Breakfast Bites: Freedom, Tariffs, and Payrolls

Trump launches Project Freedom at the Strait of Hormuz, reopens the EU trade front, and the April jobs report arrives Friday.

Rise and shine everyone

The week opens with oil markets in a tug of war, and two geopolitical fronts suddenly live at once. President Trump announced overnight that the US would begin coordinating ship passage through the Strait of Hormuz under what he is calling Project Freedom, backed by 15,000 service members, guided-missile destroyers, and aircraft. Crude oil gapped down roughly 3% on the Asian open, ground nearly all the way back, then fell again toward opening levels as markets waited for Iran’s formal response. The WSJ clarified that US Navy ships will not physically escort vessels but rather serve as a coordination mechanism for shipping organizations and insurers. That distinction matters. A coordination mechanism is not a ceasefire, and it is not an open strait and Iran has not said yes.

While everyone was watching Hormuz, President Trump dropped a separate bomb on Friday, posting that he will raise the tariff on imported EU cars and trucks from 15% to 25%, citing European non-compliance with a previously agreed trade framework. He referenced “next week” as the effective date, meaning we may see implementation as early as today. European officials pushed back quickly, though the European Auto Lobby directed pressure inward, urging EU lawmakers to finalize their own legislative response as fast as possible. This is a market that had largely moved on from the US-EU trade front. It has not moved on anymore.

Morning Macro Briefing

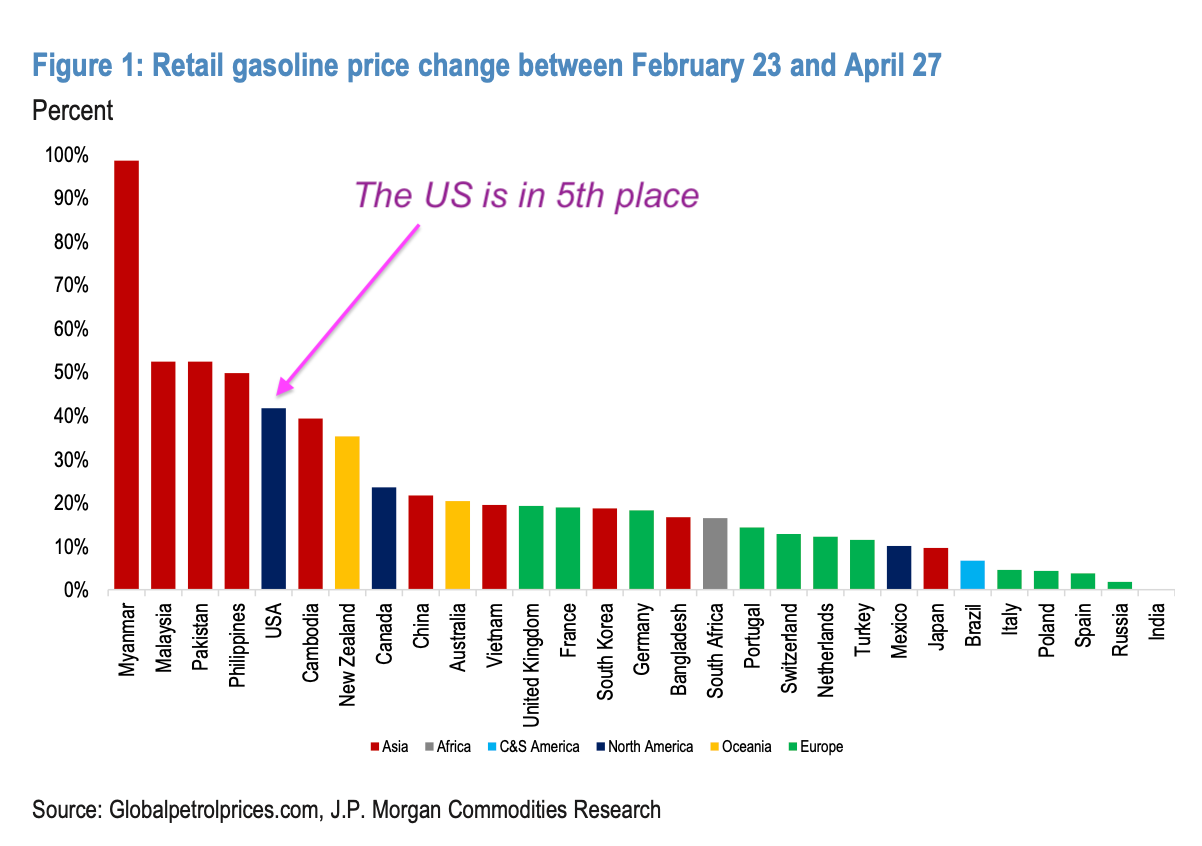

The energy picture has not fundamentally changed, but Project Freedom adds a new variable. JPM’s commodity team has been tracking the US as the second most affected region globally in refined product price terms since the conflict began. Retail gasoline is up more than 42% in the US from pre-war levels, surpassing most regions outside Asia.

