Breakfast Bites: Hot Print, Cold Strait

April CPI accelerates, Iran sets impossible preconditions, and Trump lands in Beijing tonight.

Rise and shine everyone.

April CPI printed at 3.8%, with energy accounting for roughly 40% of the increase, and the bond market moved accordingly. The 10-year closed at 4.46%, 2-year yields added 3.6 basis points, and 30-year gilts briefly hit a 28-year high of 5.813% before catching a relief bid overnight.

Six weeks of equity gains absorbed most of the shock. SPX finished down just 0.2% after recovering sharply from an intraday low that had NDX off more than 2%, and 51% of SPX names ended the day in the green.

Morning Macro Briefing

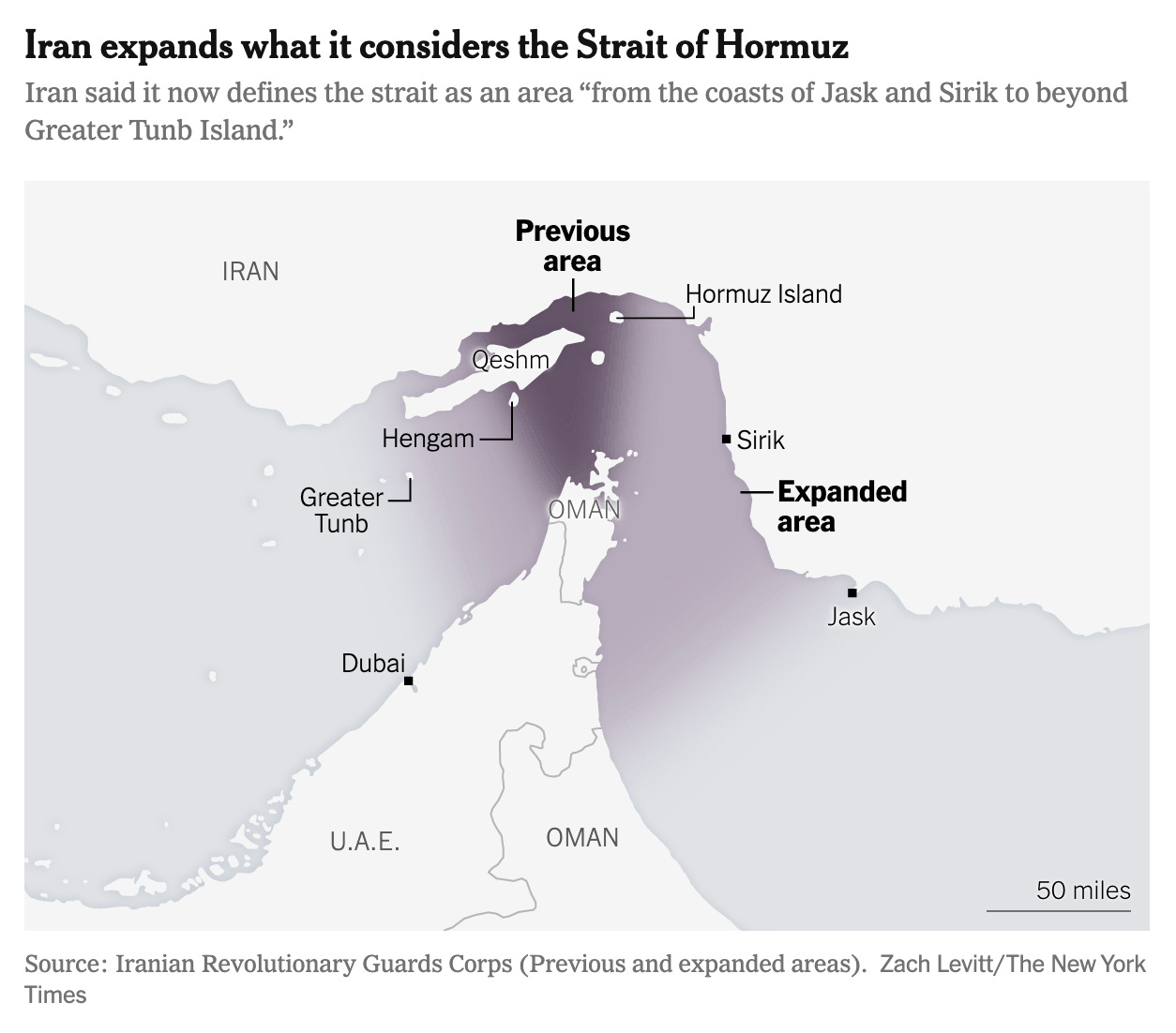

Ten weeks into the Iran war, the Strait of Hormuz has become something closer to a contested maritime battleground than a shipping lane. CENTCOM has now redirected 65 commercial vessels and disabled four ships under the American blockade, with three more redirected since Monday alone.

