Breakfast Bites: It’s Warsh Day

The Fed holds but the dot plot speaks; BofA’s survey hits sell-signal territory; oil drops 5% on the Iran deal.

Rise and shine everyone

It’s Kevin Warsh Day. I know I’ve been talking about the new Fed Chair quite a bit this week, but to be fair, I think this position is one of the most powerful positions in the world. And first impressions matter.

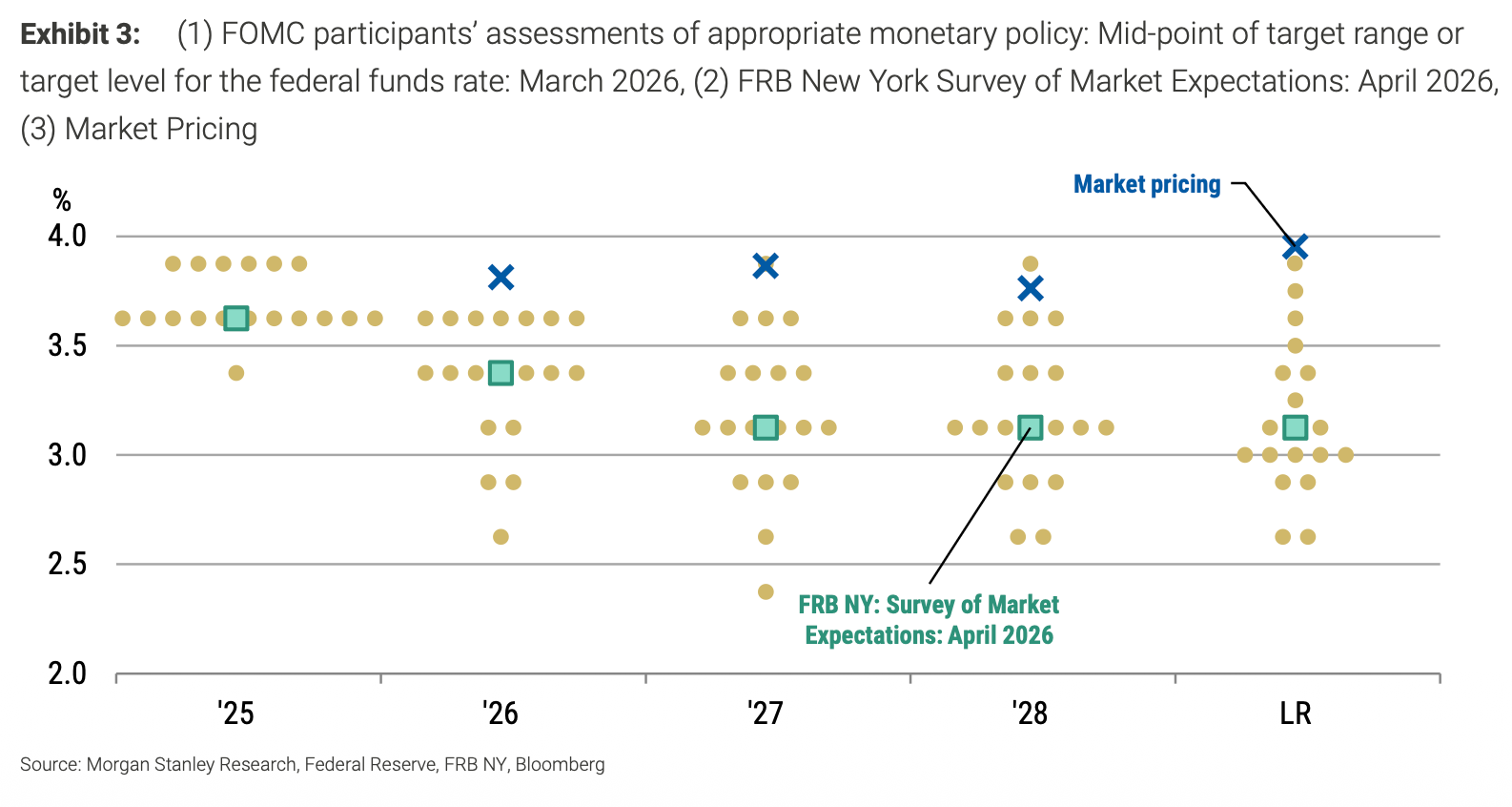

On top of that, we have the Summary of Economic Projections (SEP) being released today. We will see how the dot plot plays out, i.e., what everyone is thinking in terms of the terminal rate. So far, we’ve been thinking that the neutral rate lower than the current levels, meaning there’s room to cut. But a lot has changed in the past three months.

