Breakfast Bites: Fragile Ground

Iran deal in the balance, PCE on Thursday, and Central Banks done being patient.

Rise and shine everyone

We’re back from Memorial Day and walking straight into one of the messier setups of the year. Three things will define this week:

The Iran ceasefire is under active stress. New strikes resumed overnight, a deal framework exists but the critical details are unresolved, and the Strait of Hormuz remains disputed.

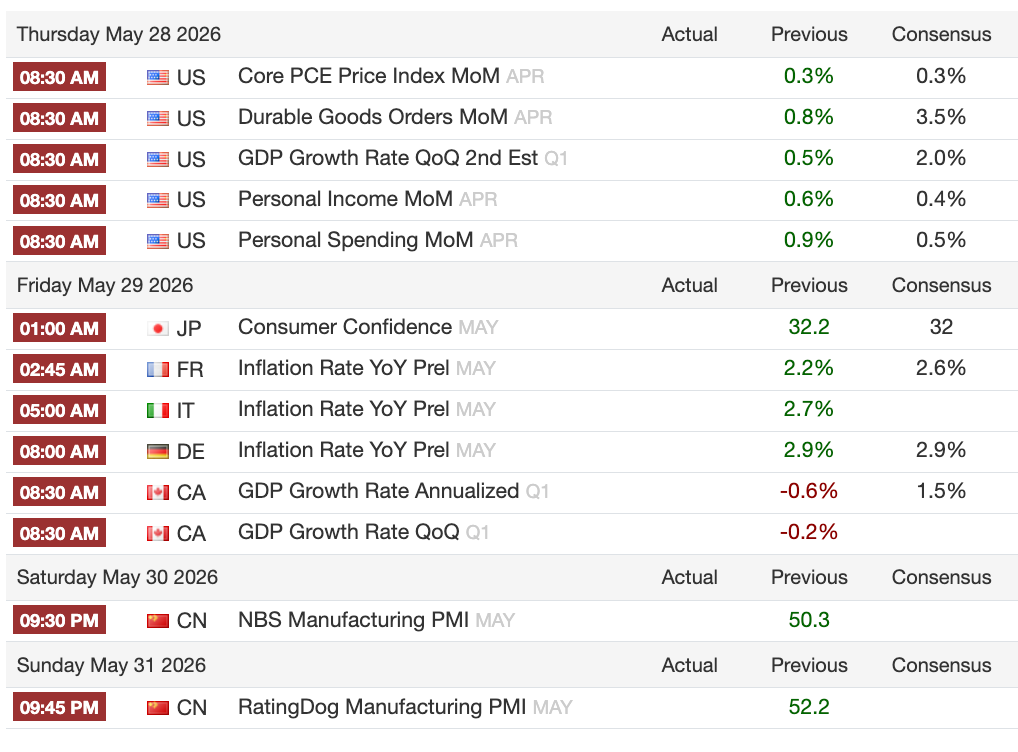

PCE is out Thursday. We’re likely to see an uptick in core PCE to 3.31% YoY in April, up from 3.2% last month. That’s five consecutive years above target and counting, and both the Fed and ECB are now signaling that patience has a limit.

Positioning is still lopsided. Momentum exposure sits at historical highs, US flows are weakening, and HFs have been aggressively fading Energy in anticipation of a deal that isn’t here yet.

Major Earnings this week include - Snowflake, Salesforce, Costco. We also watching Zscaler, HP, Marvell, Dell.

The Monday gap higher is being unwound as CENTCOM struck Iranian fast boats and missile sites overnight, Iran downed a US drone in response, and both sides claimed the other violated the ceasefire. A deal framework exists, but the sequencing dispute between sanctions relief and uranium removal is exactly the detail that has killed these negotiations before.

The market has moved into the “deal is coming” trade, HFs have sold Energy hard, and yet the actual deal is not here. Conditions on the ground are deteriorating, not stabilizing. If this breaks, you have a very wrong-footed positioning picture in Energy and a commodity spike landing into a front end that is already pricing out cuts. That is not a comfortable combination.