Iran unilaterally expanded its definition of the Strait this week, from roughly 20-30 miles to more than 200-300 miles, stretching from the coasts of Jask and Sirik to beyond Greater Tunb Island. Both sides now assert jurisdictional authority over the same water.

Windward’s Ami Daniel is tracking a 600% rise in dark activity, with vessels going dark on both transponders and collision-avoidance radars as hundreds of IRGC patrol boats patrol the expanded zone. Some operators are trying to thread the needle by routing through Iranian waters and paying Tehran’s toll system, a workaround OFAC warned this week carries sanctions exposure. The Greek-managed Agios Fanouris I did exactly that, clearing the Strait with Iranian permission before CENTCOM turned it around near the Gulf of Oman.

One signal worth watching on the pressure side is a surge in inbound empty Iranian tankers. Windward’s Daniel reads this as Tehran rushing in storage capacity while exports are blocked, suggesting the American strategy of filling Iranian storage to force well shutdowns may be starting to bite. Kharg Island shipments remained idle this week, which accelerates that pressure.

Fars News Agency confirmed Iran’s five preconditions for talks on Tuesday: ending the war on all fronts, lifting sanctions, releasing frozen funds, compensating for war damages, and accepting Iranian sovereignty over the Strait. JPM’s desk notes the last two conditions feel particularly difficult for the US side to accept, making a near-term deal unlikely.

President Trump lands in Beijing tonight ahead of Thursday’s 10:15 am local time summit with Xi. The likely shape of any agreement is an extension of the existing trade truce alongside Chinese commitments on US agricultural products, energy, and Boeing, with a Board of Trade mechanism floated as the structural vehicle. Xi is expected to push for harder US language on Taiwan in return.

Pre-summit speculation that Jensen Huang would skip the trip was put to rest by Trump confirming the Nvidia CEO was on Air Force One alongside Musk and Cook. Any signal of softening on chip export restrictions would move the semiconductor complex immediately.

The Iran angle is what gives this summit more weight than the trade issues alone. The working theory is that Beijing could lean on Tehran to reopen Hormuz in exchange for US de-escalation, giving Trump a way out before summer driving season turns pump prices into a domestic political problem. Trump downplayed the Iran dimension this week, and Beijing has so far stayed carefully out of the conflict, but the incentive structure is visible to everyone in the room.

April CPI printed at 3.8%, with energy driving roughly 40% of the increase and shelter surprising to the upside. Core ex-shelter was a more moderate 0.19% month-on-month, though core services ex rent and OER ran at 0.45%, well above the trailing-year pace, with goods the main restraint as used and new vehicle prices, apparel, and medical goods all declined. Core PCE is estimated at 0.23% month-on-month, putting the year-over-year pace at 3.2% to 3.3%, and while the Fed’s transitory framing on energy holds for now, one more accelerating print and the bond market stops looking through it entirely.

The rates pain spread across the Atlantic. European yields spiked on the combination of higher oil and the US print, with 2-year gilts adding 8 basis points and bunds 7 basis points over the past two days. Thirty-year gilt yields touched a 28-year high of 5.813% before catching a relief bid this morning, with the 10-year pulling back to 5.057% as Starmer’s position stabilized after 103 Labour MPs signed a letter of support.

Japan’s 10-year JGB yield rose to 2.575%, the highest since May 1997, as the global rates backup extended into Asia. The probability of a BOJ hike in June has moved to 76.5%.

And finally, Kevin Warsh was confirmed to the Federal Reserve Board, though the vote on the Chair position remains pending. His presence on the Board before the Chair confirmation is its own signal for front-end rates at a moment when they are already moving.

