Breakfast Bites: Korea Trips the Wire

Seoul circuit breaker, the AI unwind accelerates after Fed Hike priced in, and CPI lands Wednesday.

Rise and shine everyone

The Kospi triggered a circuit breaker this morning, falling as much as 8.8% before trading was halted. It is Friday’s New York trade playing out in a market where retail leverage is extreme and the exit is narrow.

Friday was not a fundamental reassessment. It was a crowded, over-leveraged trade finding a catalyst. Ten stocks drove 69% of the S&P’s 19% rally since March 30. Call skew on SPX and NDX was at the 100th percentile. Put skew was at zero. When something is that concentrated and that leveraged, modest profit-taking turns mechanical, and mechanical selling accelerates the lower you go.

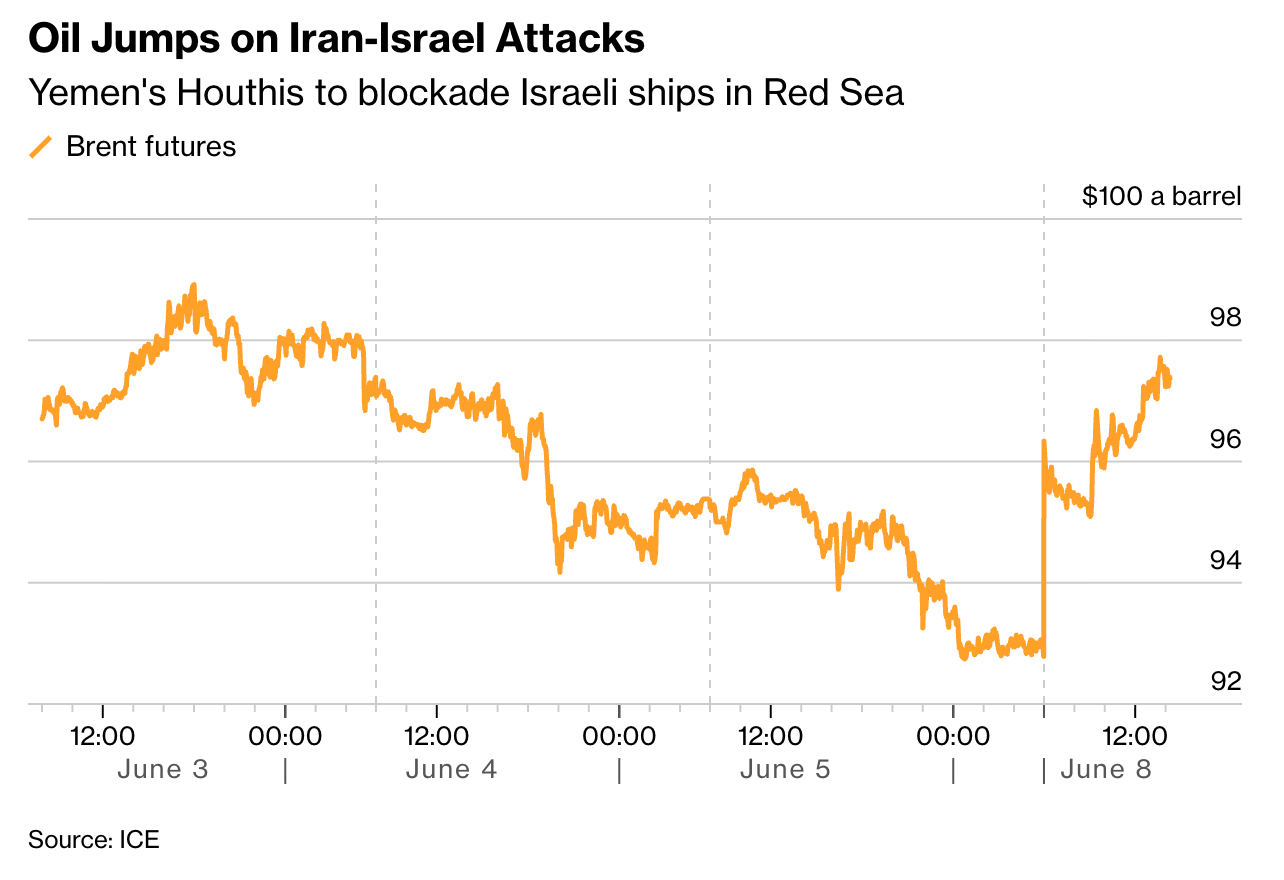

The geopolitical picture adds noise but not yet a new regime. Israel identified a missile launched from Yemen overnight, Saudi officials are monitoring near Riyadh, and Trump is playing it down with deal talks described as ongoing. Oil is only modestly higher. The market is saying this is still within the negotiating process.