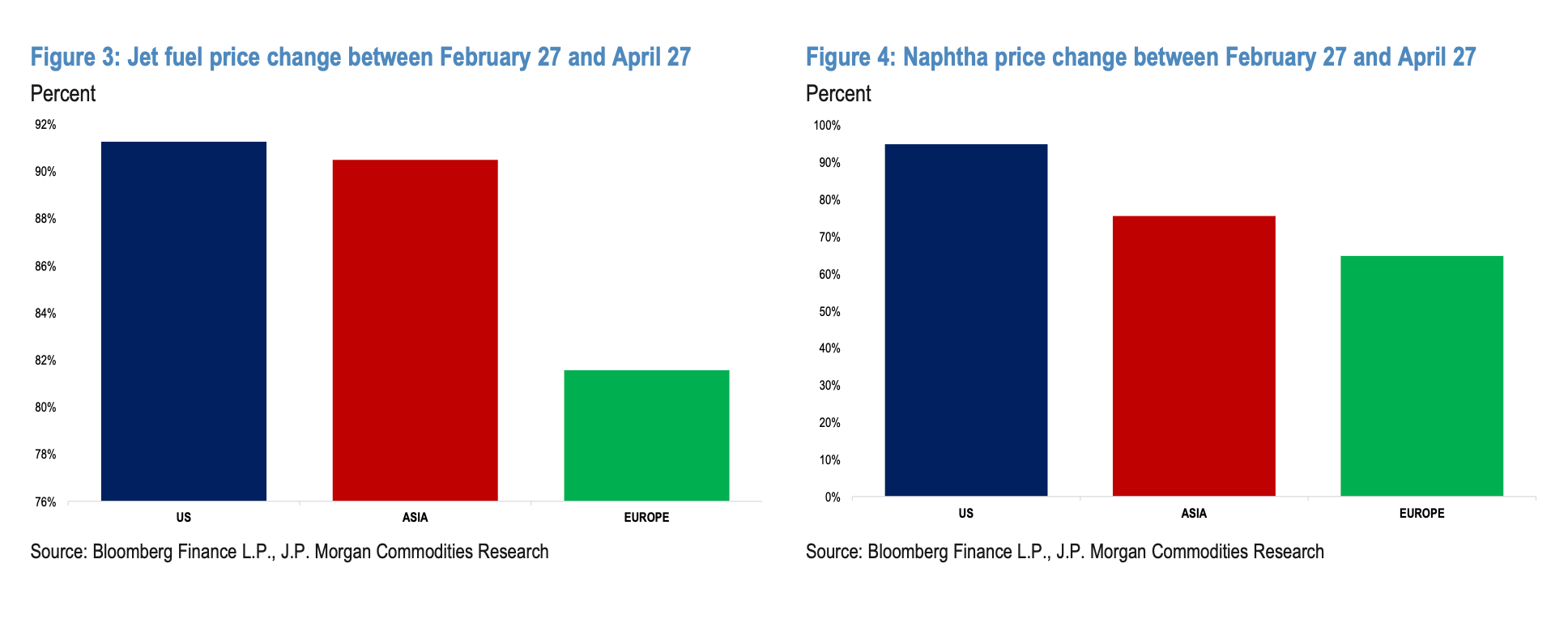

Jet fuel and naphtha are showing the largest US price increases globally. Inventories are being drawn toward critically low levels.

JPM’s commodity strategists now flag early June as the more likely timing for operational stress minimums, pushed back from an earlier May estimate.

The US enters this shock from a position of genuine underlying strength. 1Q GDP came in at 2.0%, with domestic final sales to private purchasers rising 2.5%, right in line with 2025’s average.

Labor data heading into Friday also looks constructive. Initial jobless claims fell to their lowest level since 1969 in the week ending April 25. Continuing claims are at their lowest since mid-2024. April PMI and ISM manufacturing composites hit cycle highs. The caveat is though, is both surveys flagged front-loading as a partial driver, and price indexes are surging. The ISM prices sub-index is back near post-COVID highs at 84.6. Supply delivery times are lengthening. What looks like demand strength today may in part be inventory accumulation ahead of feared supply disruptions.

