Breakfast Bites: Hormuz Is Running the Tape

Iran’s Strait of Hormuz saga dominates the week’s open, Chair Warsh’s hawkish FOMC debut reshapes rate expectations, and PCE inflation Thursday is the data event of the week.

Rise and shine everyone

The Strait of Hormuz is running the tape this morning. Iran announced Saturday it would re-close the waterway, futures fell 1%, and Sunday morning in Switzerland nearly ended in disaster when Iran’s delegation walked into the room, greeted the Pakistani mediators, and walked straight back out without acknowledging the US side. Markets recovered when Qatar and Iran confirmed the teams had ultimately met separately and made progress, with Aragchi confirming the blockade had been lifted.

I would not call this resolved. Trump has threatened to “hit Iran very hard again, only harder” if Hezbollah continues its attacks on Israel, and Sunday’s tracking data showed only around five vessels transiting the Strait. The ceasefire framework is holding, but just barely.

Here is what we are watching this week:

Whether the Strait of Hormuz stays open and whether the Switzerland talks can produce a durable framework before Trump’s patience runs out

PCE inflation on Thursday, where Goldman estimates headline at +4.04% YoY, a print that will validate or complicate Warsh’s hawkish setup

FedEx reports Tuesday and Micron reports Wednesday, giving us real-time reads on global logistics demand and AI memory capex