What we saw from the last meeting was a Fed that’s turned more hawkish. With inflation re-accelerating almost 1% in the last couple of months, and remaining above the 2% target for almost 5 years, many on the committee have started to lean away from cuts entirely. The nail in the coffin was the strong labor market report. That’s a notable shift for the markets.

Bond markets are not happy either, and we’re seeing premium being priced across the curve. Today will determine which way that premium goes - up, down or sideways.

We know that there will be HOLD today, but three things we’re looking out for in today’s Fed Meeting:

The Statement & Dot Plot - Will the statement remove the easing bias? Probably so. The dot plot is more of a given, we’re likely to see more hawkishness. Then comes the inflation, labor and growth forecasts. I think inflation will be changed, labor steady and growth steady - just my 2 cents. Watch the USD - higher for hawkish, weaker for dovish.

Fed Independence - We’ve had concerns about how independent Warsh will be from the White House, and whether he will buckle under pressure and lean dovish. I also wouldn’t want him to comment too much on the peace deal or the war, given that’s a more political standpoint.

Which Way Warsh Leans - Warsh has been known to be an inflation hawk, meaning he prioritized keeping inflation low, over labor market concerns. Over the last few months though he’s been talking about AI productivity gains allowing the economy to expand without overheating - so a more dovish view. Regardless, I don’t expect him to signal forthcoming hikes.