The week is a test of two things simultaneously: whether the Iran framework holds long enough to become an actual agreement, and whether Thursday’s data gives the Fed hawks the ammunition they want. I suspect there will be failure of one of those tests.

Morning Macro Briefing

CENTCOM hit Iranian fast boats attempting to mine the Strait of Hormuz overnight and struck missile launch sites near Bandar Abbas. Iran downed a US MQ-9 drone in response. Both sides claim the other violated the ceasefire. The deal framework, as reported, includes Iran removing highly enriched uranium from its territory, a 30-day window for Hormuz navigation to resume, and a ceasefire extension beyond 60 days. Iranian officials have been deliberately vague on whether nuclear concessions are actually in the framework. Sec Rubio said talks will take a few more days.

The Bank of Korea meets Thursday. Thirty of thirty-two economists expect a hold at 2.50%. The RBNZ decides Wednesday with only a 20% probability of a hike priced. The Sri Lanka central bank surprised overnight with a 100bp hike, following Indonesia’s unexpected 50bp move last week. The pattern of larger-than-expected tightening from Asian central banks suggests the global inflation problem extends well beyond the US and Europe.

PM Takaichi confirmed a supplementary budget exceeding ¥3.0 trillion without issuing new deficit bonds. BOJ Deputy Governor Himino reiterated guidance that the bank will raise rates in response to economic and inflation developments, noting that rising long-term yields reflect global inflation concerns. Japan is separately pursuing an economic partnership with Mercosur targeting lithium and rare earths.

ECB’s Schnabel argued overnight that the ECB should hike in June even if an Iran deal emerges, citing persistent energy inflation and emerging second-round effects. This follows Waller’s hawkish pivot on Friday, where he said he could no longer rule out rate hikes if inflation does not abate. Both carry institutional weight and both are saying the same thing: the energy shock has become a structural inflation problem.

