Breakfast Bites: Markets celebrate the pause

Project Freedom suspended for diplomacy, AMD smashes expectations, and the global oil inventory math is becoming a genuine structural concern.

Rise and shine everyone.

President Trump paused Project Freedom at the start of the Asia session, and risk assets moved immediately higher. The message from the White House and the Pentagon was consistent: de-escalate, at least for now. Secretary of State Rubio declared offensive operations against Iran over. The president cited “Great Progress” in talks and said the decision came at the direct request of Pakistan and other mediating countries. US equity futures were +0.3% to +0.7% within minutes of the announcement.

The substance is considerably murkier. Iran’s president Masoud Pezeshkian, speaking the same day, described any return to negotiations as “impossible” so long as the US pursues maximum pressure. The US blockade on Iranian-linked ships remains fully in place. More than 1,550 commercial vessels carrying some 22,000 sailors are still stranded in the Persian Gulf.

The market is pricing in the good news. At the UN, the US and allies are backing a draft Security Council resolution that would open the door to sanctions or military action if Iran does not ease its chokehold on the waterway. That resolution needs China and Russia. Neither is a natural ally of a sanctions framework against Tehran.

Morning Macro Briefing

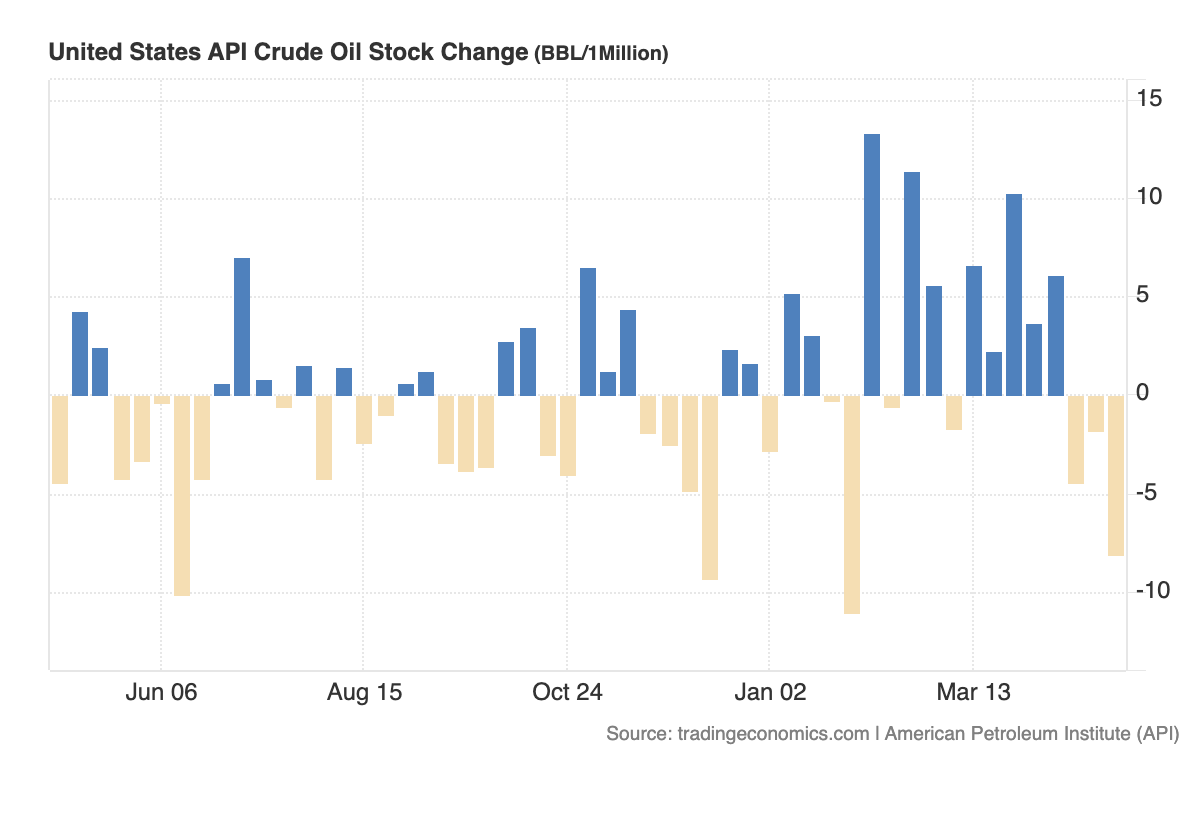

The oil inventory math has become a reason for concern by all. API data for the week ending May 1 showed a US crude stock draw of -8.10 million barrels, sharply wider than the prior week’s -1.79 million draw and far below the long-run average of around +0.18 million.