Three things define the week.

Wednesday’s US CPI. Goldman is calling 0.17% on core month-on-month versus a 0.3% consensus and a prior of 0.4%. A soft print collapses the 43% implied Fed hike probability and is the single biggest potential catalyst for relief across risk assets.

Thursday’s ECB. A 25bp hike to 2.25% is expected and fully priced. Back-to-back rate hikes from major central banks matter for global financial conditions, particularly for energy-importing economies already under pressure.

Positioning. At least half the CTA long base in NDX is estimated to remain intact. Another 90bps to 2% of downside triggers broader systematic unwinds. The level matters this week.

We have a few tech names on our tactical watchlist (behind the paywall below). I would consider looking into adding to some of these names on the pullback.

Morning Macro Briefing

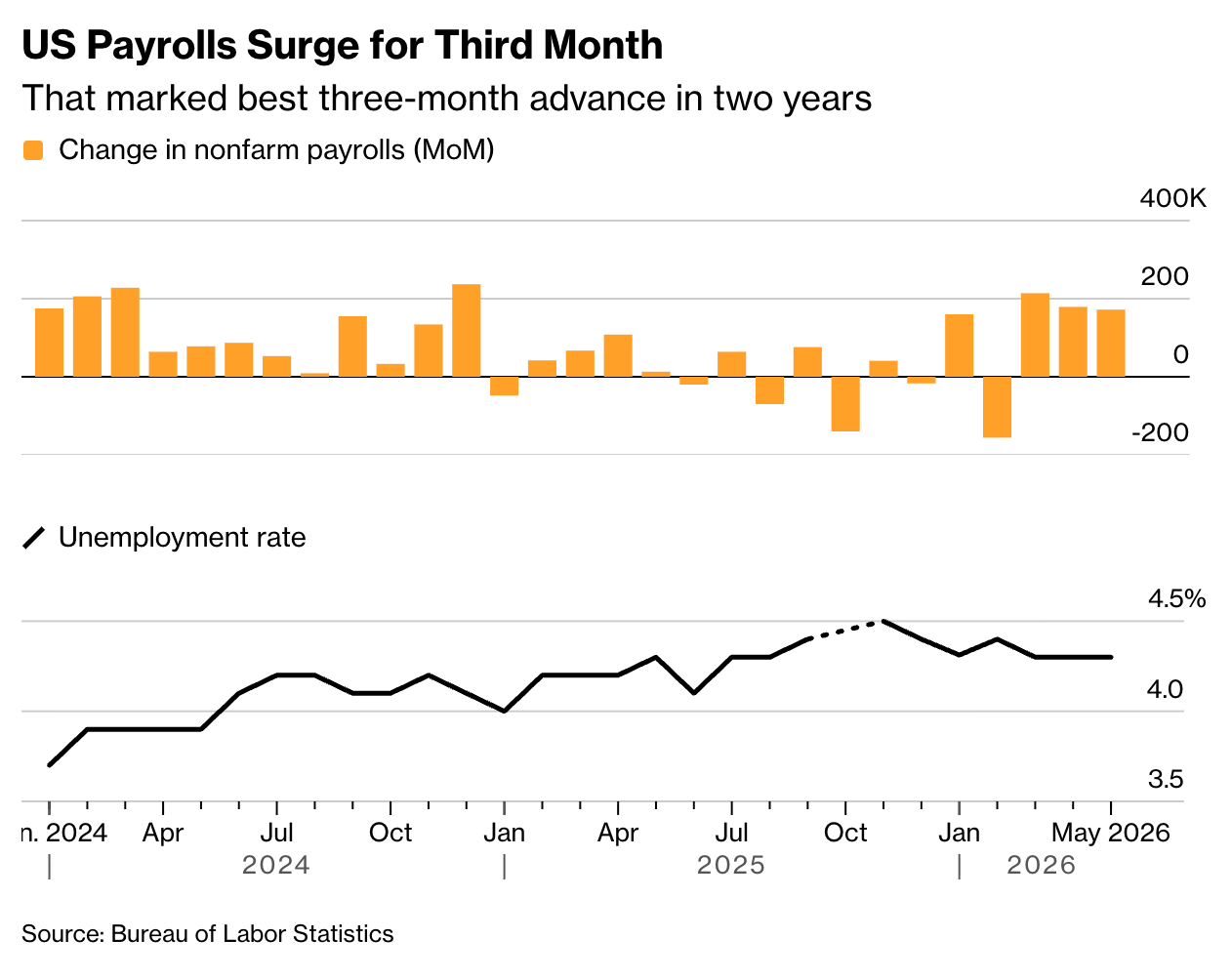

Friday’s nonfarm payrolls report topped all estimates. 172,000 jobs added in May, unemployment steady at 4.3%, with March and April revised higher for the strongest three-month advance in more than two years.

The headline was led by leisure and hospitality, which added 70,000 jobs, the most in over three years, partly boosted by World Cup hiring. Healthcare and local government also contributed at a firm pace.

The AI angle is within the construction numbers. Nonresidential construction employment rose for a seventh consecutive month, directly tied to the data center build-out, with construction spending on data centers eclipsing $50b in April for the first time. Manufacturing also added jobs, driven by data center supply chain demand and defense production. The physical infrastructure of the AI boom is now a meaningful labor market driver.