Morning Macro Briefing

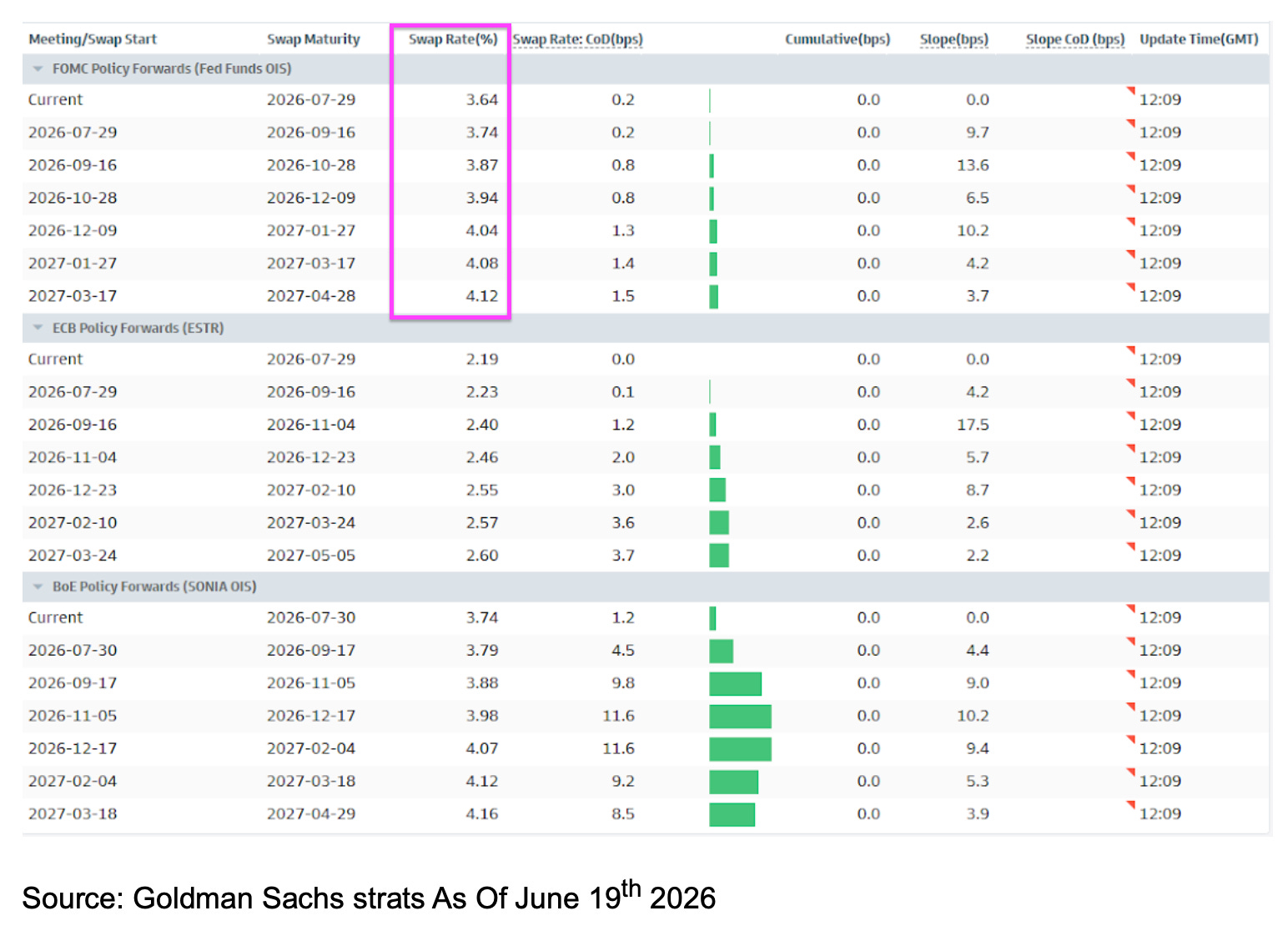

The Fed’s posture is now the cleaner of the two macro forces. Warsh’s first FOMC was distinctly hawkish, and the OIS forward curve repriced on both the 2pm statement and Warsh’s 2:30pm press conference. Goldman estimates core PCE at +3.38% YoY for May and headline at +4.04% YoY, neither of which is compatible with any near-term pause.

Fed speakers this week are worth watching. Waller speaks this morning and has said he is “prepared to be patient” but would not hesitate to hike if expectations become unanchored. Williams believes policy is “exactly in the right place.”

Goolsbee says inflation “is getting worse.” Kashkari has called hiking premature. The divergence matters when PCE lands Thursday.

The BoE held 7-2 and UK CPI came in soft, with around 50bp of conflict-related inflation still priced into 1-year RPI expected to unwind. The ECB is maintaining a tightening bias as inflation insurance even as oil has retraced.

Goldman’s Brent target is now $80 for Q4 2026 and $75 for 2027. Managed Money sold nearly $25bn of crude over the past seven weeks, with outright shorts at new highs. Investors closed the book on geopolitical oil risk quickly.

The BOJ is worth a line. October hike odds rose to 60% from 52.5% last Thursday, and the Nikkei touched a record above 73k. In Korea, SK Hynix briefly overtook Samsung by market cap and KOSPI closed above 9,000 for the first time.

PM Starmer has announced his resignation today. This is the UK’s sixth PM change in ten years. Gilts are little changed, and the GBP is down about 0.1%. Andy Burnham is expected to be the successor and in office by September, if there are no challengers.

China’s tape is weak, with e-commerce names selling off on soft 6.18 data and HSCEI down nearly 20% from October highs. BofA data shows twelve consecutive weeks of China equity fund outflows, with $9.1bn out last week alone.

