Breakfast Bites: Market awaits the Fed as Monetary meets Fiscal

Fed decision at 2pm ET; Market Volumes are low; Global Bond Yields are surging

Rise and shine everyone

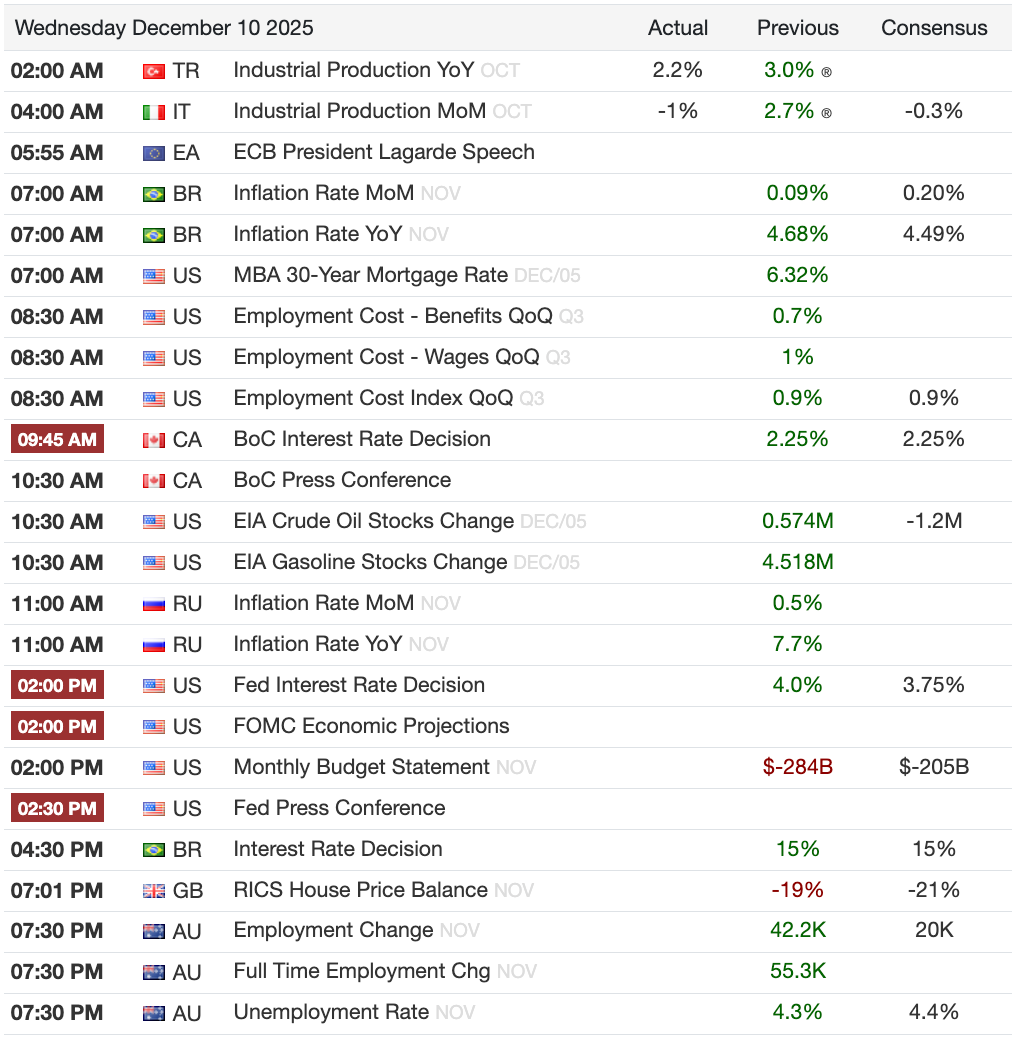

We have a big day ahead of us! We get rate decisions from:

The Fed (25 bps cut expected; Watch dot plot and Summary of Economic Projections)

Bank of Canada (Hold expected)

Central Bank of Brazil (Hold expected)

We also get earnings from Oracle and Adobe. Oracle will be important, and we should look for them to shed more light on their plans surrounding capex, and financing that capex.