The one note of caution was wages. Average hourly earnings rose just 3.4% year-on-year, the slowest pace since 2021, and with inflation running above that level, real wages are under pressure. Two-year yields jumped around 10-11 basis points to 4.14% on the print. Markets moved to fully price a Fed hike by year-end.

Israel identified a missile launch from Yemen overnight, and Saudi officials are monitoring Al-Kharj near Riyadh. Trump is publicly dismissing the escalation and framing deal talks as continuing.

Oil is only modestly higher despite the flare-up, which is itself a signal. OPEC+ confirmed an additional 188K bpd output increase in July, in line with expectations, providing a modest offset on the supply side.

The ECB will likely hike 25bp to 2.25% on Thursday and this is fully priced in. Canada will likely hold at 2.25% on Wednesday. Goldman’s standout call for the week is US core CPI at 0.17% month-on-month versus 0.3% consensus. If correct, the rates repricing that followed Friday’s jobs data partially reverses and the narrative shifts from “the Fed hikes” to “the data is turning.”

USD/JPY is holding above 160 with Japanese officials on the sidelines. Japan’s Q1 GDP revision was mixed, the deflator revised lower with capex not as bad as feared, and bank lending accelerating. China’s FX reserves rose in May on exchange rate conversion and asset price movements. Both Japan and Indonesia are seeing broad-based selling on risk aversion this morning.

