Breakfast Bites - Jobs Friday

Trump-Musk feud pulls markets lower; Limited progress on trade talks; ECB may have reached neutral

Rise and shine everyone

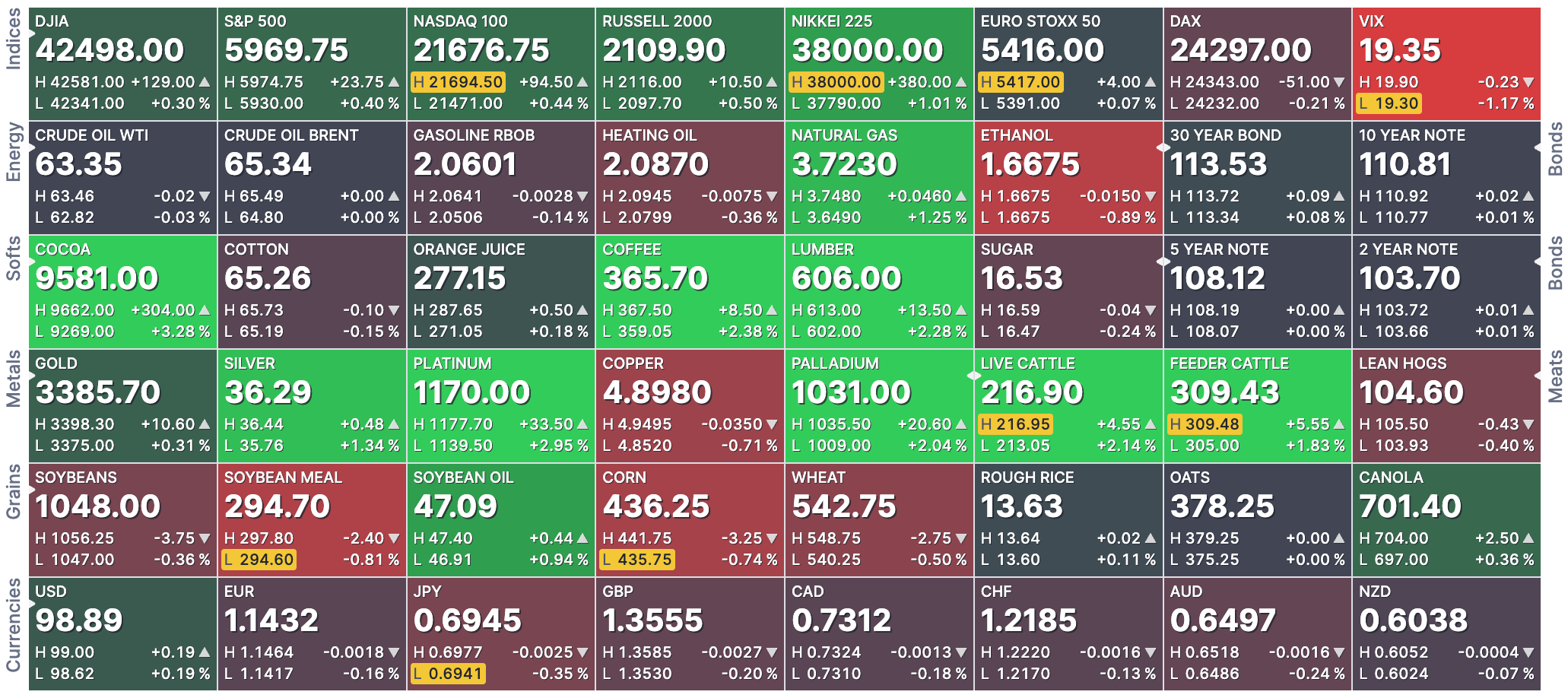

Yesterday was wild. Things between President Trump and Elon Musk got heated, with each calling the other one out. Tesla fell -17% at one point. Eventually, the broader markets also took a hit and sold off after some strong accusations from Musk against the President.

Today’s focus however, will be on the US payroll numbers, out at 8:30 am ET. The consensus is for 125k jobs added but, after recent JOLTS and ADP numbers some analysts have reduced their forecast. GS forecasts 110k jobs added. May could show the first signs of the Trump Tariffs weighing on the employment market.

The GS reaction function for the market suggests a very low print could push the market quite a bit lower.

But, what’s more interesting is that a shaky print here could actually put the Fed back on alert. It definitely makes the Fed’s job harder to hold rates with the job market in trouble. I’d ruled out a summer cut, but we could be looking at July, if the numbers are truly terrible.

US Equity Futures have gained some ground since yesterday’s sell off but not with a lot of conviction. Yesterday, we saw SPX cross 6000, and progressively sell off from there. With the market on unsure footing, we really need a solid NFP print for the market to move back to those levels.

A cordial phone call between President Trump and President Xi gave a modest lift to sentiment, with the Nikkei rising 0.5%. However, no major progress was made on key trade issues. Both leaders said talks would continue, potentially with a face-to-face meeting. The tone was overshadowed by reports that Iran ordered materials from China capable of producing ballistic missiles.

Japan proposed car tariff cuts to the US and introduced a new package aimed at reducing dependence on China, including rare earth supply chain measures. Trade rep Akazawa met US Commerce Secretary Lutnick in DC for nearly two hours, discussing non-tariff barriers and trade expansion.

India surprised markets with a 50bps cut to the repo rate and a 100bps cut to the cash reserve ratio. Despite the dovish move, the RBI shifted its stance back to Neutral. Indian 10-year yields dropped 6bps on the news.

In Europe, Q1 GDP was revised higher and April retail sales beat estimates. But weak German and French trade and industrial data weighed on the DAX and CAC. ECB speakers echoed Lagarde’s tone on nearing neutral rates, though July’s direction remains uncertain. Holzmann was the lone dissenter in the last decision, and the Italian-German 10-year spread hit a post-crisis low.

Lululemon fell -22% after hours following weak guidance in its earnings release.

Calendars

(news taken from Reuters, FT, Bloomberg; Calendar from Trading Economics)