Morning Macro Briefing

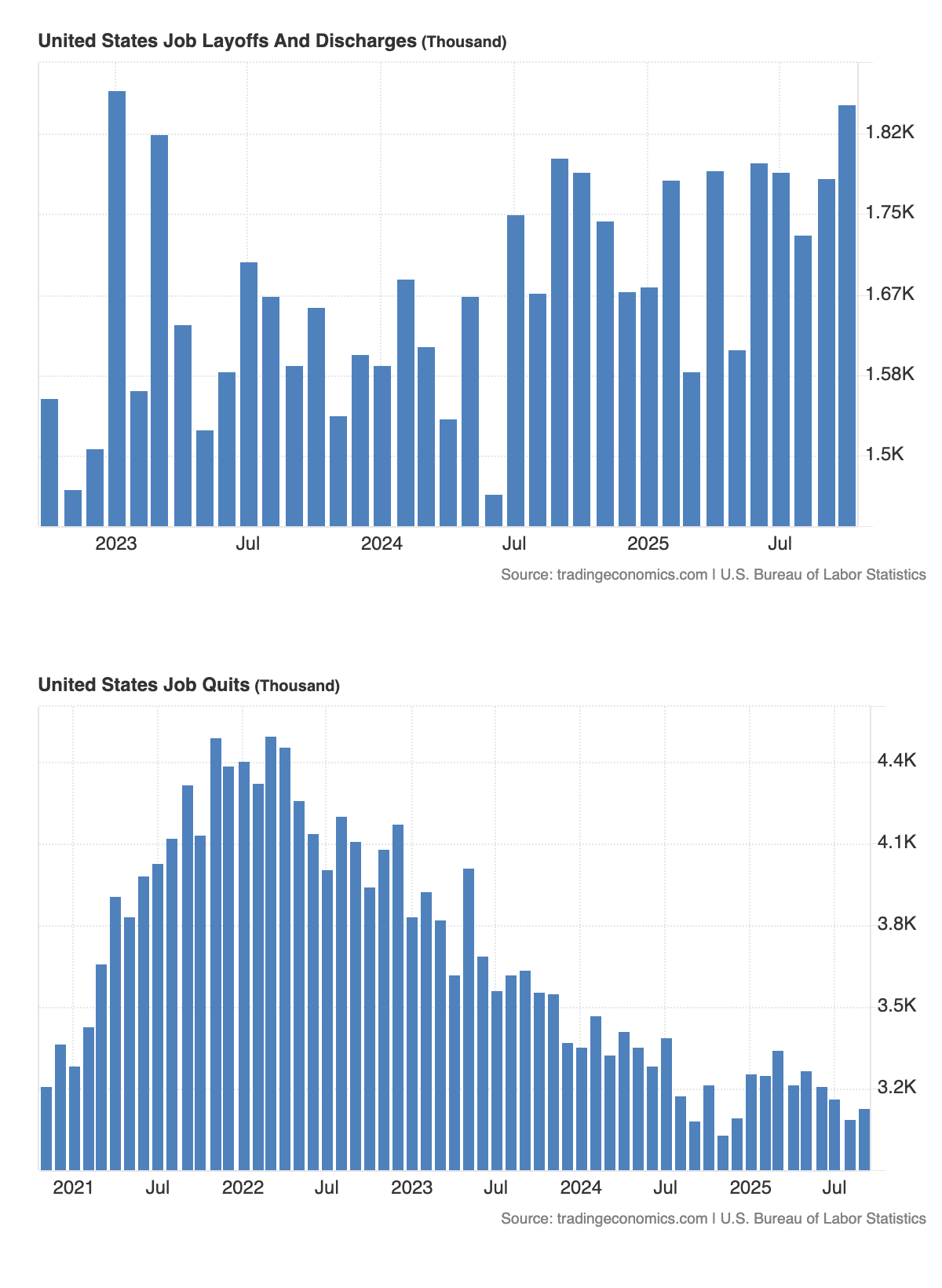

Yesterday’s JOLTS readout showed Job Openings improving, going from 7.227m in August to 7.670m in October. This headline number caused a spike in the 2Y yield, meaning people were pricing in a more hawkish Fed. But below the surface, the layoffs also spiked, and the Quits Rate came in at the lowest since 2020. Remember, people don’t quit their jobs in a strong job market.