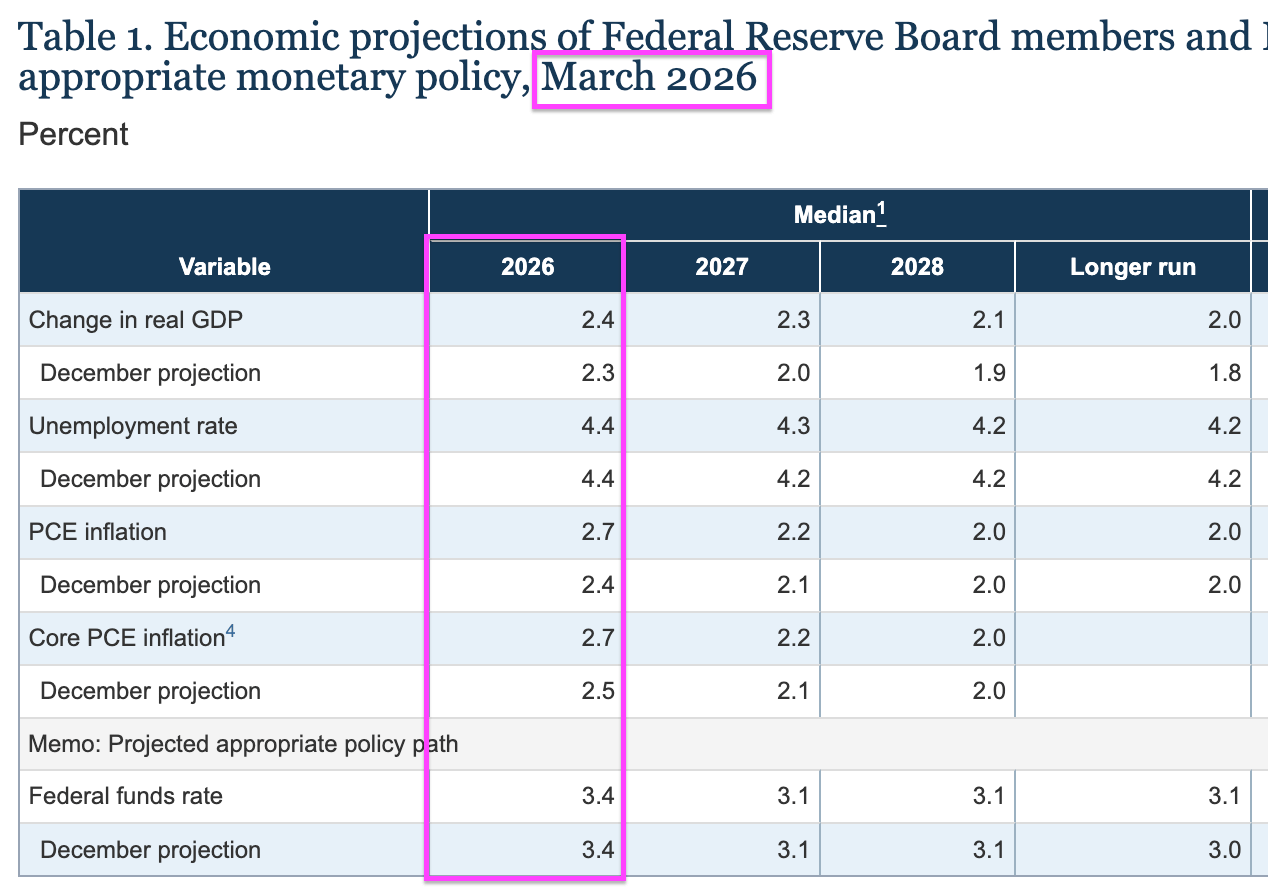

Here’s a recap of the March SEP:

Morning Macro Briefing

The US-Iran deal, reported by the Wall Street Journal, would allow Tehran to begin oil sales immediately under the MOU terms. WTI closed at $76.55, down $4-plus on the session. Qatar LNG ramp-up is also underway, with JPM’s commodities team estimating 83% of full capacity within two to three months. The headline is dramatic but the underlying supply math is more gradual.

Morgan Stanley expects the Fed to remove easing bias from today’s statement, replacing the prior “extent and timing” language with the more neutral “any adjustments.” Their updated SEP projections put 2026 core PCE at 3.0%, up 0.3 percentage points from the March projection, with the median fed funds dot for 2026 moving to 3.6%. Up to four members are expected to project a rate hike this year. The Atlanta Fed Wage Growth Tracker is running at 3.8%, the slowest pace since December 2021. Three-month annualized average hourly earnings are at 2.8%, so there is real softening in underlying wages even as the headline labor market holds firm. That internal contradiction is exactly what makes this FOMC interesting.