Chart of the Day

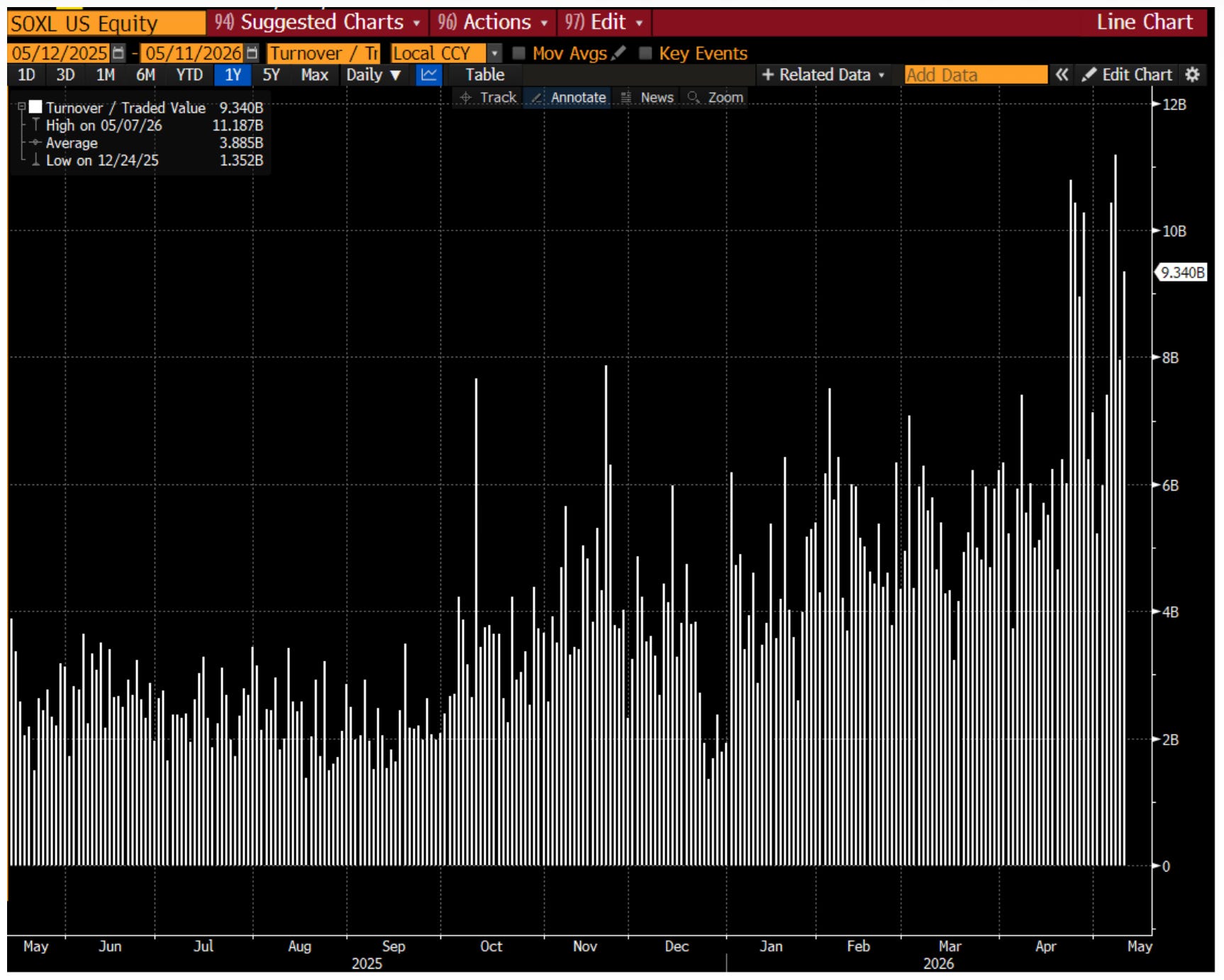

SOXL traded $9.5 billion in value on Tuesday, roughly $30 billion in underlying notional, against a prior-year daily average of $3.9 billion. The semi trade has structurally transformed into something retail-levered and momentum-driven, where a single session of hesitation produces moves that clean delta-one positioning simply does not reproduce. Goldman called Tuesday a digestion, not a reassessment, and the buyers who came back in the afternoon did so with conviction.

Calendars

Market Prep

US futures are up 0.2% to 0.4% in Asia trading as this session opens, recovering after Tuesday’s pullback. SPX finished -0.2%, NDX -0.9%, RTY -1.0%, with WTI at $102.43, the 10-year at 4.46%, and VIX at 17.99.

The structure of Tuesday matters more than the headline loss. Goldman’s high-beta momentum basket fell 4.71%, a day after its best session since 2021. The long leg of momentum, highly correlated to semis, dropped 5.2%, with memory stocks off 7.5%, AI inference beneficiaries down 6.5%, and data centers down 5.35%.

