Breakfast Bites: Markets remain cheerful

Nasdaq logs a winning steak amid the lack of shocking news; Banks say the US consumer is resilient

Rise and shine everyone

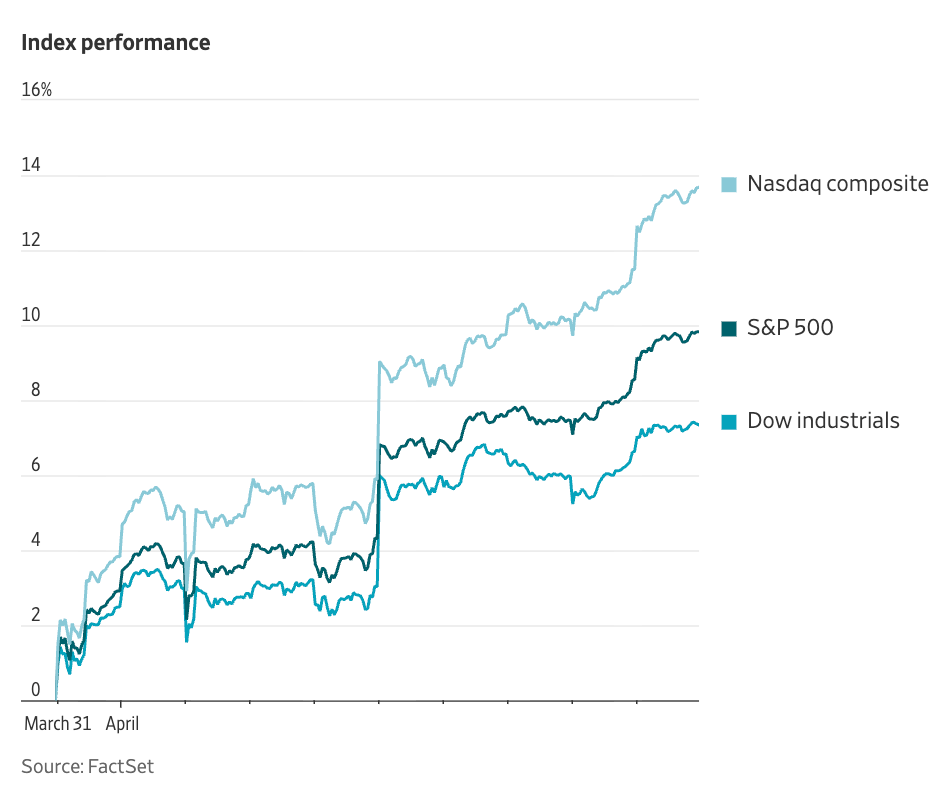

The Nasdaq captures an 11-day winning streak, its longest since 2021, while the S&P 500 moves within 0.2% of its January record.

Earnings reports from major financials confirm the US consumer remains fundamentally healthy, with spending growth at JPMorgan and Citi outpacing last year’s levels despite higher energy costs. While physical oil markets remain under strain, geopolitical risk is retreating as a holding ceasefire allowed over 20 vessels to transit the Strait of Hormuz in the last 24 hours.

Morning Macro Briefing

Overnight sentiment remains defined by cautious optimism as the Iran ceasefire holds and commercial shipping resumes through the Strait of Hormuz. President Trump noted that new talks could occur in Pakistan over the next two days, signaling that the conflict may be very close to an end. US officials confirmed that over 20 ships cleared the chokepoint recently, though physical oil markets still show signs of extreme stress as the system runs down buffers.