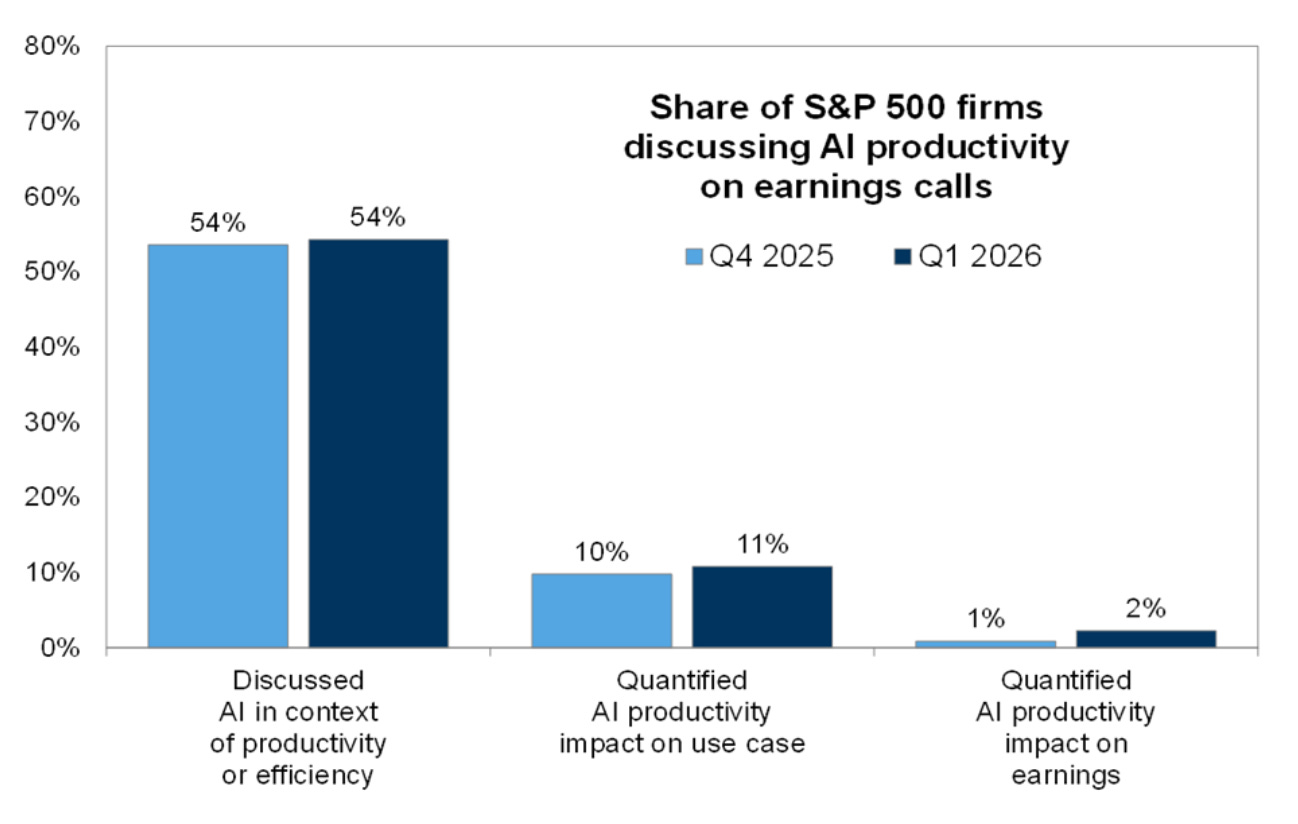

Chart of the Day

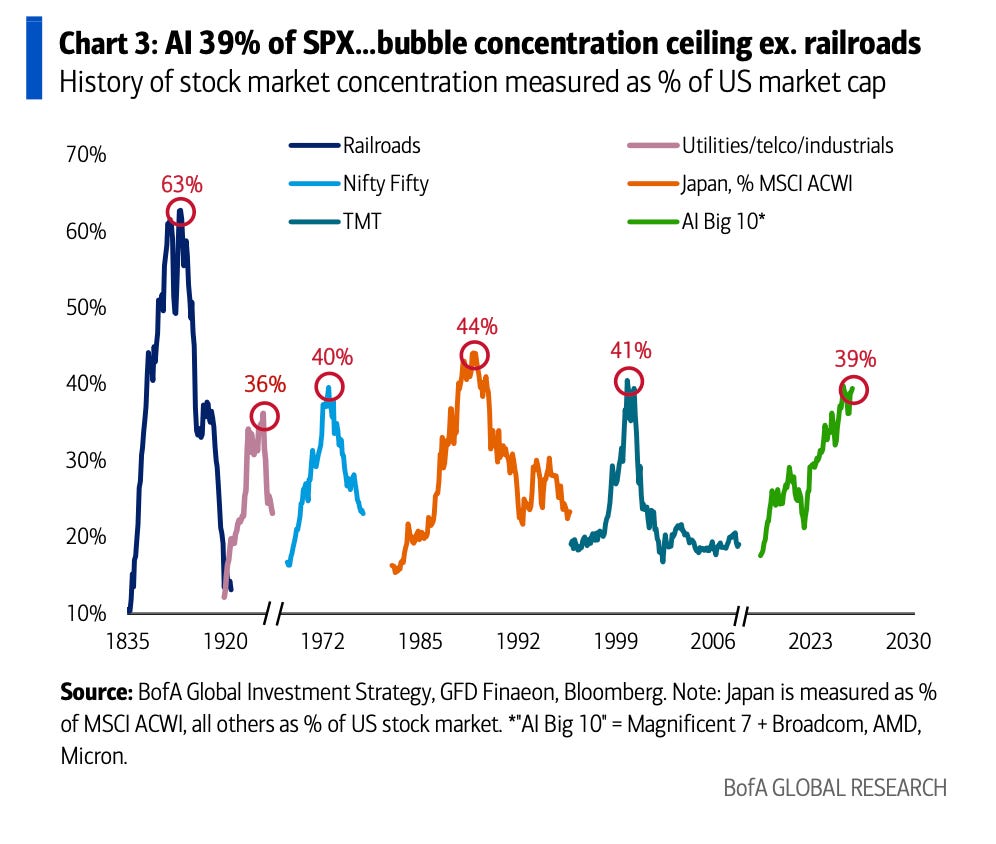

54% of S&P 500 companies are discussing AI productivity on earnings calls, 11% have attached a use case, and only 2% can quantify the actual impact on earnings. The bulls read this as early innings. The bears read it as evidence that the market is pricing outcomes not yet in the numbers.