Goldman’s desk identified five dynamics driving the semi selloff: a proliferation of levered ETFs with exploding notional volumes, heavy retail engagement in a narrow group of names, explicit momentum factor trading, increased short covering as the notional value of short positions has grown, and asset manager flows rotating into 12-month AI winners while selling 12-month losers. When that bid hesitates, the move is fast.

The buyers came back in the afternoon with real size, and JPM’s desk agrees the pullback was positioning-driven rather than fundamental. Tuesday was a flush, not a reassessment.

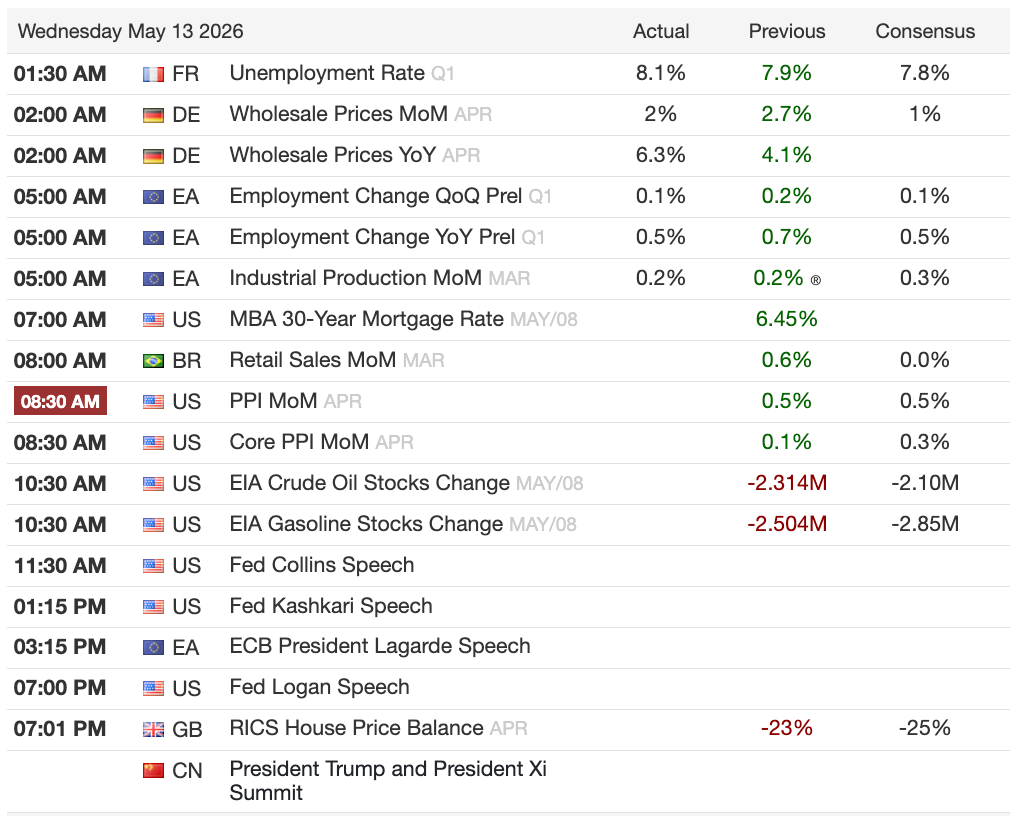

Watch three things today. PPI at 8:30am ET is first: a hot print following Tuesday’s CPI is what stops the bond market from looking through the Iran inflation premium and starts the conversation about whether the June FOMC meeting is live.