Berkshire Hathaway reported Saturday: operating earnings up 18%, revenue beat, headline earnings missed. New CEO Greg Abel has a short list of acquisition targets. Buybacks resumed at $234-235mn in March and April, well short of the $2-3bn some had expected, leaving cash and short-term securities at a fresh record $397.4bn. Berkshire holding nearly $400bn in cash while the world argues about oil is its own kind of statement.

Chart of the Day

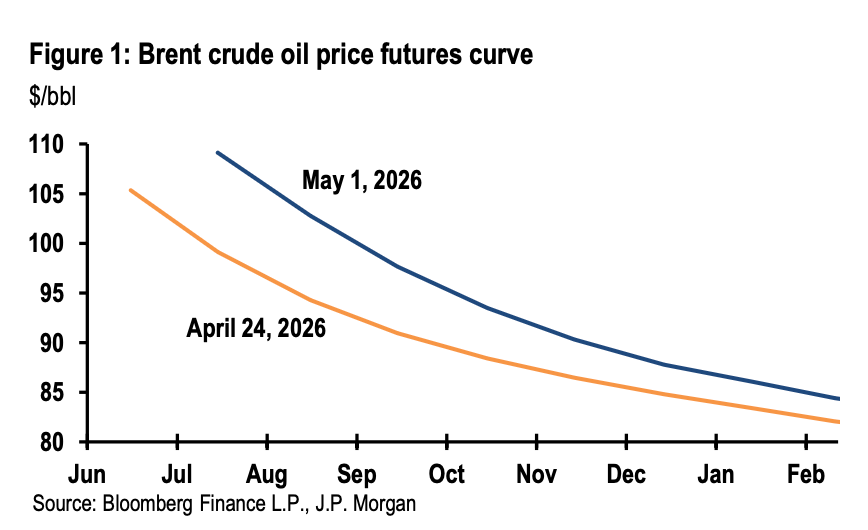

This chart tells an interesting story. The forward curve has steepened meaningfully over the past week, with the July contract spiking to an intraweek high of $115 before settling back to $108, while December Brent remains anchored near $88. Markets are still pricing resolution, but that mid-curve spike shows how quickly sentiment can shift when inventory draws are this aggressive and diplomacy stalls. Project Freedom has introduced a new variable this morning, but until Iran responds and ships start moving, the curve should not be taken as complacency.

Calendars: The Week Ahead

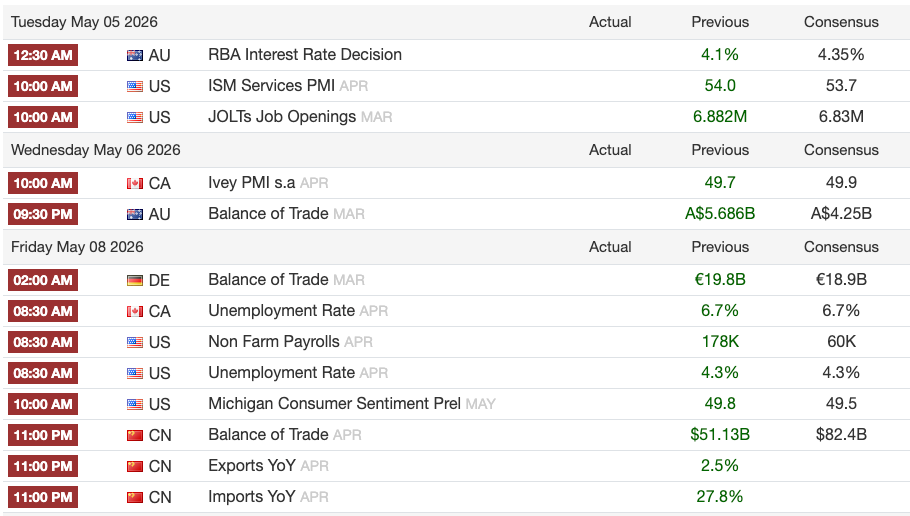

Tuesday: ISM services (JPM: 54.0, unchanged), JOLTS, new home sales, trade balance, plus Bowman and Barr speaking; RBA expected to hike 25bps to 4.35%

Wednesday: ADP employment (Goldman: +170k, well above consensus of +120k)

Thursday: Preliminary 1Q productivity (JPM: +0.6%), initial claims, Kashkari and Hammack speaking; Banxico (Mexico) expected to cut 25bps to a neutral 6.5%

Friday: April nonfarm payrolls (JPM: 50k, Goldman: 75k); unemployment rate (JPM: 4.2%, Goldman: 4.3%); average hourly earnings (both houses: +0.3% m/m)

Market Prep

The Kospi powered to fresh record highs today, up 4.5% after Friday’s holiday, with SK Hynix surging 11% and crossing KRW1,000 trillion in market cap for the first time. The AI bid in Korean semiconductors is not subtle. Japan’s Nikkei is closed through Wednesday and China’s mainland exchanges through Tuesday.

