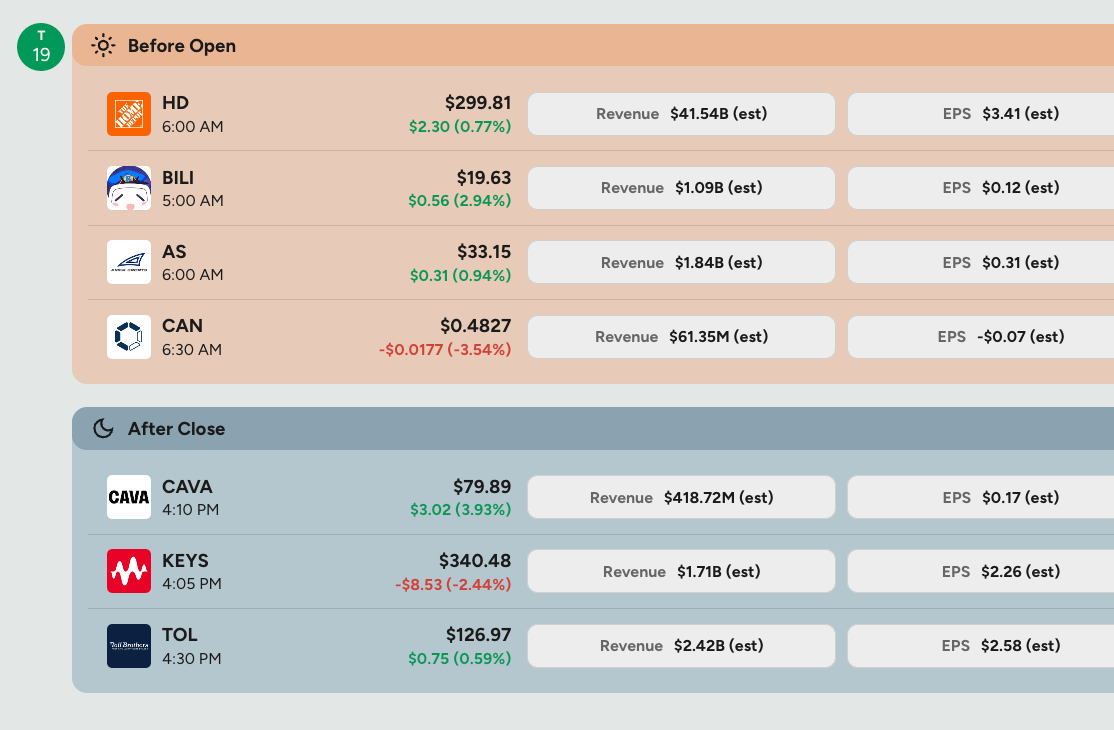

On to action… Monday’s session was relatively quiet. Goldman’s desk scored activity at a 3 on a 1-10 scale, discussing that the the street is likely holding back ahead of NVDA earnings Wednesday, Google’s I/O today, and WMT Thursday. When the catalysts that could move the market are all still ahead of you, nobody wants to be caught leaning the wrong way.

Interestingly, the S&P closed near flat at 7,403, but the headline masked meaningful dispersion underneath. The NDX was down -0.45%, the Russell underperformed at -0.65%, but more than 70% of S&P constituents actually closed higher on the day. Tech dragged the index lower while the rest of the market held up - this is the kind of bread dynamic that signals broad-based rotation. This is a good thing.