Chart of the Day

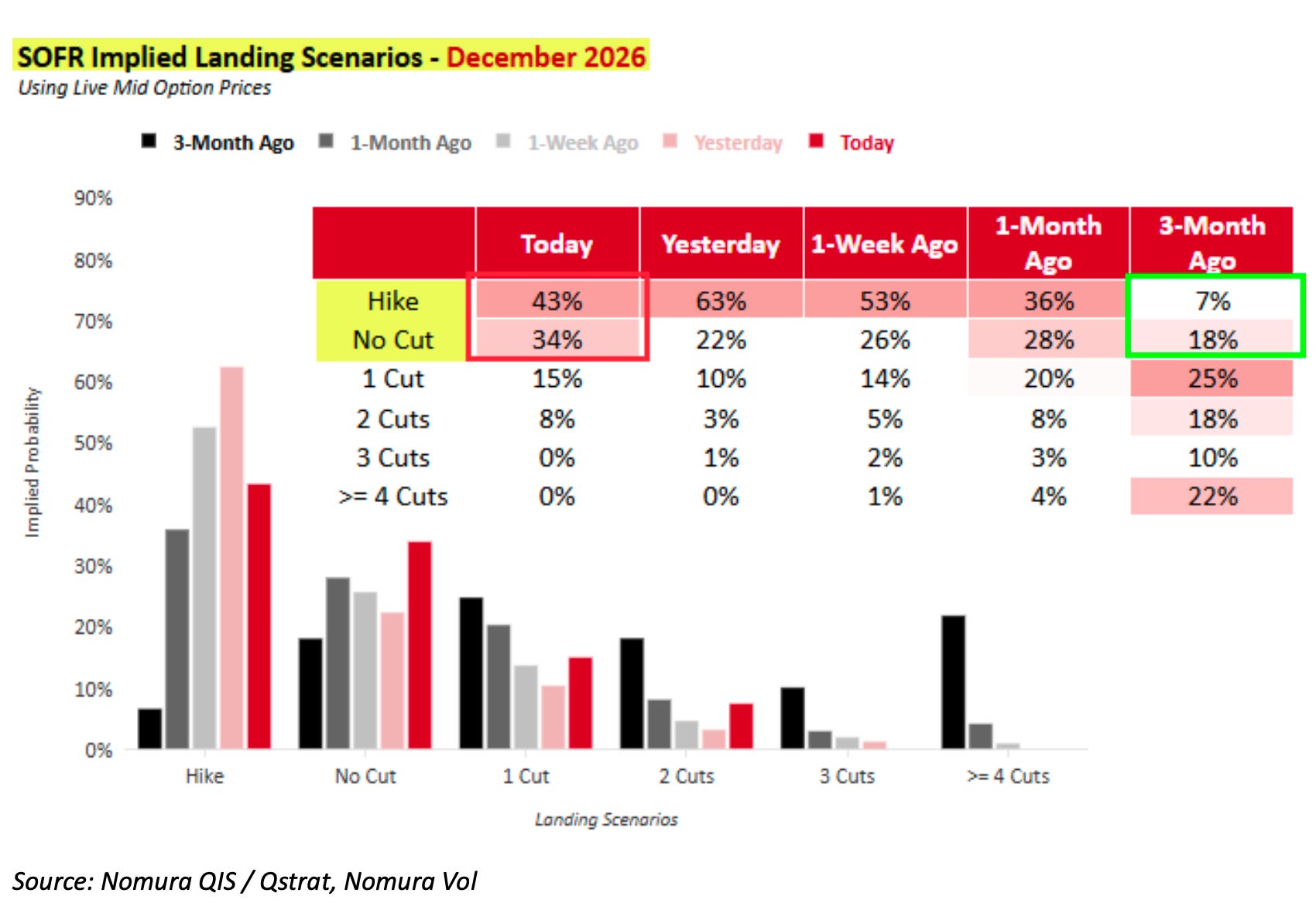

Three months ago, markets priced a 7% probability of a Fed hike by December 2026 and a 22% chance of four or more cuts. Today, the hike probability sits at 43% and the no-cut scenario at 34%.

That is the rates regime shift in a single visual. Every asset class is short rate volatility. Wednesday’s CPI is the next test of whether this repricing extends or begins to fade.