US equity futures are up 0.2% to 0.4% in Asian trading, a notably composed reaction given the two open geopolitical fronts. The crude gap-and-recover overnight is worth watching closely at the US open. Markets appear to be treating Project Freedom as a partial positive, enough to pare the oil risk premium at the margin, without fully pricing a resolution. That is probably the right read for now, but Iran’s response changes the calculus entirely.

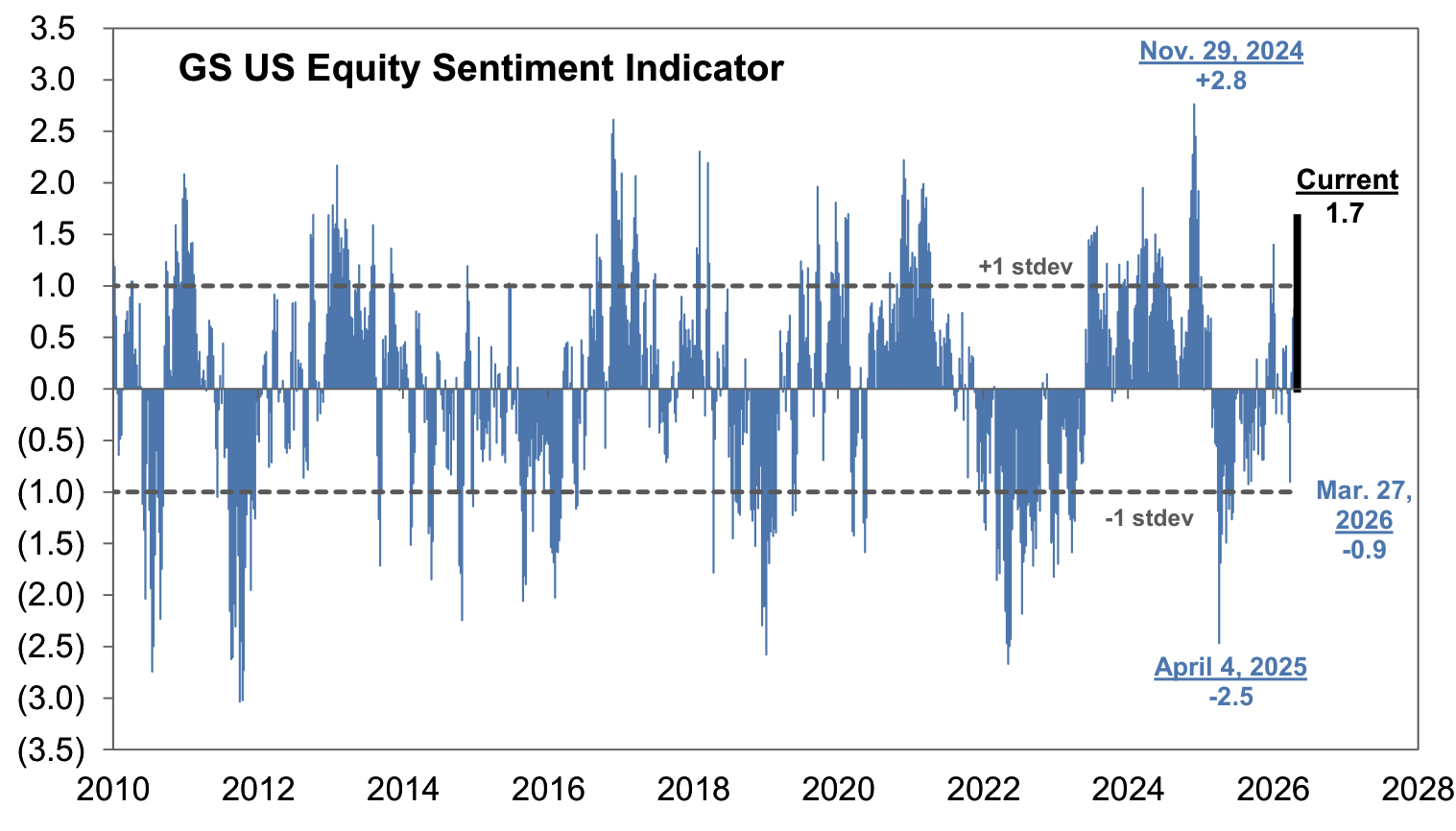

Goldman’s US Equity Sentiment Indicator rose to 1.7 last week, the highest reading since late 2024, driven by passive equity fund inflows and declining mutual fund cash balances. Readings at this level have historically preceded below-average S&P 500 returns over the subsequent two to eight weeks, with 1-month forward returns averaging -0.4% since the GFC when the indicator sits between 1.5 and 2.0. The S&P 500 itself is up 6% year-to-date, with Energy (+33%) and Communication Services (+10%) leading, while Healthcare (-5%) and Financials (-4%) lag. The index currently trades at 21x forward earnings, at the 63rd percentile of its 20-year history.

