Breakfast Bites: Long-term yields put pressure on stocks

US markets grapple with corporate news; Tactical Watchlist performance update and discussion

Rise and shine everyone

We’re seeing upward pressure in yields, which is weighing on global equities. The macro discussion is obviously surrounding the Fed, and the BoJ to a certain extent. Today’s macro focus for the US will be on the JOLTS data.

Morning Macro Briefing

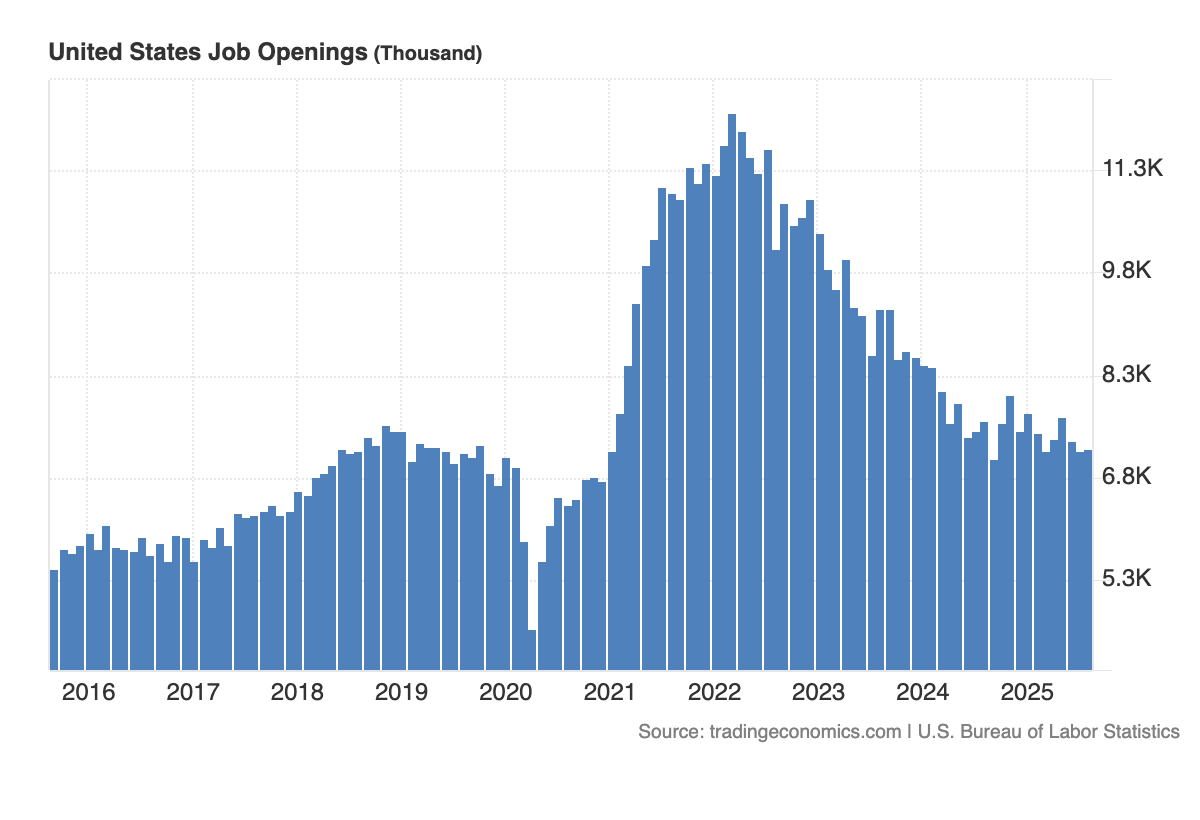

The JOLTS (Job Openings and Labor Turnover Survey) is set to be released at 10 am ET. Now, the calendar suggests we will get September and October’s data releases. Let’s look at what we got through August.