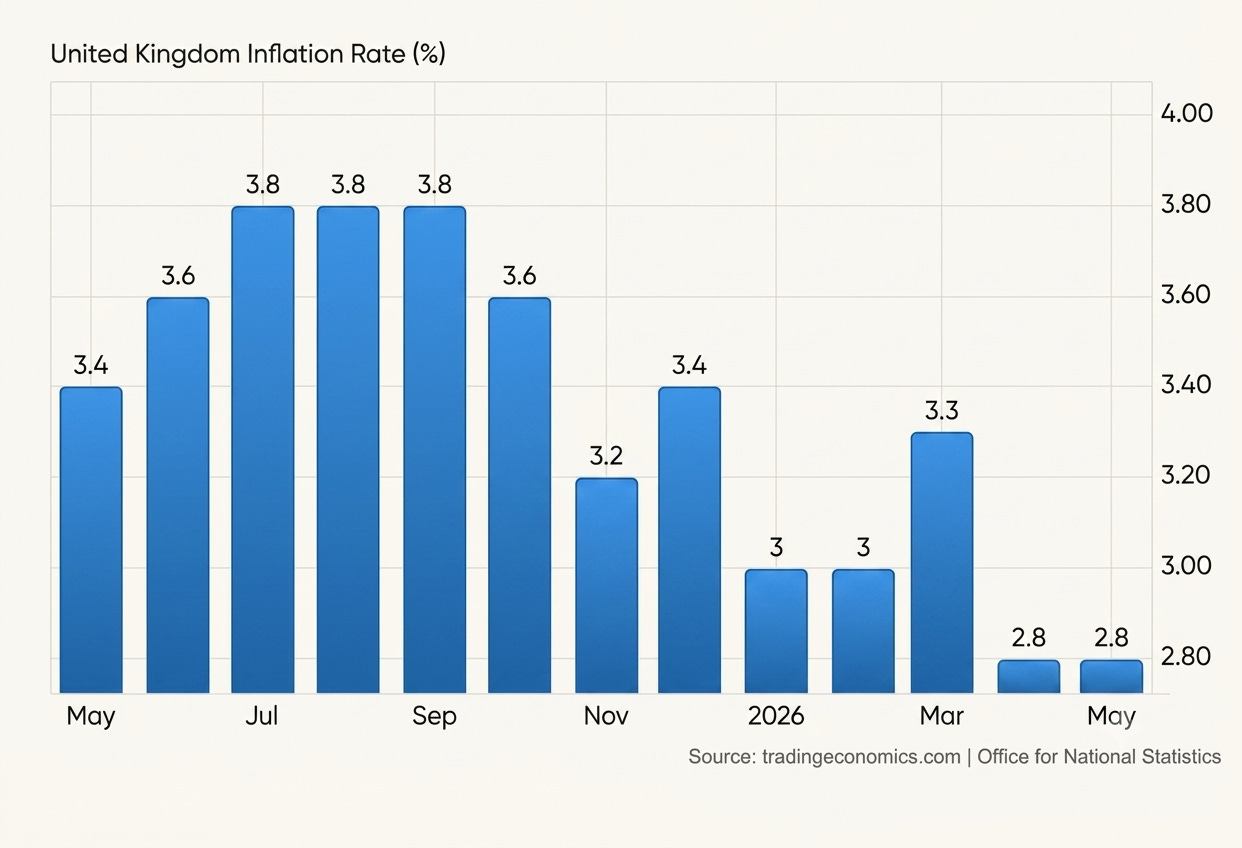

UK inflation came in softer than expected in May, with the headline rate holding at 2.8% against a 3% consensus, the monthly rise of 0.2% undershooting forecasts of 0.4%, and core inflation ticking up to 2.6% but still below the 2.7% forecast.

This gives the Bank of England cover to hold rates at 3.75% on Thursday, which markets already price as the overwhelming favorite at around 96% probability. The bigger question is tone rather than action, since the MPC's April vote saw one dissent in favor of a hike and the Bank's projections still show inflation rising further through Q3 and Q4 on energy related pressure from the Middle East conflict. The May data is unlikely to be soft enough to shift the committee toward signaling future cuts, and the hawkish dissent could persist given the pickup in core and services inflation.

China’s annual Lujiazui Forum opens today, running through June 18, with Vice Premier He Lifeng and the heads of the PBOC, CSRC, NFTA, and SAFE all scheduled to speak. The focal theme is yuan internationalization. China is launching an offshore yuan repo facility for foreign central banks and sovereign wealth funds, with Shanghai targeting an offshore finance legal framework by end-2030. PBOC Governor Pan Gongsheng also addressed the low-yield environment in China, outlining plans to adjust overnight RRP operations to improve yield curve function.

Japan’s May trade data came in better than expected, with exports growing at the fastest pace in more than three years and imports below forecast. Semiconductor-related exports rose 61.2% year-on-year. Singapore echoed the same theme, with electronics exports up nearly 95% in May. MAS trimmed its 2026 GDP forecast while maintaining the 2027 figure. The tech supply chain is running hot even as end-market demand questions build.

US housing starts fell to their lowest post-pandemic level in May, with building permits roughly unchanged. This is a demand signal, not a supply collapse, and it sits awkwardly alongside the 36% of FMS respondents now assigning a “boom” scenario to the macro outlook.