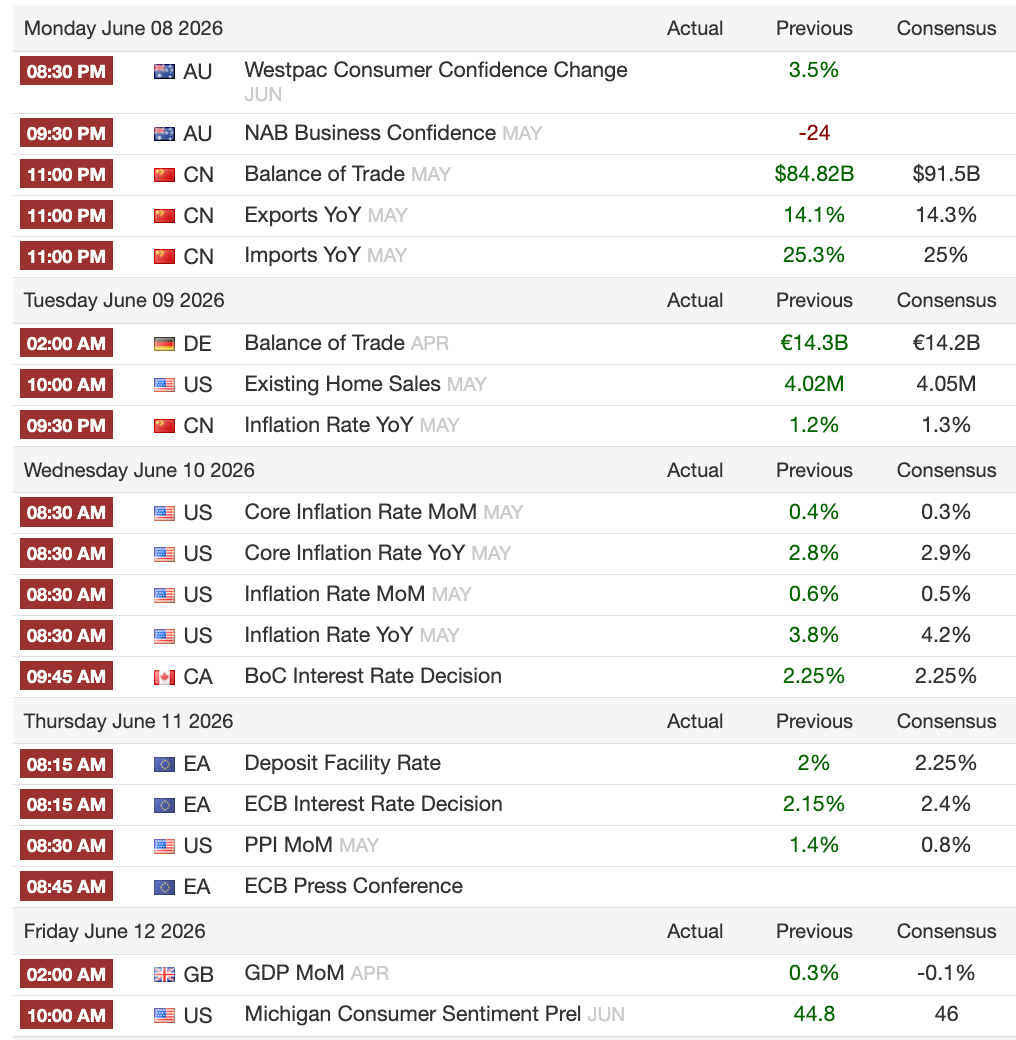

Calendars: The Week Ahead

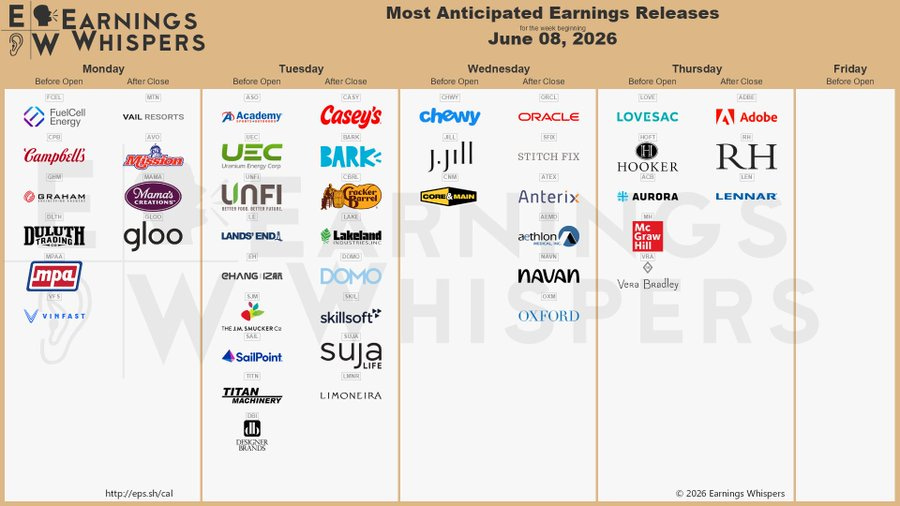

This week’s calendar is dense with macro risk. US CPI on Wednesday and the ECB on Thursday are the two events with the most potential to move markets globally. On the earnings side, Oracle reports Wednesday after the close and is the one to watch, with AI infrastructure demand signals from its cloud segment carrying extra weight given where semis are trading. Adobe reports Thursday before the open.

Monday June 8, no major releases

Tuesday June 9, Australia May NAB Business Confidence; US April Trade Balance; China May Trade Balance; Kenya central bank rate decision

Wednesday June 10, Japan May PPI; China May CPI and PPI; US May CPI; Canada rate decision (hold at 2.25%)

Thursday June 11, Korea May unemployment; ECB rate decision (expected +25bp to 2.25%); US May PPI; US OPEC Monthly Report

Friday June 12, UK April GDP; US June preliminary Michigan Consumer Sentiment

Market Prep

US equity futures came into Monday oscillating between -0.1% and +0.2% through Asian trading. Cautious, but not in free fall. The Kospi is a different story, down as much as 8.8% with a circuit breaker triggered, and the Korean won rebounded from its weakest level against the dollar since March 2009 after the government announced currency support measures on Sunday.