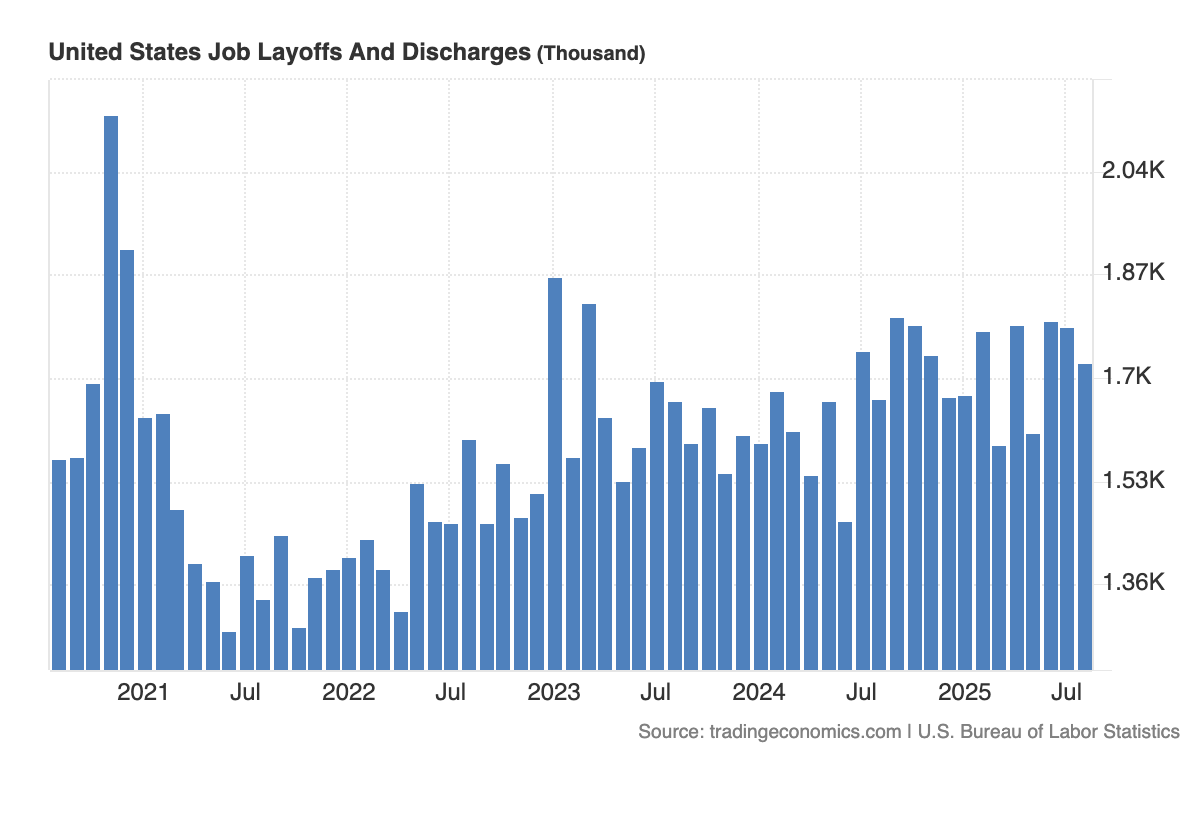

We’ve been seeing job openings steadily decline. But if you look at the longer-term picture, we are actually hovering around pre-COVID levels. This is what we wanted to see because the job market had become too tight. And then when we look at layoffs (below), we see that we are around average levels. So the low-hiring, low-firing thesis is holding, thus far.