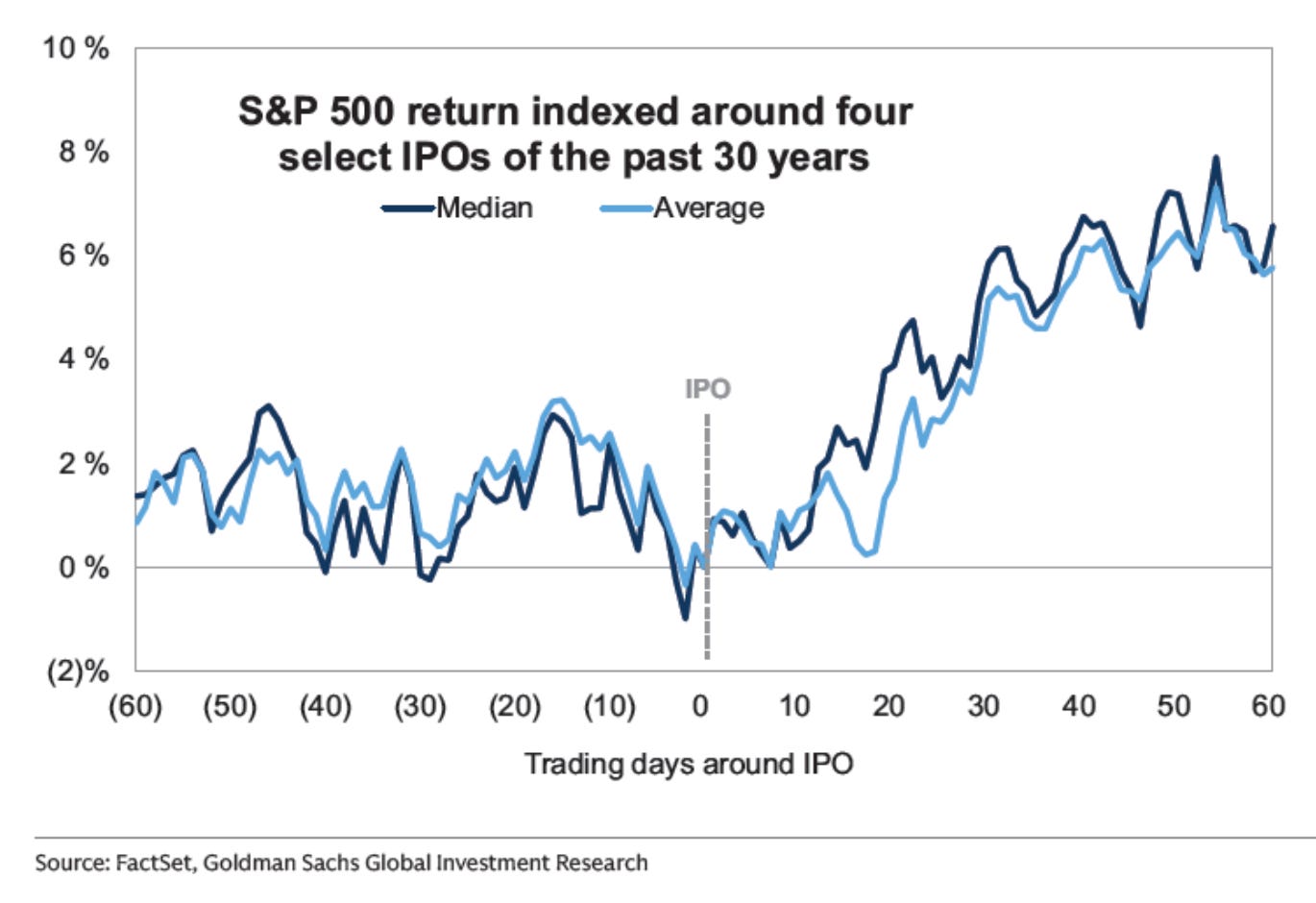

Chart of the Day

Goldman expects “roughly 100 IPOs totaling $160 billion will come to market in 2026.” But there’s some good news…

“Mega IPOs ≠ market pain. Historically the S&P 500 dipped 1% the month before mega IPOs (BABA, GM, META, V), then rallied 5% the month after — and HY credit moved similarly, suggesting macro (not IPO supply) was the driver. No evidence of Mega-cap selling pressure or Momentum factor selling (popular longs) around past mega IPOs.”

Calendars: The Week Ahead

This week effectively starts today. The calendar is front-loaded with Fed speakers and back-loaded with data. Thursday is the session that matters.

Data to look out for:

Tuesday: Conference Board consumer confidence (consensus 92.0, last 92.8) — the first sentiment read post-ceasefire announcement.

Wednesday: Logan and Jeferson both speak at the BOJ event. RBNZ decision.

Thursday: The day that matters. Core PCE (Goldman +3.31% YoY), headline PCE (+3.78% YoY), Q1 GDP second release, durable goods, and jobless claims. Bank of Korea decision.

Friday: Bowman, Paulson, and Daly all speak.

Market Prep

US stocks opened sharply higher on Monday after positive ceasefire headlines over the weekend. By Tuesday morning, most of those gains have been given back as the situation on the ground deteriorated overnight. Expect a choppy first session back — markets are digesting fast-moving headlines and traders are repositioning after a long weekend.

According to JPM’s prime brokerage desk, hedge fund positioning in the US has been quietly weakening. Funds reduced their overall exposure last week, and the trend over the past month has been consistently lower. In simple terms: the smart money is not adding risk right now.

The Iran deal is driving some very specific bets across sectors, and those bets are now quite stretched:

Energy and Oil Services stocks have been heavily shorted — funds are betting these fall if a deal removes the oil supply risk. If the deal collapses, those bets unwind fast and energy stocks could spike.

Airlines have been sold down since March — another deal trade, on the assumption that cheaper oil and reopened airspace helps carriers.

Building Products stocks have been bought aggressively — a play on post-conflict reconstruction activity. That trade is crowded.

Restaurant and Packaged Food stocks are among the most shorted in years. Funds are betting that high energy and food costs continue to squeeze these businesses.

Outside the US, South Korean and Taiwanese stocks are seeing strong buying from hedge funds and have been for weeks. That momentum looks intact. Japan, by contrast, is starting to see selling after its big recent run.

Three things to watch today: whether US futures stabilise or continue sliding; any new statements from CENTCOM or Iranian officials before markets open; and the consumer confidence reading at 10am, the first real data point of the week.