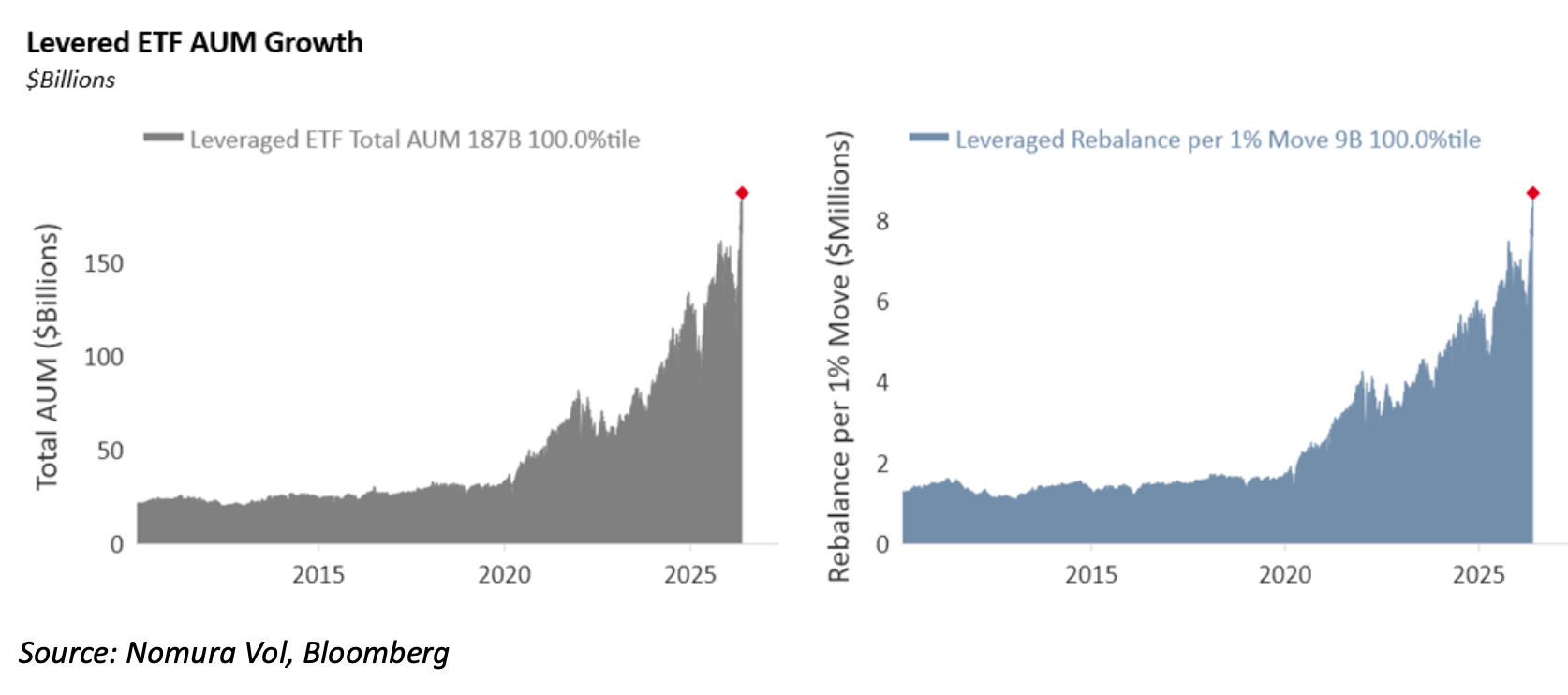

Friday set the table for everything this week. The NDX fell 4.8% in a steady grind lower, the 13th worst sigma decline since 1985 at roughly 4.7 standard deviations. SPX option gamma sat at $9.6bn, the 99th percentile since 2014, but Friday’s move demonstrated the limits of that long gamma cushion. When the spot move is large enough, dealer hedging becomes irrelevant. L&I ETFs sold over $12bn of NDX on Friday, the largest on record.