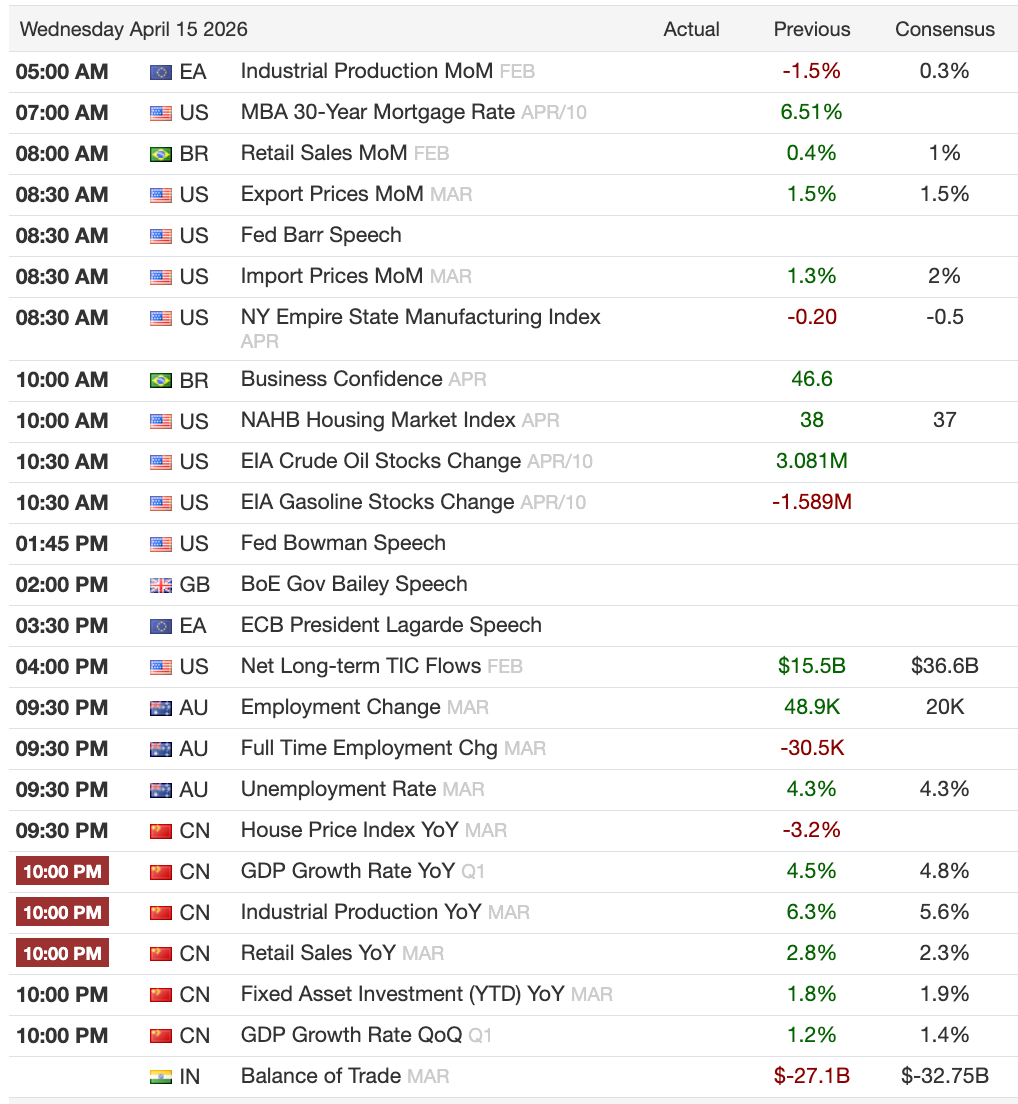

The inflation narrative shifted after the March PPI printed at 0.5%, significantly cooler than the 1.1% survey expectation. This added to the relief for markets, but something to note is that PCE-relevant components like airfares and medical care were actually stronger. The JPM economics team now estimates March core PCE at 0.32%, suggesting that the year over year rate could move up to 3.2%.

Attention now pivots to a major data dump from China, including Q1 GDP, industrial production, and retail sales. Treasury Secretary Bessent has affirmed that the US will pursue secondary sanctions if necessary while noting that the US maintains a 3 to 6 month lead over China in AI. This global activity data will be critical as refiners in Asia have already cut throughput by 2 mbd due to crude shortages.