Today, we also get the Employment Cost Index for Q3. The Fed looks at this number quite closely because it tells us how sticky core inflation could be. We’ve seen the index move lower since the spike in 2022, but it’s now leveling off, and at a level higher than pre-Covid times. Technically, this should be the case because inflation has brought about a permanent increase in price over the last 5 years, and we’re still seeing positive inflation, which means prices are not going down, they are just growing at a slower pace.

Finally, the Fed. We’ve done our preview on Monday and wrote about it yesterday as well. We’re seeing the market take a bit of a pause before the Fed as well because we’re expecting a “hawkish cut”.

Economic Outlook - Monetary meets Fiscal

Global bond yields are pricing in slower cuts in 2026 because of stronger economic growth, with a possible return of inflation. We’ve already seen Australia even talk about hikes!

We’re gearing up for a deluge of fiscal spending, and that comes with the risk of higher inflation. Then we have the tariffs in the US. Even if some get slashed by the Supreme Court, some may continue. Worse still, if they do get slashed, there may be a “refund situation.”

Easing drastically at a time when fiscal spending is also hitting the economy could make inflation even worse. Finally, the fiscal spending in most cases is very lopsided. They don’t benefit the low-income consumer. Wealth and spending will be even more in the hands of the top 10-20%.

China Inflation

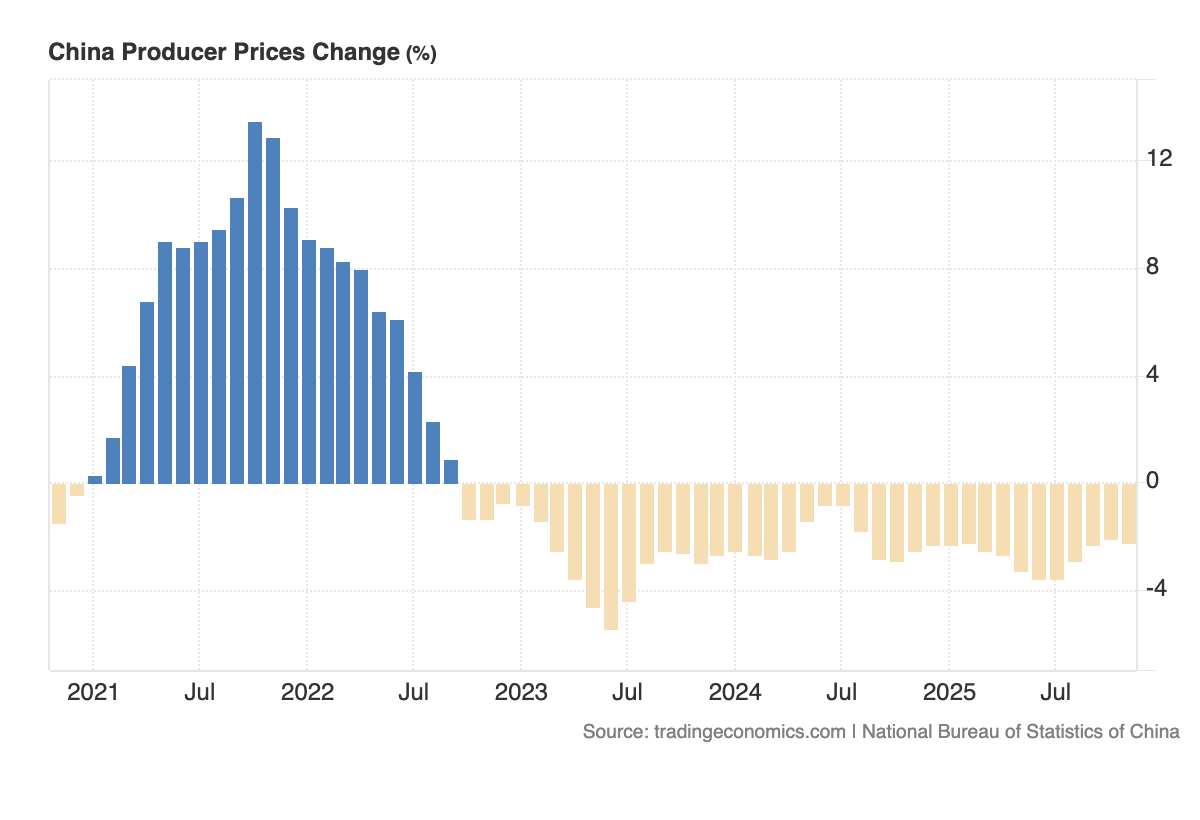

The big macro data in international markets was China’s Inflation report. China is moving out of its deflationary situation, at least partially. YoY Inflation came out to 0.7% from 0.2%, while the MoM readout was still negative at -0.1% from 0.2%. PPI, however, continues to track negative, worsening to -2.2% from -2.1%.