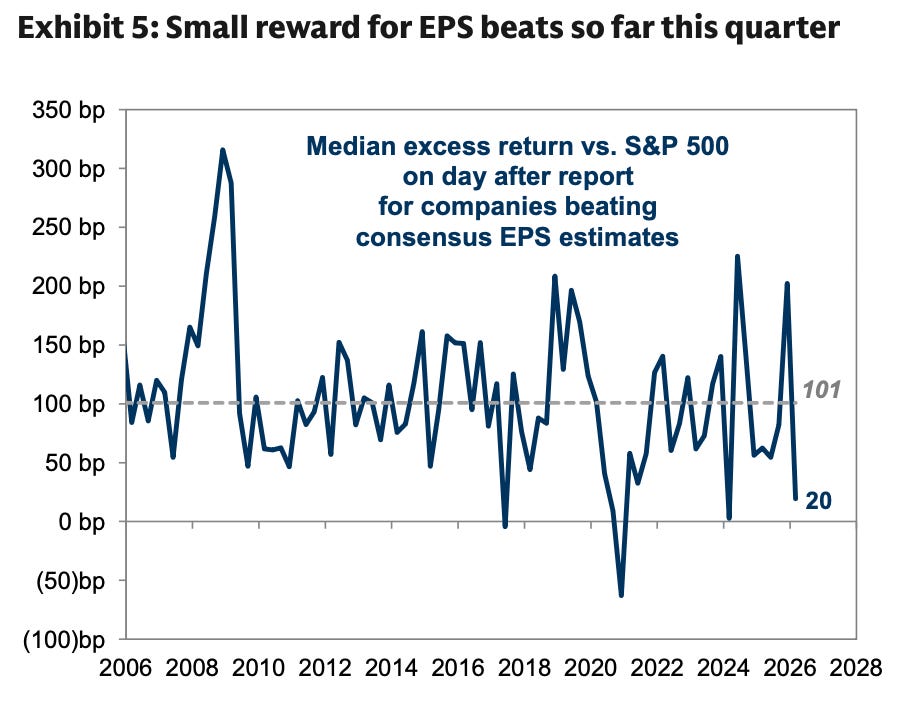

With 63% of S&P 500 companies having reported Q1 results, the earnings season has been exceptionally strong by the numbers. EPS growth is tracking at 25% year-over-year in aggregate, or 16% excluding one-time items, the strongest quarterly pace since 2021. Only 5% of companies have missed estimates, the lowest miss rate in 25 years outside the COVID reopening. The catch is that the reward for beats has been unusually thin: the median stock beating consensus outperformed the index by just 20 basis points on its report day.

Management commentary is increasingly flagging commodity input cost pressure, analysts have trimmed Q2 margin estimates across most sectors, and many consumer names have yet to report.

The week-ahead positioning setup is skewed by a data-heavy Friday that will pull attention forward. The jobs number lands into a market where the FOMC has explicitly moved toward a neutral bias and three dissenters want the option to hike. A weak payroll print does not buy the Fed much room given where inflation is sitting; a strong print removes any residual cut pricing for 2026. Watch the unemployment rate and average hourly earnings as much as the headline. JPM and Goldman both expect 0.3% month-over-month on earnings, which would push the year-over-year rate back to 3.8%.

My Take

The oil market’s reaction to Project Freedom this morning is informative but let’s remember that a coordination mechanism is not a convoy and Iran has not said yes. The gap closed quickly not because the strait is opening but because the announcement changed the tail risk calculus slightly at the margin. I would not be positioning for resolution on the basis of a press release.

The EU tariff escalation is the development that strikes me as more immediately underpriced. Markets had moved on from the US-Europe trade front. The auto tariff hike from 15% to 25% reopens it, and this week may be the implementation window. European equities and EUR have a lot of catching up to do if this lands.

The three things to watch this week are Iran’s formal response to Project Freedom and whether any vessels successfully transit Hormuz, the EU auto tariff implementation date and any retaliatory moves from Brussels, and Friday’s jobs report, which is genuinely hard to call at this point.