Chart of the Day

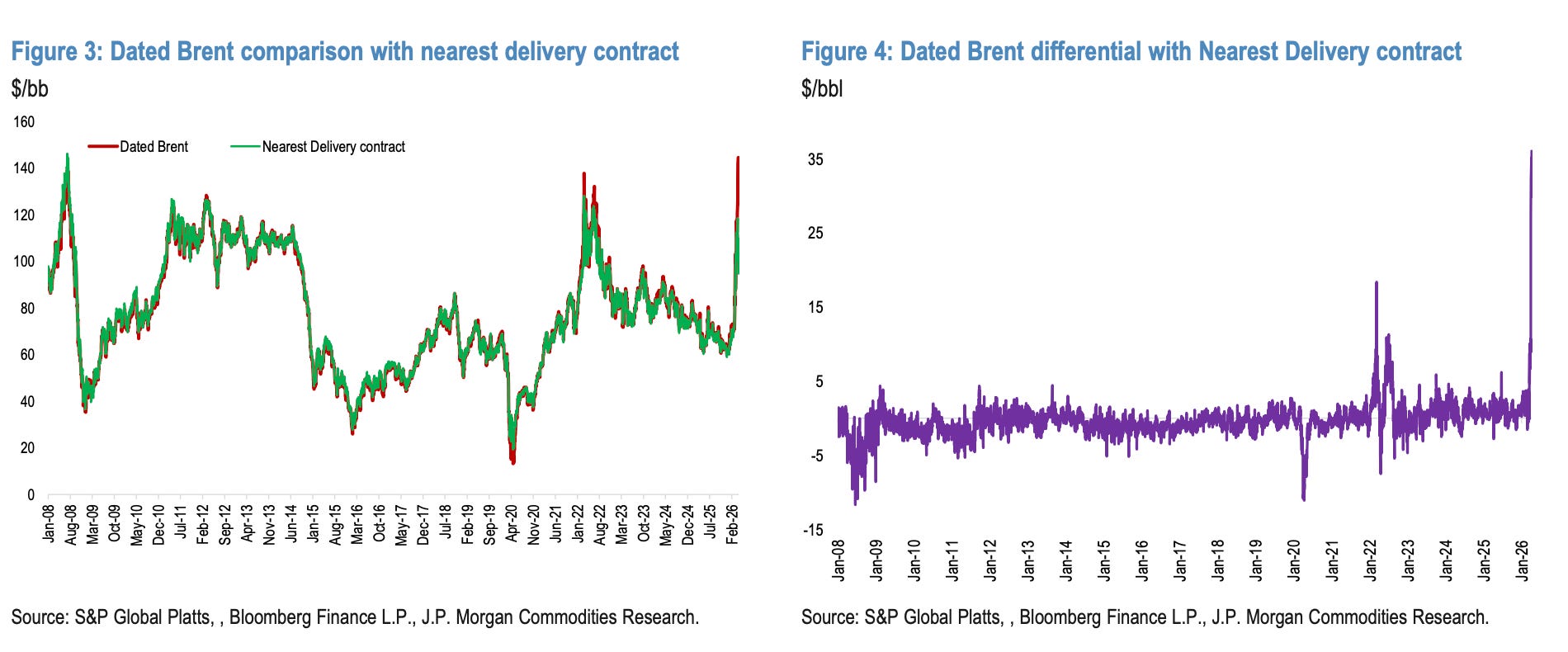

These charts show the divergence between physical spot prices (Dated Brent) and the front-month paper futures contract, highlighting a massive recent premium for prompt delivery (physical). The unprecedented spike in the differential to approximately $35 per barrel reflects a market in extreme backwardation, signaling that immediate physical supply has become a scarce commodity as global inventories approach operational minimums.