I keep coming back to that 2% figure. If it moves meaningfully toward 10%, the entire valuation framework for this market looks different.

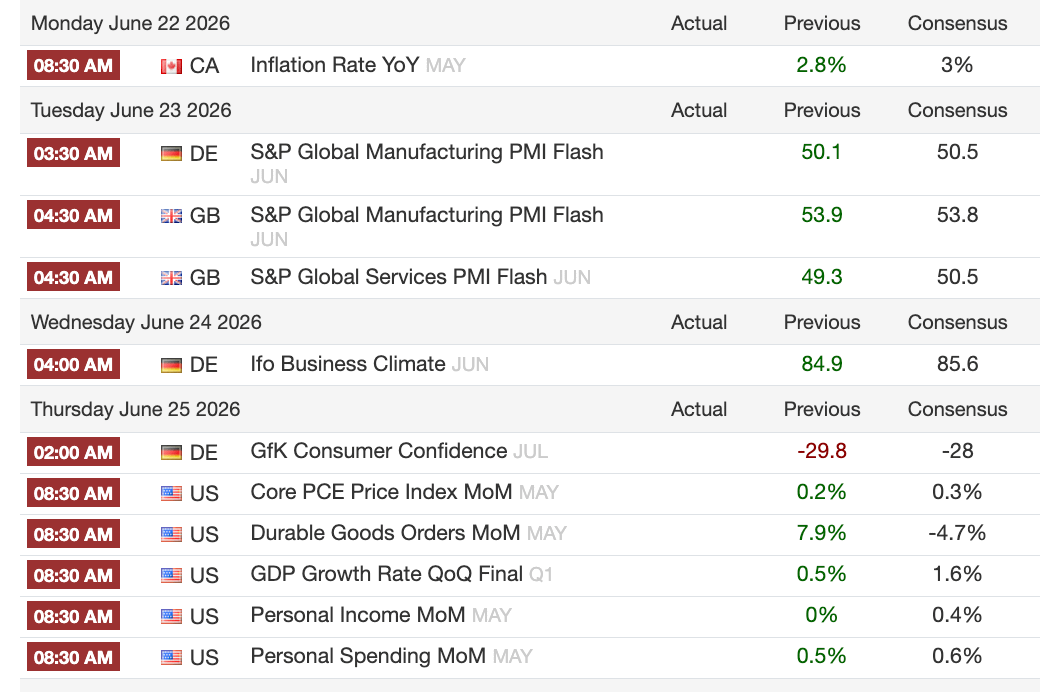

Calendars - The Week Ahead

This is a meaty week for data. Thursday is the headline event, with PCE inflation, the Q1 GDP third release, personal income and spending, durable goods, and jobless claims all at 8:30am ET. Goldman estimates headline PCE at +4.04% YoY and core at +3.38% YoY.