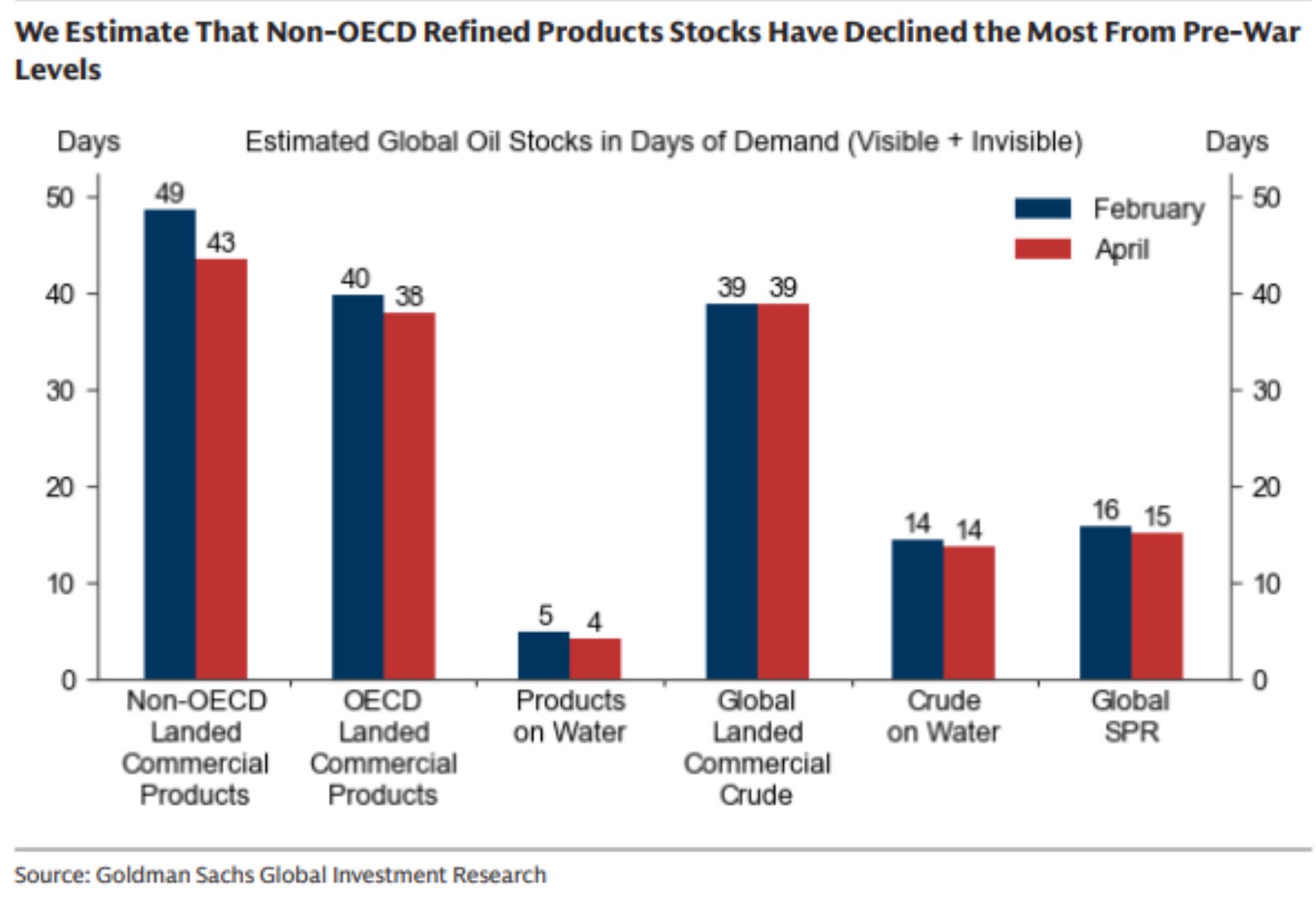

Goldman’s commodity team is now flagging a broader structural concern. Global commercial refined product stocks have drawn to 45 days of demand from 50 days pre-war, with non-OECD stocks leading the decline. European commercial jet fuel inventories are at particular risk, with Goldman estimating they could fall below the IEA’s critical 23-day shortage threshold as early as June. Naphtha, LPG feedstocks, and EM Asia ex-China are the other acute pressure points. These draws are accelerating, and the physical market is signaling a supply problem that exists independently of whatever diplomatic progress is or is not being made in the Strait.

Late in the Japan session, the yen gained nearly three big handles against the dollar in under 30 minutes, approaching the 155 level. This has the hallmarks of MOF intervention for the second time in a week, though the move was smaller than last week’s five big handle surge from above 160. The MOF has not confirmed.

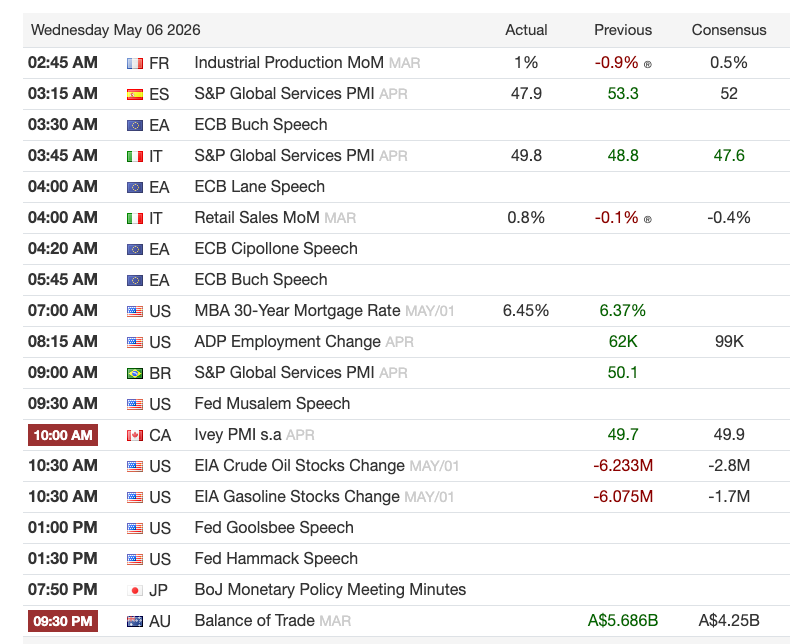

Tuesday’s ISM Services for April slipped 0.4 points to 53.6, in line with consensus, with a mixed composition: new orders fell 7.1 points while business activity and employment rose. The prices paid component held at 70.7, its highest since October 2022, and Goldman flagged that petroleum cost increases have not yet fully worked through supply chains, suggesting further elevated readings ahead. JOLTS job openings came in at 6,866k in March, broadly in line with expectations, and Goldman left their Q2 GDP tracking estimate unchanged at +1.7%, a level JPM noted maps directly to the current ISM reading.

China’s April RatingDog PMI Services marked the 38th consecutive month of expansion, with new projects and product launches cited as the main drivers. New Zealand’s Q1 average hourly earnings slowed even as unemployment ticked down slightly, and the RBNZ Financial Stability report noted banks are well positioned ahead of the May 27 rate decision.

The Treasury will make its quarterly refunding announcement at 8:30am ET this morning. JPM’s Jay Barry expects Treasury to remove the “at least” language from its guidance on maintaining nominal coupon and FRN auction sizes, signaling upcoming increases beginning around February 2027. If that language change materializes, it could push intermediate yields higher.