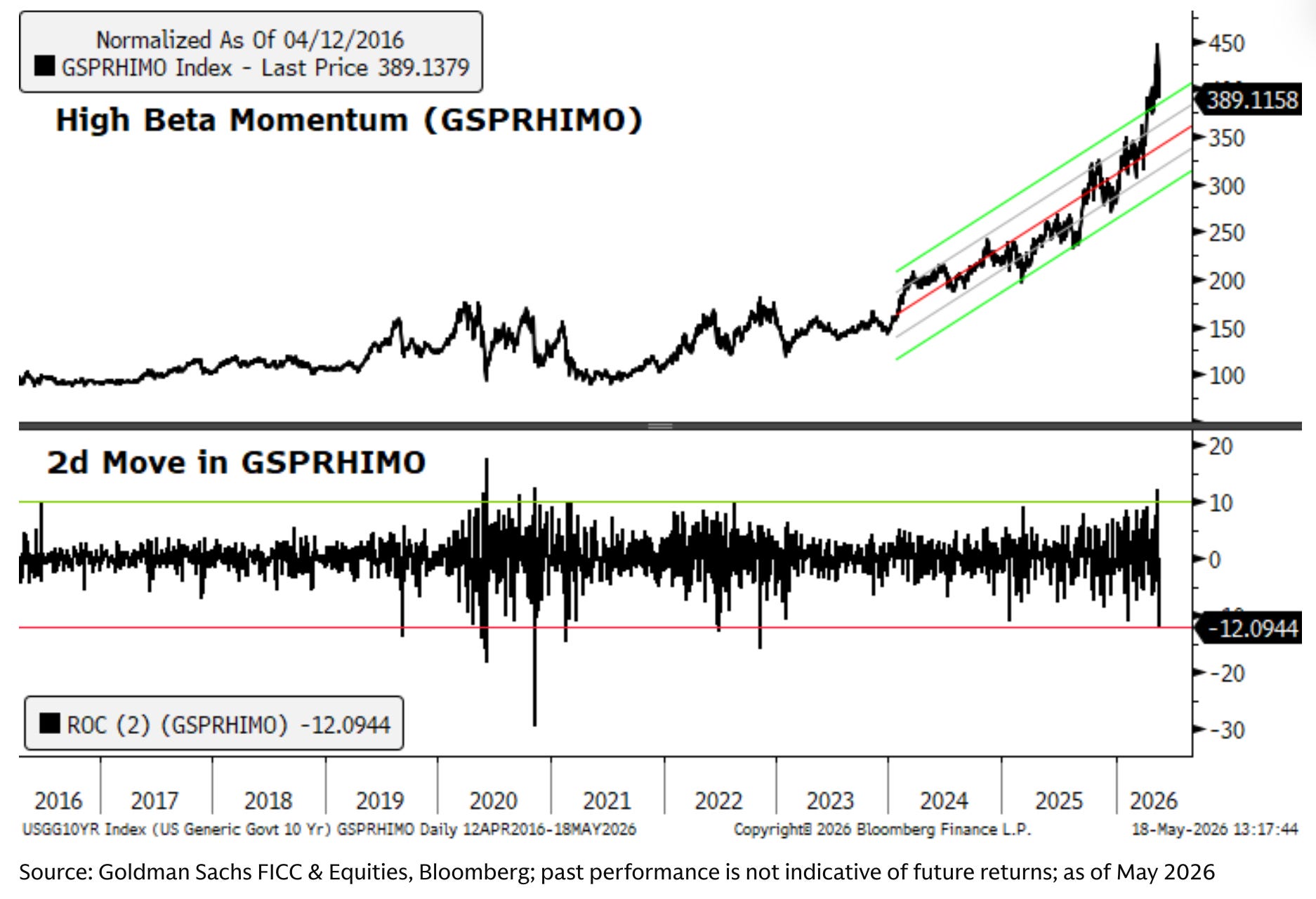

The dominant risk for positioning right now is the momentum unwind. (See also chart of the day).

The momentum trade has pulled back roughly 14% from its peak in just three sessions, but it is still up 40% for the year, which means there is a long way to fall if the unwind accelerates.

Hedge funds, retail investors, and institutional allocators are all crowded into the same high-momentum names, with positioning metrics across the board sitting at multi-year highs. If that trade starts to break, the selling pressure would not be contained to a handful of tech stocks; it would spread quickly as funds rush to reduce exposure across their books. The catalysts to watch are NVDA earnings Wednesday, any breakdown in Iran negotiations, and continued pressure on bond yields, any one of which could be enough to tip the balance.

On the systematic side, CTAs remain significantly long global equities with momentum signals broadly positive across major US indices, and CTA equity beta is near historic highs. JPM estimates there is still more than a 5% drawdown cushion in US large caps before the first momentum trigger levels are crossed. That cushion exists, but it is not unlimited, and the setup gets considerably more dangerous below it.

As always, our tactical watchlist is behind the paywall.