GS Financials Conference - JPM

JPM emphasizes that AI is already lifting efficiency, with operations specialist productivity running near 6% this year versus the historical 3% pace. Management estimates productivity can rise 40 to 50% over the next five years as digital self-service, process automation, and AI-assisted workflows scale across the bank. The takeaway is that JPM is treating AI as a present driver of cost efficiency and throughput, not a distant narrative.

However, this AI expansion also comes at a cost. Alongside branch expansion and other growth-related items, JPM now expects full-year expenses in 2026 to be about USD 105billion, up from estimates for 2025, and meaningfully higher than analyst estimates. The stock price fell -4.66% yesterday.

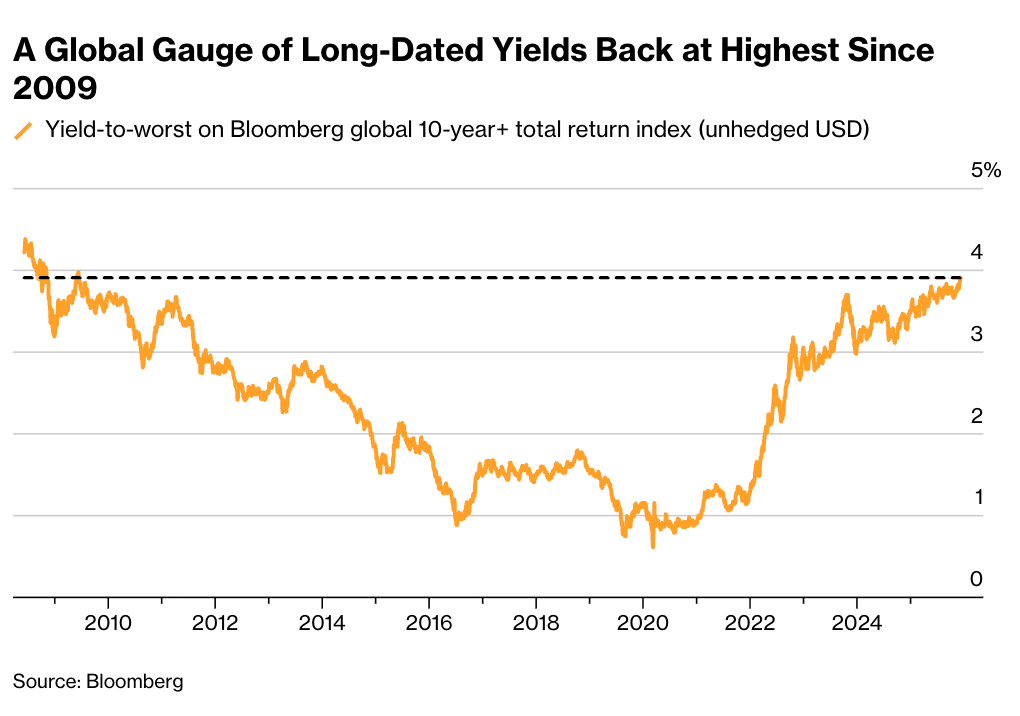

Chart of the Day - The Global Yield Curve

We showed the US yield curve steepening yesterday, and we talked about global bond yields moving higher. This is a great chart from Bloomberg showing the steepening of the Global Yield Curve.

Calendars

Market Prep

Trading on Fed day should always be done with caution. Markets are taking a breather, as we see higher global bond yields. (discussed in the Macro Section above)

I expect the 25bp cut to lead to a spike upon announcement, but in usual fashion, the first reaction to the Fed could be people taking off hedges. Moreover, if we do get hawkish rhetoric, it will be as the Summary of Economic Projections is being digested, and during Chair Powell’s press conference.