Chart of the Day

The chart captures the thesis at the center of this morning’s macro story. Non-OECD landed commercial product stocks have declined from 49 days of demand in February to 43 in April. OECD landed commercial products are down from 40 to 38 days over the same period. Products on water have shrunk to just 4 days. Goldman estimates that European commercial jet fuel inventories could fall below the IEA’s 23-day critical shortage threshold in June, and the pace of draws is accelerating.

Calendars

Market Prep

Asian equities closed broadly higher on the de-escalation news. The Kospi surged more than 7% to another fresh record high. SK Hynix added 10% to a new all-time high and Samsung outdid it, up 16%. The memory complex is absorbing the AI capex story from last week’s hyperscaler earnings directly. China’s mainland markets reopened after a two-day holiday, gaining more than 1%. The Nikkei remained closed for the final day of its holiday period.

US equity futures were trading +0.3% to +0.7% during the Asia session on the Project Freedom pause. Tuesday’s close saw SPX +0.8%, NDX +1.3%, and RTY +1.8%, with all 11 S&P 500 sectors finishing in the green. Small-cap outperformance has been a consistent feature of the de-escalation trade, and breadth was healthy with roughly 64% of SPX stocks finishing higher.

AMD delivered a clean beat after the close, with revenue of $10.3bn ahead of consensus, datacenter revenue of $5.8bn as the standout, and a Q2 guide of $11.2bn at the midpoint well above the Street’s $10.5bn. Goldman upgraded AMD to Buy with a $450 price target on the same night, building the case that agentic AI drives structural server CPU demand with AMD as an outsized x86 beneficiary, putting their 2027/28 EPS estimates roughly 20% above the Street.

Apple is reported to be weighing Intel and Samsung as secondary chip suppliers beyond Taiwan Semiconductor, a development that sent Intel up nearly 14% and Micron up nearly 11% in Tuesday’s session.

Goldman PB data for May 4 showed US equities net sold at -1.9 standard deviations on a one-year basis, driven by short selling. Single names saw -2.5 SDs with short sells dominating, while macro products saw -0.6 SDs. Gross leverage fell 5.1 points to 307.8%, which sits at the 96th percentile on a five-year basis. Net leverage edged down to 76.0%, a 23rd percentile reading on a one-year basis. De-grossing is continuing even as the market grinds higher.

Goldman’s desk also noted a large unwind of tech longs last week, which likely came from the hyperscaler names rather than hardware, given that the hardware bid has been essentially one-directional since. Momentum broke out again Tuesday, driven by the semis and AI long leg. The semis long/software short pair was one of the worst-performing thematic pairs on the day. Market liquidity has improved with S&P top-of-book depth at $11.15 million, up 32% versus the 20-day moving average.

The three things to watch today are the Treasury refunding language at 8:30 am, the ADP print at 8:15 am, and the 30-year yield. Goldman’s desk flagged 5% on the long end as a significant level, with bond vol beginning to tick higher. If JPM is right that the refunding removes “at least” from coupon guidance, intermediate yields move higher, and that has historically been a larger speed limit on equity appreciation than oil. With gross leverage still elevated and the semis-led momentum trade extended, a backup in rates today ahead of a softer NFP Friday would be an uncomfortable combination.

My Take

The Project Freedom pause is being priced as a step toward resolution, and I think that is premature. Iran’s president called negotiations impossible on the same day Trump cited great progress, the Strait is still holding over 1,550 vessels hostage, and the UN resolution that could actually change the calculus requires Russia and China, neither of whom shows any inclination to cooperate.

The oil inventory picture is not getting the attention it deserves, with global commercial refined product stocks at 45 days of demand versus 50 pre-war and European jet fuel at risk of falling below the IEA’s shortage threshold in June.

The refunding announcement at 8:30 am ET is what I am watching most closely today. If Treasury removes “at least” from its coupon guidance, JPM thinks intermediate yields move higher, and that matters more for this market than any single data print or Project Freedom headline.

More on positioning and specific names below the paywall.