Chart of the Day

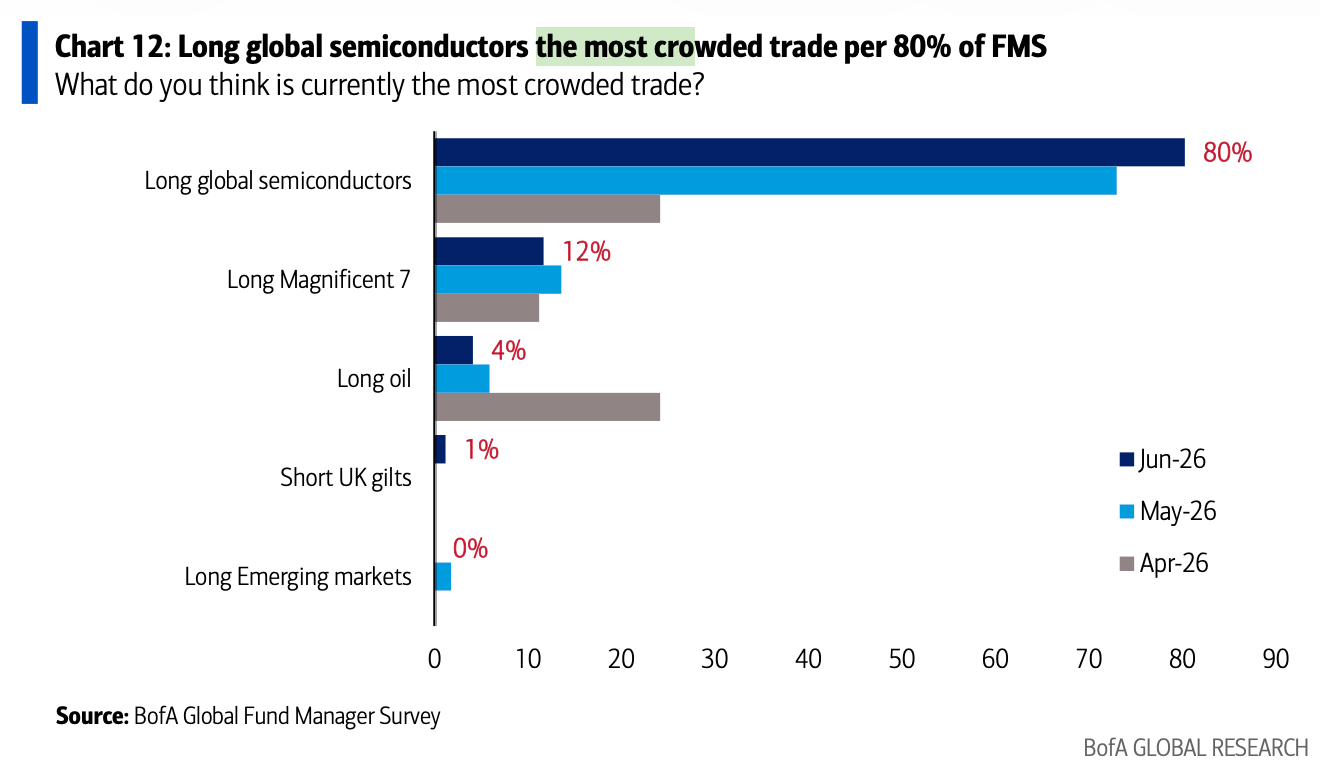

The most important chart today is the BofA Fund Manager Survey’s reading on the most crowded trade. Long global semiconductors now sits at 80% of surveyed managers, an all-time FMS record high. The prior peak was 73% last month. This is not a valuation argument; it is a positioning warning. When 80% of surveyed fund managers representing $540bn in AUM identify the same trade as the most crowded in the market, the asymmetry of any surprise is extreme. The FOMC is exactly the kind of event that could force a flush.