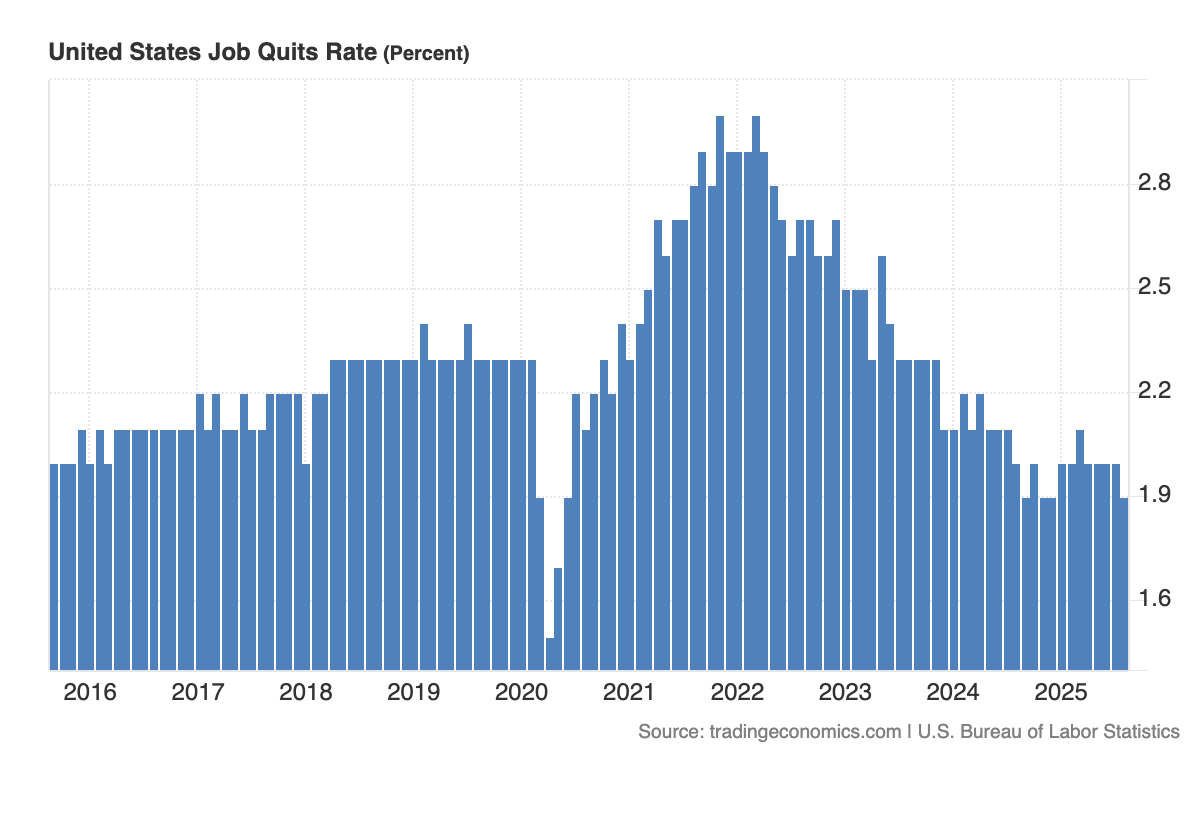

The final piece we would look at is the Quits rate. We can see that this is coming down slightly below the longer-term average, and that suggests some weakness. Fewer people quitting could suggest that they are not confident enough in outside job prospects - a sign of the low-hiring that we keep hearing about.

But most of the discourse is around the Fed now. While the Fed Fund Futures are still pricing in an 89.6% chance of a 25-bps cut announced on Wednesday, speculation continues that the Fed will remain divided on the course of action. The dot plot will be important to watch. While we may get a cut, there could be a hawkish lean because of the lack of data, weakness in the labor market, and inflation that leans sticky.

Australia had its rate decision yesterday, and as expected, it was a hawkish hold. While the official RBA statement was benign, Governor Bullock explicitly took cuts off the table during the Q&A session and said that they are open to hikes if inflation continues to run hotter than expected.

It’s looking like the BoJ will still hike next week. Japanese yields continue to push higher, and while the yield curve softened slightly, we’re not getting any news that suggests a hold.

China’s December Politburo meeting, held yesterday, Dec 8, set the tone for 2026 and made clear that policymakers are in no hurry to deploy broad stimulus. The tone was more confident on 2025 growth, and we’re still not getting any discussion on the weak consumption levels and the troubles in the property market. The focus instead stayed on technology, security, and long-term productivity themes, consistent with recent policy direction.

With the Central Economic Work Conference expected later this week in mid-December, markets are looking for whether policymakers reinforce today’s cautious stance or shift toward more explicit support. For now, the commitment to developing new growth engines and boosting high-tech manufacturing suggests that industrial policy will keep guiding the cycle.

Chart of the Day

This is a very interesting chart from Goldman Sachs, as a forecast for the coming years. GS sees equity market growth being led by EMs and the Asia Pacific. Earnings growth continues to remain the key driver. They note, however, that valuations continue to remain expensive across the board, but expect them to compress (that’s why they are negative).

“We see attractive global equity returns driven by economic and earnings growth, improved productivity and profitability, and strong shareholder returns. In particular, we expect higher nominal GDP growth and structural reforms to favor EM, while AI’s long-term benefits should be more broad-based beyond US tech. We remain optimistic on US equities, but high levels of concentration and full valuations underscore the need for diversification.”

Calendars

Market Prep

We saw a spike in the US yield curve yesterday as 10Y yield pushed to its highest level in nearly two months.

The grind up in yields weighed on equities, but that’s not the only thing that happened.