Flash PMIs hit Tuesday, and Fed speakers run all week with Waller today and Kashkari Friday.

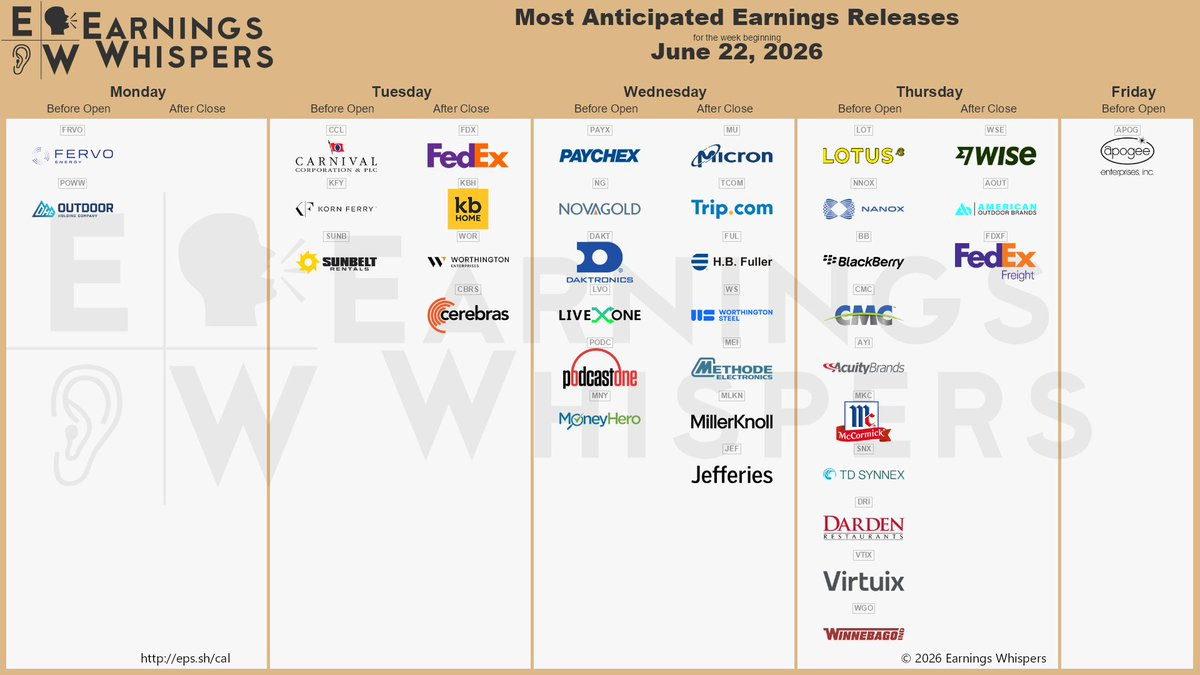

On earnings, FedEx reports Tuesday and Micron reports Wednesday. FedEx gives a read on global logistics demand, while Micron is the real-world test of whether the Semis allocation story has fundamental support or is running on narrative alone.

Market Prep

US equity futures opened Sunday down 1% on the Iran headlines and recovered to roughly flat by the Asia close. The Nikkei gained 2% to a record above 73k. Korea swung more than 1% intraday while the Hang Seng underperformed at -0.8%.