Calendars

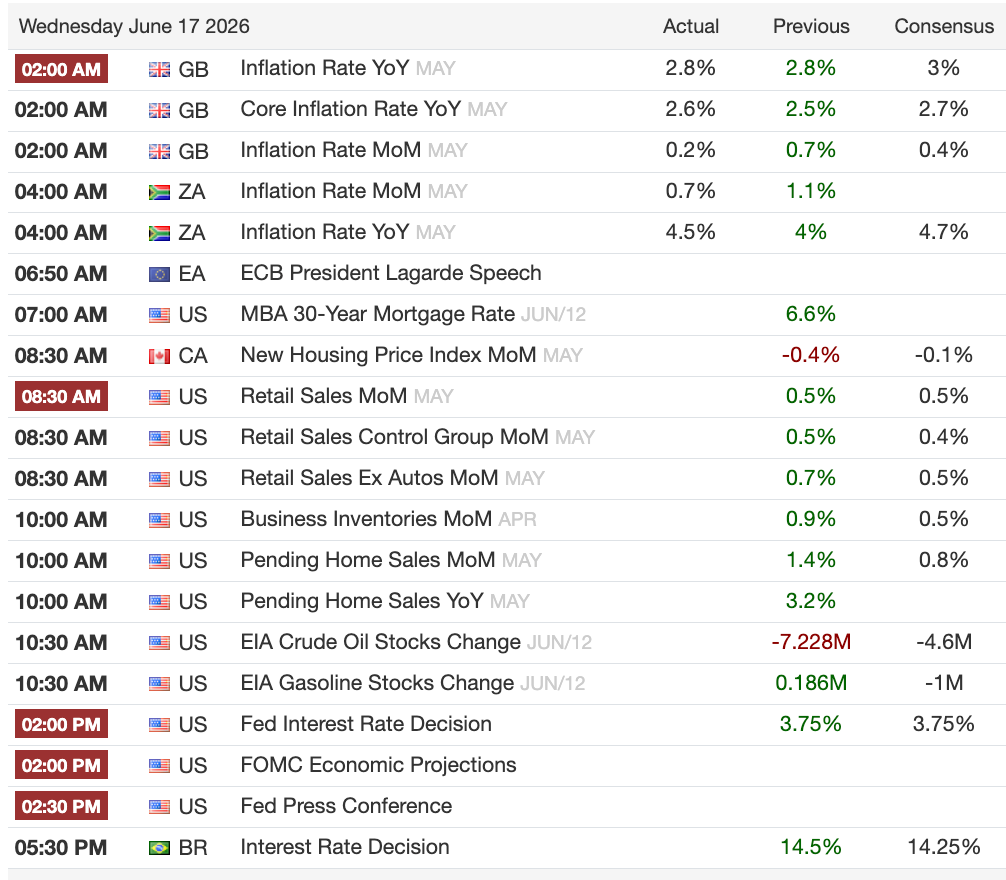

Today’s calendar is effectively one event. The FOMC decision at 2pm ET and Warsh’s press conference at 2:30pm ET will do all the work.

Market Prep

Monday’s tech selloff had no clean catalyst. JPM’s trading desk flagged three overlapping forces: crowded positioning, negative third-party channel checks on AMD showing data center CPU revenues slowing in Q2, and the ongoing fallout from Anthropic’s withdrawal of its Fable 5 and Mythos models. Financials were the standout, with XLF up 1.5%. Hormuz reopening trades outperformed alongside financials.

SpaceX crossed $206 per share, up another 6% including after hours, putting it in competition with Microsoft for fourth-largest company in the world just three days into public trading. Separately, the US Commerce Department is reported to be holding off on blacklisting DeepSeek and 100 other China-linked companies, with Microsoft among the firms considering hosting DeepSeek as a cheaper, controllable model alternative.

On AI infrastructure, JPM’s team raised total AI capex estimates to $5.5 trillion through 2030, up from $5.1 trillion in November 2025. Google and Amazon are each on track for approximately $300bn in capex in FY27, rising to $350bn in FY28. Microsoft is flagged as roughly a year behind on its funding curve with a potential $90-130bn supply gap opening in investment-grade bond markets through FY27-28.

The session heading into FOMC has a layered positioning picture. BofA’s Bull and Bear indicator is at 8.9, above the 8.0 sell signal threshold for the first time in months. The FMS Cash Rule sits at 4.1%, a neutral signal, but barely. Global equity allocation dropped from net 50% overweight last month to net 38%, a meaningful single-month drawdown even if the absolute level remains elevated. Japan flipped from net 13% overweight to net 5% underweight in one month. Eurozone saw the biggest underweight swing since December 2024. The rotation out of expensive, consensus positions is underway, even if no one wants to call it that.

The crowded positioning extends into currency markets. Morgan Stanley’s franchise flow data shows investors heavily long USD, particularly against EUR. MS expects downside USD risk if Warsh comes in less hawkish than expected, though their own forecast is that he strikes a middle ground. UBS has speculative short-yen positioning at stretched levels, with USDJPY risks skewed to the downside if Fed expectations get repriced lower.

Gold is at $4,332, up modestly. BofA’s survey shows gold is now seen as fairly valued for the first time since February 2024, with the net overvaluation reading collapsing from 16% last month to just 1%.