Calendars

Market Prep

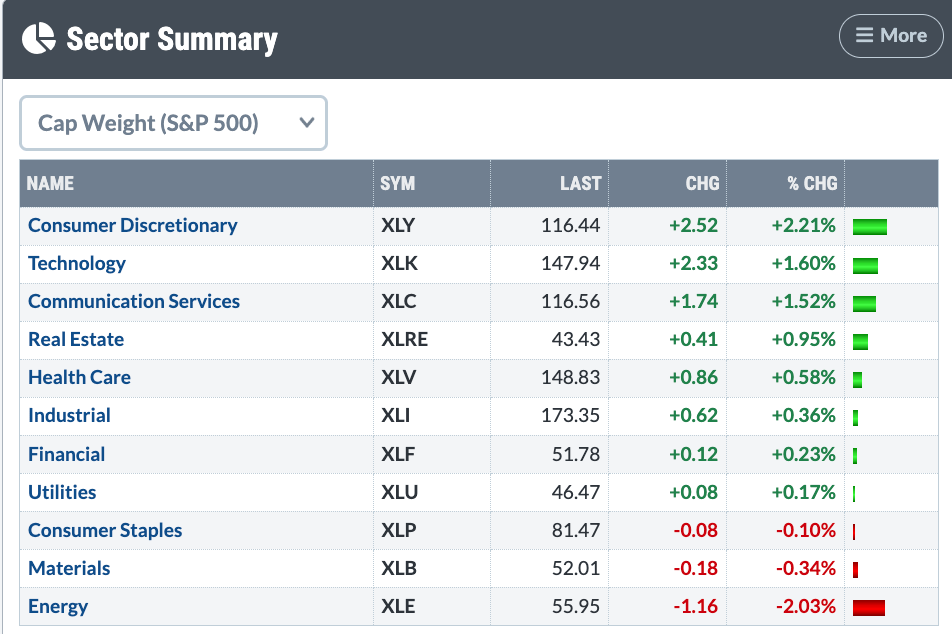

The setup for the session seems to be a continuation of the risk-on we’ve seen, as 8 out of 11 sectors finished higher in the prior day, led by semiconductors and airlines.

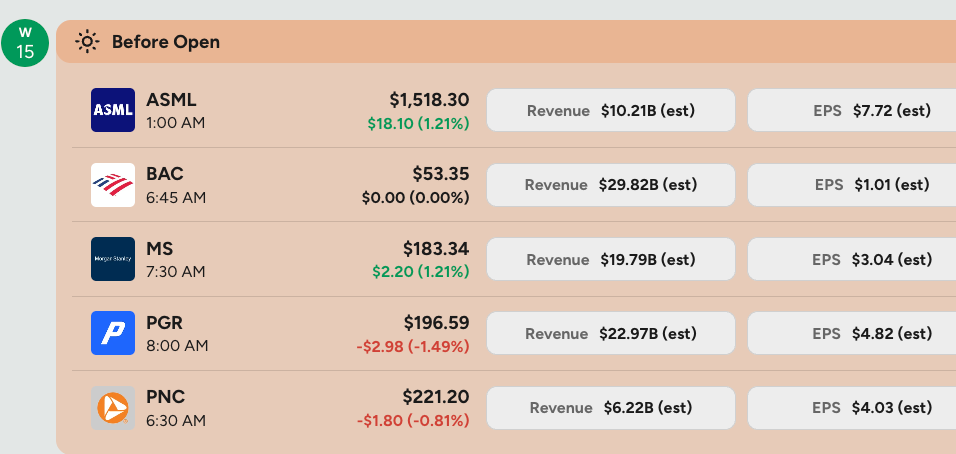

Bank earnings yesterday were defined by strong bottom-line beats fueled by record-breaking market activity, though a more cautious outlook from management teams tempered the initial enthusiasm. JPMorgan Chase reported a core EPS of $5.94, surpassing estimates of $5.58, as record Markets revenue of $11.6 billion (up 20% year over year) and an 82% surge in mergers advisory revenue drove results.

Citigroup logged its highest quarterly revenue in a decade at $24.6 billion, beating profit targets on the back of a 19% jump in markets revenue and resilient 4% growth in US consumer cards. While Wells Fargo delivered an EPS beat of $1.60, it slightly missed revenue forecasts as net interest margin compression offset growth in noninterest income.

Despite the strong numbers, the sector reaction was balanced by JPMorgan lowering its 2026 net interest income (NII) guidance to $103 billion and management teams citing geopolitical tensions and energy price volatility as significant ongoing risks. Management commentary across the board, however, affirmed that the US consumer remains fundamentally healthy, with spending growth at JPMorgan and Citi continuing above last year’s pace despite inflationary pressures.

Positioning shows a heavy tilt toward tech hardware and software as the AI hardware arms race remains the primary market driver. Dated Brent oil reached $144 per barrel, a record premium over paper futures that highlights the struggle to source prompt physical delivery. Additionally, capital flows may be boosted by a court confirmation that $127 billion in tariff refunds will begin processing next week.

Developments from Asia and Europe show a continued shift into cyclical and HALO companies, which focus on heavy assets and low obsolescence. While energy prices have retreated 20% from recent highs, physical supplies remain precarious with pre-closure barrels set to be exhausted by April 20. Traders are closely watching Bank of America today for further confirmation of the resilient consumer spend seen in the JPMorgan and Citi results.