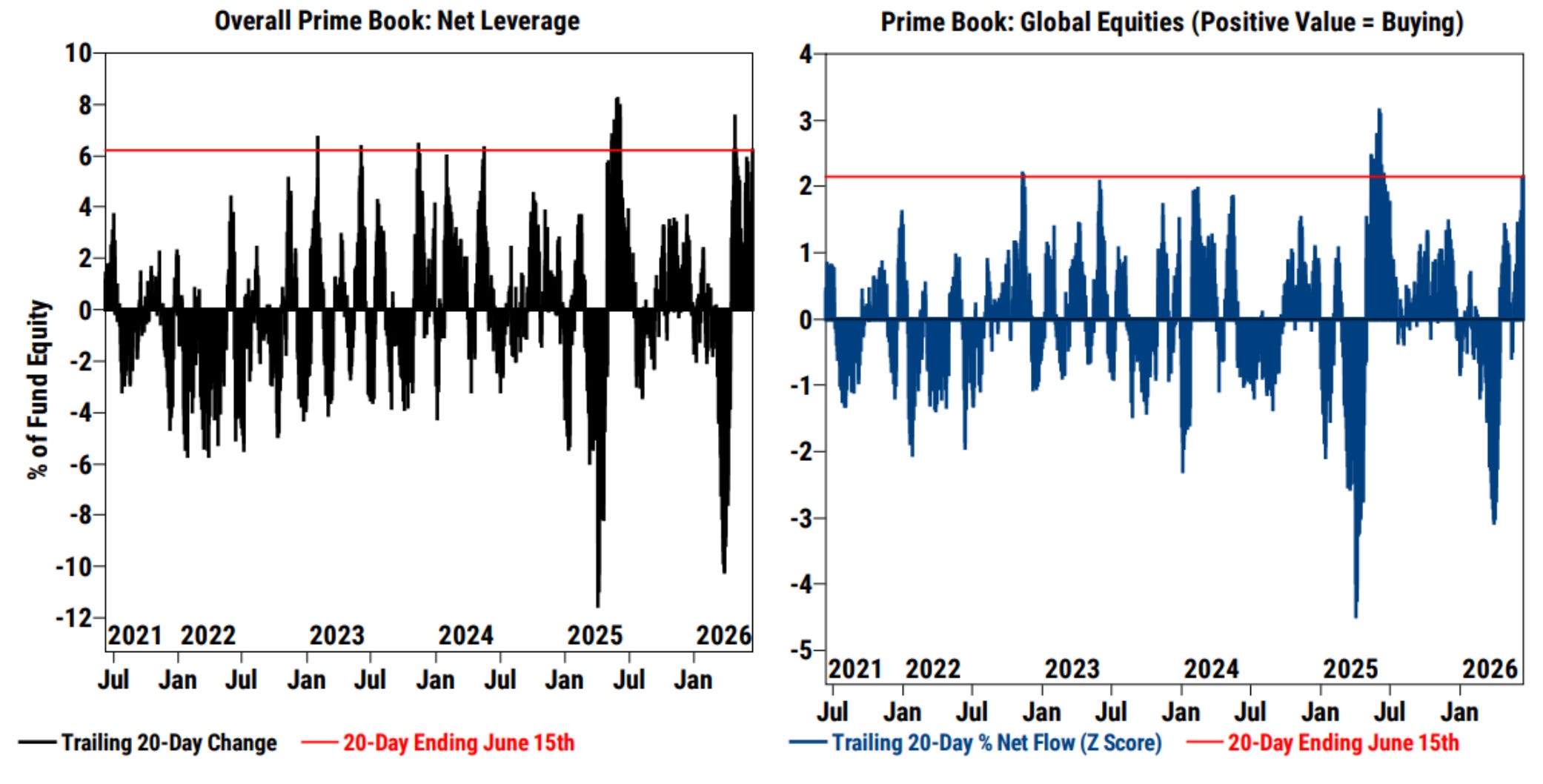

The positioning picture is uniformly stretched. Goldman’s prime book shows gross and net equity exposure in the 97th percentile of the past three years, with its positioning gauge at +8 out of +10 matching the January highs. Global hedge fund net leverage has hit four-year highs, the market absorbed $125bn of new equity issuance in under two weeks and kept moving higher, and BofA recorded a weekly US equity inflow of $119.2bn.