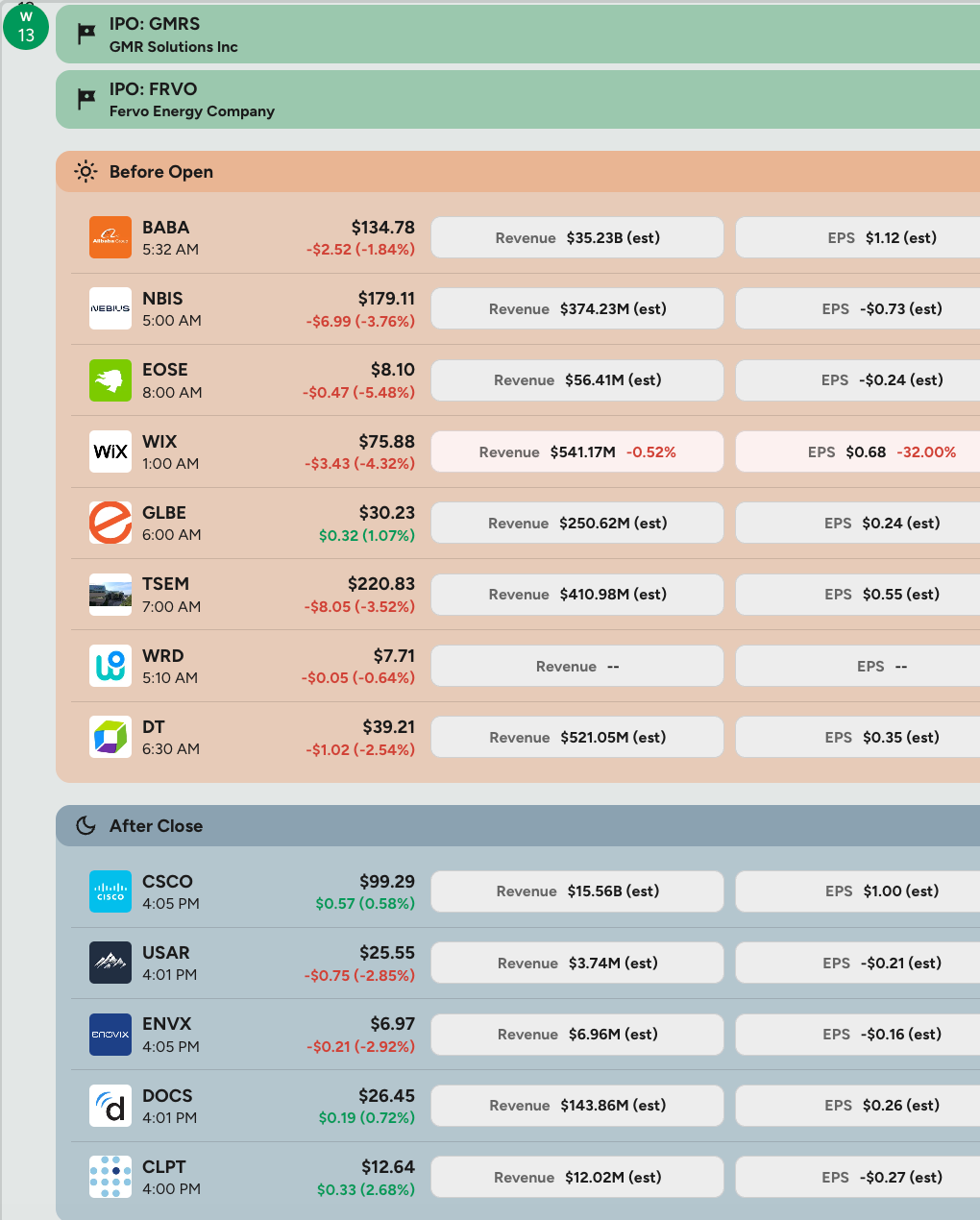

CSCO after the close is second, where management’s tone on AI infrastructure demand and memory cost guidance matters more for the tape than the earnings per share figure. Investors are modestly short into the print, according to JPM, with positioning at -2 on a -5 to +5 scale, and an implied move of 5.7%. Memory costs are the central debate, with management already taking some price and exploring de-specification options, while the Splunk transition and security business trajectory divide the bulls and bears. What matters most is not whether they beat but what they say about AI infrastructure demand, because after Tuesday’s semi wobble, this call gets read as a verdict on whether that was a pause or a preview.

Third is the dollar and rates: Goldman’s divided dollar thesis holds only as long as energy shock concerns stay in the background, and any further deterioration in the Strait picture pushes us toward the scenario where the trade-weighted dollar starts moving in ways that matter for positioning.

My Take

Tuesday’s session told you a lot about where this market stands. The headline loss was small, the afternoon recovery was genuine, and the buyers who stepped back into semis did so with real size.

The problem is that Iran’s five preconditions landed on the same day CPI moved yields, and together they paint a picture of a market running on two assumptions that are starting to pull against each other. The AI capex trade needs rates to stay cooperative, and rates stay cooperative only if the energy shock stays contained, and right now neither of those things looks certain.

I am skeptical Beijing produces anything meaningful on Iran. Trump downplayed the Iran dimension himself this week, and Tehran’s five preconditions are not an opening bid, they are a closing position.

PPI this morning is the number I am watching most closely, because if it runs hot, the transitory framing on energy inflation starts to crack and rate hike odds move in a way this market is simply not priced for. CSCO after the close is the second test, where the back-half guide on AI infrastructure demand will tell us whether Tuesday was a pause or a preview.