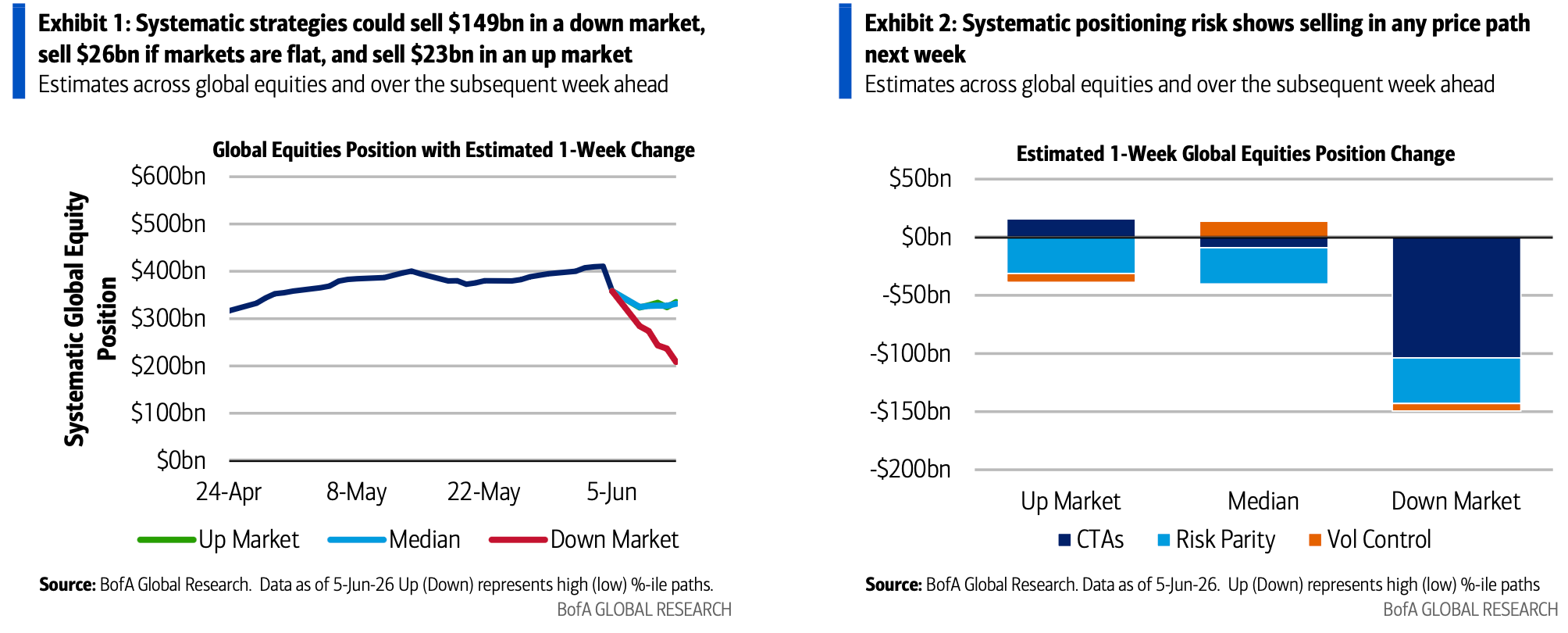

BofA’s systematic flow model shows net equity selling in every price path over the coming week, roughly $149bn in a down scenario, $26bn if markets are flat, and $23bn even in a bull scenario. CTA positioning in NDX came into Friday at maximum long across all time horizons.

NDX CTA stop-loss levels were 4.3% to 6.8% lower from Friday’s open; most risk-averse models likely began deleveraging Friday

At least half the CTA long base is estimated to remain intact; another 90bps to 2% of downside triggers broader unwinds

S&P 500 CTA stop-loss range sits roughly 40bps to 2.6% lower

Russell 2000 triggers run 2% to 5% lower

LevETF AUM sits at all-time highs of roughly $187bn with 87% of exposure in AI tech leadership. The pro-cyclical rebalancing flows turn aggressively the other way as spot falls. The lower we go, the more they are forced to sell.

The Korea structural detail matters for understanding the severity of this morning’s move. Margin debt hit a record 38 trillion won as of end-May. CSOP’s SK Hynix leveraged ETF became the world’s largest single-stock leveraged ETF. Samsung Asset Management’s equivalent fell 20% on Friday and is down 18% since its late-May launch. Foreign investors withdrew more than $10bn from the Kospi on a net basis last week and have been net sellers every session for a month. Goldman’s Timothy Moe called it a technical correction in a longer-term bull market with fundamentals intact, and Goldman raised its Kospi target to 12,000 from 9,000 last week. The long-term framing is probably right. The short-term path through forced selling is less clean.