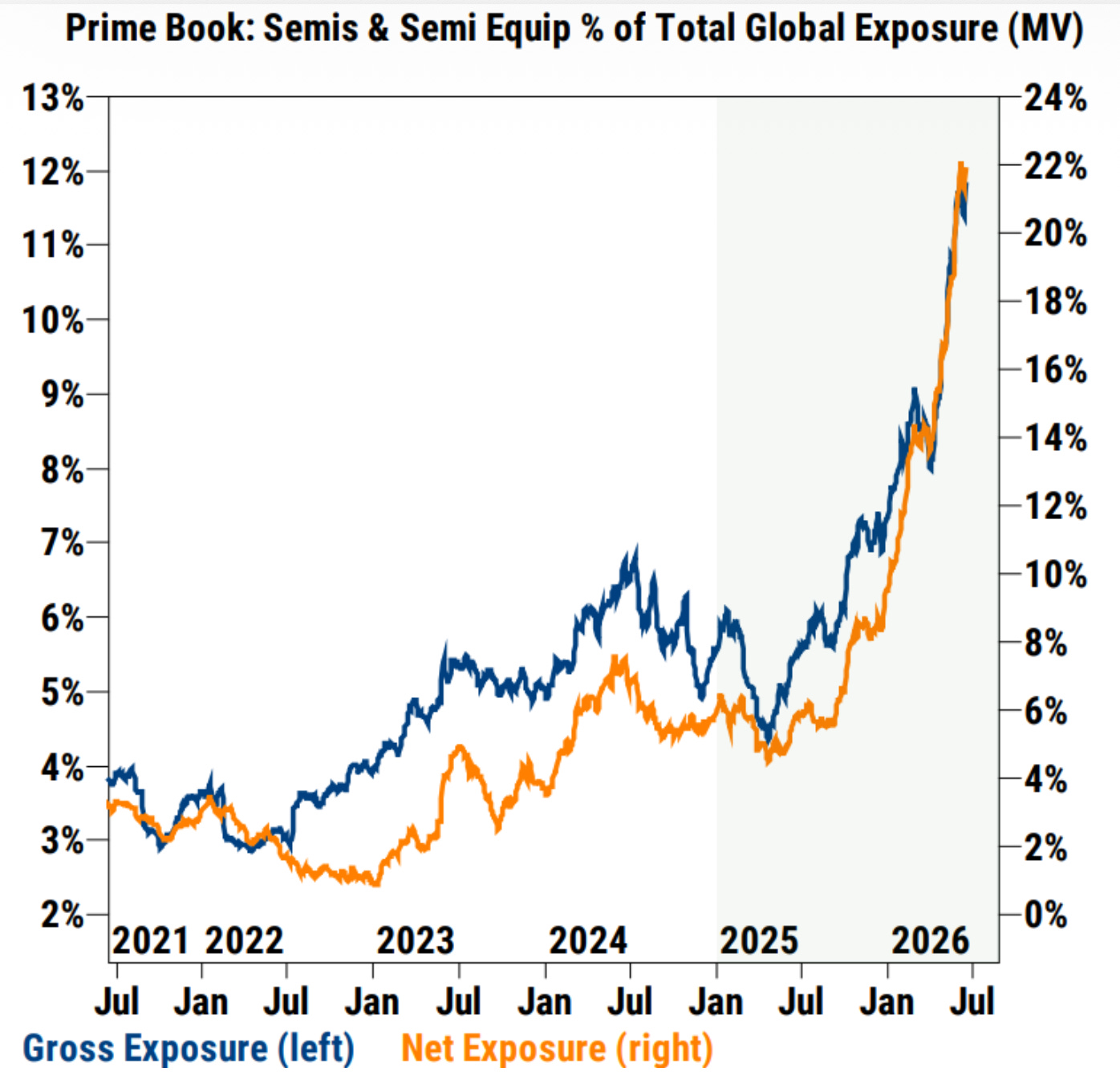

The rotation beneath the surface is real. While overall US tech exposure is near five-year highs, Mag 7 gross and net exposure has fallen to one-year lows as investors rotate into Semis and Asian chipmakers. Goldman’s prime book shows Semis on pace to be the most net bought global subsector for a second consecutive year.

BofA’s sell signal at 9.2 historically produces 2 to 3% losses in global equities over two to three months with a ~60% hit ratio. Alongside 97th percentile positioning and record inflows, this market is long, leveraged, and concentrated in one theme.

Three things will define the week. First, whether Iran holds the Strait open, because any re-escalation immediately reprices oil and risk sentiment. Second, Thursday’s PCE print, where a headline above +4.04% puts a September hike firmly on the table.

Third, what Micron says on Wednesday. That call is the clearest real-world test of whether the Semis conviction is grounded in order books or runs ahead of them.